Chemical Peel Market Report Scope & Overview:

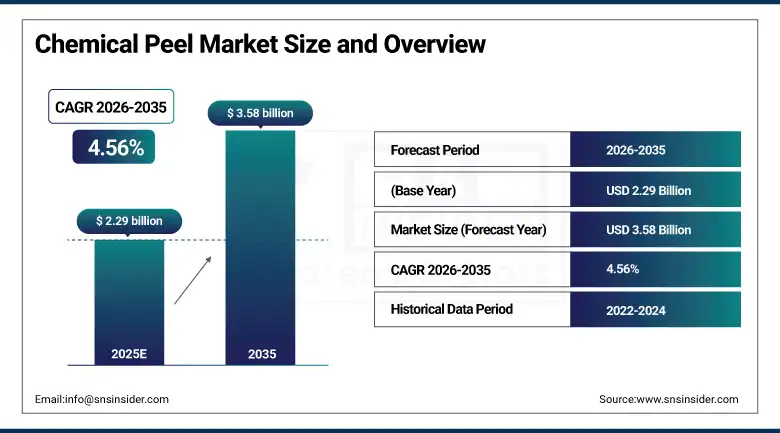

Chemical Peel Market was valued at USD 2.29 billion in 2025 and is expected to reach USD 3.58 billion by 2035, growing at a CAGR of 4.56% from 2026–2035.

The chemical peel market is expanding globally due to increased consumer inclination towards non-surgical cosmetic treatments, high incidences of skin conditions like acne, hyperpigmentation, and photoaging, as well as rapid growth in the number of dermatology clinics and medical spas in mature and developing economies. Chemical peeling involves application of specially blended acids to the skin surface in order to facilitate exfoliation and improve skin texture through collagen restructuring, melanin realignment, and cellular regeneration. Over 1.4 million chemical peel treatments were conducted in the United States in 2023, according to records from the American Society of Plastic Surgeons. The introduction of more sophisticated formulas containing AHAs, BHAs, and TCA at optimized concentrations has led to reduced risk of irritation, broadened scope of skin types suitable for treatment, and improved safety standards, which are factors behind the popularity of the procedure among physicians. Teledermatology services and skincare subscription models are helping democratize access to chemical peel consultations by demographics that were hitherto geographically or financially disenfranchised.

The 4.56% CAGR growth rate of the chemical peel market from 2026 to 2035 is supported by the ever-growing base of the global elderly population who seek out aesthetic treatments for anti-aging purposes, the increasing acceptance of chemical peels as scientifically proven treatments for various dermatological disorders besides cosmetic reasons, and innovations in chemical peel formulations that have been increasingly catering to the dermatological needs of patients with dark skin tones. The partnership between Estee Lauder Companies and the lab of Dr. Robert Langer at MIT in January 2025 to develop innovations in cosmetic science and the introduction of SKINVIVE by JUVEDERM by AbbVie's Allergan Aesthetics as an FDA-approved intradermal treatment complementing chemical peels serve as two instances of innovation driving market growth.

Market Size and Forecast

-

Study Period: 2022–2035

-

Market Size (2025E): USD 2.40 Billion

-

Market Size 2035: USD 3.58 Billion

-

CAGR: 4.56% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Chemical Peel Market - Request Free Sample Report

Chemical Peel Market Trends

-

Accelerating development of combination peel formulations blending AHAs, BHAs, kojic acid, and retinoids that address multiple skin concerns simultaneously, reducing procedure frequency while improving treatment economics for both practitioners and patients.

-

Rapid expansion of the medical spa sector as the primary growth channel for chemical peel procedures, with the global medical spa industry growing at 12 to 15% annually and creating tens of thousands of new treatment points adopting standardized peel protocols as core service menu offerings.

-

Rising consumer interest in peel treatments for skin tone evenness across all ethnic skin types driven by K-beauty's global influence, expanding chemical peel market engagement beyond the historically Caucasian-dominant aesthetic procedure patient population to South Asian, East Asian, and Latin American demographics.

-

Growing integration of chemical peels with complementary energy-based procedures including laser resurfacing and microneedling in multimodal anti-aging protocols, increasing average patient spend per treatment cycle and expanding addressable market size for each individual procedure category.

