Cider Market Report Scope & Overview:

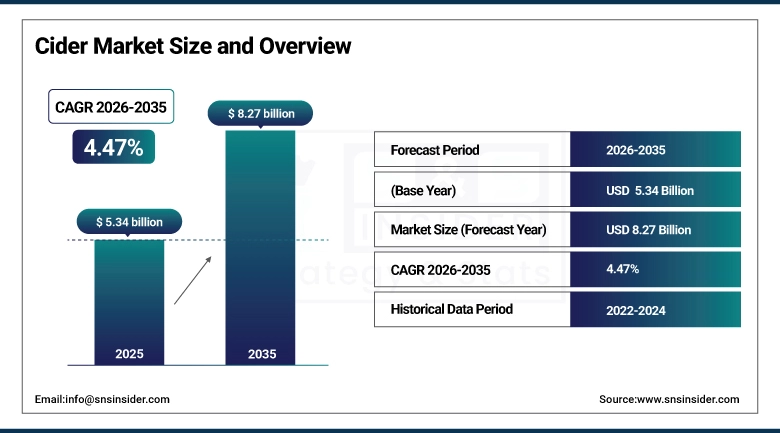

The Cider Market was estimated at USD 5.34 Billion in 2025 and is expected to reach USD 8.27 Billion by 2035 and grow at a CAGR of 4.47% over the forecast period of 2026-2035.

The Cider Market analysis highlights the growing popularity of both alcoholic and non-alcoholic ciders is broadening market penetration throughout urban and rural areas. And packaging innovation in cans and multipacks are making them convenient and portable for consumers. The influx of the premiumization trend and brand varying approaches by market participants have found resonance among younger consumers.

Global cider consumption rose by 9.5% in 2024, with non-alcoholic variants growing fastest at 18%, driven by health-conscious Gen Z and millennial buyers

Market Size and Forecast:

-

Market Size in 2025: USD 5.34 Billion

-

Market Size by 2035: USD 8.27 Billion

-

CAGR: 4.47% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Cider Market - Request Free Sample Report

Cider Market Trends

-

Increasing consumer interest in craft and artisanal cider forges world trends that target flavours, premium packaging styles, and small batch limited edition production.

-

Surging demand for non-alcoholic and low-alcoholic cider variants woo health-conscious and younger consumers, broadening market reach and retail prospects.

-

E-commerce and online retail opportunities are becoming more accessible to facilitate direct-to-consumer cider sales, seasonal promotions and a subs beverage delivery service.

-

Flavored ciders such as berry, citrus or spice-infused blends are rapidly expanding, catering to consumers' thirst for a variety of flavour profiles.

-

Sustainable efforts in production, packaging and logistics are also driving packages including recyclable bottles and environmentally -friendly sourcing as consumers make decisions globally on how they buy.

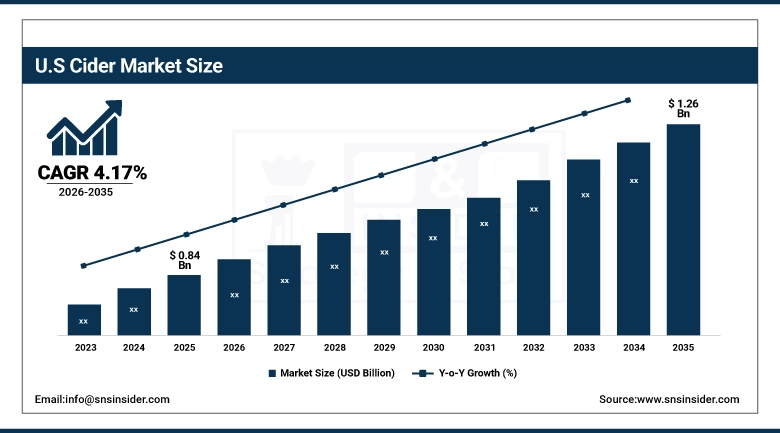

The U.S. Cider Market size is valued at USD 0.84 Billion in 2025 and is projected to reach USD 1.26 Billion by 2035, growing at a CAGR of 4.17% during 2026-2035. Cider Market growth is driven by growing at a steady pace due the increasing popularity of craft, flavored and premium ciders. The move by consumers to natural, low ABV and gluten-free is adding excitement to what can be offered.

