Automotive Safety System Market Report Scope & Overview:

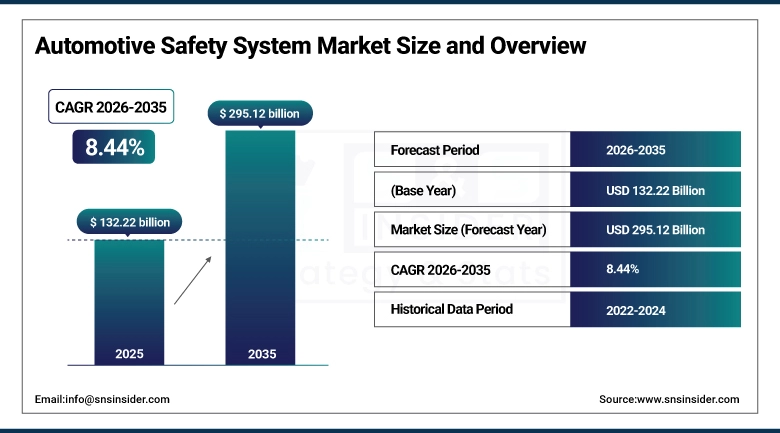

The Automotive Safety System Market was estimated at USD 132.22 Billion in 2025 and is expected to reach USD 295.12 Billion by 2035 and grow at a CAGR of 8.44% over the forecast period of 2026-2035.

The Automotive Safety System Market analysis report includes an in-depth analysis of the market, including its dynamics, technology, and innovations, as well as vehicle safety systems. The increased regulatory environment, rise in the adoption of EVs, growth in the adoption of advanced driver assistance systems, and OEM investment are some of the key factors that are contributing to the growth of the Automotive Safety System Market during the forecast period of 2026-2035.

Automotive safety system installations exceeded 150 billion USD in 2026, led by active safety technologies and accelerating demand across Asia-Pacific.

Market Size & Forecast:

-

Market Size in 2025: USD 132.22 Billion

-

Market Size by 2035: USD 295.12 Billion

-

CAGR: 8.44% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Automotive Safety System Market - Request Free Sample Report

Automotive Safety System Market Trends:

-

Active safety systems dominate because they prevent accidents rather than just mitigating damage.

-

Technologies like ABS, ESC, blind spot detection, and lane departure warning are increasingly mandated worldwide.

-

OEMs are embedding ADAS features even in mid-range vehicles, not just luxury models.

-

Safety systems now include battery monitoring, crash protection, and thermal management.

-

Aftermarket retrofits are gaining traction in emerging markets like India and Brazil, where consumers upgrade older vehicles with ADAS kits.

-

AI-powered predictive safety systems are emerging, using IoT and V2X (vehicle-to-everything) communication.

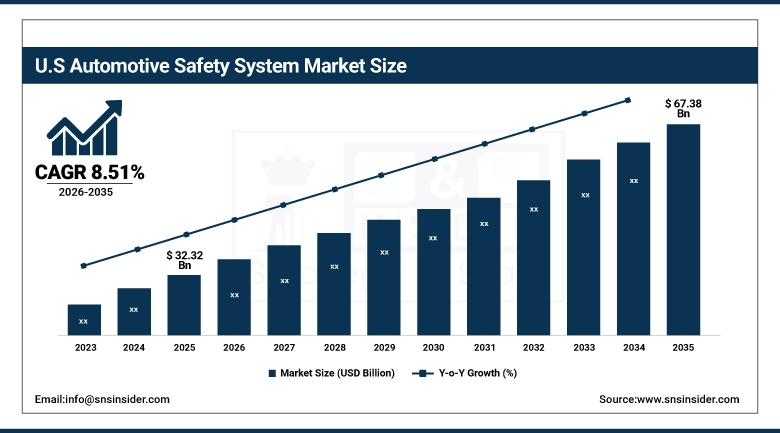

The U.S. Automotive Safety System Market is projected to grow from USD 32.32 Billion in 2025 to USD 67.38 Billion by 2035, at a CAGR of 8.51%. Growth in the US Automotive Safety System Market is attributed to the increased emphasis on NHTSA safety regulations, the rise in the adoption of EVs, the high adoption rate of advanced driver assistance systems, and the focus of OEMs on the development of radar, lidar, and camera-based systems in passenger as well as commercial vehicles.

