Biological Buffers Market Report Scope & Overview:

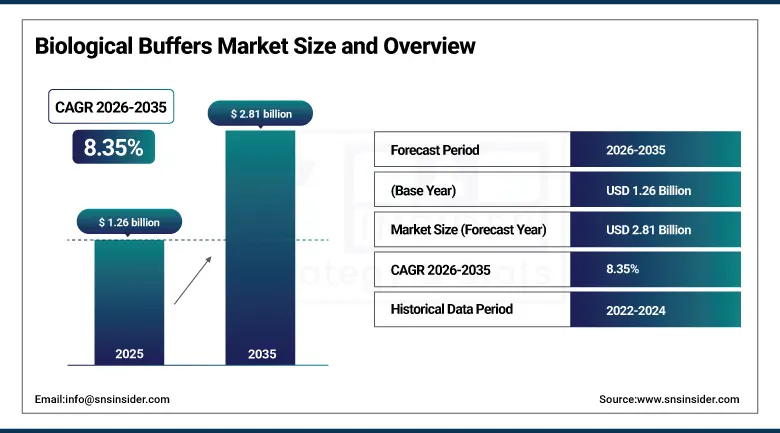

The Biological Buffers Market is valued at USD 1.26 billion in 2025 and is expected to reach USD 2.81 billion by 2035, growing at a CAGR of 8.35% from 2026-2035.

The biological buffers market is growing rapidly due to increasing biopharmaceutical production, rising demand for vaccines, and expanding cell and gene therapy research. Greater adoption of biologics, continuous advancements in life science research, and higher investment in biotechnology and pharmaceutical R&D are driving buffer consumption. In addition, growth in diagnostic testing, protein purification, and molecular biology applications, along with stricter quality standards in biomanufacturing, is accelerating demand for high-purity and customized biological buffer solutions.

83% of biopharma and research labs prioritized high-purity, customized biological buffers driven by vaccine production, cell and gene therapy advances, and stringent biomanufacturing standards propelling global market growth.

Biological Buffers Market Size and Forecast:

-

Market Size in 2025: USD 1.26 Billion

-

Market Size by 2035: USD 2.81 Billion

-

CAGR: 8.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Biological Buffers Market - Request Free Sample Report

Biological Buffers Market Trends:

-

Rising demand for stable pH control solutions across biopharmaceutical manufacturing and life science research applications

-

Increasing use of biological buffers in cell culture, protein purification, and vaccine development processes

-

Growing adoption of high-purity and custom buffer formulations to support sensitive biologics and diagnostic workflows

-

Expansion of biotechnology and pharmaceutical R&D activities driving consistent consumption of biological buffering agents

-

Rising focus on reproducibility and assay reliability increasing demand for standardized biological buffer solutions

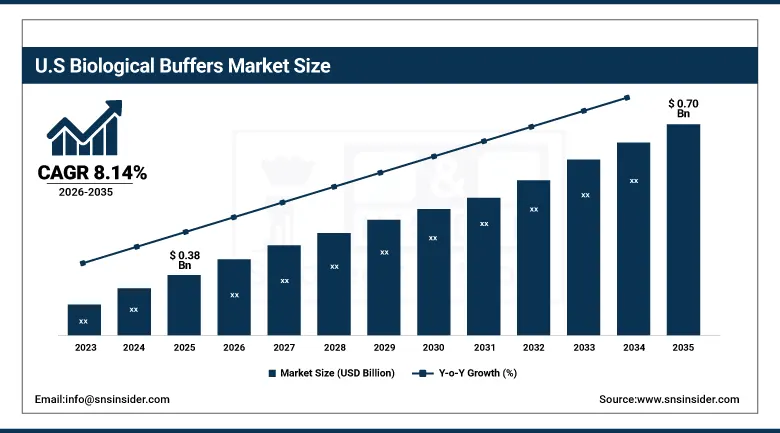

U.S. Biological Buffers Market is valued at USD 0.38 billion in 2025 and is expected to reach USD 0.70 billion by 2035, growing at a CAGR of 8.14% from 2026-2035.

The U.S. biological buffers market is driven by strong biopharmaceutical manufacturing, rising biologics and vaccine development, and expanding cell and gene therapy research. Increased R&D spending, growth in diagnostic testing, and stringent regulatory standards are boosting demand for high-quality, reliable buffer solutions.