Cider Market Growth Drivers:

-

Rising Demand for Flavored, Craft, and Low-Alcohol Ciders Driven by Shifting Consumer Lifestyle Preferences

Rapidly expanding global cider consumption is being fuelled by increasing demand for natural, fruit-based and gluten-free drinks. Craft premium offerings and modern fruit combinations are appealing to younger consumers who wish to consume lighter alcohol products. Category adoption is growing around the world with retail expansion, better branding and new product offerings driving growth. And with more brewery-conversions and Orchard-based micro-cidery operations, market penetration and production scalability are underpinned. Annual cider production from leading orchards supplies 4.8 million tons of processed apples to global manufacturers.

74% of Gen Z and millennial drinkers chose cider over beer for its lower ABV (4–5%) and fruity profile, fueling 20% annual growth in flavored and dry variants

Cider Market Restraints:

-

Competition from Beer, Hard Seltzers, and RTD Alcoholic Beverages Restricts Cider’s Global Growth Momentum

Cider has been running uphill against bigger alcohol categories like beer and seltzers, which enjoy more loyalty and distribution. But cider is still struggling to be competitive, with little shelf visibility, seasonality and a price that is not uniform around the world. Supply-side risks including apple supplies, weather influence and higher processing costs add additional constraints on production. Legal differences and typical alcohol tax systems act as further hurdles in the cross-country scaling up process for cider producers. Global cider consumption relies on 3.1 million tons of imported fruit concentrates supporting year-round beverage production.

Cider Market Opportunities:

-

Expansion of Premium, Organic, and Innovative Fruit-Blend Ciders Unlocks Strong Future Market Growth Pathways

Growth opportunities for cider brands the high demand for organic, clean-list and low-sugar alcoholic beverages is opening up big opportunities for cider brands. Producers are turning to exotic fruits, botanical infusions and hybrid blends to create distinct offerings. Growing awareness for culture of taproom, micro-cideries and e-commerce availability boost the adoption of premium segment. Sustainability programs and local orchard procurement expand consumer confidence and brand status. Export-oriented cider producers ship 820,000 tons of fruit-based formulations annually to expanding international beverage markets.

In 2025, 64% of premium cider buyers actively sought “organic,” “no added sugar,” or “non-GMO” labels, driving a 28% YoY increase in certified clean-label cider launches.

Cider Market Segment Analysis

-

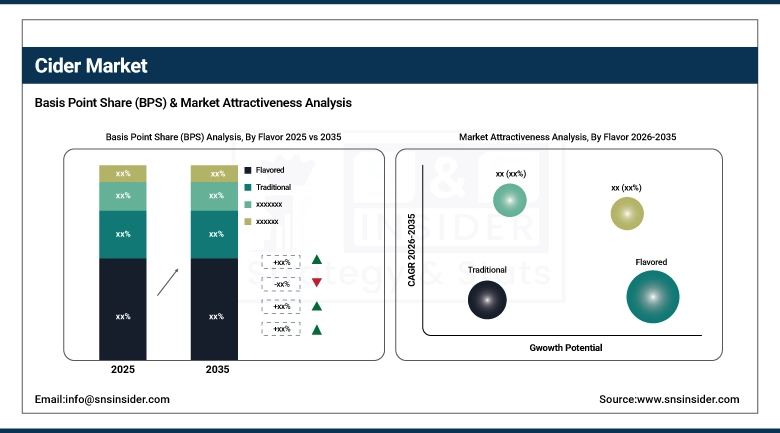

By flavor, the flavored segment led the market with a 64.12% share in 2025, while spiced cider emerged as the fastest-growing segment with a CAGR of 7.10%.

-

By packaging, bottles dominated with a 48.17% share in 2025, whereas cans represented the fastest-growing format, expanding at a 6.25% CAGR.

-

By type, apple cider led with a 65.32% share in 2025, while mixed fruit cider recorded the fastest growth at a 5.52% CAGR.

-

By distribution channel, supermarkets/hypermarkets held a 45.28% share in 2025, with online retail growing the fastest at a 6.82% CAGR.

