Cellulite Treatment Market Report Scope & Overview:

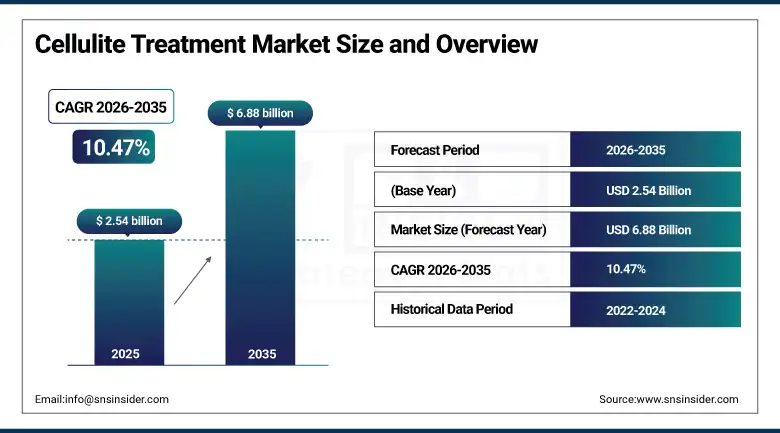

The Cellulite Treatment market was valued at USD 2.54 billion in 2025 and is expected to reach USD 6.88 billion by 2035, growing at a CAGR of 10.47% from 2026–2035.

The cellulite treatment market is being fundamentally transformed by a new generation of minimally invasive and non-invasive treatment platforms that have achieved FDA clearance for cellulite reduction indications and that demonstrate clinically meaningful improvements in cellulite appearance with acceptable safety profiles and minimal patient downtime. FDA-cleared radiofrequency devices including Thermage and Exilis Ultra, acoustic wave therapy systems, laser-based treatment platforms, and the subcision-based Cellfina and acoustic micropulse Aveli systems have collectively established a clinical evidence base for effective cellulite treatment that was largely absent a decade ago. Most recently, the development of Qwo collagenase injection therapy that directly targets the fibrous septae responsible for cellulite dimpling through enzymatic cleavage has opened a new treatment category, though early commercial results were mixed before the product's U.S. withdrawal.

The January 2025 RealSelf platform report of a 40% increase in cellulite treatment interest among U.S. women driven by influencer content, rising aesthetic spending, and seasonal body-shaping demand confirms that consumer awareness of and willingness to invest in professional cellulite reduction treatment has meaningfully expanded beyond the early adopter aesthetic medicine consumer segment toward mainstream accessibility.

Market Size and Forecast

-

Market Size in 2026E: USD 2.81 Billion

-

Market Size by 2035: USD 6.88 Billion

-

CAGR: 10.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cellulite Treatment Market - Request Free Sample Report

Cellulite Treatment Market Trends

-

Rapid adoption of combination treatment protocols that sequentially or simultaneously deploy multiple energy modalities including radiofrequency, acoustic wave therapy, laser, and infrared light to address different structural contributors to cellulite from different tissue depth perspectives, producing superior aesthetic outcomes compared with single-modality treatment and increasing average revenue per patient encounter for aesthetic medicine practitioners.

-

Growing development of AI-guided energy delivery systems that dynamically adjust radiofrequency, ultrasound, and laser parameters during treatment based on real-time tissue temperature and response feedback, optimising treatment efficacy within each patient's specific tissue characteristics and safety parameters without requiring the manual adjustment judgements that create inter-operator result variability in current treatment platforms.

-

Increasing interest in injectable treatment approaches beyond the withdrawn Qwo collagenase therapy, including investigational phosphatidylcholine and deoxycholate formulations, emerging peptide-based injectable remodelling agents, and novel subcision approaches using blunt cannula techniques that can be performed in office settings with local anaesthesia rather than requiring the specialised training and equipment of original Cellfina technology.

-

Rising demand for cellulite treatment among male patients as changing aesthetic norms and reduced social stigma around male cosmetic procedure seeking are expanding the historically female-dominant cellulite treatment patient base, with treatments emphasising improvement of skin texture and firmness rather than the aesthetic language of traditional cellulite marketing better aligned with male patient motivations.

