Antiarrhythmic Drugs Market Report Scope & Overview:

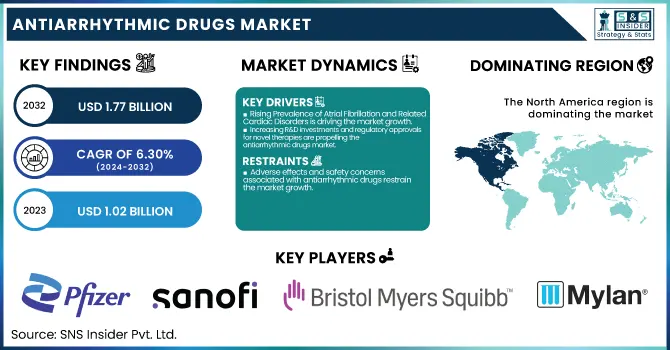

The Antiarrhythmic Drugs Market was valued at USD 1.02 billion in 2023 and is expected to reach USD 1.77 billion by 2032, growing at a CAGR of 6.30% from 2024-2032.

To Get more information on Antiarrhythmic Drugs Market - Request Free Sample Report

This report provides a statistical perspective by providing intricate information on the incidence and prevalence of cardiac arrhythmias, highlighting the region-wise disease burden. Additionally, it reviews pharmaceutical expenditure incurred on antiarrhythmic medicines by major geographies, pay-type-wise. The report also showcases drug approval and pipeline trends, with a focus on regulatory trends and up-and-coming therapies. Further, it contains a detailed examination of hospitalization and rehospitalization rates for arrhythmias and provides a generic vs. branded drug market share forecast comparison with unique long-term commercial visibility.

The U.S. Antiarrhythmic Drugs Market was valued at USD 0.30 billion in 2023 and is expected to reach USD 0.51 billion by 2032, growing at a CAGR of 6.28% from 2024-2032. The United States dominates the North American Antiarrhythmic Drugs Market due to a high rate of atrial fibrillation and an established healthcare system. This is complemented by the dominance of key pharma companies and robust regulatory structures.

Market Dynamics

Drivers

-

Rising Prevalence of Atrial Fibrillation and Related Cardiac Disorders is driving the market growth.

The rising global incidence of atrial fibrillation (AF) is one of the key market drivers for the antiarrhythmics drugs industry. The Centers for Disease Control and Prevention (CDC) reports that an estimated 12.1 million Americans will have AF by 2030, a rise from about 6 million in 2023. AF is linked to serious risks, including stroke and heart failure, making long-term rhythm and rate control, mainly treated with antiarrhythmic drug therapy, a necessity. In addition, elderly populations in the likes of Europe and Japan have led to an acute increase in cardiac arrhythmia prevalence. This increased clinical demand has stimulated pharmaceutical firms to diversify their product lines. For instance, Sanofi's Multaq (dronedarone) continues to be a popular treatment for AF, whereas investigations into new agents such as abelacimab by Anthos Therapeutics have accelerated with the acquisition by Novartis in 2025.

-

Increasing R&D investments and regulatory approvals for novel therapies are propelling the antiarrhythmic drugs market.

The antiarrhythmic drugs market is significantly driven by growing R&D investment and a surge in regulatory approvals for innovative therapies. Between 2020 and 2025, the U.S. FDA and European Medicines Agency (EMA) have increasingly supported expedited pathways for drugs targeting unmet needs in arrhythmia care. Notably, Multaq by Sanofi was the first antiarrhythmic drug to demonstrate reduced cardiovascular hospitalization, a key milestone in drug approval standards. Furthermore, pipeline drugs such as Omacetaxine mepesuccinate and Vernakalant are in advanced clinical trials, showcasing the industry's innovation pipeline. Large pharma companies like Pfizer, Novartis, and Bristol-Myers Squibb have raised R&D expenditures on cardiovascular therapeutics. Collaborations, like Novartis' 2025 acquisition of Anthos Therapeutics for access to abelacimab, reflect the strategic interest in new antiarrhythmic solutions for both safety and efficacy improvement.

Restraint

-

Adverse effects and safety concerns associated with antiarrhythmic drugs restrain the market growth.