By Flavor, Flavored Leads Market While Spiced Registers Fastest Growth

Flavored ciders are dominate the market due to it is exported to foreign markets, as consumers demand a fruitier and more refreshing and innovative flavor. Companies are also experimenting with such flavours as berries, tropical fruits and botanical infusions in a bid to attract younger consumers and broaden their premium portfolio. While, spiced ciders made with cinnamon, ginger, nutmeg and various exotic flavor combinations are growing fastest as memories of anything warm, aromatic and festive take hold. Seasonal rollouts, craft players and limited-edition releases are also spurring segment growth at retail and on-premise accounts both domestically and abroad. Global flavored cider production uses 2.9 million tons of processed fruits supplying manufacturers across major cider markets.

By Packaging, Bottles Dominate While Cans Shows Rapid Growth

Bottles cider is the dominating segment due to favorite format with good brand recognition, premium image and a fit with glass driven retail. When consumers see glass bottles, they think authentic, craft and premium formulations all of them are reasons that continue to contribute to a leadership position in the segment. Meanwhile, cans ciders are growing fastest and taking the market by storm as younger buyers score portability, on-the-go ease and environmentally friendly packaging, easy open lids and can go places where a bottle wouldn't stand up as well. Rising preference in festivals, restaurants, and ready to chill forms continues support the demand for aluminium based packaging solutions. Craft brands are increasingly turning to cans in order to capitalize on quick-turn retail opportunities. Global cider packaging consumption includes 1.7 million tons of glass and aluminum materials across production facilities.

By Type, Apple Cider Lead While Mixed Fruit Cider Registers Fastest Growth

Apple cider remains the market leader with plentiful apple availability, cultural heritage and strong production systems. It still has a classic image, is known for what it is, and comes in alcoholic as well as non-alcoholic versions that keep them at the top of their global game. Mixed fruit cider is growing fastest due to trending in exactly the opposite direction, mixed fruit ciders berry-apple cider, mango-pear, tropical blends and more are popping up the most this year due to changing consumer taste preferences for sweeter and more colorful flavor mixes. With the increase of craft production and high-quality fruit sourcing, this category is trending upward. Apple cider production consumes 4.2 million tons of orchard apples annually across global cider-producing regions.

By Distribution Channel, Supermarkets/Hypermarkets Lead While Online Retail Grow Fastest

Supermarkets/hypermarkets continue to lead and are supported by large selection of products, strong brands and high traffic. Their ability to deliver limited-time promotions, multipacks, seasonal flavors and exclusive partnerships also helps consolidating supremacy. While, Online retail is growing at the fastest rate, supported by increasing penetration of e-commerce and convenient at-home delivery options while leading to digital discovery of premium and craft ciders. Subscription services, one-size-fits-all flavor boxes and direct-to-consumer sales are helping expand the market among urban dwellers. Online retail shipments distribute 520,000 tons of assorted cider products annually through global e-commerce logistics networks.

Regional Insights:

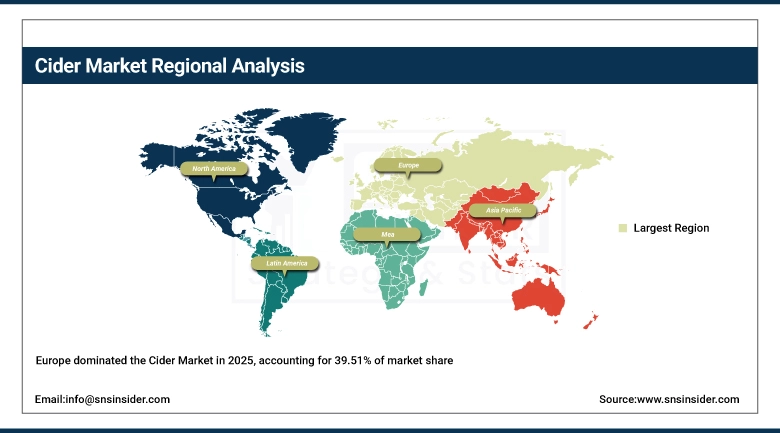

Europe Cider Market Insights

In 2025 Europe dominated the Cider Market and accounted for 39.51% of revenue share, this leadership is due to maintains its status as the global epicenter of cider consumption, with long-standing cultural customs and a wide range of regional styles. The launches of some of the largest markets, including the UK, Ireland, Spain, and France, are complemented by innovative approaches. Interest in premium craft styles, organic blends, and heritage Ciders is expected to grow. The broad product selection offered by retailers boosts market maturity and ensures stable growth. European cider producers process over 3.5 million tons of apples annually for domestic and export markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Germany Market Insights

