Anti-Satellite (ASAT) Weapons Market Report Scope & Overview:

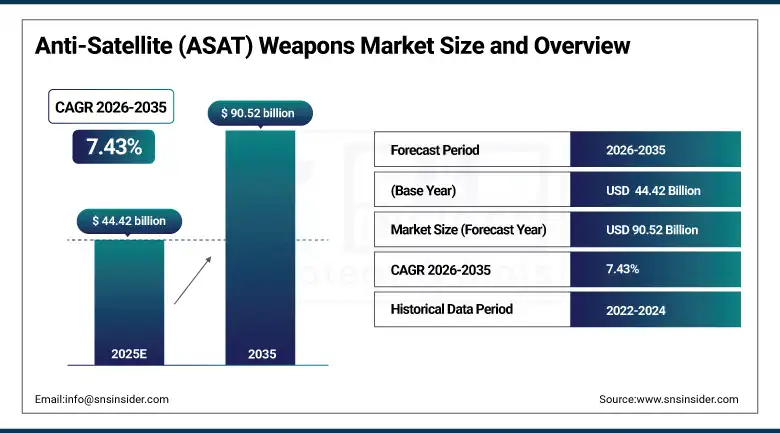

The Anti-Satellite (ASAT) Weapons Market size was valued at USD 44.42 Billion in 2025 and is projected to reach USD 90.52 Billion by 2035, growing at a CAGR of 7.43% during 2026–2035.

The Anti-Satellite (ASAT) weapons market is expanding, fueled by escalating geopolitical conflicts and the growing dependence on satellites for communication, navigation, and surveillance. The quest for space superiority in contemporary warfare is also a significant driver. Countries are pouring resources into counter-space capabilities to safeguard vital assets and dissuade potential opponents. Progress in missile technology, directed energy systems, and cyber warfare capabilities is further hastening this development. Moreover, the militarization of space and the proliferation of satellite constellations worldwide are creating a robust demand for both offensive and defensive ASAT solutions.

Anti-Satellite (ASAT) Weapons Market Size and Forecast:

-

Market Size in 2025: USD 44.42 Billion

-

Market Size by 2035: USD 90.52 Billion

-

CAGR: 7.43% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Anti-Satellite (ASAT) Weapons Market - Request Free Sample Report

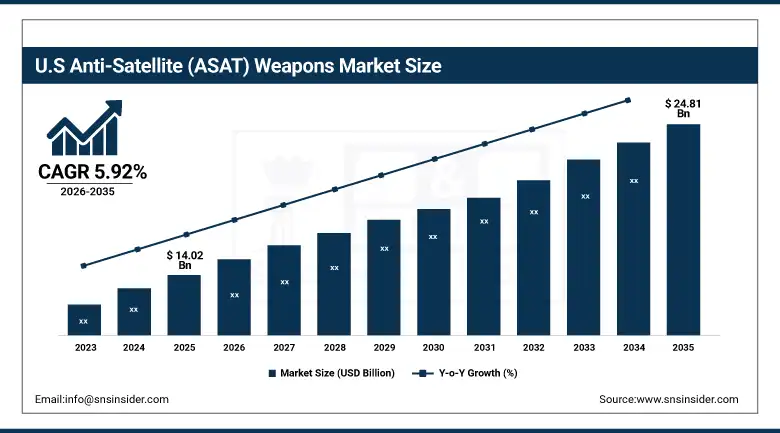

The U.S. Anti-Satellite (ASAT) Weapons Market was valued at USD 14.02 Billion in 2025 and is projected to reach USD 24.81 Billion by 2035, growing at a CAGR of 5.92% during 2026–2035. The United States remains the market’s largest national contributor, driven by sustained Space Force investment in electronic warfare systems, directed energy programs, and cyber capabilities for space domain operations, alongside classified procurement programs that supplement publicly budgeted space defense spending.

Anti-Satellite (ASAT) Weapons Market Highlights:

-

Space domain competition between the United States, China, and Russia is the fundamental demand driver, with each power simultaneously expanding satellite constellation capacity and investing in ASAT capabilities needed to threaten adversary constellations in conflict scenarios.