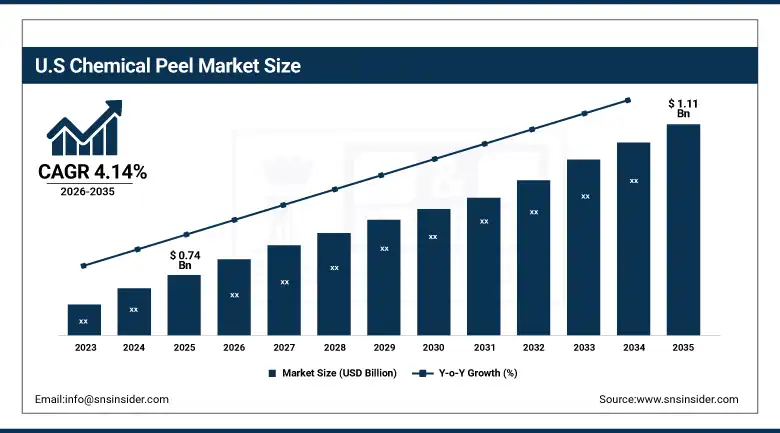

U.S. Chemical Peel Market Size Outlook

U.S. Chemical Peel Market was valued at approximately USD 0.74 billion in 2025 and is expected to reach USD 1.11 billion by 2035, growing at a CAGR of approximately 4.14%, driven by robust consumer spending on anti-aging procedures, advanced dermatology infrastructure, and the early adoption of innovative chemical peel formulations.

The United States holds the position of being the biggest national market for chemical peel treatments based on consumer willingness to purchase professional skin care services, the presence of an extensive network of board-certified dermatologists in excess of 12,000 and medical spas, and the market dominance of companies such as The Estee Lauder Companies, Obagi Medical, SkinCeuticals, and ZO Skin Health that set global standards for chemical peel treatments. The level of sophistication in the U.S. market can be seen in the rising popularity of combination treatments that incorporate chemical peels alongside laser treatments, microneedling, and injectables for delivering superior results than a single modality approach would yield.

The Estee Lauder Companies made public a strategic alliance with the laboratory of Dr. Robert Langer at MIT in January 2025 for undertaking groundbreaking research into cosmetic science including innovative delivery systems for active ingredients that will be used in future chemical peel treatments. Such a collaboration underscores the dedication of the premium skincare industry to raising the scientific standards of peel formulae to pharmaceutical levels during the forecast period of 2026 to 2035.

Chemical Peel Market Segment Highlights

-

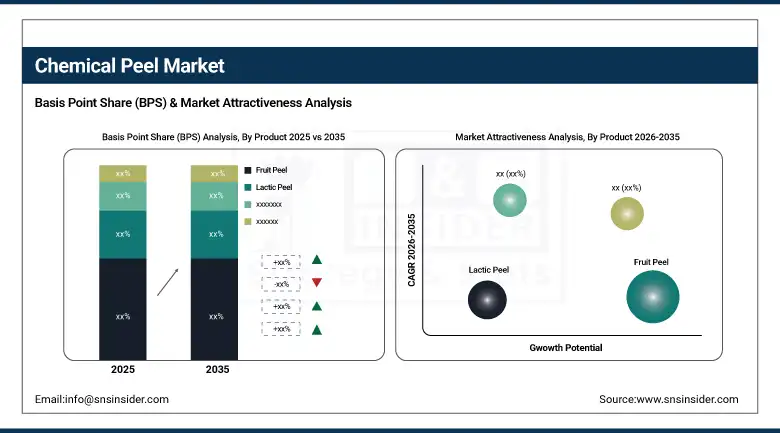

By Product, Fruit Peel dominated with approximately 24.10% revenue share in 2025; Lactic Peel is expected to grow fastest through 2026 to 2035, driven by its dual AHA exfoliating and natural moisturizing factor properties that make it uniquely suited for sensitive and darker skin tones underserved by more aggressive peel chemistries.

-

By Type, Superficial/Light Peel held the highest revenue share in 2025 due to minimal downtime and broad safety profile; Medium Peel is expected to grow at the fastest CAGR driven by increasing demand for treatments addressing moderate wrinkles, acne scars, and deeper pigmentation with single-session efficacy.

