Candle Market Report Scope & Overview:

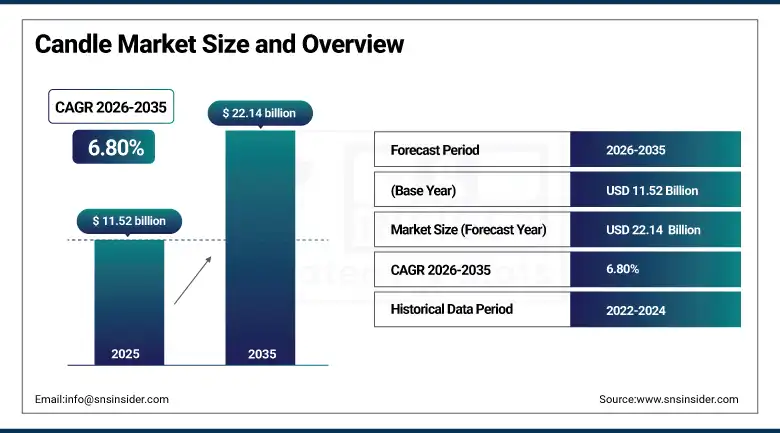

The Candle Market was valued at USD 11.52 Billion in 2025 and is expected to reach USD 22.14 Billion by 2035, growing at a CAGR of 6.80% from 2026–2035.

The global candle market has evolved far beyond its historical identity as a functional light source into a multidimensional lifestyle category sitting at the intersection of home fragrance, wellness, interior decoration, ceremonial tradition, and self-care. Candles today serve as therapeutic tools, aesthetic objects, gifting staples, and atmospheric anchors in residential spaces, hospitality environments, and commercial settings whose collective demand sustains a market that is proving remarkably resilient to discretionary spending pressures because of the deeply personal and emotionally resonant role candles play in consumers’ daily routines and celebratory occasions. The market’s structural transformation over the past decade has been driven by the explosive growth of the scented candle segment, whose convergence with the mainstream wellness movement has made fragrance-led candles an affordable luxury that a broad demographic of middle-class consumers across North America, Europe, and increasingly Asia Pacific now purchases regularly as a self-care investment rather than an occasional indulgence. Social media platforms, particularly Instagram, Pinterest, and TikTok, have played an extraordinary role in amplifying candle culture, as aesthetic home environment content featuring lit candles as central mood-setting elements consistently generates high engagement and creates commercial pull for brands whose visual and olfactory identity is communicated through the digital content of influencers, interior designers, and lifestyle creators who have collectively normalised candle investment as a standard component of thoughtfully curated domestic space.

The National Candle Association’s annual survey confirming that approximately 35% of all candle sales in the United States occur during the holiday season, driven by gifting, home entertainment hosting, and the deep cultural associations of candlelight with warmth, celebration, and seasonal tradition, underscores the category’s extraordinary seasonal demand elasticity and the commercial importance of new product launches timed to capture the heightened consumer attention and spending willingness of the October through December gifting window.

Market Size and Forecast

-

Market Size in 2026E: USD 12.30 Billion

-

Market Size by 2035: USD 22.14 Billion

-

CAGR: 6.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Candle Market - Request Free Sample Report

Candle Market Trends

-

Rising consumer demand for clean-burning natural wax candles made from soy, beeswax, and coconut wax formulations that eliminate the petroleum-derived particulates and potential volatile organic compound emissions associated with standard paraffin wax combustion, driven by health consciousness, sustainability commitments, and the strong commercial pull of natural ingredient positioning in the wellness and eco-conscious consumer segments that are growing fastest within the premium candle category.

-

Expanding personalisation and customisation offerings across the candle market, including made-to-order fragrance blending services, custom vessel design programmes, personalised label printing for gifting applications, and subscription box models delivering curated seasonal or mood-matched candle collections to subscribers who value the curation and discovery experience over standard retail purchasing.

-

Growing adoption of luxury and premium candle positioning as independent artisan candle brands and established premium fragrance houses including Diptyque, Jo Malone, NEST New York, and Maison Margiela Replica extend their brand authority into home fragrance through candle collections whose premium packaging, complex multi-note fragrance architecture, and brand storytelling justify price points that growing numbers of aspirational consumers are willing to pay as luxury accessible substitutes for fashion and jewellery expenditure.