-

Kinetic kill vehicle programs are the largest market segment by value but carry international criticism for debris generation, pushing major powers toward non-kinetic approaches including directed energy, electronic warfare, and cyber that achieve satellite denial without creating long-lived orbital debris.

-

Directed energy weapons are the fastest-growing weapon type, with laser systems capable of dazzling or permanently blinding satellite electro-optical sensors attracting accelerated investment from the U.S. and allied nations pursuing reversible, graduated ASAT effect options.

-

Space-based ASAT platforms are the fastest-growing launch category, reflecting investment in co-orbital systems and resident space object programs that operate within adversary satellite operating envelopes and are difficult to attribute or counter using ground-based defensive measures.

-

The intersection of ASAT capability and satellite protection is generating dual-use program investment, where the same sensing and maneuvering systems that can disable an adversary satellite also provide the situational awareness needed to protect friendly satellites from attack.

Anti-Satellite (ASAT) Weapons Market Drivers:

-

Accelerating Space Militarization, Satellite-Dependent Military Operations, and Adversary ASAT Demonstrations Are Compelling Major Defense Budgets to Prioritize Space Superiority Investment

The operational dependence of modern military forces on satellite services is documented in every major exercise and threat assessment produced since 2015. GPS navigation, tactical satellite communications, missile defense early warning, and reconnaissance imagery collectively underpin the force multiplier effects that distinguish high-technology military operations. China’s ASAT programs including the DN-3 direct-ascent missile tested in late 2024 and co-orbital systems maneuvering near U.S. Government satellites in geosynchronous orbit throughout 2024 and 2025 have given U.S. defense planners concrete threat references sustaining congressional support for Space Force funding. Russia’s electronic warfare activity against Ukrainian satellite communications infrastructure throughout 2024 validated investment in both offensive and defensive space capabilities across NATO member defense budgets.

Anti-Satellite (ASAT) Weapons Market Restraints:

-

International Legal Uncertainty, Debris Generation Risk, and the Escalation Dynamics of Space Conflict Are Creating Policy Friction That Complicates Kinetic ASAT Program Expansion

International legal ambiguity, apprehensions regarding space debris, and the potential for conflict escalation are impeding the proliferation of kinetic anti-satellite (ASAT) programs. The lack of definitive global regulations engenders uncertainty for countries pursuing these capabilities, and the resultant debris from satellite destruction poses a risk to vital space infrastructure. Furthermore, the prospect of igniting wider space or terrestrial conflicts is fostering a more circumspect approach to policy. These elements, in conjunction, generate strategic and regulatory friction, thereby constraining the assertive deployment and testing of kinetic ASAT weapons.

Anti-Satellite (ASAT) Weapons Market Opportunities:

-

Non-Kinetic ASAT Approaches, Commercial Space Resilience, and Allied Nation Capability Development Create Growth Pathways That Kinetic Programs Cannot Address

Policy pressure against kinetic testing has redirected investment toward non-kinetic capabilities that achieve satellite denial without creating debris. Directed energy systems that dazzle or damage satellite sensors, electronic warfare systems that jam satellite command and control links, and cyber tools that intrude on ground station networks all achieve effects against adversary space systems without the debris externality or treaty ambiguity that kinetic systems generate. These capabilities are less visible, more deniable, and more reversible attributes that make them attractive to military planners who need graduated response options below the threshold of openly destructive ASAT employment. The growth of commercial satellite constellations including Starlink, OneWeb, and Amazon Kuiper has created a new ASAT planning dimension: protecting friendly commercial satellite services while disrupting adversary use of commercial space infrastructure is an emerging requirement driving new program investment in both offensive and defensive space capabilities.