-

By Application, Acne Spots dominated in 2025 driven by rising global acne prevalence; Dark Circles is expected to grow fastest from 2026 to 2035 driven by escalating periorbital pigmentation concerns among working and geriatric populations globally.

-

By End Use, Dermatology Clinics led with approximately 72.2% revenue share in 2025; Med Spa is expected to grow fastest from 2026 to 2035 driven by rising demand for luxury non-invasive cosmetic services with consumer-friendly scheduling and accessible pricing models.

By Product, Fruit Peel dominates, Lactic Peel expected to grow fastest

The Fruit Peel product type retained its leading position in the global Chemical Peel Market by product with a share of roughly 24.10% of total revenues owing to the vast body of clinical evidence in its support from decades of research published in dermatological journals regarding its efficacy in the treatment of acne, photoaging, and hyperpigmentation in various forms using glycolic acid, citric acid, and malic acid over more than three decades of research. This product's leadership is also aided by the large body of practitioner training programs available to support its usage through various dermatological and aesthetic clinics worldwide in products like SkinCeuticals, IMAGE Skincare, and NeoStrata.

The Lactic Peel product type is forecasted to be the fastest-growing segment in the global Chemical Peel Market with a CAGR through 2026 to 2035 owing to its unique two-pronged action as both an AHA as well as a natural moisturizing agent, excellent tolerance with darker fitzpatrick phototype skin types without any risk of post-inflammatory hyperpigmentation in other acid concentrations, and the increasing body of clinical evidence in favor of using lactic acid as the introductory peel for treatment-naive patients suffering from sensitive skin conditions.

By End Use, Dermatology Clinics dominate, Med Spa grows fastest

Dermatology Clinics retained the commanding position in the global Chemical Peel Market in 2025 with approximately 72.2% of revenues, reflecting deep patient trust in physician-supervised peel administration, practitioner prescribing authority for highest-concentration formulations including medium-depth TCA and deep phenol peels requiring clinical supervision, and the extensive clinical evidence and practitioner education programs of brands including Obagi Medical, ZO Skin Health, and SkinMedica that have established dermatology clinics as the primary channel for professional peel delivery globally.

The Med Spa end-use segment is expected to grow at the fastest CAGR through 2026 to 2035, driven by the exceptional commercial momentum of the global medical spa industry whose accessibility, luxury environment, competitive pricing, and online booking convenience are attracting consumer demographics that find traditional dermatology clinic environments time-inefficient or cost-prohibitive for elective aesthetic procedures. Brands including IMAGE Skincare, PCA Skin, and Dermalogica are developing med spa-specific peel education and treatment menu systems establishing chemical peels as a standardized service category across the rapidly expanding global med spa network.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~83% |

|

Europe |

Germany |

~27% |

|

Asia Pacific |

China |

~32% |

|

Middle East & Africa |

UAE |

~36% |

|

Latin America |

Brazil |

~51% |

North America Chemical Peel Market Insights

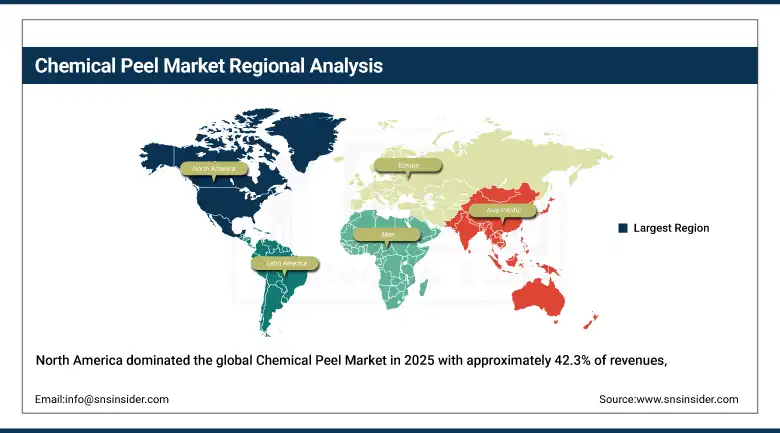

North America dominated the global Chemical Peel Market in 2025 with approximately 42.3% of revenues, anchored by the United States whose robust consumer spending on anti-aging procedures, over 1.4 million annual peel procedures, and established market presence of leading peel brands create the world's highest-revenue national market. The region benefits from advanced dermatology infrastructure, early adoption of innovative formulations, and strong brand presence across both professional clinic and direct-to-consumer channels.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chemical Peel Market Insights