-

Accelerating shift toward online retail and direct-to-consumer brand building as the candle market’s commercial landscape is transformed by e-commerce accessibility, with digital-native brands building loyal customer bases through Instagram storytelling, TikTok unboxing content, subscription services, and Shopify-powered direct commerce that bypass the traditional wholesale retail gatekeeping that previously limited candle market access for small and independent producers.

-

Rising commercial and hospitality sector adoption of custom-branded candles as scent-signature brand identity tools, with hotels, spas, restaurants, and luxury retail environments commissioning signature fragrance candle programmes whose ambient scent delivery creates memorable sensory brand associations and whose retail availability as branded take-home products generates incremental revenue and brand affinity among customers whose positive experiential associations with the scent motivate purchase.

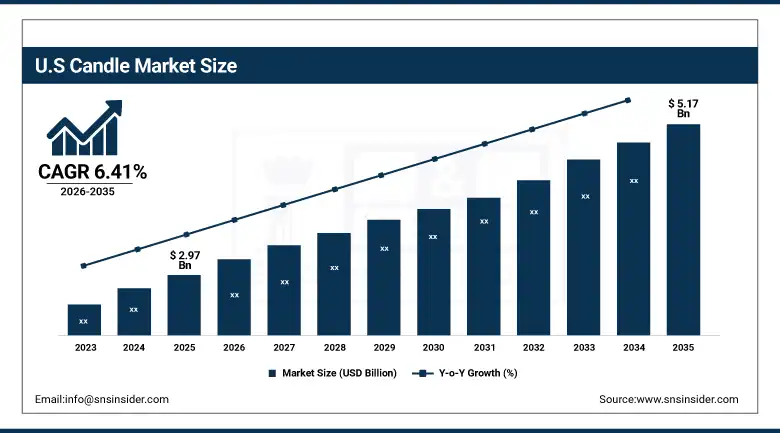

U.S. Candle Market Outlook

The U.S. Candle Market was valued at approximately USD 2.97 Billion in 2025 and is expected to reach approximately USD 5.17 Billion by 2035, growing at a CAGR of 6.41%.

The United States represents the world’s largest and most commercially sophisticated candle market, anchored by a deeply embedded gifting and home fragrance culture that the National Candle Association estimates generates retail sales touching approximately 85% of American households as regular or occasional candle purchasers. The market’s commercial infrastructure is extraordinary in its breadth and depth, spanning Bath & Body Works’ nationwide speciality retail network whose candle collections drive substantial seasonal foot traffic and repeat purchase frequency, Yankee Candle’s distribution across mass market, drug, and e-commerce channels that achieves near-universal brand recognition, the prestige department store counter presence of Jo Malone London and Diptyque serving the luxury candle consumer segment, and the growing Shopify and Amazon ecosystem of artisan candle brands whose direct-to-consumer reach and social media-driven brand building are capturing millennial and Gen Z consumers’ candle spending with authentic craftsmanship narratives that larger corporate brands struggle to replicate.

The U.S. candle market’s wellness positioning alignment is perhaps its most commercially durable structural advantage, as the cultural and clinical association of aromatherapy fragrance candles with stress reduction, sleep quality improvement, and mindfulness practice is supported by a growing evidence base in consumer health research that legitimises candle purchase as a healthcare-adjacent self-care investment rather than a pure aesthetic indulgence, enabling consumers to justify premium candle spending within mental health and wellness budget frameworks whose size and cultural priority are expanding substantially across every U.S. demographic cohort.