Anti-Satellite (ASAT) Weapons Market Segment Highlights:

-

By Weapon Type: Dominant Kinetic Kill Vehicles (41.38% in 2025, CAGR 5.36%); Fastest-Growing Directed Energy Weapons (14.62% in 2025, CAGR 10.22%)

-

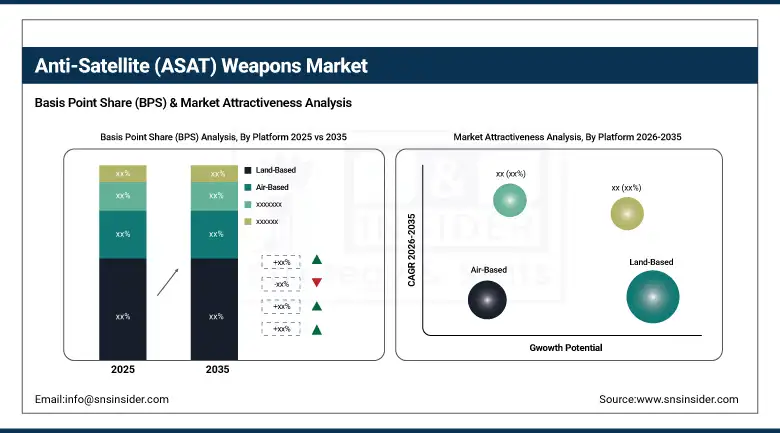

By Platform: Dominant Land-Based (52.47% in 2025, CAGR 5.83%); Fastest-Growing Space-Based (14.95% in 2025, CAGR 10.26%)

-

By Application: Dominant Strategic Military Deterrence (39.64% in 2025, CAGR 5.87%); Fastest-Growing Space Security & Satellite Protection (14.45% in 2025, CAGR 11.21%)

-

By End-User: Dominant Government & Defense Agencies (39.64% in 2025, CAGR 5.87%); Fastest-Growing Space Agencies / Research Institutions (14.45% in 2025, CAGR 11.21%)

Anti-Satellite (ASAT) Weapons Market Segment Analysis:

Kinetic Kill Vehicles Lead; Directed Energy Weapons Drive Fastest Growth

Kinetic systems lead because direct-ascent ballistic missile technology is the most technically mature ASAT approach and the most clearly demonstrable capability from a deterrence signaling perspective. Directed energy is growing fastest because policy pressure against kinetic testing, advances in solid-state laser power and beam control, and the operational advantages of speed-of-light engagement make laser-based satellite disruption increasingly viable and politically preferable.

Land-Based Platforms Lead; Space-Based Drives Fastest Growth

Land-based dominance reflects the maturity and cost-effectiveness of ground-launched systems for low Earth orbit targeting. Space-based is growing fastest because co-orbital systems and resident space object programs operating within adversary satellite operating envelopes create threat vectors that ground-based defenses cannot intercept.

Strategic Military Deterrence Leads; Space Security & Satellite Protection Drives Fastest Growth

Deterrence-oriented ASAT programs dominate because the primary purpose of deployed capability is to hold adversary constellations at risk as a strategic lever rather than actively destroy satellites in peacetime. Space security is growing fastest because Russia’s electromagnetic attacks on Viasat and Starlink terminals supporting Ukrainian operations throughout 2024 elevated the procurement priority of defensive space domain awareness and counter-interference systems.

Government & Defense Agencies Lead; Space Agencies / Research Institutions Drive Fastest Growth

Defense agencies hold the dominant share because ASAT program funding flows primarily through classified and unclassified defense appropriations. Space agencies and research institutions are growing fastest because the dual-use nature of space situational awareness, rendezvous and proximity operations, and directed energy research creates legitimate civilian research program funding for technologies with direct ASAT relevance.

