Anti-Migrating Agent Market Report Scope & Overview:

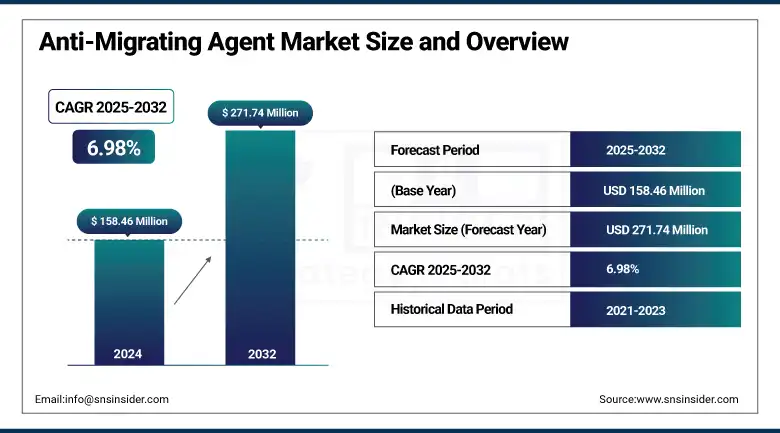

The anti-migrating agent market size was valued at USD 158.46 million in 2024 and is expected to reach USD 271.74 million by 2032, growing at a CAGR of 6.98% over the forecast period of 2025-2032.

The growing need for colorfast and high-quality textiles and coatings is propelling the demand for the anti-migrating agent market. These agents are preventers of the traveling of dye, nowadays more important in digital textile printing, where accuracy and brightness are of great importance.

To Get more information On Anti-Migrating Agent Market - Request Free Sample Report

-

For instance, the NTR Printing System, launched by Archroma in 2024 along with PRINTOFIX BLACK NTR-TF, made from 79% renewable carbon content, aims to drive eco-advanced printing.

Increasing environmental regulations are also driving the demand for green antimigrating additives. Increasing textile production in the Asia-Pacific, particularly in India, which saw textile and apparel exports of $35.87 billion in 2023 to 2024, is driving the market. Increasing application of dye migration inhibitors in the U.S. and Europe is also expected to boost the trend. The India Textiles Committee puts it that the ongoing high demand for chemicals will be the ongoing trend!

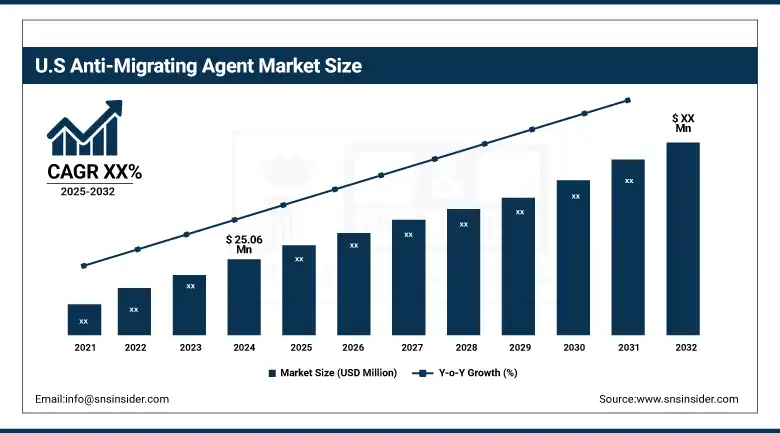

The U.S. is holding a market size of 25.06 million USD due to the growing demand for textiles and printing, with a market share of 70.6%. Growing eco-consciousness and strict environmental regulations, raised in part by companies like Dow and DuPont, are also pushing growth.

Market Dynamics

Drivers

-

Growing Demand for Eco-Friendly Solutions in Textile and Coating Industries Drives Market Expansion

The global trend of sustainability is driving market growth, as producers concentrate on using green additives that can help in inhibiting the dye migration in fabrics. Biodegradable, non-toxic solutions are encouraged by governments and organizations such as the Textiles Committee of India. This is particularly pronounced in the Asia-Pacific, where many of the world’s textiles are made. Enterprises like Archroma are at the forefront by offering environment-friendly anti-migrating solutions that are sustainable and in line with global industry standards, allowing them to gain significant market share with the growing awareness of environmental pollution.

-

Rising Adoption of Digital Printing Techniques Fuels Demand for Anti-Migrating Additives

The increasing adoption of digital printing within the textile industry is augmenting the requirements of anti-migrating agent additives. These additives maintain the stability of the dye and prevent migration during the printing process as manufacturers continue to push the envelope with high-performance and customized designs. The accuracy and versatility of digital printing mean dye migration inhibitors are simply a must for jobs that need accurate colour representation. The demand for the solution is also increasing due to technological developments in the field of textile printing. SNF Floerger is driving the trend of anti-migrating agent market with advanced additives developed for high-resolution, sustainable, and consistent digital textile production.

