Canine Vaccines Market Report Scope & Overview:

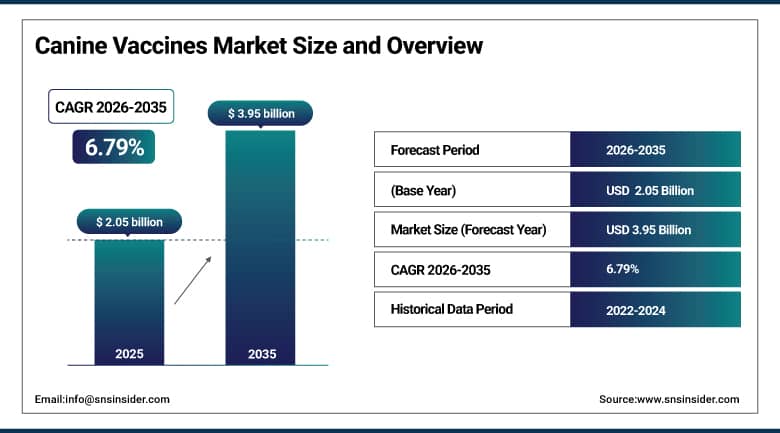

The Canine Vaccines Market was estimated at USD 2.05 Billion in 2025 and is expected to reach USD 3.95 Billion by 2035 and grow at a CAGR of 6.79% over the forecast period of 2026-2035.

The canine vaccines market is expanding due to the increasing pet population and rising awareness among pet owners about preventive healthcare for dogs. Growing adoption of dogs as companion animals, coupled with the prevalence of infectious diseases, is driving demand for routine and advanced vaccinations. Advances in veterinary biotechnology, development of combination and multivalent vaccines, and government and veterinary initiatives promoting animal health further support market growth. Additionally, increased spending on pet healthcare, higher disposable incomes, and awareness of zoonotic disease prevention contribute to sustained market expansion.

86% adopted advanced canine vaccines due to rising pet ownership, biotech advances, and zoonotic disease concerns, driving global market growth.

Market Size and Forecast

-

Market Size in 2025: USD 2.05 Billion

-

Market Size by 2035: USD 3.95 Billion

-

CAGR: 6.79% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Canine Vaccines Market - Request Free Sample Report

Canine Vaccines Market Trends

-

Rising awareness of preventive pet healthcare driving routine canine vaccination adoption globally

-

Increasing demand for combination vaccines reducing clinic visits and improving compliance among pet owners

-

Growing prevalence of zoonotic and infectious diseases boosting vaccination rates in companion dogs

-

Expansion of veterinary clinics and animal hospitals supporting higher vaccine accessibility and administration

-

Advancements in recombinant and DNA-based vaccines enhancing safety, efficacy, and long-term immunity

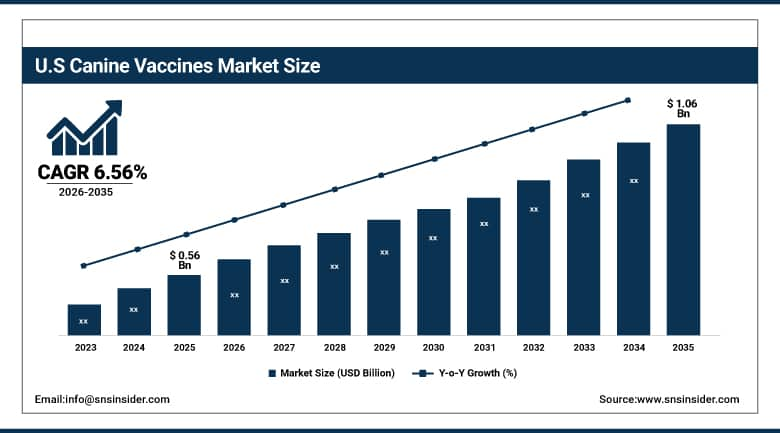

The U.S. Canine Vaccines Market is valued at USD 0.56 billion in 2025 and is expected to reach USD 1.06 billion by 2035, growing at a CAGR of 6.56% from 2026-2035. The U.S. canine vaccines market is growing due to rising dog ownership and increasing awareness of preventive healthcare among pet owners. Greater focus on controlling infectious diseases, advancements in veterinary vaccines, and higher spending on pet health are driving demand. Additionally, government initiatives and veterinary recommendations are supporting the adoption of routine and advanced vaccinations across the country.