Biological Buffers Market Growth Drivers:

-

Rising investments in biopharmaceutical research, drug development, and life sciences are driving strong demand for high-purity biological buffers across laboratories globally

Global investments in biopharmaceutical research and life sciences have increased significantly, driven by rising demand for advanced therapeutics, biologics, and precision medicines. Biological buffers play a critical role in maintaining optimal pH and stability during drug formulation, protein analysis, and biochemical reactions. Pharmaceutical companies, research institutes, and academic laboratories require high-purity buffers to ensure experimental accuracy and regulatory compliance. Increased funding for R&D, expansion of biotech startups, and growth of contract research organizations is collectively accelerating demand for reliable biological buffer solutions across diverse laboratory environments worldwide.

81% of global laboratories reported increased demand for high-purity biological buffers fueled by surging investments in biopharmaceutical R&D, drug discovery, and life sciences innovation.

-

Growing use of biological buffers in cell culture, protein purification, and diagnostic applications is accelerating market growth across academic, clinical, and industrial research settings

Biological buffers are essential components in cell culture media, protein purification processes, and in vitro diagnostic assays. Their ability to maintain stable chemical environments ensures consistency and reliability in experimental outcomes. The rising adoption of cell-based research, recombinant protein production, and molecular diagnostics has increased buffer consumption across laboratories. Clinical diagnostics and industrial bioprocessing facilities increasingly rely on standardized buffers to improve reproducibility and efficiency. As research activities expand across academic institutions and commercial laboratories, the widespread application of biological buffers continues to drive sustained market growth.

79% of academic, clinical, and industrial research facilities increased biological buffer usage driving market growth through expanded applications in cell culture, protein purification, and diagnostics.

Biological Buffers Market Restraints:

-

High costs associated with high-purity buffer formulations and stringent quality standards limit affordability and adoption among small laboratories and research institutes

Producing high-purity biological buffers requires stringent quality control, specialized raw materials, and advanced manufacturing processes. These factors significantly increase production costs, resulting in higher prices for end users. Small laboratories, academic institutions, and budget-constrained research facilities often struggle to afford premium buffer solutions, limiting widespread adoption. Additionally, compliance with regulatory and quality standards adds to operational expenses. Cost sensitivity among smaller end users can restrict market penetration, particularly in developing regions, making affordability a key challenge for manufacturers seeking to expand their customer base.

68% of small labs and research institutes limited buffer usage due to high costs of high-purity formulations and stringent quality requirements, hindering experimental scalability and reproducibility.

-

Storage stability challenges and limited shelf life of certain biological buffers increase handling complexities and operational costs for manufacturers and end users

Many biological buffers are sensitive to temperature, light, and contamination, leading to limited shelf life and stability concerns. Improper storage conditions can cause degradation, reduced effectiveness, or contamination, increasing the risk of experimental failure. Manufacturers must invest in specialized packaging, preservation methods, and logistics to maintain buffer quality. End users also face challenges related to cold storage, inventory management, and frequent replacement. These handling complexities increase operational costs and can discourage bulk purchasing, posing a restraint on market efficiency and broader adoption of biological buffers.

65% of labs and manufacturers faced higher operational costs due to the limited shelf life and storage instability of biological buffers requiring cold-chain logistics, frequent reordering, and rigorous inventory management.

Biological Buffers Market Opportunities:

-

Expansion of biologics, biosimilars, and vaccine manufacturing creates significant opportunities for biological buffer suppliers to support large-scale production processes globally

The rapid growth of biologics, biosimilars, and vaccine production has created substantial demand for biological buffers used in upstream and downstream bioprocessing. Buffers are essential for maintaining optimal conditions during fermentation, purification, and formulation stages. Large-scale manufacturing facilities require consistent, high-quality buffer solutions to meet regulatory standards and ensure product safety. As pharmaceutical companies expand production capacities globally, buffer suppliers have opportunities to establish long-term supply agreements, develop scalable formulations, and support growing demand across commercial biomanufacturing operations.

In 2025, 76% of biological buffer suppliers expanded capacity to meet surging global demand from biologics, biosimilars, and vaccine manufacturing enabling scalable, compliant, and high-yield production processes.

-

Advancements in customized and ready-to-use buffer solutions offer opportunities to improve workflow efficiency and attract time-sensitive pharmaceutical and research laboratories

Laboratories increasingly prefer customized and ready-to-use buffer solutions to reduce preparation time, minimize errors, and improve workflow efficiency. Advances in formulation technologies allow suppliers to offer pre-mixed, sterile, and application-specific buffers tailored to customer requirements. These solutions are particularly attractive to pharmaceutical manufacturers and high-throughput research labs operating under tight timelines. Ready-to-use buffers enhance reproducibility, reduce labor costs, and improve compliance with quality standards. Growing demand for convenience and operational efficiency presents strong opportunities for buffer manufacturers to differentiate products and strengthen customer relationships.