Restraints

-

Lack of Awareness Among Manufacturers About Anti-Migrating Agent Benefits

A low to moderate level of awareness among manufacturers is limiting the overall adoption of anti-migrating additives. While many can see that color consistency and fabric quality can be strengths, much of the market is still using traditional dyeing processes. A failure to understand the longer-term benefits, such as fewer faults and higher customer satisfaction, is still hampering market expansion. To solve this, the industry needs to invest in educating smaller end-users, particularly in emerging nations, to promote the adoption and realization of the full utilization of the anti-migrating agent market with wider application and usage.

-

Stringent Regulations and Compliance Requirements May Hinder Growth

Stringent regulations in areas such as the EU and North America are hampering the market growth. Manufacturers are fighting to comply with stringent safety and environmental standards, which increase production costs and require further testing and certification. Failing to comply could result in expensive fines or product recalls, both of which would undermine adoption. Although these laws safeguard against consumer and environmental hazards, they may also impede market expansion and increase the difficulty for enterprises to bring new, innovative anti-migration solutions to market due to influencing market dynamics and the constraint of production flexibility.

Segmentation Analysis

By Source

The synthetic source dominated the anti-migrating agent market and held 66.2% of the market share in 2024. Artificial anti-migrating agents are used extensively in textiles, coatings, plastics, and other materials for which dye migration is a problem. They are more veracious, and less wandering and diffusing, than the natural ones, especially with synthetic fibers which are commonly used in the textile industry. The growing demand for high-quality textiles and coatings has led players, including BASF and Huntsman Corporation, to invest in testing synthetic alternatives. Synthetic anti-migrating additives are preferred in that they provide longer-lasting effects and are more economical for production in bulk.

Natural source is the fastest growing segment in the anti-migrating agent market at a CAGR of 7.52% due to the growing demand from technological industries for eco-friendly and sustainable materials. These natural anti-migrating additives, derived from renewable resources, are more likely options for manufacturers to consider as eco-processes. Environmental regulations and the trend of sustainable manufacturing, especially for textiles and packaging, are driving their uptake.

By Type

The Anionic segment is dominant and had the highest share in the anti-migrating agent market at around 42.5% in 2024. This predominance is due to the anionic agent's ability to inhibit dye migration in textiles and plastics. Anionic agents combine well with negatively charged substrates, so they are excellent for synthetic fibers and other substrates for which dye stability is important. The fact that they have been used in combination with anti-migrating agents to provide anti-migration benefits has made them the most widely used of all AMAs. The world's fabric giants, DuPont, Dow Chemical Company, and the like, depend upon anionic additives for sufficient colorfastness in their fabrics.

The non-ionic segment is projected to be the fastest-growing segment, with a CAGR of 6.91% over the forecast period due to its tremendous flexibility in the textiles, coatings, and plastics industry. These are agents that are well-tolerated with both natural and synthetic fibers and protect against dye migration while maintaining the quality of materials. The advantages in their performance are leading to greater use in top applications. Leading players such as Clariant and AkzoNobel develop high-end non-ionic formulations to accommodate increasing demand for high-performance, long-lasting product solutions.

By Grade

The technical grade dominated the anti-migrating agent market, which held 59.4% of the market share in 2024. Technical grade is mainly applied in industrial applications, such as textile coatings and plastics. Such agents are relatively inexpensive and exhibit good performance for the inhibition of migration. Their market share is large, as they are commonly used in industrial-scale processes throughout the industry. The market dominance is also attributable to a demand for lower-cost technical-grade additives sought after by the industry as an economical means to minimize dye migration.

Pharma grade is projected as the most promising segment, with a CAGR of 7.41% from 2025-2032. The demand for hand sanitizers is increasing due to further demand from the pharmaceutical and food industries, which have very high safety and quality standards. Pharma-grade anti-migrating additives fit the bill to maintain purity, particularly in drug packaging and coating applications. Furthermore, focusing on sustainable human and environmental safety manufacturing is promoting the uptake of eco-friendly anti-migrating additives, augmenting growth in heavily regulated, health-sensitive sectors.

By Application

Dyeing application dominated with a 46.8% market share in the anti-migrating agent market. Dye migration is creating a noticeable effect on textile production, therefore, demand is high for anti-migrating additives used for keeping the color of dyed cotton materials. In dyeing, additives are added to prevent cross-dyeing, especially with synthetic fibers.Textile and fabric producers and firms like Lenzing AG and Indorama Ventures are major users of anti-migrating additives in their dying operations for our fabric dyes to maintain quality, colorfast, and vivid shades.

During the forecast period, the fastest-growing segment is expected to be digital printing, with a 7.65% CAGR. Growing use of digital textile printing, which is known for customization and speed, is also providing an updated boost to the Anti-Migrating Additives market to prevent dye migration. The phenomenon is most pronounced in North America and Europe, where the fashion and home decoration communities have been centring their attention on premium and sustainable prints. With digital printing growing to new applications, it’s becoming more critical than ever for manufacturers to employ anti-migrating additives to improve their print clarity and durability and to comply with changing environmental and performance standards.