Candle Market Segment Analysis

-

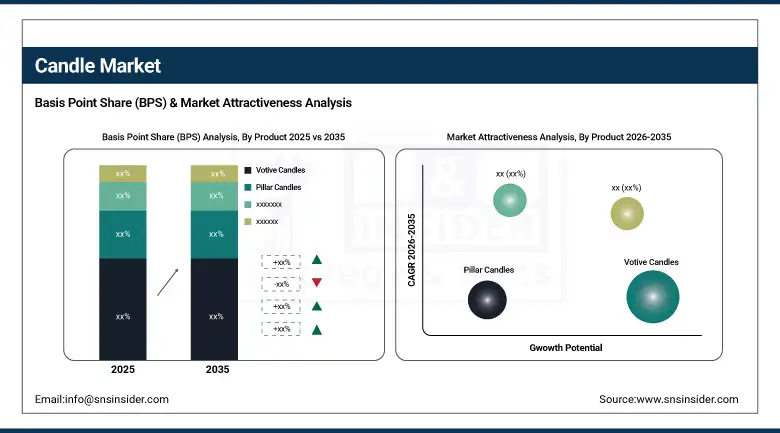

By Product, votive candles led the candle market with approximately 31.25% share in 2025 owing to their versatility in decorative, ceremonial, and aromatherapy applications and their compatibility with the vessel-based candle display formats that home interior decorating trends favour; taper candles are the fastest-growing segment at a CAGR of approximately 8.50% driven by their resurgence in dining occasion, event decoration, and premium home hospitality contexts where the elegant aesthetic of tapered candlelight aligns with the experiential hosting investment that post-pandemic home entertainment culture prioritises.

-

By Wax Type, paraffin wax candles led the market with approximately 48.65% share in 2025 due to their established manufacturing scale, cost efficiency, excellent fragrance throw characteristics, and wide availability across all price tiers; soy wax candles are the fastest-growing wax type at a CAGR of approximately 9.20% driven by the powerful commercial pull of natural, renewable, and clean-burning positioning that the wellness and sustainability-conscious consumer segment prioritises and whose premium willingness to pay supports the higher raw material cost of soy formulations relative to petroleum-derived paraffin alternatives.

-

By Scent Type, scented candles dominated the market with approximately 75.36% share in 2025 and showed the fastest growth driven by the convergence of aromatherapy wellness culture, home fragrance as interior design element, and the extraordinary fragrance innovation that prestige candle brands are driving through complex multi-note scent architectures; the unscented segment retains commercial relevance for ceremonial, religious, and decoration-focused applications where fragrance-free performance is a prerequisite.

-

By Distribution Channel, supermarkets and hypermarkets held the largest share at approximately 42.58% in 2025 through mass market accessibility for the everyday and seasonal candle purchases that represent the majority of volume; online stores are the fastest-growing channel at a CAGR of approximately 11.87% driven by direct-to-consumer brand strategies, subscription models, social commerce discovery, and the product range depth that digital channels deliver versus physical retail shelf space constraints.

-

By End User, the residential segment held approximately 68.46% share in 2025 as the dominant end user through household self-purchase and gifting consumption; the commercial segment is the fastest-growing end user at a CAGR of approximately 8.70% driven by hospitality sector candle adoption, spa and wellness centre fragrance programming, restaurant atmospheric investment, and corporate gifting programme expansion.

By Product, votive candles dominate, taper candles expected to grow fastest

Votive candles retained the dominant product position with approximately 31.25% of the candle market in 2025, a dominance grounded in the format’s extraordinary versatility that makes it the preferred choice across the widest range of candle use cases simultaneously. The votive’s compact dimensions allow for grouping and arrangement in both decorative and functional configurations, its typically three to five hour burn time provides a complete single-occasion illumination experience without requiring the extended commitment of large pillar or container formats, and its universal compatibility with the glass votive holders that home retailers stock as accessory items creates a complete ecosystem where votive candle purchase is naturally paired with an accessible vessel investment. The votive format’s particular strength in the scented candle application, where its contained combustion environment within a glass holder concentrates fragrance dispersal and creates a more intense aromatic throw relative to its small wax mass, makes it the preferred format for aromatherapy and home fragrance consumers who prioritise scent intensity and atmospheric impact over extended burn duration.

Taper candles are the fastest-growing product segment at a CAGR of approximately 8.50% through 2035, propelled by a distinctive and commercially powerful resurgence driven by the elevation of home dining as a high-investment lifestyle experience that post-pandemic entertaining culture has normalised across middle-class households who formerly reserved formal table-setting for special occasions but are now extending candlelit dinner aesthetics to regular weeknight occasions where candle investment is treated as standard domestic hospitality infrastructure. The aesthetic appeal of tapered candlelight in dining contexts has been significantly amplified by the extraordinary influence of ‘candlelit dinner’ aesthetic content on Instagram and TikTok, where the distinctive elongated flame and graceful form of taper candles in elegant holders has become a standard visual element of aspirational home entertaining content that inspires purchasing behaviour among the hundreds of millions of consumers whose home decoration decisions are meaningfully influenced by the curated domestic aesthetic imagery they consume on social media platforms daily.