Germany The German sector maintains its unique characteristics through a regional cider known as “Apfelwein” consumption. Young customers drive market innovation, and flavored and international brands are popular. On-premise driving temporary pacing spikes due to festivals and other seasonal shifts. Domestic producers are exploring wider orchard adaptation and updated packaging options. German cider makers consume 540,000 tons of apples yearly to sustain national cider and Apfelwein production.

Asia-pacific Cider Market Insights

Asia-pacific is expected to witness the fastest growth in the Cider Market over 2026-2035, with a projected CAGR of 4.95% due to new generation adopts flavored and craft-style alcoholic beverages. Rapid urbanization, premium on-trade venues, and increasing awareness of international cider brands stimulate category growth. Local producers rapidly expand capacity to address the growing regional demand, especially in the flavored and low-ABV categories. Australia and Japan uphold the market of the cider hub in Asia; while emerging Southeast Asia markets show consistent tendencies. Regional cider imports supply 310,000 tons of beverages annually to meet expanding Asia-Pacific consumption needs.

China Market Insights

China enjoys the fast development of the cider market with the rise of fruit-based alcoholic beverages among young adults and premium customers. Domestic production benefits from scaling using modern brewing technologies, and diversified fruit blends, and concession of strong international brands continues, which increase through the online retail and premium supermarket chains. China’s cider production utilizes 420,000 tons of domestically sourced apples annually for expanding beverage demand.

North America Cider Market Insights

In 2025, North America emerged as a promising region in the Cider Market, due to premium craft offerings and growing flavors felt in the natural fruit beverages. U.S. and Canada show steady consumption of the bottled and canned ciders in off-trade and on-premise venues. Category growth speeds up through seasonal innovation and lowering the added sugars by most producers. Craft production continues to benefit an integrated orchard supply chain with high-quality apples sourcing. North American cider manufacturers process 1.1 million tons of apples yearly for large-scale beverage production.

U.S. Market Insights

U.S. exemplifies one of the world’s largest cider markets with craft innovation and growing regional orchards. Flavored and mixed-fruit ciders outgrow their traditional competitors, as young adult customers include them into a regular diet. Breweries and cider houses benefit from a developing taproom network expanding their presence in all states. U.S. cider production consumes 820,000 tons of apples annually across commercial and craft cider operations.

Latin America (LATAM) and Middle East & Africa (MEA) Cider Market Insights

The Cider Market is experiencing moderate growth in the Latin America (LATAM) and Middle East & Africa (MEA) regions, due to the expanded market activities as fruit-based beverages become popular in modern retail and e-commerce. Latin America is particularly popular with youngsters, with elsewhere in the world growing the popularity of non-alcohol and low-alcohol variants. International brands are well-established and thriving, thanks to the vast improvements in cold-chain and logistics capabilities. Combined regional cider imports exceed 260,000 tons annually to support growing LATAM and MEA beverage consumption.

Competitive Landscape:

Diageo is further reinforcing its position in the global cider category with premium brand extensions and regional flavor innovations. Its extensive distribution network facilitates increased penetration in supermarkets and bars, driving exposure across developed and developing markets. Sustainability-focused apple sourcing and pinpointed marketing also aid the company grow its high-end cider category presence. Robust seasonal launches additionally generate consumer momentum in North America and Europe. Diageo supported operations with an estimated 110,000 metric tons of cider production across partner facilities last year.

-

In August 2024, Diageo expanded its beverage portfolio by launching a Smirnoff-branded cider, marking the company’s strategic entry into the growing fruit-cider segment. The launch strengthens Diageo’s presence in flavored alcoholic beverages and targets rising consumer demand for refreshing, fruit-forward cider options.

