Clad Pipe Market Report Scope & Overview:

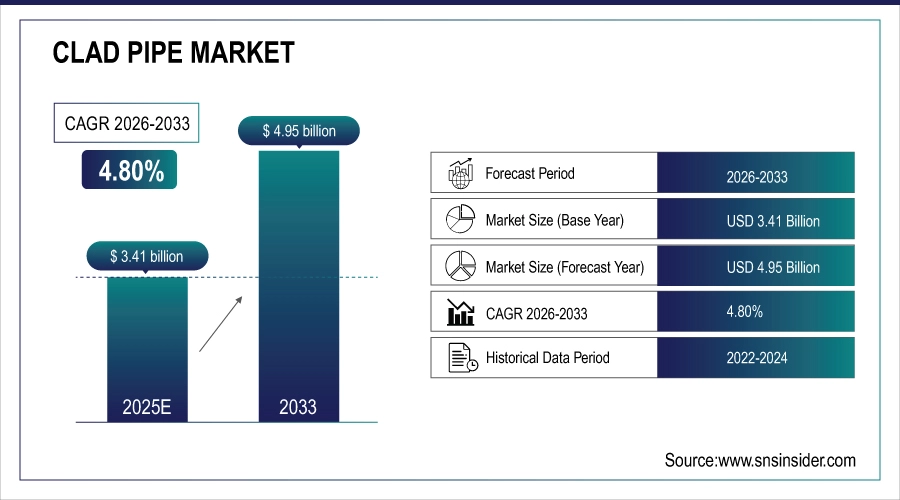

The Clad Pipe Market size was valued at USD 3.41 Billion in 2025E and is expected to reach USD 4.95 Billion by 2033, growing at a CAGR of 4.80% over the forecast period 2026–2033.

The market is witnessing increasing adoption driven by rising demand for corrosion-resistant pipeline infrastructure, extended operational lifespan requirements, and cost optimization across oil & gas, chemical, and subsea applications. By combining mechanical strength with superior corrosion protection, clad pipes enable long-term pipeline reliability while reducing maintenance frequency and failure risks.

Clad Pipe Market Size and Forecast

-

Market Size in 2025E: USD 3.41 Billion

-

Market Size by 2033: USD 4.95 Billion

-

CAGR: 4.80% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Clad Pipe Market - Request Free Sample Report

Key Clad Pipe Market Trends

-

Rising offshore and deepwater oil & gas projects are increasing demand for corrosion-resistant clad pipelines.

-

Growing focus on pipeline lifespan extension is driving adoption of metallurgically bonded pipes.

-

Advances in bonding and welding technologies are improving structural integrity and performance reliability.

-

Expanding chemical and petrochemical capacities are boosting clad pipe utilization.

-

Increasing preference for cost-effective alternatives to solid alloy pipes is accelerating mechanically lined pipe adoption.

-

Regulatory emphasis on pipeline safety and leakage prevention is strengthening market growth.

U.S. Clad Pipe Market Insights

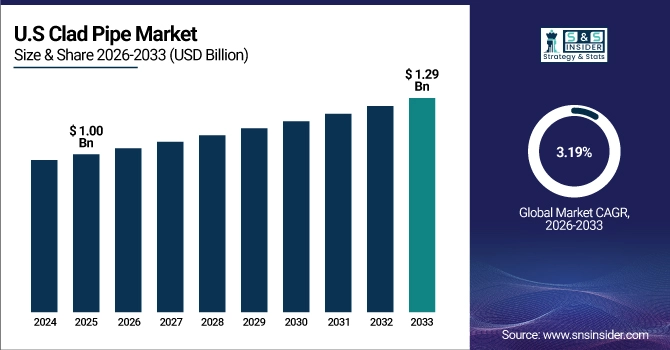

The U.S. Clad Pipe Market size was USD 1.00 billion in 2025E and is expected to reach USD 1.29 billion by 2033, growing at a CAGR of 3.19% over the forecast period 2026–2033. According to a study, increasing shale gas production and offshore investments have raised corrosion-related pipeline failures by nearly 18%, causing operators to adopt clad pipe solutions. This cause, rising operational risk, effects reduced maintenance downtime by up to 25% while extending pipeline service life beyond 30 years, supporting infrastructure reliability and long-term cost efficiency.