By Wax Type, paraffin dominates, soy wax expected to grow fastest

Paraffin wax candles retained the dominant wax type position with approximately 48.65% of the candle market in 2025, reflecting the material’s enduring commercial advantages in terms of manufacturing cost efficiency, formulation versatility across every candle product format, excellent fragrance retention and release characteristics, and the structural consistency that allows paraffin candles to maintain their dimensional integrity across the storage temperature variations that retail supply chains impose. The paraffin wax segment’s commercial resilience reflects both the inertia of established consumer familiarity and the genuine performance advantages that high-quality paraffin formulations deliver: superior fragrance throw relative to many natural wax alternatives at equivalent fragrance load percentages, lower melting points enabling more consistent burn characteristics across ambient temperature ranges, and the ability to achieve the high-gloss smooth surfaces and precise colour saturation that mass market decorative candle aesthetics require through manufacturing processes whose cost structures cannot be replicated with natural wax inputs.

Soy wax candles are the fastest-growing wax type at a CAGR of approximately 9.20% through 2035, driven by the structural and durable shift in consumer preference toward natural, renewable, and clean-burning candle formulations that the wellness and sustainability movements have elevated from niche preference to mainstream purchase consideration across the premium and mid-market candle consumer segments that define the market’s highest growth value pools. Soy wax’s commercial positioning advantages are multiple and reinforcing: its derivation from soybeans, a renewable agricultural crop primarily grown in the United States, enables domestic sourcing narratives that resonate with American consumers’ growing preference for local and traceable ingredient supply chains; its slower burn rate relative to paraffin delivers longer burn times per unit of wax weight that consumers experience as tangible value; and its clean burn characteristics producing minimal black soot reduce surface staining and indoor air quality concerns that wellness-conscious candle consumers increasingly cite as key purchasing considerations when selecting between paraffin and natural wax alternatives.

By Scent Type, scented candles dominate and also grow fastest

Scented candles retained the dominant scent type position with approximately 75.36% of the candle market in 2025, a dominance that reflects the extraordinary commercial convergence of home fragrance, wellness culture, and the democratic luxury market that has made scented candles one of the most commercially successful affordable lifestyle product categories of the past decade. The scented candle segment’s market leadership is built on a remarkably diverse consumer motivation architecture spanning aromatherapy stress relief, home atmosphere creation, seasonal scent marking of celebrations and occasions, gifting appeal enhanced by fragrance identity, and the hedonic pleasure of surrounding oneself with preferred fragrances whose neurological impact on mood and emotional state provides genuine daily wellbeing value that purely functional or decorative unscented candles cannot deliver. The extraordinary fragrance innovation investment that prestige candle houses including Diptyque’s May 2025 sustainable collection featuring 100% soy wax and FSC-certified packaging, Jo Malone London, and NEST New York are directing toward complex multi-note fragrance architectures whose olfactory sophistication rivals fine perfumery is simultaneously elevating the category’s premium tier and creating aspirational anchor points that pull the broader market toward higher quality and spending standards.

Scented candles also represent the fastest-growing segment within the scent type categorisation, driven by the continuous expansion of fragrance occasion occasions and consumer scent sophistication that is broadening the contexts in which scented candle investment is considered appropriate and desirable beyond the traditional bedroom and bathroom settings into kitchen, home office, outdoor entertaining space, and even automobile fragrance applications where candle formats are evolving to serve new ambient fragrance delivery needs. P.F. Candle Co.’s February 2025 partnership with wellness app Calm to launch a limited-edition line of aromatherapy candles aligned with the app’s sleep and meditation content programmes exemplifies the convergence of digital wellness platforms and physical candle products as a commercial category development strategy whose appeal spans the wellness technology consumer audience and candle category enthusiasts simultaneously.