-

Growing body-positive cultural discourse creating complex market dynamics where acceptance of natural body diversity reduces some treatment-seeking behaviour while simultaneously expanding awareness of available treatment options among the significant proportion of individuals for whom cellulite represents a meaningful source of aesthetic self-consciousness that motivates investment in professional treatment.

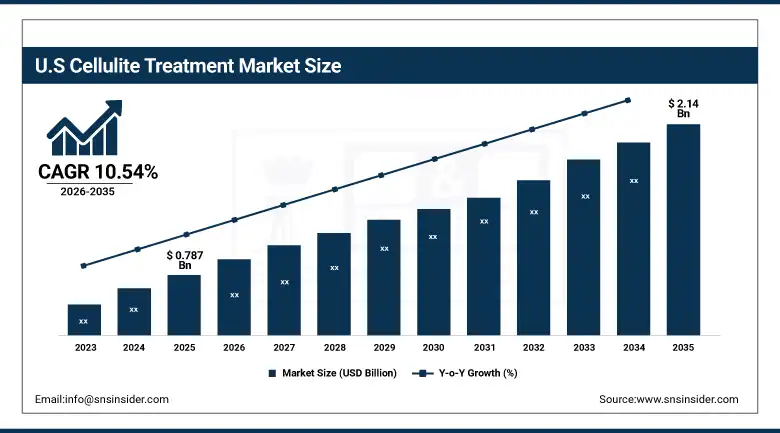

U.S. Cellulite Treatment Market Outlook

The U.S. Cellulite Treatment Market was valued at approximately USD 0.787 billion in 2025 and is expected to reach approximately USD 2.14 billion by 2035, growing at a CAGR of 10.54%, driven by high consumer awareness of available cellulite treatments, strong aesthetic spending culture, a well-developed medical spa and dermatology practice infrastructure deploying FDA-cleared devices, and the continued innovation activity of U.S. aesthetic device manufacturers competing for market share in the non-invasive body contouring category.

The United States is the world's largest cellulite treatment market by both revenue and treatment volume, where the combination of high per-capita disposable income, strong cultural emphasis on aesthetic self-care and body image, a dense network of medical spas, dermatology practices, and plastic surgery centres offering FDA-cleared cellulite treatment systems, and the world's most active aesthetic medical device innovation ecosystem collectively create favourable conditions for sustained market growth. The American aesthetic medicine market's maturity means that consumers have access to the full range of cellulite treatment options across all price tiers, from non-surgical device-based treatments at medical spas through minimally invasive subcision procedures at surgical practices, and the competitive market environment drives both pricing accessibility and continuous technology innovation that expands the treatable patient population. Significant insurance and consumer financing infrastructure including CareCredit enables a broader income spectrum of patients to access premium cellulite treatments than would be possible under cash-only purchase dynamics.

The U.S. aesthetic device market's pattern of technology adoption suggests that the next generation of cellulite treatment devices using AI-guided energy delivery, in-device biological response monitoring, and combination modality integration currently in advanced development and clinical investigation stages will achieve significant commercial penetration within the 2026 to 2035 forecast period, sustaining above-market revenue growth for the categories of aesthetic device companies that successfully navigate the FDA clearance pathway for these innovations.

Cellulite Treatment Market Segment Analysis

-

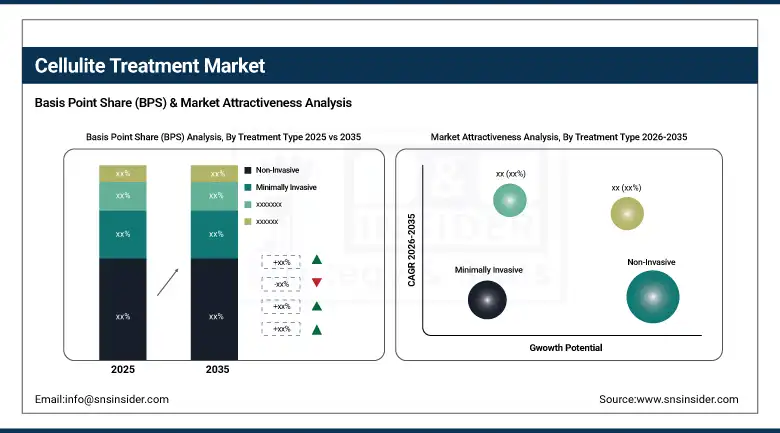

By Treatment Type, Non-Invasive treatments dominated with approximately 48% of revenues in 2025 through their broad accessibility, absence of recovery time requirements, and patient preference for procedures that improve cellulite appearance without needles, incisions, or anaesthesia; Minimally Invasive procedures are the fastest-growing treatment type driven by clinical evidence demonstrating superior and more durable outcomes compared with non-invasive options for moderate to severe cellulite grades.