In 2025, 71% of pharmaceutical and research labs adopted advanced ready-to-use buffer solutions reducing preparation time by 40% and accelerating time-sensitive workflows without compromising precision.

Biological Buffers Market Segment Highlights:

-

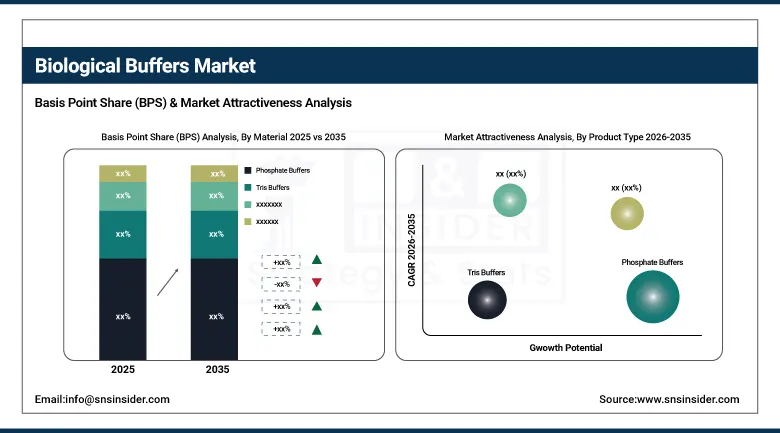

By Product Type: Phosphate Buffers led with 39.6% share, while HEPES Buffers are the fastest-growing segment with CAGR of 11.8%.

-

By Form: Powder led with 52.4% share, while Liquid is the fastest-growing segment with CAGR of 10.9%.

-

By Application: Cell Culture led with 41.7% share, while Biopharmaceutical Manufacturing is the fastest-growing segment with CAGR of 12.3%.

-

By End User: Biopharmaceutical Companies led with 44.8% share, while Contract Research Organizations (CROs) are the fastest-growing segment with CAGR of 11.6%.

Biological Buffers Market Segment Analysis:

By Product Type: Phosphate Buffers led, while HEPES Buffers are the fastest-growing segment.

Phosphate buffers dominate the biological buffers market due to their wide compatibility with biological systems, stable pH control, and extensive use across cell culture, molecular biology, and diagnostic workflows. Their cost-effectiveness, ease of preparation, and regulatory familiarity make them the preferred choice for both research and commercial biomanufacturing environments. Phosphate buffers are routinely used in large volumes, supporting consistent demand from laboratories and biopharmaceutical producers. Their broad applicability across upstream and downstream processes continues to reinforce their dominant market position.

HEPES buffers are the fastest-growing product type due to their superior buffering capacity in physiological pH ranges and strong performance under open-air and temperature-variable conditions. Increasing adoption in advanced cell culture systems, gene therapy research, and sensitive biologics manufacturing is driving growth. Researchers favor HEPES for applications requiring high precision and minimal pH drift, particularly in mammalian cell cultures. Rising investment in cell-based therapies, regenerative medicine, and precision biologics is accelerating demand for high-performance buffers like HEPES.

By Form: Powder led, while Liquid is the fastest-growing segment.

Powdered buffers dominate the market because of their long shelf life, ease of storage, and cost efficiency for bulk laboratory and manufacturing use. They are widely preferred by biopharmaceutical companies and research institutes that require large-scale buffer preparation with flexible concentration control. Powder forms reduce transportation costs and minimize stability concerns, making them ideal for global supply chains. Their compatibility with automated buffer preparation systems further enhances adoption, especially in high-throughput research and industrial bioprocessing environments.

Liquid buffers are the fastest-growing form due to increasing demand for ready-to-use solutions that improve operational efficiency and reduce preparation errors. Growth is driven by time-sensitive laboratory workflows, diagnostic testing, and GMP-compliant biomanufacturing processes where consistency is critical. Liquid buffers eliminate weighing and mixing steps, enabling faster turnaround and improved reproducibility. Rising outsourcing of research, expanding diagnostic testing volumes, and the shift toward standardized, pre-formulated solutions are significantly boosting demand for liquid biological buffers.

By Application: Cell Culture led, while Biopharmaceutical Manufacturing is the fastest-growing segment.