Europe represents a sophisticated chemical peel market where Germany's advanced dermatology specialty infrastructure, France's cosmetic science heritage, and the United Kingdom's large and affluent aesthetic medicine consumer base collectively create the second-largest regional market. EU Cosmetics Regulation enforcement of ingredient safety standards and the European aesthetic medicine community's strong evidence-based practice culture define the region's premium positioning for professional peel product development.

Asia Pacific Chemical Peel Market Insights

Asia Pacific is the fastest-growing region with approximately 5.62% CAGR through the forecast period, driven by the K-beauty movement's elevation of skin tone uniformity to a universal beauty standard across Korean, Japanese, Chinese, Indian, and Southeast Asian markets, and the surging aesthetic clinic openings across South Korea, China, Japan, and India supported by medical tourism and a growing middle class. The region's high clinical prevalence of melasma and post-inflammatory hyperpigmentation creates exceptional structural demand for peel formulations addressing pigmentation disorders.

Middle East & Africa and Latin America Chemical Peel Market Insights

The UAE leads MEA chemical peel revenues through Dubai's concentration of world-class aesthetic medicine clinics serving affluent international consumers with high sun exposure-driven pigmentation treatment demand. Brazil dominates Latin American market revenues through its globally recognized aesthetic medicine culture where cosmetic procedures are socially normalized, combined with high clinical prevalence of melasma among Brazilian women of mixed ethnic backgrounds creating exceptional demand for hyperpigmentation-targeting lactic and glycolic acid peel protocols.

Market Dynamics

Growth Drivers: Rising global prevalence of acne, hyperpigmentation, and skin aging concerns creating sustained clinical and consumer demand for chemical peel interventions

The primary structural growth driver for the Chemical Peel Market is the widening gap between the extraordinary global clinical burden of treatable skin conditions — acne affecting an estimated 85% of people aged 12 to 24, melasma affecting 15 to 35% of women of reproductive age, and photoaging affecting virtually all adults in high sun exposure geographies — and growing consumer awareness that chemical peels represent a cost-effective, evidence-based, minimally invasive intervention delivering measurable improvements within clinically meaningful timeframes. The growing global aging population, as forecasted by the United Nations to double the over-60 population from 2020 to 2050, provides a growing consumer base for anti-aging procedures. The normalization of aesthetic procedure sharing on social media platforms by younger generations is resulting in a reduction of age at first peel and an increase in lifetime peeling procedure frequency within the next generation of aesthetic consumers.

The Estee Lauder Companies entered into a research collaboration with Dr. Robert Langer's laboratory at MIT in January 2025 for innovative developments in cosmetic science related to active ingredient delivery and skin biology, which will aid in developing formulations for chemical peels. This indicates ongoing prestige industry investment in the advancement of peel science, ensuring that there is continued improvement in efficacy, safety, and patient pool of professional peels in the forecast period up to 2026 to 2035.

Restraints: Risk of adverse events in people with darker skin, downtime issues related to treatments, and competition from energy-based treatments that prevent fast patient adoption rates

One major limitation to the Chemical Peel Market is the increased risk of post-inflammatory hyperpigmentation among individuals having fitzpatrick phototypes IV to VI, which makes up the majority of patients who belong to the South Asian, East Asian, Middle Eastern, African, and Latin American population. Medium and deep chemical peeling may even exacerbate the issue of pigmentation in these individuals, despite being the primary cause of seeking treatment. The downtime period of between five to fourteen days following medium and deep peels is one practical drawback, forcing professionals to resort to superficial peels and energy-based treatments.