Aston Manor's extensive U.K. history and orchard sourcing keeps it at the forefront of the craft cider category. The lantern company broadens private-label pacts, further penetrates retail chains and value-selling outlets. A product development that is flavor-forward is attractive to younger customers while also maintaining its traditional base. Environmentally friendly packaging investments reinforce premium branding ideology. Aston Manor’s annual cider output reached nearly 95,000 metric tons, supporting both domestic consumption and export shipments.

-

In April 2025, Aston Manor expanded its Crumpton Oaks portfolio by launching two new fruity variants—Strawberry and Berry—aimed at strengthening its appeal among younger consumers. The launch supported growing demand for refreshing, flavour-led ciders across supermarkets and value-oriented retail channels.

C&C Group broadens the distribution of its Magners flagship with scale in marketing and significant distribution synergies. The firm enriches logistics strengths via vertically integrated supply chains in Ireland, the U.K. and mainland Europe. Product renovation initiatives such as new flavors and packaging reinforce competitiveness among global competitors. Tactical retail collaborations continue to enable listings in supermarkets and on-trade outlets. C&C Group maintained over 140,000 metric tons of cider production to service European consumption demand and export channels.

-

In February 2024, C&C Group PLC opened a new 114,000 sq ft distribution depot at Orbital West in London, significantly strengthening its logistics network, improving delivery efficiency, enhancing service speed, and supporting higher-volume cider distribution across key U.K. retail and on-trade channels.

Carlsberg boosts cider presence, leveraging its strong position in the beverage market in Europe and Asia. Innovations in fruit blends, and light varieties keep experimenting consumers interested. Sustainability initiatives from the company increase brand equity and decrease environmental damage. Further penetration in retail underpinning robust growth in mass markets. Carlsberg’s cider operations generated approximately 120,000 metric tons in annual output, supporting rising consumption across its priority regions.

-

In March 2025, Carlsberg India expanded its partnership with WaterAid India to scale water-replenishment projects across 30 villages in Telangana, Maharashtra, and West Bengal, strengthening community water access, supporting sustainability commitments, and enhancing the company’s long-term environmental stewardship across high-impact regions.

Cider Market Key Players:

-

Diageo

-

Aston Manor

-

C&C Group PLC

-

Carlsberg Breweries A/S

-

Halewood Sales

-

Heineken N.V.

-

AB InBev

-

Thatchers Cider

-

KOPPARBERGS BRYGGERI AB

-

The Boston Beer Company, Inc.

-

Magners

-

Bulmers

-

Strongbow

-

Somersby

-

Woodchuck Cider

-

Crispin Cider

-

Ace Cider

-

Angry Orchard

-

Stella Artois Cider

-

Brothers Cider

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.34 Billion |

| Market Size by 2035 | USD 8.27 Billion |

| CAGR | CAGR of 4.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Flavor (Traditional, Flavored, Spiced, Honey, Herbal) • By Packaging (Bottles, Cans, Kegs, Tetra Packs, Multipacks) • By Type (Apple Cider, Pear Cider, Mixed Fruit Cider, Dry Cider, Sweet Cider) • By Distribution Channel (Supermarkets/Hypermarkets, Liquor Stores, Bars & Restaurants, Online Retail, Convenience Stores) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Diageo, Aston Manor, C&C Group PLC, Carlsberg Breweries A/S, Halewood Sales, Heineken N.V., AB InBev, Thatchers Cider, KOPPARBERGS BRYGGERI AB, The Boston Beer Company, Inc., Magners, Bulmers, Strongbow, Somersby, Woodchuck Cider, Crispin Cider, Ace Cider, Angry Orchard, Stella Artois Cider, Brothers Cider. |

Frequently Asked Questions

The market is valued at USD 5.34 Billion in 2025 and is projected to reach USD 8.27 Billion by 2035.

The Cider Market is expected to grow at a CAGR of 4.47% during 2026–2035.

Europe dominated the Cider Market in 2025.

Growth is driven by rising demand for flavored alcoholic beverages, premium craft offerings, and fruit-based drinks is driving strong global growth in the cider market.

The Apple Cider segment dominated during the projected period.

Get in Touch