Anticoagulant Rodenticides Market Report Scope & Overview:

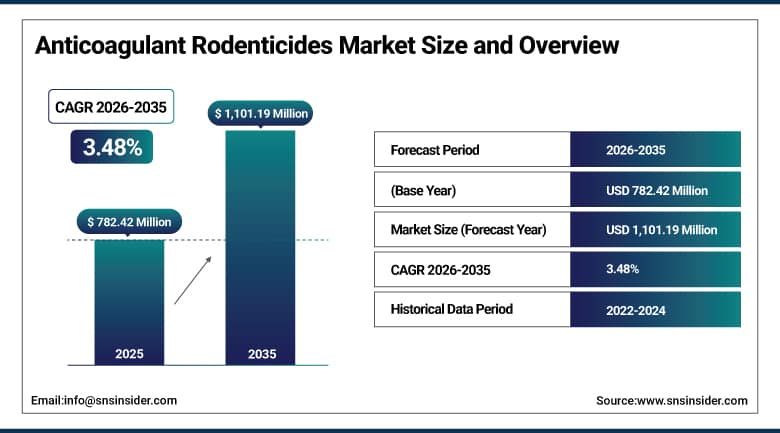

The Anticoagulant Rodenticides Market was valued at USD 782.42 Million in 2025 and is expected to reach USD 1,101.19 Million by 2035, growing at a CAGR of 3.48% from 2026 to 2035.

Anticoagulant rodenticides have been growing in terms of performance on a consistent basis in the global marketplace. The market includes not only first-generation anticoagulant rodenticides such as warfarin, chlorophacinone, and diphacinone but also second-generation anticoagulant rodenticides such as bromadiolone, brodifacoum, and flocoumafen. The rise of urbanization, leading to denser areas for humans that generate much more food waste, as well as the climate changes that increase the breeding period of rodents and the growth of grain storage areas that require proper rodent population management, all contribute to this above-market growth of demand.

SecureChoice was launched by Syngenta in the UK in October 2023 as an innovative and intelligent remote rodent detection system. SecureChoice is a digital tool that helps pest control technicians implement their rodent control programs more effectively, thus giving their clients the added benefit of increased visibility into their services. This technological advancement is the direction that anticoagulant rodenticides are taking in their commercial use.

Market Size and Forecast

-

Market Size in 2026E: USD 809.65 Million

-

Market Size by 2035: USD 1,101.19 Million

-

CAGR: 3.48% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Anticoagulant Rodenticides Market - Request Free Sample Report

Anticoagulant Rodenticides Market Trends

-

IoT-enabled smart bait stations are improving rodent monitoring, bait management, and pest control efficiency.

-

Second-generation anticoagulants are gaining adoption for controlling resistant rodent populations with single-feed effectiveness.

-

Regulatory restrictions are driving development of safer bait delivery systems that reduce non-target wildlife exposure.

-

Integrated pest management programs are increasing demand for continuous rodent control across commercial and agricultural sectors.

-

Moisture-resistant and eco-friendly bait formulations are improving performance in outdoor and high-humidity environments.

U.S. Anticoagulant Rodenticides Market Size Outlook

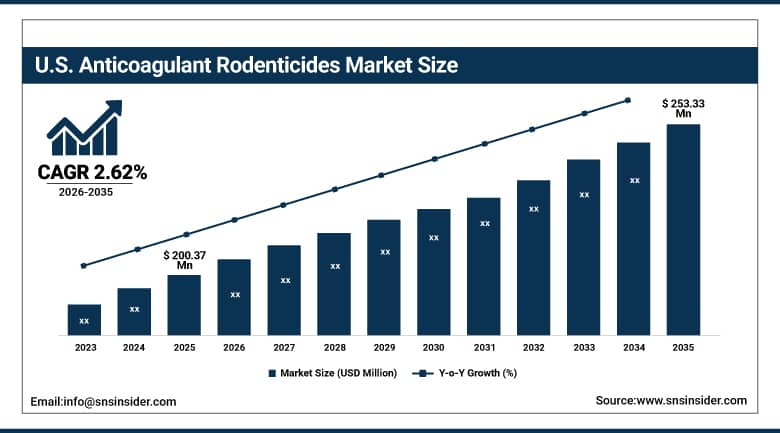

The U.S. anticoagulant rodenticides market was valued at approximately USD 200.37 Million in 2025 and is expected to reach approximately USD 253.33 Million by 2035, growing at a CAGR of approximately 2.62%.