By End-use Industry

The textile industry dominated with a 63.5% anti-migrating agent market share in 2024. By application, anti-migrating additives see significant application in the textile industry owing to dye migration between textiles. Anti-migrating agents, which can improve the blacking fastness and the fastness to various factors for textile materials, are in high demand. Even larger textile companies on a worldwide stage, like Arvind Limited and Vardhman Textiles, rely on anti-migrating additives to ensure that quality is preserved in their dyed or printed fabrics, considering they are both responsible for shipping out massive amounts of synthetic and natural fiber fabrics to the rest of the world.

The paper segment is projected to be the fastest-growing end-use industry, driven by the increasing adoption of sustainable packaging. Anti‐migrating agents are additionally often used to obstruct migrations of inks and dyestuffs through the paper. Adoption is being driven by the move toward sustainable packaging, especially in food. And in terms of food safety and environmental, the standard is stricter, because of this, the use of high-performance anti-migrating agents can better control the printing quality and ensure compliance, and promote the demand for anti-migrating agents market.

Regional Analysis

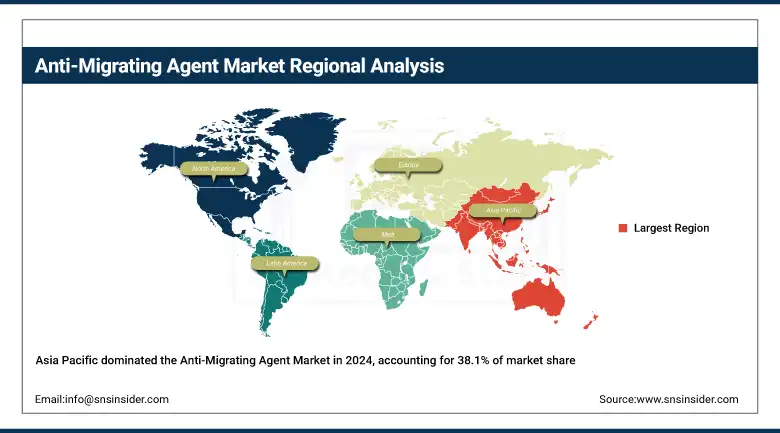

Asia Pacific dominated the anti-migrating agent market with 38.1% share and is followed by the textile giants, including China, India, and Japan. China, the world’s largest exporter of textiles, applies dye migration inhibitors to prevent color run. International standards help in shaping India’s demand. Low-cost manufacturing, increasing sustainability concerns, and foreign investments in the region drive the market growth. To scale production to meet this demand, companies are turning the Asia Pacific into a hub for high-quality textiles.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America emerged as the fastest-growing region with the highest growth rate in the anti-migrating agent market and a market share of 22.4%. Government policy towards green supply-side production will accelerate market expansion. The proliferation of manufacturing infrastructure and R&D know-how in the North American region has made it a fertile ground in the anti-migrating additives arena, and dye migration inhibitors are evolving rapidly.

Europe had held a substantial market share in 2024, driven by stringent environmental policies, including the EU Green Deal. Germany and France are at the forefront in the development of textile manufacturing and increasing demand for a range of eco-certified additives. Companies such as BASF and Clariant are paving the way toward sustainable chemical solutions, and the regulations are prompting faster adoption of safer methods for producing textiles. Its focus on circular economy principles and quality assurance is making Europe a leading player in the anti-migrating agent Market.

Key Players

The major competitors in the anti-migrating agent market include Archroma, Rudolf GmbH, SNF, Sarex Chemicals, Zschimmer & Schwarz Holding GmbH & Co KG, CHT Group, Bozzetto Group, Dymatic Chemicals, Inc., GYC Group, and Asutex.

Recent Developments

-

In February 2024, Archroma launched AVITERA® SE GENERATION NEXT, reducing water and energy use by 50%, boosting productivity by 25%, and offering new dark shades.

-

In October 2023, CHT Group, with Inditex, introduced PIGMENTURA, reducing water use by 96%, energy by 60%, and supporting sustainable textile production across fiber types.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 158.46 million |

| Market Size by 2032 | USD 271.74 million |

| CAGR | CAGR of 6.98% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Source (Synthetic, Natural) •By Type (Non-ionic, Anionic, Cationic, Amphoteric) •By Grade (Technical Grade, Pharma Grade, Food Grade) •By Application (Dyeing, Textile Printing, Digital Printing, Coatings, Others) •By End-use Industry (Textile, Plastics Industry, Paper Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Archroma, Rudolf GmbH, SNF, Sarex Chemicals, Zschimmer & Schwarz Holding GmbH & Co KG, CHT Group, Bozzetto Group, Dymatic Chemicals, Inc., GYC Group, Asutex |

Frequently Asked Questions

Environmental regulations and textile demand are accelerating North America's anti-migrating agent market growth.

Natural sources are the fastest-growing in the anti-migrating agent market, driven by eco-demand.

Sustainability trends are driving adoption of green additives in the anti-migrating agent market.

Digital printing needs precise color control, boosting the anti-migrating agent market for dye stability.

The anti-migrating agent market is expected to reach USD 271.74 million by 2032.

Get in Touch