Canine Vaccines Market Growth Drivers:

-

Rising pet ownership, increasing awareness of preventive animal healthcare, and growing expenditure on companion animal health are driving demand for canine vaccines globally

The global rise in pet adoption, particularly dogs, is fueling demand for preventive healthcare solutions, including vaccines. Pet owners are increasingly conscious of maintaining their pets’ health to avoid infectious diseases, improve longevity, and ensure overall wellbeing. Growing disposable incomes and willingness to spend on veterinary services have contributed to increased vaccine uptake. Veterinary professionals actively promote routine immunizations, further driving awareness. Additionally, pet wellness programs, campaigns by animal welfare organizations, and rising adoption of premium pet care products are encouraging consistent vaccination practices, supporting the growth of the canine vaccines market worldwide.

84% of companion animal owners prioritized preventive care fueled by rising pet ownership, heightened awareness of canine health, and increased spending on veterinary services propelling sustained global demand for canine vaccines.

-

Increasing prevalence of infectious canine diseases and zoonotic risks is encouraging routine vaccination programs and strengthening demand for advanced canine vaccines worldwide

The rising incidence of contagious canine diseases, such as rabies, parvovirus, and distemper, poses a significant health risk to pets and, in some cases, humans. Zoonotic disease concerns have prompted governments and veterinary organizations to implement vaccination programs for dogs. Pet owners are proactively vaccinating their animals to prevent outbreaks and ensure safety within communities. Advances in vaccine formulations, including combination vaccines, have made it easier to protect pets from multiple diseases simultaneously. As awareness of disease prevention grows, both private and public initiatives continue to strengthen global demand for canine vaccines.

82% of veterinary health authorities prioritized routine canine vaccination programs spurred by rising outbreaks of infectious diseases and growing concerns over zoonotic transmission driving robust global demand for next-generation canine vaccines.

Canine Vaccines Market Restraints:

-

High costs of advanced vaccines and limited access to veterinary services in rural or low-income regions restrict widespread adoption of canine vaccination programs

Advanced canine vaccines, including recombinant or combination vaccines, often come at a premium, making them less affordable for pet owners in low-income or rural areas. Additionally, limited veterinary infrastructure in remote regions restricts access to professional services required for proper administration and follow-up care. This creates uneven adoption rates and leaves large populations of dogs unvaccinated, increasing susceptibility to disease outbreaks. The combination of high costs and limited service availability hinders market penetration and slows overall growth, particularly in emerging economies where affordability and accessibility remain critical barriers to the widespread adoption of canine vaccines.

73% of pet owners in rural and low-income regions reported limited access to advanced canine vaccines due to high costs and insufficient veterinary infrastructure impeding widespread immunization and leaving large canine populations vulnerable to preventable diseases.

-

Stringent regulatory approval processes and lengthy clinical trial requirements increase time-to-market for new canine vaccines, slowing innovation and product launches

Canine vaccines must comply with rigorous regulations to ensure safety and efficacy, including extensive preclinical and clinical trials. These processes are time-consuming and expensive, delaying the launch of innovative products. Manufacturers must invest heavily in research, testing, and documentation, which can be a barrier for smaller companies. Differences in regulatory requirements across regions add complexity for global product distribution. Delays in approvals limit the availability of advanced vaccines, slow market expansion, and reduce competitive opportunities for companies seeking to introduce newer, safer, or more effective immunization solutions for dogs worldwide.

76% of new canine vaccines faced delays of 12–24 months due to stringent regulatory requirements and complex clinical trial protocols hindering rapid innovation and limiting the pace of product commercialization in the veterinary vaccine market.

Canine Vaccines Market Opportunities:

-

Technological advancements in vaccine development, including recombinant and DNA-based vaccines, create opportunities for safer, more effective canine immunization solutions

Innovations in vaccine technology are revolutionizing the canine vaccines market. Recombinant, subunit, and DNA-based vaccines offer improved safety profiles, longer immunity duration, and reduced side effects compared to traditional vaccines. These technologies allow for combination vaccines, reducing the number of injections required and enhancing compliance among pet owners. Continuous research and development in molecular biology and immunology provide opportunities for introducing novel formulations targeting emerging canine diseases. Manufacturers leveraging these technological advancements can differentiate their products, expand market share, and meet growing demand for safe, effective, and convenient vaccination solutions in both domestic and international markets.

81% of canine vaccine developers leveraged recombinant and DNA-based platforms enabling safer, more targeted immunization with enhanced efficacy, fewer side effects, and improved stability ushering in a new era of veterinary preventive care.