The U.S. is the most commercially significant anticoagulant rodenticides market within North America’s dominant regional position. BASF SE’s Selontra and Storm Ultra products, Bell Laboratories’ Contrac and Fastrac portfolio, Syngenta’s Talon and Talon Soft Bait, Neogen Corporation’s Havoc and Ramik rodenticide range, and Liphatech’s Generation and Ditrac products collectively define the domestic commercial landscape. The Federal Insecticide, Fungicide, and Rodenticide Act’s regulatory framework governs registration, distribution, and use, maintaining product quality standards that sustain professional pest control industry procurement. The CDC’s documentation of rising rodent populations in major U.S. cities creates consistent institutional demand for effective rodent control solutions.

In 2024, BASF SE strengthened its position in the global anticoagulant rodenticides market by focusing on advanced formulations balancing high efficacy with environmental safety, innovating in bait technology to improve moisture resistance and palatability for consistent performance across varied climatic conditions. The company’s investment reflects the commercial direction toward premium formulations that sustain above-commodity pricing through demonstrable performance differentiation in challenging deployment environments.

Anticoagulant Rodenticides Market Segment Analysis

-

By Type, the second-generation anticoagulants segment dominated market with the largest revenue share in 2025, while the first-generation anticoagulants segment remains commercially significant.

-

By Form, the Blocks segment dominated the market with approximately 46% share in 2025, while the pellets segment is the fastest growing.

-

By Application, the agriculture segment dominated the market with the largest revenue share in 2025, while the pest control companies segment is the fastest growing.

-

By Distribution Channel, supermarkets/hypermarkets dominated the market with 43.7% share in 2025, while online stores is the fastest growing.

By Application, agriculture dominates, pest control companies grow fastest

Agriculture retained the dominant application position with the largest revenue share of the anticoagulant rodenticides market in 2025. The agricultural sector’s commercial primacy reflects the extraordinary economic cost of rodent damage to global crop production, with the Food and Agriculture Organization documenting that rodents destroy approximately 20% of global food production annually through direct consumption, contamination, and storage damage. Each grain storage facility whose stored crop inventory represents millions of dollars in agricultural commodity value creates rodenticide procurement whose investment is justified by the prevention of much larger crop loss.

Pest control companies are the fastest growing application segment because the professional pest management industry’s systematic adoption of structured anticoagulant rodenticide service contracts for urban residential, commercial building, food service, and institutional clients creates above-average procurement growth from commercial buyers whose contract service model creates consistent and predictable rodenticide consumption. Each pest control company that expands its residential and commercial client base creates rodenticide procurement whose annual volume scales with the client portfolio. The growing rat population in major cities creates expanding urban pest control service demand that sustains professional pest control company procurement growth.

By Form, blocks dominate, pellets grow fastest

Blocks retained the dominant form position of the anticoagulant rodenticides market in 2025. The commercial primacy of block formulations reflects their exceptional environmental durability and deployment flexibility that make them the preferred professional-grade format for pest control operators. Block rodenticides’ capacity to withstand shifting climatic conditions including high humidity, temperature extremes, and moisture exposure makes them suitable for outdoor agricultural, sewer, and industrial applications where pellet formulations degrade rapidly. The ability to secure blocks within bait stations creates important safety advantages by limiting access to non-target species meeting regulatory requirements for responsible rodenticide deployment in public and commercial areas.

Pellets are the fastest growing form because their cost-effectiveness, ease of scattered placement, uniform active ingredient distribution, and improved formulation performance in moisture-resistant variants create above-average adoption growth in both professional pest control and agricultural self-application markets. The driving factor for pellets is their effectiveness in delivering fast, single-dose control in challenging conditions including agricultural field edge placement and dense urban bait station filling whose operational efficiency advantages over block formats sustain pellet procurement growth. Growing adoption in food storage facilities and public health programmes where precise placement and quick rodent access create procurement preference reflects pellets’ reliability in high-traffic rodent environments.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Anticoagulant Rodenticides Market Insights