Cell culture dominates buffer consumption as it is foundational to biological research, drug discovery, vaccine development, and biopharmaceutical production. Buffers are essential for maintaining optimal pH, osmolarity, and cell viability throughout culture processes. Expanding use of mammalian cell lines, stem cell research, and recombinant protein production sustains high buffer demand. The rapid growth of biologics, monoclonal antibodies, and cell therapies continues to position cell culture as the largest and most consistent application segment within the biological buffers market.

Biopharmaceutical manufacturing is the fastest-growing application due to rising global production of biologics, biosimilars, and advanced therapies. Buffers play a critical role in upstream fermentation, downstream purification, formulation, and fill-finish operations. Increasing regulatory emphasis on process consistency and quality control is driving higher buffer consumption. Expansion of large-scale manufacturing facilities, particularly in Asia, along with strong investment in biologics pipelines, is accelerating buffer demand across commercial production environments.

By End User: Biopharmaceutical Companies led, while Contract Research Organizations are the fastest-growing segment.

Biopharmaceutical companies dominate the end-user segment because they consume buffers across the entire product lifecycle, from early-stage research to commercial-scale manufacturing. Their continuous production requirements, stringent quality standards, and reliance on reproducible buffer systems generate sustained demand. The rapid growth of biologics, vaccines, and cell-based therapies has further increased buffer usage intensity. Large production volumes, global manufacturing footprints, and long-term supply contracts reinforce the dominant position of biopharmaceutical companies in the biological buffers market.

Contract Research Organizations are the fastest-growing end-user segment due to increasing outsourcing of drug discovery, development, and analytical testing activities. Pharmaceutical and biotech companies are relying more on CROs to reduce costs and accelerate timelines, driving higher buffer consumption in outsourced laboratories. CROs support diverse applications including cell culture, molecular biology, and bioanalytical testing, requiring consistent buffer supply. Expansion of CRO operations in Asia and emerging markets further supports strong growth in this segment.

Biological Buffers Market Regional Analysis:

North America Biological Buffers Market Insights:

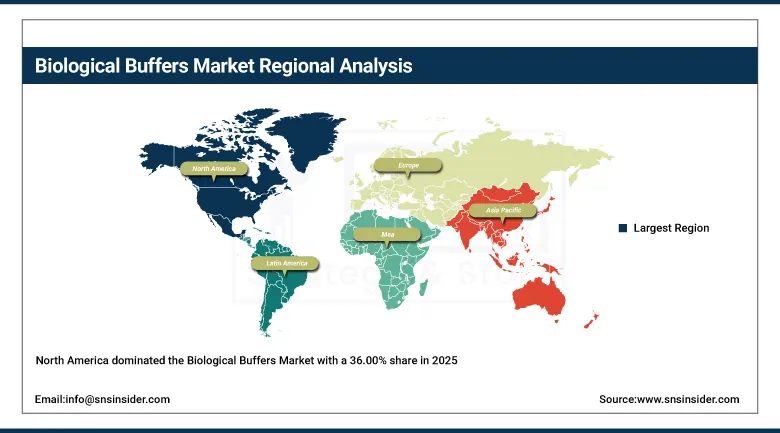

North America dominated the Biological Buffers Market with a 36.00% share in 2025 due to strong biopharmaceutical manufacturing capacity, high R&D spending, and the presence of leading life sciences companies. Widespread adoption of advanced cell culture, protein purification, and molecular biology techniques, supported by well-established regulatory and research infrastructure, reinforced regional market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Biological Buffers Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 10.39% from 2026–2035, driven by expanding biopharmaceutical production, rising research activities, and increasing investments in biotechnology and life sciences. Growth in contract research and manufacturing organizations, improving laboratory infrastructure, and government support for biotech innovation are accelerating market expansion across the region.

Europe Biological Buffers Market Insights

Europe held a significant share in the Biological Buffers Market in 2025, supported by strong pharmaceutical and biotechnology industries, extensive academic and clinical research activities, and well-established laboratory infrastructure. Stringent quality standards, growing bioprocessing applications, and continuous investments in life sciences R&D further strengthened Europe’s market position.

Middle East & Africa and Latin America Biological Buffers Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Biological Buffers Market in 2025, driven by expanding healthcare and research infrastructure, increasing adoption of biopharmaceutical manufacturing, and rising demand for laboratory reagents. Growing investments in life sciences, development of research institutes, and gradual expansion of contract research activities supported regional market growth.

Biological Buffers Market Competitive Landscape:

Thermo Fisher Scientific Inc. is a global leader in life sciences and analytical solutions, offering a comprehensive portfolio of biological buffers for research, diagnostics, and biopharmaceutical manufacturing. The company supports applications across molecular biology, cell culture, protein purification, and clinical testing. Its strong focus on quality, consistency, and regulatory compliance makes it a preferred supplier for academic, industrial, and clinical laboratories worldwide. Continuous innovation, global distribution capabilities, and extensive technical support strengthen its position in the biological buffers market.