-

Expansion of veterinary clinics, pet insurance coverage, and government-supported animal health initiatives offers significant growth opportunities for canine vaccine manufacturers globally

The increasing number of veterinary clinics and hospitals worldwide is improving access to professional pet healthcare, facilitating higher vaccine adoption rates. Growing pet insurance coverage encourages routine preventive care, including immunizations, by reducing out-of-pocket costs for pet owners. Government initiatives promoting animal health, such as vaccination campaigns against rabies and other infectious diseases, further support market growth. Emerging economies are investing in veterinary infrastructure and awareness programs, creating new revenue streams. Together, these developments provide significant opportunities for manufacturers to expand distribution, increase vaccine uptake, and strengthen their presence in the global canine vaccines market.

79% of canine vaccine manufacturers reported accelerated market expansion driven by the proliferation of veterinary clinics, rising pet insurance penetration, and government-led animal health programs promoting preventive care worldwide.

Canine Vaccines Market Segmentation Analysis

-

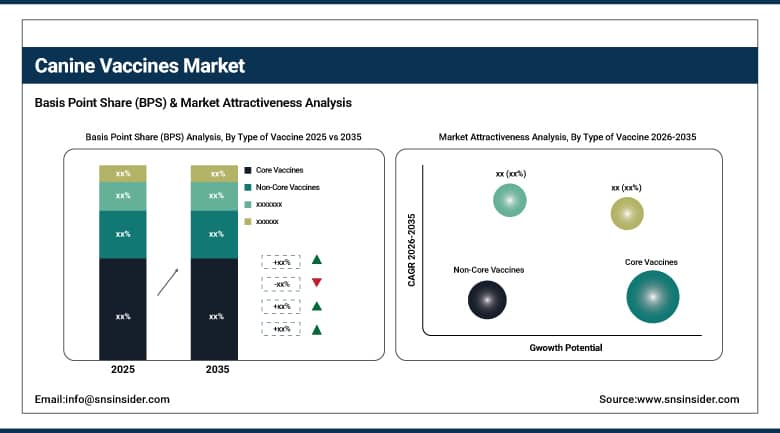

By Type of Vaccine: Core Vaccines led with 42.3% share, while Combination Vaccines is the fastest-growing segment with CAGR of 9.1%.

-

By Disease Targeted: Rabies led with 38.7% share, while Lyme Disease is the fastest-growing segment with CAGR of 9.4%.

-

By Distribution Channel: Veterinary Hospitals & Clinics led with 44.1% share, while Online Pharmacies is the fastest-growing segment with CAGR of 10.2%.

-

By End-User: Pet Owners led with 46.5% share, while Animal Shelters & Kennels is the fastest-growing segment with CAGR of 9.6%.

By Type of Vaccine: Core Vaccines led, while Combination Vaccines is the fastest-growing segment.

Core Vaccines dominate the market due to their essential role in preventing major canine diseases like distemper, parvovirus, and rabies. They are widely recommended by veterinarians, ensuring high adoption across households, shelters, and clinics. Their proven efficacy, routine vaccination schedules, and strong awareness campaigns contribute to recurring demand. Core vaccines form the backbone of canine preventive healthcare programs and remain critical in both urban and rural pet populations, driving consistent market share and revenue growth.

Combination Vaccines are the fastest-growing segment as they offer multiple protections in a single dose, reducing stress for pets and lowering treatment costs for owners. Rising awareness of convenience, increasing pet ownership, and preference for time-efficient preventive care are driving adoption. Veterinary professionals are recommending combination vaccines to simplify vaccination schedules while ensuring comprehensive protection against multiple diseases. Growth is particularly strong in emerging markets were accessibility and convenience influence treatment choices.

By Disease Targeted: Rabies led, while Lyme Disease is the fastest-growing segment.

Rabies vaccines dominate due to regulatory mandates in most countries, high mortality risk of the disease, and widespread awareness among pet owners. Veterinary clinics and hospitals prioritize rabies vaccination for all dogs, ensuring universal coverage. Campaigns from governments and NGOs reinforce its importance, maintaining consistently high adoption. Rabies vaccination also serves as a legal requirement for pet registration in many regions, further cementing its dominant share in the canine vaccines market.

Lyme Disease vaccines are the fastest-growing segment due to rising awareness of tick-borne diseases in dogs and increasing pet outdoor activities. Growth is fueled by urbanization, rising pet spending, and preventive healthcare trends. Owners are increasingly seeking protection against emerging infectious threats, and veterinarians are actively promoting Lyme vaccination in high-risk areas. Improved formulations and combination vaccines targeting Lyme alongside other diseases further accelerate adoption.

By Distribution Channel: Veterinary Hospitals & Clinics led, while Online Pharmacies is the fastest-growing segment.