By Distribution Channel, supermarkets & hypermarkets dominate, online stores grow fastest

Supermarkets and hypermarkets retained the dominant distribution channel position with approximately 42.58% of the candle market in 2025, as the primary weekly shopping destination for the majority of global consumers provides the mass market candle category with unmatched purchase convenience, impulse buying opportunity from high-traffic store locations, and the critical shelf presence visibility during peak seasonal sales windows including Halloween, Thanksgiving, Christmas, and Valentine’s Day whose volume concentration creates enormous commercial value for retail partners willing to commit premium endcap and seasonal feature space to candle category management. The supermarket channel’s enduring commercial advantage in candles reflects the category’s high incidence of unplanned purchase, where consumers who enter a store for grocery purposes encounter candle promotions in seasonal display areas and add to basket based on fragrance appeal, decorative attractiveness, or price promotion without prior purchase intention in ways that require the physical retail environment’s ability to engage the senses that digital retail cannot replicate for a fragrance-driven product category where smell is the primary quality signal.

Online stores are the fastest-growing distribution channel at a CAGR of approximately 11.87% through 2035, driven by the transformative impact of direct-to-consumer e-commerce on the candle market’s brand and channel landscape as both established brands and independent artisan producers leverage digital commerce infrastructure to build direct customer relationships that generate higher margins, more robust customer data, and more sustainable brand loyalty than wholesale retail relationships characterised by margin pressure, shelf space competition, and limited brand expression opportunity. The social commerce acceleration created by TikTok Shop, Instagram Shopping, and Pinterest’s shoppable pin formats has been particularly commercially significant for the candle category, as the visual and sensory appeal of candle content on these platforms creates direct purchase intent that shoppable post infrastructure converts without requiring users to navigate away from the content discovery context to a separate retail environment, compressing the distance between fragrance aspiration and commercial transaction to near-zero.

By End User, residential segment dominates, commercial segment grows fastest

The residential segment retained the dominant end user position with approximately 68.46% of the candle market in 2025, anchored by the household self-purchase and gifting occasions that collectively generate the large majority of global candle volume across the everyday home fragrance, seasonal decorating, relaxation ritual, and intimate occasion candlelight use cases that define residential candle consumption’s extraordinary breadth and frequency. The residential segment’s dominance reflects candle’s rare commercial characteristic of being simultaneously a repeat purchase consumable whose combustion creates continuous replacement demand and a lifestyle product whose usage frequency grows with the consumer’s investment in home environment quality, creating a compounding engagement dynamic where consumers who begin purchasing candles for specific occasions progressively increase their category engagement as the positive experiential associations of candlelit domestic spaces motivate broader and more frequent usage that sustains the residential segment’s large-scale procurement volume.

The commercial segment is the fastest-growing end user at a CAGR of approximately 8.70% through 2035, propelled by the hospitality sector’s progressive adoption of bespoke fragrance programmes as a core brand differentiation tool, with luxury hotels, boutique guesthouses, premium spas, high-end restaurants, and premium retail environments all investing in signature scent identities delivered through custom-formulated candles whose distinctive fragrances create memorable sensory brand associations that guests and customers carry home as experiential brand memories. The spa and wellness centre segment represents a particularly high-value commercial candle procurement category, as the therapeutic use of aromatherapy candles in treatment room settings, relaxation lounges, and meditation spaces requires professional-grade candle performance including clean burn quality, consistent fragrance release, and appropriate burn time that creates ongoing commercial demand for specification-grade candle products whose unit economics substantially exceed mass market residential alternatives.