One of the major constraints in the antiarrhythmic drugs market is the risk of severe side effects, which tends to limit long-term treatment and physician preference. Several Class I and Class III antiarrhythmic agents, including amiodarone and flecainide, have been implicated in proarrhythmic effects, hepatotoxicity, pulmonary toxicity, and thyroid dysfunction. These safety issues result in repeated treatment discontinuation and close monitoring needs, thus lowering patient compliance. As per research work published in the Journal of the American College of Cardiology (2023), almost 25–30% of the patients withdraw from amiodarone during the first year because of intolerance or complications. Additionally, the absence of biomarkers for forecasting adverse effects complicates patient stratification. The conservative regulatory environment and the reluctance of doctors in prescribing these medications add to the limited growth of the market despite growing demand for arrhythmia treatment services.

Opportunities

-

Expansion of antiarrhythmic therapies in emerging economies presents a significant opportunity to the market.

The increasing healthcare expenditures and enhancing access to cardiac treatment in emerging markets offer a favorable opportunity for growth in antiarrhythmic drugs. Asia Pacific, Latin America, and certain parts of the Middle East & Africa are experiencing a rise in cardiovascular disease incidence with increasing populations and lifestyles due to urbanization and aging. These markets continue to have insufficient availability of sophisticated cardiac drugs. As generic producers increase their presence and governments focus on managing non-communicable diseases, the penetration of antiarrhythmic drugs will increase substantially. For example, India's National Health Mission and other government initiatives are making cardiovascular drugs more accessible at public hospitals. Drug companies that provide affordable generics and collaborate with local distribution channels can take advantage of this unmet need and increase their worldwide market share.

Challenges

-

Limited Innovation and Slow Clinical Pipeline Progression are challenging the market to grow.

Notwithstanding the increased need for more effective and safer antiarrhythmics, the industry is constrained by the industry's low pace of clinical innovation. With few exceptions, all existing drugs have been formulated over decades, and very less have entered as a new class over that period. Complicated electrophysiology, in addition to the high likelihood of failure for clinical trials of new agents resulting from toxicity and proarrhythmia, constitutes a hindrance to innovation. For instance, many late-stage studies on atrial fibrillation medication have previously been stopped due to safety concerns. The expense of drug development, as well as demanding regulations on cardiac safety endpoints, deters numerous firms from investigating new molecules. This has resulted in a pipeline that is dominated by reformulations or combination therapies as opposed to first-in-class drugs, which presents a challenge for firms seeking to differentiate in a risk-averse and competitive environment.

Segmentation Analysis

By Drugs

In 2023, the Beta Blockers segment dominated the Antiarrhythmic Drugs Market with a 35.20% market share because of the wide range of therapeutic uses and long-standing clinician acceptance. They are predominantly prescribed not only for arrhythmias but also for comorbid cardiovascular illnesses like hypertension, heart failure, and ischemic heart disease—a first-line preferred treatment. Agents such as metoprolol, propranolol, and atenolol possess established safety profiles and are recommended in many clinical guidelines for rate control in atrial fibrillation. Their capacity to decrease myocardial oxygen demand, delay atrioventricular conduction, and reduce mortality in post-myocardial infarction patients also contributes to their prevalence. In 2023, beta blockers accounted for a significant majority of antiarrhythmic drug prescriptions in the hospital and ambulatory settings in particularly in high cardiovascular disease regions like North America and Europe.

Potassium Channel Blockers segment is the fastest growing segment over the forecast period, with growing embracement of rhythm-control strategies along with the appearance of newer as well as safer formulations. This segment contains powerful agents such as amiodarone, dofetilide, and dronedarone that are effective in the maintenance of sinus rhythm in atrial fibrillation and ventricular arrhythmias. Notwithstanding past issues regarding toxicity, newer agents such as dronedarone (Multaq) provide enhanced safety profiles, which is part of increasing physician confidence. In addition, research into selective potassium channel modulators continues with the goal of minimizing adverse effects while maintaining efficacy, further driving growth in this segment. The move towards individualized cardiology and increasing application of potassium channel blockers in managing complex arrhythmias, particularly in Asia Pacific and elderly populations, also drives this upward trend.