Automotive Safety System Market Growth Drivers:

-

Stricter global safety regulations and government mandates (airbags, ABS, ESC) are driving widespread adoption of advanced safety technologies.

Increase in penetration of EVs, rise in adoption of ADAS technology, and increasing demand for radar, LiDAR, and camera solutions are the main factors driving the market. OEMs are leading the way in providing OE solutions, and retrofits are also picking up in emerging markets. Advances in active safety solutions, EV crash safety solutions, and connected vehicle solutions are driving the market with healthy growth potential in terms of road safety.

Over 60% of passenger cars and commercial vehicles incorporated advanced active safety systems in 2026, led by ABS, ESC, and ADAS integration.

Automotive Safety System Market Restraints:

-

High costs of advanced sensors such as LiDAR, radar, and cameras significantly raise vehicle prices, limiting adoption in budget segments.

Cybersecurity risks involved with connected safety systems, which use AI, pose a challenge, as well as the lack of standardization across the globe, making it difficult for these safety systems to adhere to different laws and regulations. Furthermore, lack of awareness among consumers, as well as affordability challenges faced by emerging markets, have hindered the growth of this market, as well as the complexity involved in integrating these safety systems, which depends on the availability of supporting infrastructure such as V2X and IoT.

Over 40% of cost-sensitive consumers in emerging markets delayed adoption of advanced safety systems in 2026 due to high sensor costs and affordability challenges, limiting penetration beyond premium vehicle segments.

Automotive Safety System Market Opportunities:

-

Growing EV adoption and the need for specialized safety solutions present significant opportunities, particularly in battery monitoring, crash protection, and thermal management.

The increasing demand for LiDAR and AI-based ADAS solutions is leading to innovation in the field of autonomous driving technology. The development of new markets in countries like India and Brazil is creating opportunities in retrofitting, while original equipment manufacturers are also benefiting from the integration of advanced radar, cameras, and connected vehicles. Moreover, the rise of consumer, government, and industry partnerships is creating safety benefits as well as growth opportunities in passenger as well as commercial vehicles.

Over 65% of new passenger cars sold globally in 2026 integrated advanced ADAS features, creating strong opportunities for OEMs and suppliers to expand EV-specific safety solutions, LiDAR adoption.

Automotive Safety System Market Segmentation Analysis:

-

By Technology, Active Safety Systems segment held the largest market share of 61.46% in 2025, while Blind Spot Detection & Lane Departure Warning segment are expected to grow at the fastest CAGR of 10.87% during 2026–2035.

-

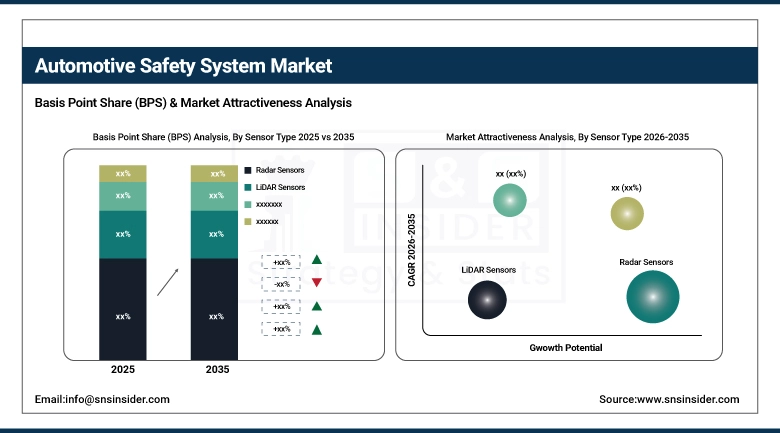

By Sensor Type, Radar Sensors segment dominated with 36.55% market share in 2025, whereas LiDAR Sensors are projected to record the fastest CAGR of 12.98% through 2026–2035.

-

By Vehicle Type, Passenger Cars segment accounted for the highest market share of 66.12% in 2025, while Heavy Commercial Vehicles (HCVs) segment is expected to grow at the fastest CAGR of 9.71% during the forecast period.

-

By Propulsion Type, ICE Vehicles segment dominated with a 69.72% share in 2025, while Battery EVs segment is anticipated to expand at the fastest CAGR of 12.64% through 2026–2035.

-

By End Market, Original Equipment Manufacturer (OEM) segment held the largest share of 86.72% in 2025, while Aftermarket are expected to grow at the fastest CAGR of 9.64% during the forecast period.