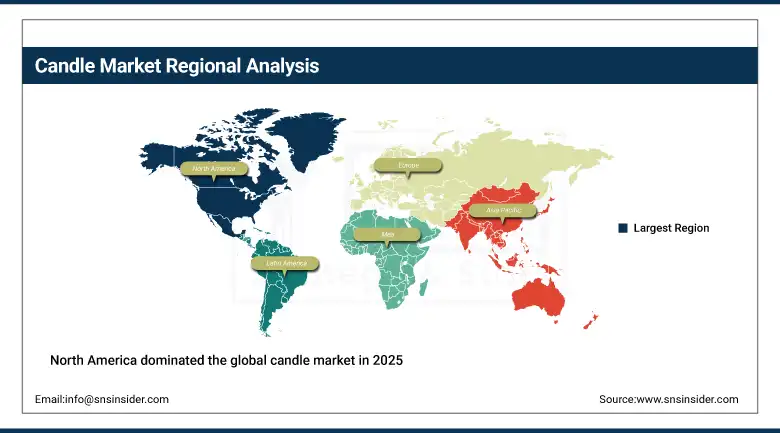

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

24.2% |

|

Asia Pacific |

China |

33.0% |

|

Middle East & Africa |

UAE |

26.7% |

|

Latin America |

Brazil |

42.5% |

North America Candle Market Insights

North America dominated the global candle market in 2025, with the United States accounting for approximately 83.4% of North American revenues and approximately 32.2% of global candle market revenues, driven by the world’s most commercially developed home fragrance culture, the highest concentration of premium candle brands and retail distribution infrastructure, and a gifting economy that integrates candle purchases into the seasonal gift-giving occasions that drive the category’s extraordinary fourth-quarter sales concentration. The U.S. market benefits from the commercial depth created by Bath & Body Works’ nationwide store network, Yankee Candle’s multi-channel mass market distribution, and the prestige department store and specialty beauty retail ecosystem that supports the premium and luxury candle segment’s growth through the Jo Malone London, Diptyque, NEST New York, and Voluspa brand presences whose retail execution and fragrance education programmes develop the consumer sophistication that sustains premium price acceptance. Canada contributes approximately 16.6% of North American candle revenues through a market that mirrors U.S. home fragrance culture with a particular emphasis on natural and sustainable wax formulations aligned with Canadian consumers’ above-average environmental consciousness and the premium specialty candle channel’s strength in major urban markets including Toronto, Vancouver, and Montreal.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Candle Market Insights

Europe is a mature and sophisticated candle market where the category has deep cultural roots in Northern European hygge tradition, Mediterranean religious and ceremonial candlelight practice, and the continent-wide association of candles with quality domestic hospitality and interior refinement that sustains high per-capita candle consumption across the United Kingdom, Germany, France, Scandinavia, and the Benelux countries whose combined market volume makes Europe the world’s most important candle market outside North America. Germany accounts for approximately 24.2% of European candle revenues as the region’s largest national market, driven by strong seasonal candle purchase during the Advent period when candle decoration is a deeply embedded cultural tradition, a manufacturing excellence tradition that has produced some of Europe’s most respected pillar and church candle producers, and a growing premium fragrance candle market whose consumer base’s willingness to invest in quality and sustainable formulations has made Germany a lead market for natural wax and luxury fragrance candle brands. The European market’s sustainability orientation is shaping candle product development most forcefully in this region, with EU chemical regulation of fragrance compounds, growing retailer commitments to natural wax sourcing, and consumer advocacy organisations’ communication about paraffin combustion emissions collectively creating stronger regulatory and commercial pressure for natural wax formulation transition than exists in North American or Asian markets.

Asia Pacific Candle Market Insights

Asia Pacific is the fastest-growing regional candle market, driven by China’s rapidly expanding middle class whose adoption of Western home decoration and self-care purchasing behaviours includes the progressive integration of scented candles into home environments, the extraordinary growth of the wellness and aromatherapy category across Japanese and South Korean consumer markets whose sophisticated beauty and personal care culture is extending naturally into home fragrance investment, and the rising affluence of Southeast Asian consumers in Thailand, Indonesia, Vietnam, and the Philippines whose urbanisation and income growth are creating first-time premium home fragrance adoption. China accounts for approximately 33.0% of Asia Pacific candle revenues, representing both the world’s most significant candle manufacturing base whose export production supplies the majority of global mass market candle volume and a rapidly growing domestic consumption market where China’s emphasis on sustainable product development has led to the growth of eco-friendly candle options and where luxury fragrance house Diptyque’s 2022 China collection launch validated the commercial potential of premium candle positioning in the Chinese market that domestic and international brands are progressively developing. South Korea and Japan represent sophisticated secondary Asia Pacific markets where premium fragrance candle adoption is most advanced and where consumer quality expectations and ingredient transparency requirements most closely mirror European premium market standards.