Anti-Satellite (ASAT) Weapons Market Regional Analysis:

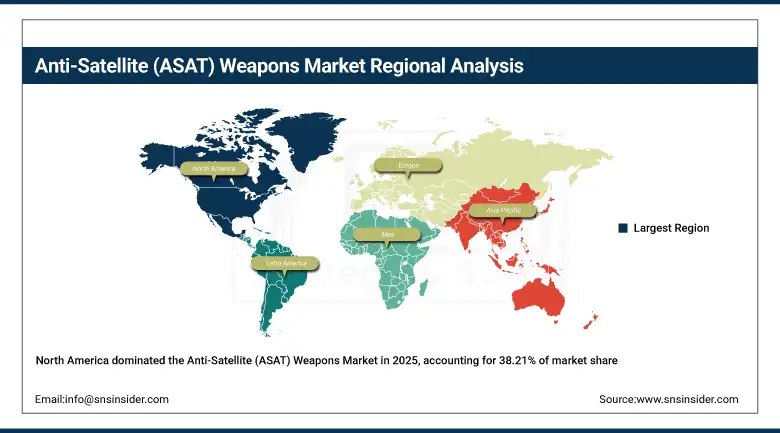

North America Anti-Satellite (ASAT) Weapons Market Insights

North America dominated in 2025 at USD 16.97 Billion (38.21%), projected to reach USD 31.29 Billion by 2035 at a CAGR of 6.36%. The region’s leadership is grounded in U.S. Space Force investment across electronic warfare, directed energy, and cyber space capabilities, classified procurement programs supplementing documented space defense spending, and a defense industrial base containing every major ASAT technology developer. Space Force budget requests in fiscal 2024 and 2025 both included significant increases in space superiority program funding.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Anti-Satellite (ASAT) Weapons Market Insights

As the globe's foremost space power, the United States leads North America in ASAT demand. The Space Force is actively developing programs across several areas, including electronic warfare, directed energy, and cyber ASAT capabilities. This effort is backed by the largest classified space defense budget in the world.

Europe Anti-Satellite (ASAT) Weapons Market Insights

Europe held a 26.84% share in 2025 at USD 11.92 Billion, growing to USD 22.79 Billion by 2035 at a CAGR of 6.75%, driven by NATO space domain awareness programs, France’s Space Command with patrol satellites and declared space defense capabilities, and 2024–2025 operational expansions of the UK’s National Space Operations Centre and Germany’s Bundeswehr Space Command.

France Anti-Satellite (ASAT) Weapons Market Insights

France leads European ASAT investment through its Space Command’s active patrol satellite programs, declared right to self-defense in space, and the most explicit European national space defense doctrine encompassing both offensive and defensive space capabilities.Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Anti-Satellite (ASAT) Weapons Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 9.38%, rising from USD 10.98 Billion in 2025 to USD 26.83 Billion by 2035. China is the dominant driver with a comprehensive ASAT program spanning all weapon types and platforms. India’s Defense Space Agency has been expanding electronic warfare and space situational awareness programs, and Japan and Australia have both increased space domain awareness investment under allied security commitments.

China Anti-Satellite (ASAT) Weapons Market Insights

China leads Asia Pacific ASAT investment through the world’s most comprehensive program spanning kinetic missiles, co-orbital systems, directed energy, electronic warfare, and cyber capabilities, with documented testing across multiple weapon types and active deployment of co-orbital rendezvous systems near U.S. government satellites.

Latin America and Middle East & Africa Anti-Satellite (ASAT) Weapons Market Insights

Latin America held a 5.62% share in 2025 at USD 2.50 Billion, growing at a CAGR of 6.62% to USD 4.72 Billion by 2035, led by Brazil’s space situational awareness programs and military satellite development. Middle East and Africa accounted for 4.60% of the market in 2025, valued at USD 2.04 billion. This region is projected to expand at a brisker compound annual growth rate (CAGR) of 9.16%, reaching USD 4.89 billion by 2035. Israel is at the forefront, driven by IAI and Rafael's space security expertise. Israel spearheads investments in ASAT and space security within the MEA, thanks to its sophisticated intelligence satellite programs, space-based surveillance capabilities developed by IAI and Rafael, and a national security strategy that has emphasized space domain awareness and satellite intelligence since the early 2000s.

Anti-Satellite (ASAT) Weapons Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin is the United States’ largest defense contractor and a primary participant in ASAT-relevant programs spanning space situational awareness, satellite protection, directed energy research, and the advanced satellite bus technologies underpinning both offensive co-orbital programs and defensive satellite resilience. Its Space division produces missile defense interceptors sharing propulsion and guidance technology with direct-ascent ASAT systems, and its directed energy programs include laser weapon systems under development for the Space Force.