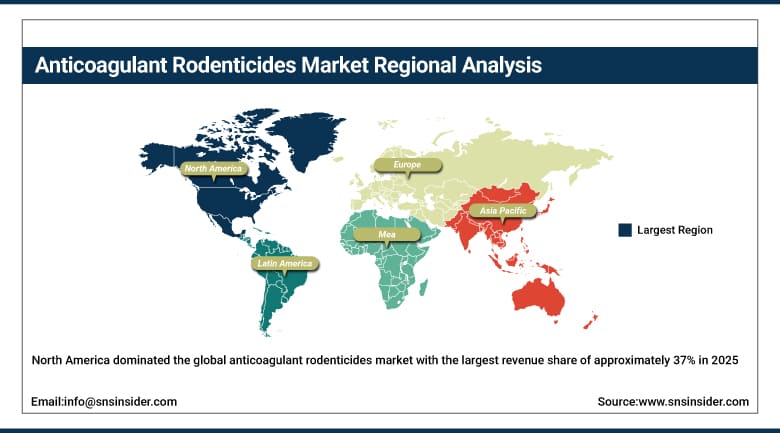

North America dominated the global anticoagulant rodenticides market with the largest revenue share of approximately 37% in 2025, driven by the robust agricultural infrastructure, widespread urbanization creating consistent urban rodent pest demand, stringent public health regulations requiring effective rodent control in food handling facilities, and the presence of leading manufacturers. The United States accounts for approximately 87.4% of North American revenues through Bell Laboratories, Neogen, Liphatech, and Syngenta’s commercial operations.

Canada contributes approximately 12.6% of North American revenues through its grain agriculture sector’s rodent control investment, the growing urban pest control industry in major Canadian cities, and the food processing sector’s regulatory compliance rodenticide procurement for HACCP-certified facilities.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Anticoagulant Rodenticides Market Insights

Europe is a technically sophisticated anticoagulant rodenticides market where strong animal welfare legislation, regulatory restrictions on second-generation anticoagulants in ecologically sensitive areas, and advanced integrated pest management culture create structured institutional demand for compliant, effective rodenticide products. Germany accounts for approximately 22.3% of European revenues through its agricultural sector’s rodent control investment, BASF’s domestic operations, and the municipal pest control sector’s urban rodent management.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS food safety compliance requirements, French agricultural rodent control programmes, and Dutch greenhouse and food production sector’s integrated pest management investment create consistent anticoagulant rodenticide procurement. PelGar International’s UK headquarters and Syngenta’s Swiss base sustain regional commercial supply.

Asia Pacific Anticoagulant Rodenticides Market Insights

Asia Pacific is the fastest growing regional anticoagulant rodenticides market with CAGR 3.34%, driven by rapid urbanization creating expanding urban rodent pest management demand, the extraordinary scale of Asian agricultural production requiring systematic rodent control, growing awareness of rodent-borne disease risks including leptospirosis and hantavirus, and government initiatives to improve food safety standards. China accounts for approximately 44.8% of Asia Pacific revenues through its massive rice and grain agricultural sector’s rodent control investment and the urban pest control industry serving China’s dense city populations.

India and Southeast Asia represent the most commercially dynamic emerging markets within Asia Pacific where rapid urbanization, the agricultural sector’s growing rodent control awareness, and the food processing industry’s improving hygiene standards collectively create above-average anticoagulant rodenticide procurement growth from previously underserved demand bases.

MEA & Latin America Anticoagulant Rodenticides Market Insights

South Africa leads MEA revenues at approximately 31.2% through its agricultural sector’s rodent control investment, the urban pest control industry, and the food processing sector’s compliance procurement. Egypt and Nigeria’s growing grain agriculture sectors add complementary regional demand. Brazil leads Latin American revenues through its large agricultural sector’s soybean and sugarcane rodent protection, the growing urban pest control industry in major cities, and the food processing sector’s HACCP compliance rodenticide procurement. Argentina and Mexico collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Rising rodent infestation in urban areas and critical food protection requirements in agriculture and food processing

Rising urban rodent populations driven by urbanization, expanding human settlements, and changing climate conditions that extend rodent breeding seasons is the anticoagulant rodenticides market’s most commercially direct structural growth driver. Each new urban development whose expanded waste generation creates rodent habitat and food source creates a new pest management requirement that sustains professional pest control procurement. The CDC’s documentation of New York City’s rat population growth from 2 million in 2014 to an estimated 3 million in 2023 reflects the commercial trajectory of urban rodent pressure whose escalation creates consistent demand expansion.

Agricultural food protection requirements sustaining systematic rodent control investment create the most commercially structured anticoagulant rodenticide procurement. Each grain storage facility whose HACCP compliance certification requires documented pest control programmes creates rodenticide procurement whose investment is mandated by food safety regulation rather than discretionary pest management preference, creating consistent procurement independent of rodent infestation severity variation.