Veterinary Hospitals & Clinics dominate the market as the primary point of care for canine vaccinations. They provide professional guidance, proper vaccine storage, and administration, ensuring safety and compliance. High trust in veterinarians, routine check-ups, and vaccination schedules drive repeat visits and high adoption rates. Their established infrastructure and trained staff make them the preferred channel for administering both core and non-core vaccines.

Online Pharmacies are the fastest-growing segment as digital adoption increases among pet owners seeking convenience and cost savings. Owners can order vaccines, accessories, and preventive care products from home, often paired with tele-veterinary consultations. The growth of e-commerce, awareness of online options, and subscription-based delivery models make online pharmacies an increasingly attractive distribution channel, especially for routine boosters and combination vaccines.

By End-User: Pet Owners led, while Animal Shelters & Kennels is the fastest-growing segment.

Pet Owners dominate the market as the primary consumers of canine vaccines. Rising pet adoption, increasing disposable income, and growing awareness of preventive care drive consistent demand. Owners are motivated by health, longevity, and disease prevention for their dogs, ensuring high adoption of both core and non-core vaccines. Educational campaigns and veterinary guidance reinforce routine vaccination practices, maintaining their dominant market share.

Animal Shelters & Kennels are the fastest-growing end-user segment as large-scale facilities increasingly adopt comprehensive vaccination programs to prevent disease outbreaks. Growth is driven by expanding shelter networks, rising dog adoption rates, and stricter health protocols. Bulk vaccination programs, preventive healthcare initiatives, and collaborations with NGOs and veterinary associations accelerate uptake, making shelters and kennels a rapidly growing segment in the canine vaccines market.

Regional Insights

North America Canine Vaccines Market Insights:

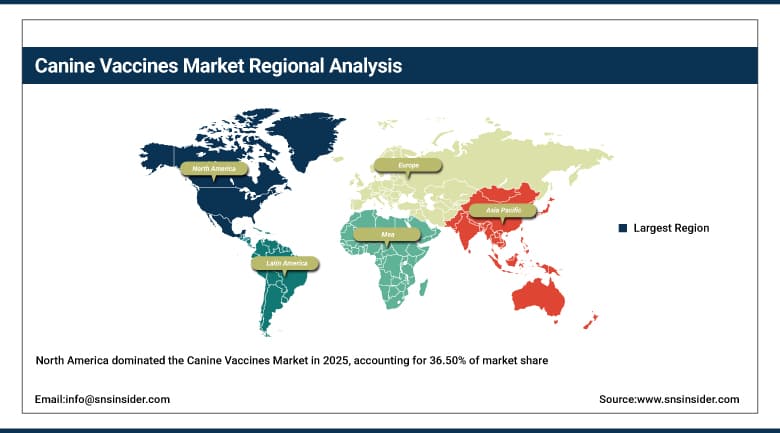

North America dominated the Canine Vaccines Market with a 36.50% share in 2025 due to high pet ownership, strong awareness of canine health, and well-established veterinary infrastructure. The presence of leading vaccine manufacturers, widespread vaccination programs, and favorable regulatory frameworks further strengthened the region’s leadership in canine immunization.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Canine Vaccines Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 8.22% from 2026–2035, driven by increasing pet adoption, rising awareness of animal health, and expanding veterinary services. Growing disposable income, government initiatives promoting pet healthcare, and entry of global vaccine manufacturers are accelerating market growth across the region.

Europe Canine Vaccines Market Insights

Europe held a significant share in the Canine Vaccines Market in 2025, supported by high pet ownership rates, well-established veterinary infrastructure, and strong awareness of pet healthcare. The region’s stringent animal health regulations, widespread adoption of routine vaccination programs, and presence of leading vaccine manufacturers further reinforced its substantial market position.

Middle East & Africa and Latin America Canine Vaccines Market Insights

The Middle East & Africa and Latin America together exhibited steady growth in the Canine Vaccines Market in 2025, driven by increasing pet adoption, rising awareness of canine health, and expanding veterinary services. Improving access to vaccines, growing disposable incomes, and gradual development of animal healthcare infrastructure contributed to strengthening the market presence in these regions.

Competitive Landscape:

Zoetis Inc.

Zoetis Inc. is a global leader in animal health, specializing in vaccines, medicines, and diagnostic products for companion and farm animals. In the canine vaccines segment, Zoetis offers a comprehensive portfolio that protects dogs against diseases such as rabies, parvovirus, distemper, and leptospirosis. The company focuses on research-driven innovation, safety, and efficacy, with a strong global distribution network. Zoetis aims to improve pet health and welfare, delivering high-quality, reliable vaccines to veterinarians and pet owners worldwide.