Opportunities: Precision peel formulations for diverse skin tones, at-home peel premiumization, and teledermatology-enabled prescription access

The most significant commercial opportunity in the chemical peel market is the development of precision peel formulations specifically engineered for fitzpatrick phototype IV through VI skin, representing the majority of the world's population whose underrepresentation in clinical trials has limited the practitioner evidence base for diverse skin tone peel protocols. The at-home premium peel segment offers high-growth opportunity as prestige brands invest in refined AHA and BHA formulations in sophisticated drug delivery systems including encapsulated acid microspheres and buffered acid gels that maximize efficacy within consumer-safe parameters. Teledermatology platforms enabling remote practitioner-supervised peel programs dramatically expand geographic access beyond physical clinic locations to previously excluded demographics.

Recent Developments:

-

January 2025: The Estee Lauder Companies Inc. revealed a strategic partnership with MIT, collaborating with the laboratory of Dr. Robert Langer to advance leading-edge research and innovation across cosmetic science including active ingredient delivery technology and next-generation peel formulation chemistry, representing the most significant academic-industry skincare research partnership announced in 2025.

-

May 2023: AbbVie's Allergan Aesthetics received FDA approval for SKINVIVE by JUVEDERM, the first HA-based intradermal microdroplet injection approved in the United States to improve skin smoothness in adult cheeks, establishing a complementary non-invasive treatment increasingly combined with superficial peel protocols in multimodal skin quality improvement programs at dermatology clinics and aesthetic practices.

Chemical Peel Market Key Players

-

Allergan Aesthetics (AbbVie Inc.)

-

L'Oreal S.A.

-

Procter & Gamble

-

Johnson & Johnson

-

Pierre Fabre Group

-

The Estee Lauder Companies Inc.

-

Obagi Medical

-

Epionce

-

NeoStrata Company Inc. (J&J)

-

IMAGE Skincare

-

DERMAdoctor LLC

-

Murad LLC (Unilever)

-

Replenix

-

ZO Skin Health Inc.

-

Glytone

-

SkinCeuticals (L'Oreal)

-

Alma Lasers

-

Vivier Pharma

-

Dermalogica (Unilever)

-

SkinMedica (AbbVie)

Chemical Peel Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.29 Billion |

| Market Size by 2035 | USD 3.58 Billion |

| CAGR | CAGR of 4.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Lactic Peel, Fruit Peel, Salicylic Acid Peel, Pigment Balancing Peel, Trichloroacetic Acid Peel, Vitalize Peel) •By Type (Superficial/Light Peel, Medium Peel, Deep/Phenol Peel) •By Application (Acne Spots, Wrinkles, Fine Lines, Hyperpigmentation, Scars, Dark Circles, Skin Brightening) •By End Use (Hospitals, Med Spa, Dermatology Clinics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Allergan Aesthetics (AbbVie Inc.), L'Oreal S.A., Procter & Gamble, Johnson & Johnson, Pierre Fabre Group, The Estee Lauder Companies Inc., Obagi Medical, Epionce, NeoStrata Company Inc. (J&J), IMAGE Skincare, DERMAdoctor LLC, Murad LLC (Unilever), Replenix, ZO Skin Health Inc., Glytone, SkinCeuticals (L'Oreal), Alma Lasers, Vivier Pharma, Dermalogica (Unilever), and SkinMedica (AbbVie) |

Frequently Asked Questions

North America dominated the Chemical Peel Market in 2025 with approximately 42.3% of global revenues, led by the United States whose robust consumer spending on anti-aging procedures, over 1.4 million annual peel procedures, advanced dermatology infrastructure, and established market leadership of major peel brand innovators collectively create the world's largest national market.

Dermatology Clinics dominated the market in 2025 with approximately 72.2% of revenues, driven by consumer trust in physician-supervised peel administration, practitioner prescribing authority for the highest-concentration professional formulations, and the extensive clinical evidence and education programs of leading chemical peel brands.

Fruit Peel dominated the market in 2025 with approximately 24.10% of revenues, driven by its well-established clinical evidence base for glycolic, citric, and malic acid formulations, universal skin type compatibility, and decades of practitioner familiarity that make it the preferred entry-point peel formulation globally.

The Chemical Peel Market was valued at USD 2.29 billion in 2025.

The Chemical Peel Market is expected to grow at a CAGR of 4.56% from 2026 to 2035.

Get in Touch