MEA & Latin America Candle Market Insights

The Middle East and Africa and Latin America are growing candle markets where rising urban affluence, expanding modern retail infrastructure, and the growing influence of global wellness and home decoration culture are creating the conditions for sustained candle market development across consumer populations whose candle purchasing is transitioning from primarily functional and religious use into the lifestyle and home fragrance applications that define the market’s highest-growth commercial segments. UAE leads Middle East and Africa candle revenues at approximately 26.7% through the combination of a high-income expatriate and local consumer population whose luxury lifestyle orientation supports premium candle brand adoption, the extraordinary luxury retail infrastructure in Dubai and Abu Dhabi that provides shelf presence for international prestige candle brands, and the growing wellness and spa culture across Gulf Cooperation Council countries that is creating commercial demand for aromatherapy and therapeutic candle applications. Brazil leads Latin American candle revenues at approximately 42.5% through its combination of a large urban middle class with growing home decoration investment, strong religious candle traditions that sustain baseline category consumption, and the rapidly expanding e-commerce ecosystem that is making premium and artisan candle brands accessible to Brazilian consumers across the country’s vast geographic extent. Byredo’s 2025 announcement of an exclusive scented candle collection for the Middle Eastern market available through new retail partnerships in Dubai and Riyadh demonstrates the strategic importance that luxury fragrance brands assign to the region’s premium consumer appetite.

Market Dynamics

Growth Drivers: Wellness culture mainstreaming candle purchase as daily self-care investment, gifting tradition sustaining seasonal demand peaks, and premiumisation driving average unit price growth across natural wax and luxury fragrance segments

The primary structural growth drivers for the candle market are the extraordinary commercial alignment between candle purchase and the wellness and self-care investment trend that has become one of the most commercially durable consumer behaviour shifts of the past decade, as the scientific and cultural validation of aromatherapy fragrance’s mood-regulating, stress-reducing, and sleep-improving effects legitimises candle spending within consumers’ health and wellbeing budget frameworks rather than competing as a pure discretionary aesthetic luxury against other home decoration categories. The gifting tradition that concentrates approximately 35% of U.S. candle sales and a comparable proportion of European candle revenues in the October through December holiday season creates an annual demand pulse whose commercial scale and predictability enables retailers and manufacturers to invest confidently in seasonal product development, packaging, and promotional programming that collectively elevates category engagement and purchase frequency across both gifting and self-purchase occasions. Premiumisation is simultaneously expanding the market’s average revenue per unit as consumers trade up from entry-level paraffin mass market candles toward natural wax, artisanal, and luxury fragrance alternatives whose per-unit economics substantially exceed the commodity candle baseline, creating revenue growth that outpaces volume growth across the market’s most commercially sophisticated segments.

Restraints: Raw material cost volatility affecting fragrance oil and wax input prices, safety regulatory compliance costs for fragrance ingredient disclosure, and market fragmentation creating competitive intensity that pressures brand pricing power

A significant restraint on the candle market is the raw material cost volatility that affects the primary inputs of candle manufacturing, including petroleum price movements that directly influence paraffin wax costs creating margin pressure for mass market producers whose commodity pricing makes cost pass-through commercially difficult, soybean agricultural cycle volatility that creates soy wax supply and pricing variability for the natural wax segment whose growth is otherwise strongly supported by consumer preference trends, and fragrance compound availability constraints created by IFRA regulatory restrictions on specific fragrance ingredients that require reformulation investment and limit the fragrance palette available to candle manufacturers seeking to maintain consumer-preferred scent profiles within tightening safety standards. The extreme market fragmentation characterising the candle industry, where thousands of small artisan producers compete alongside large corporate candle manufacturers through accessible e-commerce and social media channels, creates competitive intensity that limits the pricing power of mid-tier brands squeezed between premium luxury positioning and ultra-low-cost commodity competition from direct import sources.

Opportunities: Sustainable packaging and formulation innovation creating premium market positioning, male consumer market development, and corporate gifting and branded hospitality candle programmes creating new B2B revenue streams

The sustainable candle innovation opportunity, encompassing 100% natural wax formulations, FSC-certified wooden wick systems, compostable or refillable vessel programmes, and responsible fragrance ingredient sourcing certified to IFRA and REACH standards, represents the most commercially compelling product development direction in the premium candle segment where sustainability credentials are becoming a purchase prerequisite for the environmentally conscious consumer demographic that drives disproportionate premium category growth. The corporate gifting and branded hospitality candle segment represents a growing and commercially underexploited B2B revenue opportunity, as organisations across luxury retail, financial services, real estate, and the event industry commission custom-formulated and branded candle products for client gifting programmes, corporate event favours, and new employee welcome packages whose quality positioning communicates brand values that generic gifting alternatives cannot match at comparable per-unit cost investment.