By Technology, Active Safety Systems Dominate While Blind Spot Detection & Lane Departure Warning Grow Rapidly:

The Active Safety Systems segment has been dominating the market of the automotive safety system market, which is due to the implementation of strict regulations in the global market, as well as the implementation of active safety systems in vehicles by OEMs. In 2026, more than 60% of the vehicles were equipped with active safety systems, which is an indication of the importance of the safety system in preventing accidents.

The Blind Spot Detection and Lane Departure Warning segment is expected to grow at a rapid pace in the market of the automotive safety system market, which is due to the implementation of regulations that are focused on reducing the risks of accidents involving vehicles.

By Sensor Type, Radar Sensors Dominate While LiDAR Sensors Grow Rapidly:

The Radar Sensors segment held the largest share in the market owing to their affordability and reliability in adaptive cruise control, collision avoidance, and blind spot detection. Improvements in short-range radars for urban driving and parking assist have increased their use, which is essential in compact and mid-range segments of automobiles.

The LiDAR Sensors segment is growing at the fastest rate in the market. This is because of autonomous driving programs, premium EVs, and the need for high-resolution environmental mapping. Their use in achieving full self-driving capabilities is critical in this growth. LiDAR costs are reducing, and technology is getting compact.

By Vehicle Type, Passenger Cars Dominate While Heavy Commercial Vehicles Grow Rapidly:

Passenger Cars dominated the market share, driven by strong OEM adoption of ABS, ESC, airbags, and ADAS. The dominance of Passenger Cars is further driven by increased consumer awareness, mandatory safety compliance for vehicle manufacturers, and increased adoption of EVs equipped with sophisticated safety features.

Heavy Commercial Vehicles (HCVs) is the fastest-growing segment, driven by increased investments in vehicle safety, stringent government regulations for road transport, and increased adoption of sophisticated collision avoidance and driver monitoring solutions. The fast adoption rate of this vehicle type emphasizes the significance of vehicle safety.

By Propulsion Type, ICE Vehicles Dominate While Battery EVs Expand Rapidly:

The Internal Combustion Engine (ICE) Vehicles segment held a dominant share in the market, driven by their presence in the global marketplace, existing infrastructure, and integration of safety systems. Their availability in the aftermarkets and relatively lower prices compared to EVs contributed to their popularity, thus ensuring demand for these vehicles in both developed and developing nations despite the rise in regulatory pressure on emissions.

Battery Electric Vehicles (BEVs) segment anticipated to expand at the fastest pace, fuelled by government incentives, stricter emission regulations, and rising consumer preference for sustainable mobility. EV-specific safety innovations, such as advanced battery crash protection and thermal management, are accelerating adoption and differentiating this segment.

By End Market, OEMs Lead While Aftermarket Gains Momentum:

The Original Equipment Manufacturers (OEMs) segment dominated the market, considering the safety systems installed in the vehicle as original equipment. This dominance of the OEMs segment is further emphasized by the R&D activities carried out by the OEMs segment in partnership with the manufacturers of sensors, as well as the incorporation of AI-based ADAS systems, and the use of the connected vehicle platform for updating the safety systems through OTA software updates.

Aftermarket segment is fastest growing segment, with growth being fueled by the demand for retrofitting in emerging markets, consumer awareness, and upgrade focus on cost-effectiveness. The growing penetration of aftermarket ADAS kits in older vehicles and commercial fleets points to opportunities that remain untapped by safety system suppliers. The development of e-commerce platforms is facilitating easier access to safety solutions.

Regional Insights

North America Automotive Safety System Market Insights:

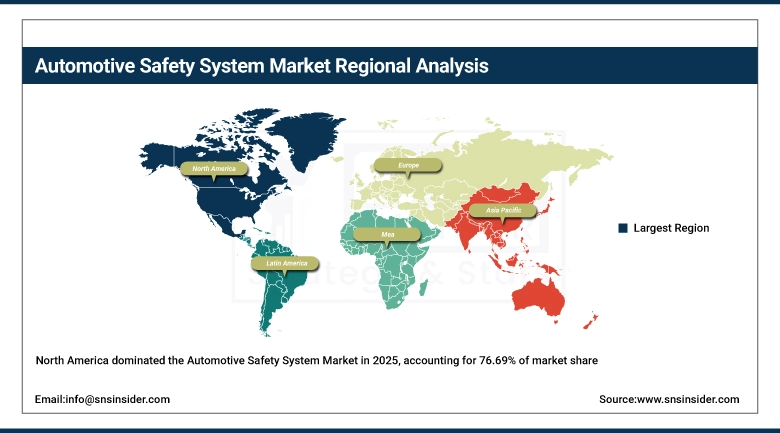

The North America Automotive Safety System Market accounted for the largest share in the global market, with a 76.69% market share in 2025. This is because of the stringent regulations, advanced OEM integrations, and increased consumer awareness in the US and Canadian markets. The region has witnessed robust adoption of radar, camera, and ADAS solutions in passenger and commercial vehicles. In addition, the increasing adoption of EVs and the need for connected and autonomous driving features are driving the market. Moreover, continuous innovations in LiDAR, AI-powered driver monitoring, and over-the-air (OTA) safety solutions, and supportive government initiatives are adding strength to the North American market.

The U.S. Automotive Safety System Market is driven by the implementation of NHTSA safety regulations, the well-developed auto industry, and the wide acceptance of ABS, ESC, ADAS, and connected safety solutions by original equipment manufacturers. The increasing acceptance of EVs, premium vehicles, and autonomous driving solutions has helped the U.S. retain its position as the market leader in North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Automotive Safety System Market Insights:

The Asia-Pacific Automotive Safety System Market is growing at the fastest rate, with a CAGR of 10.11% during 2026-2035. The Asia-Pacific Automotive Safety System Market is growing rapidly due to the ever-increasing vehicle production rates, growing middle-class consumer demand, and safety regulations in countries such as China, India, Japan, and South Korea. The growing use of ADAS features, radar, and camera-based automotive safety systems in passenger as well as commercial vehicles is boosting this market segment. The growing OEMs, along with the ever-increasing electric vehicle sales and smart mobility projects, is another significant factor that is boosting this market segment. The growing investments in LiDAR, AI-based driver monitoring, and connected vehicles, as well as government-backed road safety drives, are also boosting this segment in terms of growth.

China Market Insights:

China dominates the Asia-Pacific market, driven by its large automotive industry, adoption of EVs, and government regulations promoting advanced safety features. The integration of various safety features, such as ABS, ESC, airbags, and ADAS, by local as well as international brands has given this market segment a significant boost. Increased consumer awareness, combined with smart city projects and autonomous driving projects, is set to take this segment to the next level.

Europe Automotive Safety System Market Insights:

The Europe Automotive Safety System Market is one of the most advanced markets with stringent regulations, accounting for a considerable share in 2025. The stringent safety regulations by the European Union, such as Euro NCAP, have significantly fueled the adoption of advanced safety features by automotive manufacturers, such as ABS, ESC, airbags, and ADAS. The growing need for connected as well as autonomous vehicles, along with a high adoption rate of EVs, is another reason that will contribute to the growth of this market. The growing innovation in LiDAR, AI-based driver monitoring, as well as V2X communication, makes Europe one of the leading markets in automotive safety innovation, with a focus on sustainable mobility.

Germany Market Insights:

Germany leads the way in the European region, driven by the presence of a strong auto-manufacturing industry and premium export vehicles. The country is home to some of the world’s top auto brands, including Volkswagen, BMW, and Mercedes-Benz. These auto brands are at the forefront of using the latest and best technology available for vehicle safety. The rising sales of EVs, government-backed vehicle safety regulations, and investments in autonomous vehicle technology also play an important role.

Latin America Automotive Safety System Market Insights:

The Latin America Automotive Safety System Market is growing steadily, driven by the rise in automobile sales, increased consumer knowledge, and government efforts to promote road safety. Brazil and Mexico dominate the region, with OEM adoption of ABS, ESC, and airbags in passenger vehicles rising steadily. Economic growth and urbanization are fueling the adoption of ADAS technologies, and aftermarket installations are also becoming popular in older vehicles. Though the region faces challenges in terms of affordability and regulatory enforcement, constant investment in connected car technology and EVs continues to fuel the growth of the market.

Middle East & Africa Automotive Safety System Market Insights:

The Middle East & Africa Automotive Safety System Market is at the emerging stage with high growth prospects due to the rising rate of automobile imports and premium automobile sales, as well as the initiatives taken by the government to maintain road safety. In the Middle East region, the Gulf Cooperation Countries such as Saudi Arabia and the UAE are at the forefront in adopting automobile safety systems due to the high demand for luxury cars. In the African region, South Africa is also at the emerging stage with high growth prospects in automobile safety systems.