-

May 2024, Zoetis received USDA approval for an updated VANGUARD C9 and Lepto 7 vaccine, offering broad protection against 9 canine diseases in a single injection, including 3-year duration of immunity for core components (distemper, adenovirus, parvovirus, parainfluenza).

Merck & Co., Inc. (Merck Animal Health)

Merck Animal Health, a division of Merck & Co., Inc., is a leading provider of vaccines, pharmaceuticals, and health management solutions for companion and livestock animals. Its canine vaccine portfolio addresses diseases including rabies, parvovirus, distemper, and canine influenza. The company emphasizes innovation, clinical research, and regulatory compliance to ensure high-quality, effective products. With a global presence and strong veterinary partnerships, Merck Animal Health contributes significantly to pet disease prevention, helping maintain the health, safety, and longevity of dogs worldwide.

-

November 2023, Merck Animal Health launched NOBIVAC CANINE 1-DAP, a next-generation modified live virus (MLV) vaccine for distemper, adenovirus type 2, and parvovirus, engineered to elicit a stronger cell-mediated (Th1) immune response.

Boehringer Ingelheim International GmbH

Boehringer Ingelheim International GmbH is a top global animal health company providing innovative vaccines, pharmaceuticals, and preventive solutions for pets and livestock. In the canine vaccines market, it offers products targeting distemper, parvovirus, leptospirosis, and other infectious diseases. The company invests heavily in research and development, ensuring efficacy, safety, and quality standards. Boehringer Ingelheim focuses on improving pet health, supporting veterinarians, and enhancing the welfare of dogs globally, establishing itself as a trusted partner in the animal health industry.

-

January 2025, Boehringer Ingelheim launched EURICAN Lmulti And DAPPi2 in Europe and select global markets, a combination vaccine protecting against distemper, adenovirus, parvovirus, parainfluenza, and 6 leptospira serovars.

Canine Vaccines Market Key Players

-

Zoetis Inc.

-

Merck & Co., Inc. (Merck Animal Health)

-

Boehringer Ingelheim International GmbH

-

Elanco Animal Health Incorporated

-

Virbac S.A.

-

Ceva Santé Animale

-

Vetoquinol S.A.

-

Bioveta a.s.

-

Hester Biosciences Limited

-

Heska Corporation

-

IDEXX Laboratories

-

Phibro Animal Health Corporation

-

Indian Immunologicals Limited

-

HIPRA S.A.

-

Dechra Pharmaceuticals PLC

-

Neogen Corporation

-

Zendal Group

-

Bayer Animal Health (Animal Health Division)

-

Intervet International B.V. (MSD Animal Health)

-

Tianjin Ringpu Bio-Pharmacy Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.05 Billion |

| Market Size by 2035 | USD 3.95 Billion |

| CAGR | CAGR of 6.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type of Vaccine (Core Vaccines, Non-Core Vaccines, Combination Vaccines) • By Disease Targeted (Canine Distemper, Parvovirus, Adenovirus, Rabies, Leptospirosis, Bordetella, Lyme Disease) • By Distribution Channel (Veterinary Hospitals & Clinics, Online Pharmacies, Animal Specialty Stores, Direct Sales from Manufacturers) • By End-User (Pet Owners, Veterinary Clinics, Animal Shelters & Kennels, Research & Breeding Facilities) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zoetis Inc., Merck & Co., Inc. (Merck Animal Health), Boehringer Ingelheim International GmbH, Elanco Animal Health Incorporated, Virbac S.A., Ceva Santé Animale, Vetoquinol S.A., Bioveta a.s., Hester Biosciences Limited, Heska Corporation, IDEXX Laboratories, Phibro Animal Health Corporation, Indian Immunologicals Limited, HIPRA S.A., Dechra Pharmaceuticals PLC, Neogen Corporation, Zendal Group, Bayer Animal Health (Animal Health Division), Intervet International B.V. (MSD Animal Health), Tianjin Ringpu Bio-Pharmacy Co., Ltd. |

Frequently Asked Questions

North America dominated the Canine Vaccines Market in 2025 driven by high pet ownership, advanced veterinary infrastructure, and widespread vaccination programs.

The “Core Vaccines” segment dominated the Canine Vaccines Market due to mandatory usage, high veterinary recommendation rates, and routine immunization schedules.

Rising pet ownership, increasing awareness of preventive canine healthcare, and growing spending on companion animal health are key growth drivers.

The global Canine Vaccines Market was valued at approximately USD 2.05 billion in 2025, reflecting steady demand for preventive canine healthcare.

The Canine Vaccines Market is expected to grow at a CAGR of 6.79% percent during the forecast period from 2026 to 2035.

Get in Touch