-

By Cellulite Type, Soft Cellulite held the largest share in 2025 as the most prevalent presentation among women with advancing age and reduced skin elasticity that drives the largest patient population seeking treatment; Hard Cellulite is the fastest-growing segment as the younger female demographic seeking treatment for this firmer, more structurally complex presentation is growing with the entry of younger aesthetic medicine consumers.

-

By End User, Specialized Dermatology Clinics dominated as the largest revenue-generating setting in 2025 through their combination of advanced device technology, physician supervision, medical credentialling that enables all treatment types, and the clinical reputation that builds patient confidence for investment in premium procedures; Medical Spas and Beauty Centers are growing rapidly as expanding spa sector treatment menus and trained aesthetician delivery of non-invasive protocols bring cellulite treatment within reach of mainstream consumer pricing and geographic accessibility.

By Treatment Type, Non-Invasive dominates, Minimally Invasive is expected to grow fastest

Non-Invasive treatments retained the dominant position with approximately 48% of cellulite treatment market revenues in 2025, reflecting the fundamental commercial advantage that treatments requiring no needles, no incisions, no anaesthesia, and no recovery time have in the aesthetic consumer market where patient willingness to invest in appearance improvement is highly sensitive to the perceived risk, discomfort, and lifestyle disruption associated with treatment. Radiofrequency devices including Thermage FLX, Venus Legacy, Exilis Ultra, and BTL Vanquish create volumetric tissue heating that stimulates collagen remodelling and tightening of the dermal and subdermal connective tissue contributing to cellulite appearance, achieving visible improvement in skin texture and firmness through a series of comfortable sessions that most patients can fit into working-day schedules. Acoustic wave therapy delivered through handheld applicators creates mechanical stress waves that disrupt fat cell membranes, stimulate circulation, and promote connective tissue remodelling through biological mechanisms distinct from thermal approaches, providing a complementary tool for combination protocols and a standalone option in the lower price tier of professional cellulite treatment offerings.

Minimally Invasive procedures are the fastest-growing treatment type as the clinical evidence that subcision-based approaches achieve superior aesthetic outcomes with measurably longer duration of improvement compared with non-invasive energy-based treatments has prompted a growing segment of cellulite patients to accept the needle-based intervention requirement in exchange for more durable and dramatic results. The Aveli system's FDA clearance for cellulite treatment using an acoustic micropulse blade to release fibrous septae under real-time visualisation has introduced a technically accessible minimally invasive subcision approach that trained dermatologists and plastic surgeons can perform in office settings with local anaesthesia, expanding the minimally invasive cellulite treatment patient population beyond the specialised practitioner base that Cellfina required.

By End User, Specialized Dermatology Clinics dominate, Medical Spas are expected to grow fastest

Specialized Dermatology Clinics retained the dominant end-user position in the cellulite treatment market in 2025 as the preferred setting for both the most advanced non-invasive device-based treatments and all minimally invasive and surgical cellulite procedures that require physician supervision, medical facility credentials, and the clinical expertise to manage the full spectrum of patient presentations from mild to severe cellulite grades with appropriate treatment selection and technique. Board-certified dermatologists and plastic surgeons operating within practice environments that provide malpractice insurance coverage, sterile procedure rooms, and emergency response capability are the qualified practitioners for the FDA-cleared minimally invasive cellulite treatments that represent the highest-revenue, highest-margin segment of the professional cellulite treatment market. The concentration of premium aesthetic medical device installations in dermatology practices reflects the capital investment capacity and patient volume justification that established medical practices can sustain relative to newer entrant aesthetic businesses.