By Route of Administration

In 2023, the Oral segment dominated the Antiarrhythmic Drugs Market with a 72.13% market share due to its convenience of administration, patient compliance, and extensive application in long-term management of arrhythmia. The most frequently prescribed antiarrhythmic drugs, such as beta blockers (e.g., metoprolol), potassium channel blockers (e.g., amiodarone), and sodium channel blockers (e.g., flecainide), are oral formulations, and hence they are ideal for outpatient treatment. These drugs are favored for long-term rhythm and rate control in diseases like atrial fibrillation and supraventricular tachycardia. Oral medications are also inexpensive and readily available in hospitals and retail pharmacies, aiding their predominance. Favorable reimbursement policies and listing in guidelines for the treatment of arrhythmias have also contributed to the increased use of oral therapies, especially in high-disease prevalence areas like North America and Europe.

The Other segment, including new drug delivery methods like transdermal patches, sublingual products, and implantable drug delivery systems, is expected to see the fastest growth over the forecast period with 7.18% CAGR. The reason behind this growth is an increasing need for non-invasive, quick-onset, and targeted delivery systems, particularly among patients with low gastrointestinal tolerance or needing a quick therapeutic response. Emerging technologies, including drug-eluting cardiac devices and transdermal beta-blocker patches, are becoming increasingly popular because of their ability to enhance drug bioavailability and compliance. In addition, research and development in the pipeline are aimed at maximizing delivery in patients with challenging arrhythmias who are unable to tolerate standard oral or parenteral therapy. The transition towards precision medicine and innovation in drug formulation is expected to spur tremendous growth in this segment in the future.

By Distribution Channel

In 2023, the Hospital Pharmacies segment dominated the Antiarrhythmic Drugs Market with a 64.10% market share because of significant dependence on hospital-based treatment for complicated and acute cases of arrhythmias. Antiarrhythmic medications like amiodarone, lidocaine, and propafenone are often used in inpatient facilities, particularly during attacks of atrial fibrillation, ventricular tachycardia, or cardiac complications following surgery. Hospitals are usually the entry point of care for symptomatic or severe arrhythmias, which means they have to provide immediate access to strong antiarrhythmic drugs, usually via intravenous or high-dose oral administration. Hospitals also have an essential role in initiating treatment, dose adjustment, and following up on patients for possible drug-related side effects like QT prolongation or proarrhythmic activity, both of which need to be strictly supervised. In addition, the availability of cardiology units, electrophysiology laboratories, and integrated care pathways increases the utilization of these medications in hospital settings. Institutional procurement policies and government reimbursement further promote the dominant supply and administration of antiarrhythmic medications through hospital pharmacies, entrenching their leading market position.

Regional Analysis

North America dominated the Antiarrhythmic Drugs Market with a 38.19% market share in 2023 because of its well-developed healthcare infrastructure, high level of disease awareness, and high burden of cardiac arrhythmias like atrial fibrillation. The region is supported by the established presence of major pharmaceutical firms, strong clinical research, and favorable reimbursement policies that encourage early diagnosis and treatment. Besides, ongoing innovation and early uptake of novel antiarrhythmic treatments are responsible for the region's dominance in drug development as well as patient access. The U.S., specifically, boasts a huge patient base, which further fuels demand for antiarrhythmic drugs, as well as rapid expansion in the market for new therapies.

Asia Pacific is the fastest-growing region in the Antiarrhythmic Drugs Market with 6.76% CAGR throughout the forecast period, driven mainly by its rapidly aging population and cardiovascular disease incidence on the rise. Economic growth, wider healthcare access, and more government efforts to enhance cardiac care are fueling market growth. Also, increasing awareness, enhanced diagnostic technology, and increasing investments from international pharmaceutical firms are driving the growth of antiarrhythmic therapies in markets such as China, India, and Japan. Increased emphasis on healthcare infrastructure development and expanding healthcare insurance coverage also boosts market penetration, developing a favorable ground for antiarrhythmic drug uptake in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Market Players

-

Pfizer Inc. (Quinidex, Pronestyl)

-

Sanofi S.A. (Cordarone, Norpace)

-

Bristol-Myers Squibb Company (Coumadin, Cardarone)

-

Mylan N.V. (Disopyramide, Mexiletine)

-

Novartis AG (Tambocor, Betaloc)

-

Teva Pharmaceutical Industries Ltd. (Propafenone, Lidocaine)