Clad Pipe Market Drivers

-

Growing Demand for Corrosion-Resistant Pipeline Infrastructure Across Energy and Chemical Industries Boosts Market Growth

The rising demand for corrosion-resistant pipeline infrastructure is a key driver of the Clad Pipe Market. Energy and chemical industries increasingly operate under extreme pressure, temperature, and corrosive fluid conditions. This cause, exposure to aggressive environments, effects widespread adoption of clad pipes that provide structural strength with superior corrosion resistance. Clad pipes significantly reduce leakage risks, environmental hazards, and unplanned shutdowns. Continuous improvements in metallurgical bonding techniques have enhanced bonding strength by over 20%, increasing operational safety. Aging pipeline replacement programs and new offshore developments further accelerate adoption, reinforcing sustained market expansion.

In March 2024, a U.S. offshore operator upgraded subsea pipelines using metallurgically bonded clad pipes, achieving a 27% reduction in corrosion-related maintenance incidents within one year.

Clad Pipe Market Restraints

-

High Initial Manufacturing and Installation Costs Limit Adoption Across Small-Scale and Budget-Sensitive Projects

Despite strong benefits, high upfront manufacturing and installation costs restrain the Clad Pipe Market. This cause, complex fabrication processes and specialized bonding technologies, effects limited adoption among small-scale operators. Clad pipes often cost 30% more than conventional carbon steel alternatives at initial deployment. Budget constraints force smaller operators to delay upgrades despite long-term savings. Additionally, limited availability of skilled installation professionals increases project costs, slowing penetration in emerging markets and low-capacity pipeline projects, thereby moderating overall growth potential.

In 2024, a Southeast Asian midstream operator postponed a clad pipe upgrade after project costs exceeded budget estimates by over 35%.

Clad Pipe Market Opportunities

-

Expansion of Deepwater and Subsea Energy Projects Creates High-Growth Opportunities for Advanced Clad Pipe Solutions

The expansion of deepwater and subsea energy projects presents a major growth opportunity for the Clad Pipe Market. This cause, increasing offshore exploration in extreme environments, effects heightened demand for high-performance corrosion-resistant pipelines. Clad pipes ensure durability under deepwater pressure and aggressive chemical exposure. Continuous R&D is improving bonding efficiency while reducing alloy material waste by nearly 15%. As offshore energy investments move deeper, clad pipes are becoming essential for ensuring safety, longevity, and cost efficiency across subsea pipeline systems.

In June 2025, a global energy company adopted advanced clad pipes for a deepwater project, extending projected pipeline lifespan by more than 20 years.

Clad Pipe Market Segmentation Analysis:

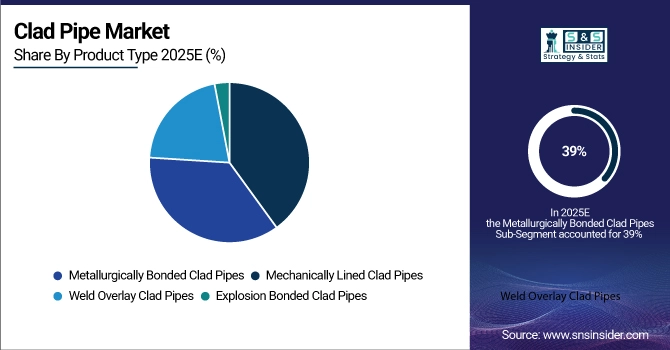

By Product Type, Metallurgically Bonded Clad Pipes Dominate Market with 39% Share in 2025E, Mechanically Lined Clad Pipes to Register Fastest Growth at 7.04% CAGR

Metallurgically bonded clad pipes held a dominant 39% share of the Clad Pipe Market in 2025E. Their widespread adoption is driven by superior metallurgical bonding strength, which provides enhanced resistance to corrosion, pressure, and fatigue in aggressive operating environments. These pipes are extensively used across oil & gas and chemical pipelines where long-term structural reliability and safety are critical. The growing need to reduce leakage risks, minimize downtime, and extend pipeline service life is further driving demand, supporting the segment’s dominance in critical infrastructure projects.