Competitive Landscape:

Robert Bosch GmbH is a German multinational engineering and technology company, recognized as the global leader in automotive safety systems. Bosch offers a comprehensive portfolio including ABS, ESC, radar sensors, and ADAS solutions, widely adopted across passenger cars and commercial fleets. Its dominance is reinforced by strong OEM partnerships, extensive R&D investments, and leadership in connected and autonomous driving technologies. Bosch’s innovations in radar, camera, and LiDAR integration, along with over-the-air (OTA) safety updates, strengthen its competitive edge.

-

In September 2025, Bosch announced the launch of its next-generation 4D radar sensors, designed to enhance autonomous driving accuracy and improve collision avoidance in complex urban environments.

Continental AG is a major German automotive supplier, holding a leading position in active and passive safety systems. Continental’s portfolio spans braking systems, LiDAR, radar, camera modules, and integrated ADAS platforms. Its strong presence in Europe, North America, and Asia-Pacific reinforces its global leadership. The company’s focus on sustainability, EV safety solutions, and AI-driven driver monitoring systems has accelerated adoption among OEMs.

-

In November 2025, Continental unveiled its advanced LiDAR sensor developed in partnership with AEye, aimed at enabling Level 4 autonomous driving capabilities in premium EVs.

ZF Friedrichshafen AG is a German multinational specializing in automotive safety, driveline, and chassis technologies. ZF is a global leader in airbags, seatbelts, and advanced driver-assistance systems, with strong OEM collaborations across Europe, the U.S., and Asia. Its integration of passive and active safety systems, combined with AI-powered driver monitoring, positions ZF as a key innovator in the market. The company’s investments in autonomous mobility and EV-specific safety solutions further reinforce its competitive strength.

-

In October 2025, ZF introduced its new integrated safety platform combining airbags, seatbelts, and ADAS sensors, designed to provide holistic protection for both conventional and electric vehicles.

Automotive Safety System Market Key Players:

-

Robert Bosch GmbH

-

Continental AG

-

ZF Friedrichshafen AG

-

Autoliv Inc.

-

Denso Corporation

-

Aptiv PLC

-

Magna International Inc.

-

Valeo SA

-

Hyundai Mobis Co. Ltd

-

Hitachi Astemo Ltd.

-

NXP Semiconductors

-

Infineon Technologies AG

-

Texas Instruments

-

Renesas Electronics Corporation

-

Panasonic Automotive Systems

-

Mobileye (Intel)

-

Nvidia Corporation

-

Hella GmbH & Co. KGaA

-

Johnson Controls

-

Mando Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 132.22 Billion |

| Market Size by 2035 | USD 295.12 Billion |

| CAGR | CAGR of 8.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Active Safety Systems, Anti-Lock Braking System (ABS), Blind Spot Detection & Lane Departure Warning, Electronic Stability Control (ESC, Others) • By Sensor Type (Radar Sensors, LiDAR Sensors, Camera Sensors, Ultrasonic Sensors, Others) • By Vehicle Type (Passenger Cars, Heavy Commercial Vehicles (HCV), Light Commercial Vehicles (LCV), Buses & Coaches, Others) • By Propulsion Type (ICE Vehicles, Battery EVs, Hybrid EVs, Plug-in Hybrid, Fuel Cell EV, Others) • By End Market (Original Equipment Manufacturer (OEM), Aftermarket, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Autoliv Inc., Denso Corporation, Aptiv PLC, Magna International Inc., Valeo SA, Hyundai Mobis Co. Ltd, Hitachi Astemo Ltd., NXP Semiconductors, Infineon Technologies AG, Texas Instruments, Renesas Electronics Corporation, Panasonic Automotive Systems, Mobileye (Intel), Nvidia Corporation, Hella GmbH & Co. KGaA, Johnson Controls, Mando Corporation. |

Frequently Asked Questions

Top players include Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG.

North America with market share of 31.87% among US with 76.69% with safety regulations and high OEM adoption.

Radar sensors measure distant and speed of objects, LiDAR provide High-resolution 3D mapping.

Passenger Cars account for the largest share i.e. 66.12%, supported by mass production, regulatory mandates, and widespread adoption of ABS, ESC, airbags, and ADAS features.

The market is primarily driven by strict government regulations, rising consumer awareness, and increasing OEM integration of advanced driver-assistance systems (ADAS).

Get in Touch