-

April 2024, Thermo Fisher launched the Connect Lab Intelligence Platform, a unified digital ecosystem that integrates instruments, data, and supplies across the lab workflow.

Merck KGaA, operating through its Life Science business, is a prominent supplier of high-purity biological buffers used in research, pharmaceutical development, and bioprocessing applications. The company provides a broad range of buffers supporting cell culture, chromatography, and analytical workflows. Merck emphasizes stringent quality standards, reliability, and regulatory alignment, serving academic institutions and biopharmaceutical companies globally. Its strong R&D capabilities and global manufacturing network enhance its competitiveness in advanced biological and life science markets.

-

November 2023, Merck KGaA (operating its life science business as MilliporeSigma) launched GreenLab, a comprehensive program offering eco-designed reagents, solvents, and lab plastics with verified sustainability metrics.

Avantor, Inc. is a leading global provider of mission-critical products and services to the life sciences and advanced technology industries, including a wide range of biological buffers. Its offerings support biopharmaceutical production, laboratory research, and quality control applications. Avantor focuses on high-performance materials, consistent quality, and supply chain reliability. With a strong global presence and customer-centric approach, the company plays a vital role in enabling scientific innovation and regulated laboratory operations worldwide.

-

February 2025, Avantor enhanced its VWR Intelligence Platform with an AI Procurement Assistant that streamlines lab supply ordering and compliance.

Biological Buffers Market Key Players:

-

Thermo Fisher Scientific Inc.

-

Merck KGaA

-

Avantor, Inc.

-

Lonza Group AG

-

FUJIFILM Irvine Scientific, Inc.

-

Bio-Rad Laboratories, Inc.

-

Takara Bio Inc.

-

GE Healthcare Life Sciences (Cytiva)

-

PAN-Biotech GmbH

-

MP Biomedicals, LLC

-

Gold Biotechnology, Inc.

-

Spectrum Chemical Manufacturing Corp.

-

Alfa Aesar (Thermo Fisher Scientific)

-

HiMedia Laboratories, Inc.

-

Carl Roth GmbH + Co. KG

-

AppliChem GmbH

-

Tokyo Chemical Industry Co., Ltd. (TCI)

-

Sisco Research Laboratories Pvt. Ltd. (SRL)

-

Santa Cruz Biotechnology, Inc.

-

Promega Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.26 Billion |

| Market Size by 2035 | USD 2.81 Billion |

| CAGR | CAGR of 8.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Phosphate Buffers, Tris Buffers, HEPES Buffers, Citrate Buffers, Acetate Buffers) • By Form (Powder, Liquid, Tablets) • By Application (Cell Culture, Protein Purification, Molecular Biology, Biopharmaceutical Manufacturing, Diagnostic Testing) • By End User (Biopharmaceutical Companies, Academic & Research Institutes, Contract Research Organizations (CROs), Diagnostic Laboratories, Hospitals & Clinical Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Merck KGaA, Avantor, Inc., Lonza Group AG, FUJIFILM Irvine Scientific, Inc., Bio-Rad Laboratories, Inc., Takara Bio Inc., GE Healthcare Life Sciences (Cytiva), PAN-Biotech GmbH, MP Biomedicals, LLC, Gold Biotechnology, Inc., Spectrum Chemical Manufacturing Corp., Alfa Aesar (Thermo Fisher Scientific), HiMedia Laboratories, Inc., Carl Roth GmbH + Co. KG, AppliChem GmbH, Tokyo Chemical Industry Co., Ltd. (TCI), Sisco Research Laboratories Pvt. Ltd. (SRL), Santa Cruz Biotechnology, Inc., Promega Corporation |

Frequently Asked Questions

Key drivers include rising demand for biopharmaceuticals, growth in life sciences research, increasing use in cell culture, and advancements in biotechnology.

Biological buffers are chemical solutions that maintain stable pH levels in biological and chemical processes, which is critical for enzyme activity, cell culture, and drug formulation.

The Biological Buffers Market is projected to grow at a CAGR of 8.35% during the forecast period from 2026 to 2035.

The market is expected to reach USD 2.81 billion by 2035, driven by increasing research activities and biopharmaceutical production.

The Biological Buffers Market is valued at USD 1.26 billion in 2025, reflecting steady demand across biotechnology, pharmaceuticals, and research applications.

Get in Touch