Medical Spas and Beauty Centers are the fastest-growing end-user category as the continued expansion of the medical spa sector across North America, Europe, and Asia Pacific is creating a rapidly expanding distribution network for non-invasive cellulite treatment devices operated by trained aestheticians and nurses under physician medical directorship that brings professional-grade treatments to consumer pricing tiers and geographic locations previously served only by topical products. The democratisation of access to aesthetic device treatments through medical spa delivery has substantially expanded the cellulite treatment patient population by making effective non-invasive treatments accessible at price points and appointment availability that full-service dermatology practice delivery cannot offer at scale. Medical spa chains including Ideal Image and LaserAway provide standardised protocols, package pricing, and national network accessibility that creates a new mass-market distribution channel for non-invasive cellulite treatment beyond the historically premium medical practice setting.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.5% |

|

Europe |

Germany |

23.8% |

|

Asia Pacific |

South Korea |

36.7% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.6% |

North America Cellulite Treatment Market Insights

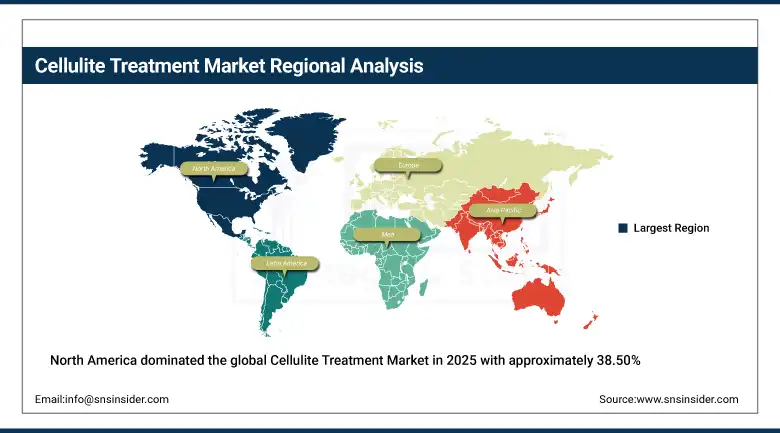

North America dominated the global Cellulite Treatment Market in 2025 with approximately 38.50% of revenues, with the United States accounting for approximately 84.5% of North American revenues. The region's market leadership reflects the combination of the world's most commercially developed aesthetic medicine sector, the highest per-capita aesthetic procedure spending among major economies, the most active medical device innovation and FDA clearance pipeline for cellulite treatment technologies, and a consumer culture where investment in appearance and body confidence is broadly normalised across age groups and income levels. Canada contributes the remaining approximately 15.5% of North American revenues through a comparable aesthetic medicine culture and medical spa infrastructure, though Health Canada's medical device licensing requirements create additional regulatory compliance steps that somewhat delay the availability of the latest U.S.-cleared cellulite treatment technologies in the Canadian market relative to their U.S. launch timing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cellulite Treatment Market Insights

Europe is a large and mature cellulite treatment market anchored by the four largest aesthetics markets of Germany, France, Italy, and the United Kingdom, where a combination of mature aesthetic medicine culture, advanced dermatology practice infrastructure, and consumer willingness to invest in professional body contouring treatments creates consistent demand for both professional device-based procedures and high-end topical treatment products. Germany accounts for approximately 23.8% of European cellulite treatment revenues as the region's largest national market, characterised by physician-dominant aesthetic treatment delivery, preference for evidence-based treatment protocols, and strong adoption of advanced energy-based device platforms from European aesthetic technology leaders including Zimmer MedizinSysteme, Cymedics, and the German operations of global aesthetic device companies. The Mediterranean markets of Italy, Spain, and Greece show particularly high aesthetic procedure acceptance among female consumers for whom body appearance investment is culturally normalised, creating above-average per-capita cellulite treatment revenue in these markets.

Asia Pacific Cellulite Treatment Market Insights

Asia Pacific is the fastest-growing regional cellulite treatment market with a CAGR of 11.26% through 2035, driven by expanding disposable income and aesthetic spending among middle-class female consumers in China, India, South Korea, Thailand, and across Southeast Asia, the extraordinary growth of medical tourism destinations including Thailand, South Korea, and India attracting international patients seeking high-quality aesthetic treatments at prices substantially below home market costs, and the powerful influence of Korean aesthetic culture and beauty standards that have elevated aesthetic procedure acceptance across the Asian consumer landscape through hallyu cultural exports and K-beauty content ecosystems. South Korea accounts for approximately 36.7% of Asia Pacific cellulite treatment revenues as the region's most advanced aesthetic medicine market per capita, where a dense network of specialist dermatology and plastic surgery clinics, rapid technology adoption culture, and strong domestic aesthetic device manufacturing capability create the world's most sophisticated aesthetic treatment environment for procedures including cellulite reduction.