-

Abbott Laboratories (Rythmol, Procan SR)

-

AstraZeneca plc (Tenormin, Toprol-XL)

-

GSK plc (Tenormin, Sotalol)

-

Zydus Lifesciences Ltd. (Amiodarone, Diltiazem)

-

Sun Pharmaceutical Industries Ltd. (Flecainide, Verapamil)

-

Dr. Reddy’s Laboratories Ltd. (Amiodarone, Mexiletine)

-

Lupin Limited (Dronedarone, Bisoprolol)

-

Glenmark Pharmaceuticals Ltd. (Amiodarone, Propranolol)

-

Aurobindo Pharma Ltd. (Sotalol, Propafenone)

-

Cipla Ltd. (Disopyramide, Flecainide)

-

Boehringer Ingelheim International GmbH (Multaq, Micardis)

-

Roche Holding AG (Lanoxin, Cardizem)

-

Takeda Pharmaceutical Company Limited (Cordanum, Lidocaine)

-

Merck & Co., Inc. (Betapace, Isoptin)

Suppliers (These suppliers commonly provide active pharmaceutical ingredients (APIs), excipients, and contract manufacturing services (CDMO) essential for the formulation, development, and large-scale production of antiarrhythmic drugs). In the Antiarrhythmic Drugs Market

-

BASF SE

-

Evonik Industries AG

-

Merck KGaA

-

Lonza Group AG

-

Thermo Fisher Scientific Inc.

-

Cambrex Corporation

-

WuXi AppTec

-

Hovione

-

Almac Group

-

Capua BioServices S.p.A.

Recent Developments

-

July 2024 – Sanofi-Aventis has announced that the U.S. Food and Drug Administration (FDA) has approved Multaq (dronedarone) 400 mg tablets. Approval offers a new treatment option for patients experiencing atrial fibrillation (AF) or atrial flutter (AFL). Multaq is the first product in the United States that has been shown to demonstrate a clinical benefit by decreasing cardiovascular hospitalization among this patient group.

-

February 2025 – Novartis confirmed that it signed a deal to acquire Anthos Therapeutics, Inc., a clinical-stage, private, biopharmaceutical corporation with operations based in Boston. The transaction consists of abelacimab, which is an investigative, late-stage drug intended to be used to prevent stroke and systemic embolism in individuals who have atrial fibrillation.

-

September 2024 – U.S. subsidiary Teva Pharmaceuticals announced new encouraging Phase 3 results for Teva's SOLARIS trial, testing TEV-'749, an extended-release olanzapine subcutaneous formulation. Results show encouraging efficacy, safety, and tolerability in adults diagnosed with schizophrenia.

Antiarrhythmic Drugs Market Report Scope:

Report Attributes Details Market Size in 2023 US$ 1.02 Billion Market Size by 2032 US$ 1.77 Billion CAGR CAGR of 6.30 % From 2024 to 2032 Base Year 2023 Forecast Period 2024-2032 Historical Data 2020-2022 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Drug Type (Sodium Channel Blockers, Beta Blockers, Potassium Channel Blockers, Calcium Channel Blockers, Other)

• By Route of Administration (Oral, Parenteral, Other)

• By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Other)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) Company Profiles Pfizer Inc., Sanofi S.A., Bristol-Myers Squibb Company, Mylan N.V., Novartis AG, Teva Pharmaceutical Industries Ltd., Abbott Laboratories, AstraZeneca plc, GSK plc, Zydus Lifesciences Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Glenmark Pharmaceuticals Ltd., Aurobindo Pharma Ltd., Cipla Ltd., Boehringer Ingelheim International GmbH, Roche Holding AG, Takeda Pharmaceutical Company Limited, Merck & Co., Inc., and other players.

Frequently Asked Questions

North America dominated the Antiarrhythmic Drugs Market in 2023.

The “Oral” segment dominated the Antiarrhythmic Drugs Market.

Increasing R&D investments and regulatory approvals for novel therapies are propelling the antiarrhythmic drugs market.

The Antiarrhythmic Drugs Market was USD 1.02 billion in 2023 and is expected to reach USD 1.77 billion by 2032.

The Antiarrhythmic Drugs Market is expected to grow at a CAGR of 6.30% from 2024-2032.

Get in Touch