The mechanically lined clad pipes segment is expected to experience the fastest growth in the Clad Pipe Market during the forecast period, registering a CAGR of 7.04%. This growth is driven by lower material costs, reduced alloy usage, and faster production cycles compared to metallurgically bonded alternatives. Mechanically lined pipes offer a cost-efficient solution for mid-pressure and moderately corrosive applications, making them increasingly attractive for chemical processing and onshore transmission systems. Rising cost optimization efforts across pipeline projects are accelerating adoption, contributing significantly to overall market expansion.

By Diameter, 4–12 Inches Segment Dominates Market with 37% Share in 2025E, 12–24 Inches Segment to Record Fastest Growth at 6.89% CAGR

The 4–12 inches diameter segment accounted for approximately 37% of revenue in 2025E, dominating the Clad Pipe Market. This dominance is attributed to extensive usage in chemical processing units, refineries, and onshore pipeline networks where moderate flow capacity and ease of handling are essential. These pipes are widely preferred for retrofit and replacement projects due to simpler installation, reduced welding complexity, and lower transportation costs. The increasing focus on upgrading aging infrastructure continues to support sustained demand for this diameter range.

The 12–24 inches diameter segment is projected to grow at the fastest rate, with a CAGR of 6.89% over the forecast period. Growth is driven by rising large-scale oil & gas transportation projects requiring higher throughput capacity and long-distance transmission. Expanding cross-country and offshore pipeline developments are increasing demand for larger diameter clad pipes that can handle high volumes while maintaining corrosion resistance. These factors collectively reinforce the segment’s accelerated growth trajectory within the market.

By Application, Oil & Gas Segment Dominates Market with 39% Share in 2025E, Chemical & Petrochemical Segment to Register Fastest Growth at 7.00% CAGR

The oil & gas segment held a dominant 39% share of the Clad Pipe Market in 2025E. This dominance is driven by harsh operating conditions involving sour gas, high pressure, and corrosive fluids across upstream, midstream, and offshore environments. Clad pipes are increasingly deployed to enhance pipeline safety, reduce failure risks, and comply with stringent regulatory standards. Rising investments in offshore exploration and aging pipeline replacement programs further strengthen demand, maintaining the segment’s leadership position.

The chemical & petrochemical segment is expected to grow at the fastest pace, recording a CAGR of 7.00% during the forecast period. This growth is supported by expanding chemical production capacities and increased handling of highly corrosive media. Clad pipes offer superior chemical resistance while optimizing lifecycle costs, making them an ideal choice for processing and transfer systems. Continuous industrial expansion and modernization initiatives are accelerating adoption across this segment.

By End User, Onshore Segment Dominates Market with 42% Share in 2025E, Subsea Segment to Record Fastest Growth at 7.15% CAGR

The onshore segment accounted for approximately 42% of revenue in 2025E, dominating the Clad Pipe Market. This leadership is driven by extensive pipeline replacement activities, refinery upgrades, and expansion of onshore transmission networks. Onshore projects prioritize cost-effective corrosion protection and ease of installation, making clad pipes a preferred solution for long-term operational reliability. The high concentration of aging infrastructure continues to support strong and consistent demand across this segment.

The subsea segment is projected to register the fastest growth, with a CAGR of 7.15% over the forecast period. Growth is fueled by increasing deepwater and ultra-deepwater energy investments that demand pipelines with exceptional corrosion resistance and structural durability. Subsea environments impose extreme pressure and chemical exposure, driving reliance on advanced clad pipe solutions. These factors position the subsea segment as a key growth contributor within the Clad Pipe Market.

Clad Pipe Market Regional Insights:

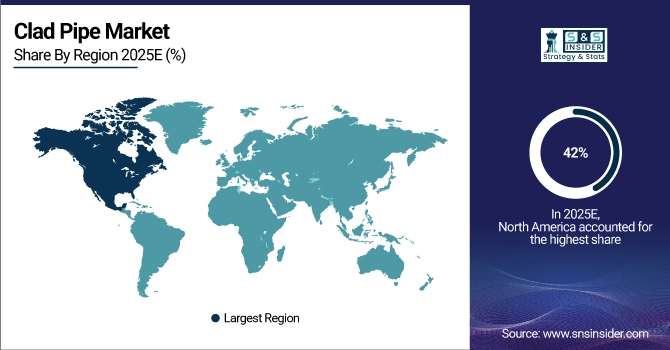

North America Dominates the Clad Pipe Market in 2025E

In 2025E, North America accounts for an estimated 42% share of the Clad Pipe Market, driven by strong offshore energy investments, aging pipeline infrastructure, and stringent safety regulations. The region’s oil & gas sector increasingly relies on corrosion-resistant pipeline solutions to mitigate leakage risks and extend asset lifespan. Rising refurbishment of legacy pipelines, combined with ongoing offshore upgrades, is amplifying demand for advanced clad pipe technologies. The emphasis on operational safety and long-term cost efficiency positions North America as a leading market for clad pipe adoption.