MEA & Latin America Cellulite Treatment Market Insights

The Middle East and Africa and Latin America are growing cellulite treatment markets where expanding aesthetic medicine sector development, rising female consumer spending on body confidence treatments, and in the case of Latin America, strong cultural emphasis on physical appearance and body aesthetics create receptive consumer demographics for professional cellulite treatment investment. UAE leads MEA cellulite treatment revenues at approximately 31.2% of regional revenues through its high per-capita income, premium aesthetic clinic density in Dubai and Abu Dhabi, and consumer population with high aesthetic procedure acceptance supported by easy access to the latest FDA and CE-cleared device technologies through Gulf region distributors of major international aesthetic device brands. Brazil accounts for approximately 44.6% of Latin American revenues as the world's second-largest aesthetic procedure market by procedure volume, where the cultural prominence of body aesthetics and the extensive infrastructure of aesthetic dermatology and plastic surgery practices create a large and commercially significant market for professional cellulite treatment alongside the substantial domestic topical treatment retail market.

Market Dynamics

Growth Drivers: FDA-cleared device technology achieving meaningful clinical outcomes driving patient conversion from topical self-treatment to professional procedures, combined with medical spa sector expansion democratising access to previously premium-priced interventions

The primary structural growth drivers for the Cellulite Treatment Market are the maturation of FDA-cleared minimally invasive and advanced non-invasive treatment technologies that have closed the historical efficacy gap between what patients could realistically expect from cellulite treatment and what motivated initial patient enquiry from consumer media about available options, combined with the medical spa sector's expansion that is progressively democratising access to effective professional treatments across consumer demographics beyond the high-income, early aesthetic adopter segment that constituted the original professional cellulite treatment patient population. The combination of clinical evidence validation for subcision-based minimally invasive treatments, advanced radiofrequency and acoustic wave platforms with demonstrated outcome data, and the entry of investor-backed medical spa chains providing standardised treatment protocols at accessible price points is creating convergent demand growth that reflects both technology maturation pull and distribution channel expansion push.

Restraints: Lack of durable long-term treatment outcomes requiring repeat sessions maintaining per-treatment pricing pressure, high device capital costs limiting treatment provider accessibility, and consumer body image discourse complexity affecting market messaging approach

A significant restraint on the Cellulite Treatment Market is the persistent challenge that most cellulite treatment modalities demonstrate effectiveness in improving cellulite appearance during and shortly following treatment completion but face evidence limitations for sustained multi-year outcome durability, as the underlying fat distribution patterns and connective tissue structural factors that create cellulite are not permanently eliminated by current treatment approaches. This durability limitation creates patient satisfaction challenges when improvements visible at three to six months post-treatment partially regress over one to two years, motivating maintenance treatment investment but also limiting referral enthusiasm among some patient cohorts whose realistic outcome expectations were not adequately calibrated during initial consultation. The capital cost of advanced radiofrequency, acoustic wave, and laser platforms ranges from USD 50,000 to over USD 200,000 per device, creating barrier-to-entry challenges for smaller practice settings and single-practitioner aesthetic businesses that limit the total addressable distribution network for professional cellulite treatment.

Opportunities: Next-generation subcision and combination platform development addressing durability limitations, AI-powered personalised treatment protocols improving outcome predictability, and male aesthetic consumer market development for cellulite treatment

The development of next-generation minimally invasive treatment platforms that combine subcision technology with volumetric tissue remodelling energy delivery in a single treatment session represents the most commercially significant innovation pathway in the cellulite treatment market, as the combination of mechanical septae release that addresses the structural tethering responsible for cellulite dimpling with concurrent radiofrequency or laser tissue remodelling that stimulates new collagen formation to fill the released dimple volume addresses both the primary structural cause and the secondary volume deficit that create the visible cellulite appearance simultaneously in one procedure. The male aesthetic consumer market for cellulite treatment represents an underserved growth opportunity as changing male aesthetic norms, reducing stigma around male cosmetic procedure seeking, and the increasing fitness culture emphasis on body composition and skin quality among active male demographics create a growing patient segment whose specific anatomical cellulite presentation and aesthetic motivations differ from the female patient majority that has historically defined the category's product development and clinical protocol design focus.