In March 2025, Lockheed Martin received a U.S. Space Force contract for a next-generation space domain awareness satellite under the Space Awareness Persistent Surveillance program, delivering enhanced detection and tracking for objects in geosynchronous orbit where co-orbital ASAT threats have been most frequently observed, with provisions for on-orbit servicing compatibility.

Northrop Grumman Corporation

Northrop Grumman participates in the ASAT market through its electronic warfare systems, space systems division, and classified programs spanning satellite vulnerability assessment, space domain awareness, and counter-space capability development. Its Mission Enabling Products and Solutions division produces electronic systems relevant to satellite communications jamming and anti-jamming, and its space systems experience across military and scientific satellite programs gives it technical depth across the precision mechanisms and thermal management challenges that directed energy and space-based ASAT systems require. Its Strategic Space Systems division is a primary contractor for classified overhead reconnaissance and space control programs.

In January 2025, Northrop Grumman received a contract modification for the Space Force’s Evolved Strategic SATCOM program a next-generation protected military satellite communications system adding hardening requirements reflecting updated assessments of adversary electronic warfare capabilities targeting U.S. military satellite communications.

Anti-Satellite (ASAT) Weapons Market Key Players:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Raytheon Technologies Corporation

-

The Boeing Company

-

Airbus Defence and Space

-

Thales Group

-

BAE Systems plc

-

General Dynamics Corporation

-

L3Harris Technologies Inc.

-

Almaz-Antey Corporation

-

Rostec State Corporation

-

Israel Aerospace Industries

-

China Aerospace Science and Technology Corporation

-

China Aerospace Science and Industry Corporation

-

Mitsubishi Heavy Industries Ltd.

-

Saab AB

-

Leonardo S.p.A.

-

Rafael Advanced Defense Systems Ltd.

-

MBDA

-

Kratos Defense & Security Solutions

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 44.42 Billion |

| Market Size by 2035 | USD 90.52 Million |

| CAGR | CAGR of 7.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Weapon Type (Kinetic Kill Vehicles (Direct-Ascent Missiles), Co-orbital / Microsatellite Systems, Directed Energy Weapons (Laser, Microwave), Electronic Warfare & Jamming Systems, and Cyber ASAT Tools) • By Platform (Land-Based, Air-Based, Sea-Based, and Space-Based) • By Application (Strategic Military Deterrence, Counter-Reconnaissance / Intelligence Denial, Tactical Battlefield Satellite Disruption, and Space Security & Satellite Protection), • By End-User (Government & Defense Agencies, Armed Forces, Intelligence Agencies, and Space Agencies / Research Institutions) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, The Boeing Company, Airbus Defence and Space, Thales Group, BAE Systems plc, General Dynamics Corporation, L3Harris Technologies Inc., Almaz-Antey Corporation, Rostec State Corporation, Israel Aerospace Industries, China Aerospace Science and Technology Corporation, China Aerospace Science and Industry Corporation, Mitsubishi Heavy Industries Ltd., Saab AB, Leonardo S.p.A., Rafael Advanced Defense Systems Ltd., MBDA, Kratos Defense & Security Solutions |

Frequently Asked Questions

North America dominated the Anti-Satellite (ASAT) Weapons in 2025

Kinetic Kill Vehicles (Direct-Ascent Missiles) dominated the Anti-Satellite (ASAT) Weapons with a 19.38% share in 2025.

Rising geopolitical tensions and increasing dependence on satellite-based communication, surveillance, and navigation systems are the key drivers of the Anti-Satellite (ASAT) Weapons Market.

The Anti-Satellite (ASAT) Weapons size was USD 44.42 Billion in 2025 and is expected to reach USD 90.52 Billion by 2035.

The Anti-Satellite (ASAT) Weapons is expected to grow at a CAGR of 7.43% from 2026–2035.

Get in Touch