Recent Developments:

-

2025: Bath & Body Works debuted its flagship store on London’s iconic Oxford Street, marking a significant milestone in the brand’s international expansion and demonstrating the export potential of the U.S.’s most commercially successful mass-market candle brand into the world’s most visited luxury retail high street and establishing a flagship presence that serves both direct sales and brand awareness objectives across the European market.

-

2025: Diptyque Paris unveiled a sustainable collection in May 2025 featuring 100% soy wax formulations and FSC-certified packaging, marking one of the luxury fragrance house’s most significant product philosophy transitions and demonstrating the category’s highest-premium tier’s commitment to aligning with the natural and sustainable candle formulation standards that its environmentally conscious luxury consumer base increasingly demands as a prerequisite for purchase consideration alongside the fragrance quality that the brand’s reputation is built upon.

-

2025: P.F. Candle Co. partnered with wellness app Calm in February 2025 to launch a limited-edition line of aromatherapy candles aligned with the app’s sleep and meditation content programmes, creating a cross-category wellness partnership that simultaneously expands P.F. Candle Co.’s consumer base into the tens of millions of Calm app users and provides a physical sensory product companion to Calm’s digital wellness content offering.

-

2025: Byredo announced the launch of an exclusive scented candle collection for the Middle Eastern market in partnership with new retail partners in Dubai and Riyadh, marking the Swedish luxury fragrance house’s strategic commitment to the Gulf Cooperation Council’s rapidly growing luxury fragrance retail market whose high-income consumer base is demonstrating strong appetite for Western prestige home fragrance brands.

-

2026: Yankee Candle announced in January 2026 an exclusive year-long partnership with Reese’s Book Club, creating a co-branded candle collection aligned with the book club’s seasonal reading selections and demonstrating the sophisticated community-marketing and cultural alignment strategies that established mass-market candle brands are deploying to maintain meaningful connections with millennial and Gen Z consumers whose purchasing decisions are strongly influenced by the values and aesthetic sensibilities of the community figures they trust.

Candle Market Key Players

-

Newell Brands Inc. (Yankee Candle, WoodWick, Chesapeake Bay Candle)

-

Bath & Body Works, Inc.

-

Diptyque Paris (LVMH)

-

Jo Malone London (Estée Lauder Companies)

-

Bolsius International B.V.

-

NEST New York

-

Voluspa (DLM Designs Inc.)

-

S.C. Johnson & Son Inc. (Glade)

-

Henkel AG & Co. KGaA (Schwarzkopf)

-

Coty Inc.

-

Paddywax LLC

-

LAFCO New York

-

Chesapeake Bay Candle (Newell Brands)

-

P.F. Candle Co.

-

Village Candle

-

Byredo AB

-

Bridgewater Candle Company

-

Colonial Candle

-

Malin+Goetz

-

Le Labo (Estée Lauder Companies)

Candle Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.52 Billion |

| Market Size by 2035 | USD 22.14 Billion |

| CAGR | CAGR of 6.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Votive Candles, Pillar Candles, Taper Candles, Container Candles, Others) • By Wax Type (Paraffin Wax, Soy Wax, Beeswax, Coconut Wax, Others) • By Scent Type (Scented, Unscented) • By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Stores, Others) • By End User (Residential, Commercial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Newell Brands Inc., Bath & Body Works, Inc., Diptyque Paris (LVMH), Jo Malone London (Estée Lauder Companies), Bolsius International B.V., NEST New York, Voluspa (DLM Designs Inc.), S.C. Johnson & Son Inc. (Glade), Henkel AG & Co. KGaA (Schwarzkopf), Coty Inc., Paddywax LLC, LAFCO New York, Chesapeake Bay Candle (Newell Brands), P.F. Candle Co., Village Candle, Byredo AB, Bridgewater Candle Company, Colonial Candle , Malin+Goetz, Le Labo (Estée Lauder Companies) |

Frequently Asked Questions

North America dominated the Candle Market in 2025, with the United States accounting for approximately 83.4% of North American revenues.

Votive candles led the Candle Market with approximately 31.25% of revenues in 2025.

The mainstreaming of wellness and self-care culture elevating candle purchase from occasional indulgence to daily lifestyle investment, combined with the gifting tradition sustaining predictable seasonal demand peaks and the premiumisation trend driving average unit price growth through consumer trade-up from paraffin mass market to natural wax and luxury fragrance alternatives.

The Candle Market was valued at USD 11.52 Billion in 2025.

Get in Touch