Recent Developments:

-

February 2025: Lumenis and Cynosure co-hosted the inaugural aesthetic medicine technology summit in Miami, Florida, featuring sessions focused on next-generation laser therapies, radiofrequency, and ultrasound-assisted cellulite treatments led by renowned cosmetic dermatologists, establishing a collaborative industry education format for professional cellulite treatment technique development and outcome optimisation.

-

January 2025: RealSelf reported a 40% increase in cellulite treatment interest among U.S. women compared with the prior year period, driven by increased influencer content featuring professional cellulite treatment experiences, rising consumer aesthetic spending, and growing seasonal body-shaping demand across a broadening demographic range of aesthetic procedure consumers.

-

August 2025: Cytrellis Biosystems received Canadian and Saudi Arabian regulatory approvals for its Ellacor Micro-Coring technology system for skin tightening, expanding the geographic availability of minimally invasive precision tissue removal platforms that address the skin laxity component contributing to cellulite appearance in patients with concurrent skin quality concerns alongside structural dimpling.

-

April 2024: Caliway Biopharmaceuticals announced successful Phase 2 results for CBL-514, an injectable therapy designed specifically to treat raised cellulite areas through targeted adipose tissue reduction in the protrusions that create the textured cellulite appearance, representing the first clinical success for an injectable approach that addresses elevated rather than depressed cellulite elements.

-

2025: BTL Aesthetics expanded its EMTONE combination platform adoption among U.S. medical spa and dermatology practices, with the simultaneously delivered radiofrequency and targeted pressure energy system gaining market share as combination energy delivery without sequential device application demonstrated improved patient experience and treatment efficiency advantages in busy aesthetic practice environments.

Cellulite Treatment Market Key Players

-

Cynosure LLC

-

Lumenis Ltd.

-

InMode Ltd.

-

BTL Aesthetics

-

Zimmer Aesthetics

-

Cutera Inc.

-

Merz Pharma GmbH & Co. KGaA

-

Hologic Inc.

-

Galderma

-

Allergan Aesthetics (AbbVie)

-

Solta Medical

-

Sinclair Pharma

-

Venus Concept

-

Invasix Ltd.

-

Nubway Co. Ltd.

-

Cymedics

-

Inceler Medikal Co. Ltd.

-

Cartessa Aesthetics

-

EndyMed Medical

-

Cytrellis Biosystems

Cellulite Treatment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.54 Billion |

| Market Size by 2035 | USD 6.88 Billion |

| CAGR | CAGR of 10.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Non-Invasive, Minimally Invasive, Topical, Surgical) • By Cellulite Type (Soft Cellulite, Hard Cellulite, Edematous Cellulite) • By End User (Specialized Dermatology Clinics, Medical Spas & Beauty Centers, Hospitals, Home Care) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cynosure LLC, Lumenis Ltd., InMode Ltd., BTL Aesthetics, Zimmer Aesthetics, Cutera Inc., Merz Pharma GmbH & Co. KGaA, Hologic Inc., Galderma, Allergan Aesthetics (AbbVie), Solta Medical, Sinclair Pharma, Venus Concept, Invasix Ltd., Nubway Co. Ltd., Cymedics, Inceler Medikal Co. Ltd., Cartessa Aesthetics, EndyMed Medical, Cytrellis Biosystems |

Frequently Asked Questions

North America dominated with approximately 38.50% of revenues in 2025.

Non-Invasive treatments dominated with approximately 48% of revenues in 2025.

FDA-cleared non-invasive and minimally invasive treatment technology achieving meaningful clinical outcomes for the first time driving patient conversion from topical products to professional procedures, combined with medical spa sector expansion democratising access to effective treatments across a broader income and geographic consumer spectrum.

The Cellulite Treatment Market was valued at USD 2.54 billion in 2025.

The Cellulite Treatment Market is expected to grow at a CAGR of 10.47% from 2026 to 2035.

Get in Touch