The United States dominates the North American Clad Pipe Market, supported by extensive shale gas development, offshore exploration activities, and strict pipeline integrity regulations. U.S. operators prioritize long-life pipeline solutions to manage corrosive environments and reduce maintenance downtime. Strong investments in energy infrastructure modernization and the presence of major pipeline manufacturers further reinforce the country’s leadership, making it the primary contributor to regional market revenues.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Is the Fastest-Growing Region in the Clad Pipe Market

Asia Pacific is projected to be the fastest-growing region, expanding at an estimated CAGR of 6.94% in 2026-2033, fueled by rapid industrialization and expanding energy infrastructure. Increasing demand for oil, gas, and chemical products is accelerating pipeline construction across emerging economies. This cause, rising industrial output, effects heightened demand for corrosion-resistant and cost-efficient pipeline solutions, positioning clad pipes as a preferred choice for long-distance transmission and processing applications.

China dominates the Asia Pacific Clad Pipe Market, driven by large-scale petrochemical expansion and extensive long-distance pipeline projects. The country’s aggressive infrastructure development and growing energy consumption require durable pipelines capable of handling corrosive media. Continuous investments in refinery capacity expansion and cross-regional energy transport strengthen China’s leadership, making it the key growth engine for the regional market.

Europe Clad Pipe Market Insights, 2025

Europe held a significant position in the Clad Pipe Market in 2025, supported by refinery modernization initiatives and stringent environmental regulations. The region emphasizes pipeline safety, emission reduction, and long-term infrastructure reliability, driving steady adoption of clad pipes. Increasing investments in upgrading aging refinery and chemical processing assets are reinforcing demand for corrosion-resistant piping systems across Europe.

Germany leads the European Clad Pipe Market, owing to its advanced industrial infrastructure and strong focus on pipeline retrofitting projects. The country’s well-established chemical and energy sectors prioritize compliance with strict safety and environmental standards, accelerating clad pipe adoption. Germany’s emphasis on high-quality engineering and infrastructure sustainability continues to support its dominant position within the region.

Middle East & Africa and Latin America Clad Pipe Market Insights, 2025

In 2025, the Middle East & Africa (MEA) region demonstrated steady growth in the Clad Pipe Market, driven by offshore oil developments and sour gas projects requiring high corrosion resistance. Increasing investments in upstream and offshore energy infrastructure are strengthening demand for long-life clad pipelines. Saudi Arabia dominates the region due to large-scale pipeline expansions and ongoing energy diversification initiatives.

Latin America also experienced consistent market growth, supported by expanding energy transport infrastructure and pipeline modernization programs. Brazil leads the Latin American market, driven by extensive oil & gas pipeline investments and offshore developments. Together, MEA and Latin America represent emerging growth regions, supported by rising energy demand and infrastructure expansion.

Clad Pipe Market key Players:

-

BUTTING Group

-

NobelClad

-

Proclad (FTV Proclad International)

-

EEW Group

-

Cladtek Holdings

-

Vallourec

-

JFE Steel Corporation

-

TMK Group

-

Sandvik Materials Technology

-

Precision Castparts Corporation

-

Zhejiang Jiuli Hi-Tech Metals

-

Gieminox (Tectubi Group)

-

Eisenbau Krämer

-

Canadoil Forge

-

Guangzhou Pearl River Petroleum Steel Pipe

-

IODS Pipe Clad

-

Inox Tech

-

Gautam Tube Corporation

Competitive Landscape of the Clad Pipe Market

Tenaris

Tenaris is a global leader in steel pipe and clad pipe manufacturing, serving oil & gas, energy, and industrial applications worldwide. The company specializes in advanced corrosion-resistant alloy and clad pipe solutions designed to withstand high pressure, extreme temperatures, and aggressive operating environments. Its product portfolio includes metallurgically bonded and mechanically lined clad pipes that enhance pipeline durability while reducing maintenance and operational risks. Tenaris plays a critical role in the Clad Pipe Market by enabling long-life pipeline infrastructure, supporting offshore, onshore, and subsea energy projects with high-performance solutions.