Restraints: Environmental and wildlife protection regulations restricting second-generation anticoagulant use

Tightening regulatory restrictions on second-generation anticoagulant rodenticide use near wildlife habitats, in residential areas accessible to non-target species, and in ecologically sensitive agricultural zones create compliance complexity that moderates procurement growth in markets whose regulatory frameworks impose strict application conditions. The EU’s Biocidal Products Regulation’s restriction on consumer use of second-generation products and California’s AB 1788 restricting SGAR use create geographic procurement substitution patterns that increase formulation compliance cost.

Secondary poisoning risk for birds of prey, particularly barn owls and red-tailed hawks that consume poisoned rodents, creates environmental advocacy pressure that motivates regulatory restriction proposals in multiple jurisdictions, creating manufacturer investment in enclosed bait station formats and alternative active ingredient development that addresses non-target poisoning concerns.

Opportunities: Smart pest management technology and emerging market agricultural demand growth

Smart bait station technology integration represents the most commercially premium near-term market enhancement whose real-time rodent activity monitoring, automated bait consumption reporting, and predictive rebaiting recommendation capability create service differentiation for professional pest control operators whose data-driven pest management value proposition sustains premium service contract pricing above commodity rodenticide treatment alternatives.

Emerging market agricultural demand growth in Asia Pacific and Africa where improving food safety standards, expanding grain storage infrastructure, and growing awareness of economic losses from rodent crop damage create first-time structured rodenticide programme adoption from large but previously underserved agricultural demand bases represents the most commercially significant geographic expansion opportunity.

Recent Developments:

-

2024: Syngenta AG extended the reach of its Talon Soft Bait portfolio throughout Southeast Asia in 2024, emphasizing environmentally responsible solutions for urban rodent management and expanding its professional pest control product availability across the region’s growing commercial pest management sector.

-

2024: BASF SE advanced its bait technology development in 2024 with improved moisture resistance and palatability formulations, ensuring consistent anticoagulant rodenticide performance in varied climatic conditions including high-humidity tropical and subtropical agricultural environments.

-

2023: Syngenta launched SecureChoice in October 2023, a smart remote rodent detection system in the UK enabling real-time 24/7 monitoring of rodent activity with proactive alerts and data-driven pest management insights for professional pest control operators.

-

2023: Neogen Corporation launched updated Havoc XT rodenticide bait formulations in 2023 with enhanced palatability and moisture-resistant bait matrix technology improving performance consistency in challenging outdoor agricultural and industrial deployment environments.

-

2023: PelGar International introduced new Racan Place Packs in 2023, pre-filled single-use bait pouches providing convenient, hygienic anticoagulant rodenticide deployment for professional pest controllers without direct contact with the active ingredient, addressing operator safety and ease of use requirements.

Anticoagulant Rodenticides Companies are:

-

BASF SE

-

Neogen Corporation

-

PelGar International Limited

-

Liphatech Inc.

-

JT Eaton & Company Inc.

-

UPL Limited

-

Motomco (Woodstream Corporation)

-

Heranba Industries Ltd.

-

Arbuda Agrochemicals Limited

-

Zapi S.p.A.

-

Sharda Cropchem Limited

-

Ensystex, Inc.

-

Impex Europa S.L.

-

Frowein GmbH & Co. KG

-

Lodi Group

-

Bayer AG

-

Syngenta AG

-

Reckitt Benckiser Group plc

Anticoagulant Rodenticides Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 782.42 Million |

| Market Size by 2035 | USD 1,109.19 Million |

| CAGR | CAGR of 3.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (First-Generation Anticoagulants, Second-Generation Anticoagulants) • By Form (Pellets, Blocks, Powder, Others) • By Application (Agriculture, Pest Control Companies, Warehouses, Residential/Household, Urban Centers, Others) • By Distribution Channel (Online Stores, Specialty Stores, Supermarkets/Hypermarkets, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Bell Laboratories Inc., Neogen Corporation, PelGar International Limited, Liphatech Inc., JT Eaton & Company Inc., UPL Limited, Motomco (Woodstream Corporation), POMAIS Agriculture Co. Ltd., Heranba Industries Ltd., Arbuda Agrochemicals Limited, Zapi S.p.A., Sharda Cropchem Limited, Ensystex, Inc., Impex Europa S.L., Frowein GmbH & Co. KG, Lodi Group, Bayer AG, Syngenta AG, Reckitt Benckiser Group plc. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 3.48% from 2026 to 2035.

Blocks dominated the Anticoagulant Rodenticides Market share in 2025.

North America dominated the Anticoagulant Rodenticides Market in 2025.

Rising urban rodent populations driven by urbanization and changing climate conditions creating consistent urban pest management demand.

The market was valued at USD 782.42 Million in 2025.

Get in Touch