-

In April 2025, Tenaris expanded its corrosion-resistant alloy clad pipe portfolio to support offshore pipeline projects requiring enhanced resistance to sour gas and harsh marine conditions.

BUTTING Group

BUTTING Group is a Germany-based specialist in stainless steel, clad pipes, and pipeline systems for chemical, energy, and industrial applications. The company focuses on high-precision manufacturing of longitudinally welded clad pipes designed for high-pressure and corrosive environments. Its expertise in mechanically lined and metallurgically bonded pipes supports cost-efficient and reliable pipeline solutions across chemical processing and energy transport sectors. BUTTING’s role in the Clad Pipe Market is significant, as it delivers customized piping systems that optimize corrosion protection while maintaining mechanical strength.

-

In February 2025, BUTTING Group introduced enhanced mechanically lined clad pipes specifically developed for chemical plants handling corrosive media under elevated pressure conditions.

The Japan Steel Works, Ltd.

The Japan Steel Works, Ltd. (JSW) is a Japan-based industrial manufacturer providing high-performance metallurgically bonded clad pipes for extreme operating environments. The company leverages advanced forging, rolling, and bonding technologies to produce clad pipes with superior structural integrity and corrosion resistance. JSW plays an essential role in the Clad Pipe Market by supplying solutions for offshore oil & gas, petrochemical, and power generation applications where long-term reliability is critical. Its strong focus on precision engineering ensures compliance with stringent safety and performance standards.

-

In January 2025, JSW upgraded its clad pipe manufacturing capabilities to enhance bonding strength and production efficiency for high-demand energy infrastructure projects.

NobelClad

NobelClad is a global leader in explosion-bonded clad materials, providing advanced corrosion-resistant solutions for demanding pipeline and industrial applications. The company specializes in producing explosion-bonded clad plates and pipes that combine high-strength carbon steel with corrosion-resistant alloys. NobelClad’s role in the Clad Pipe Market is pivotal, as its products are widely used in subsea pipelines, chemical processing, and offshore energy projects requiring superior bonding integrity and durability under extreme conditions.

-

In May 2025, NobelClad introduced next-generation explosion-bonded clad plates designed for subsea pipeline applications, offering enhanced corrosion resistance and extended service life.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | US$ 3.41 Billion |

| Market Size by 2033 | US$ 4.95 Billion |

| CAGR | CAGR of 4.80 % From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Metallurgically Bonded Clad Pipes, Mechanically Lined Clad Pipes, Weld Overlay Clad Pipes, Explosion Bonded Clad Pipes) • By Diameter (4–12 inches, 12–24 inches, 24–48 inches, Above 48 inches) • By Application (Oil & Gas, Chemical & Petrochemical, Water Treatment & Desalination, Power Generation) • By End-Use (Onshore, Offshore, Subsea, Industrial Processing Facilities) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tenaris, BUTTING Group, The Japan Steel Works, Ltd., NobelClad, Proclad (FTV Proclad International), EEW Group, Cladtek Holdings, Vallourec, JFE Steel Corporation, TMK Group, Sandvik Materials Technology, Precision Castparts Corporation, Zhejiang Jiuli Hi-Tech Metals, Gieminox (Tectubi Group), Eisenbau Krämer, Canadoil Forge, Guangzhou Pearl River Petroleum Steel Pipe, IODS Pipe Clad, Inox Tech, Gautam Tube Corporation |

Frequently Asked Questions

North America dominated the Clad Pipe Market in 2025E.

The “Metallurgically Bonded Clad Pipes” segment dominated during the projected period.

The Clad Pipe Market is driven by rising demand for corrosion-resistant pipeline infrastructure, expanding oil & gas and chemical projects, and the need to extend pipeline lifespan while reducing maintenance and failure risks.

The market was valued at USD 3.41 Billion in 2025E and is projected to reach USD 4.95 Billion by 2033.

The Clad Pipe Market is expected to grow at a CAGR of 4.80% during 2026–2033.

Get in Touch