Comparator Drug Sourcing Market Report Scope & Overview:

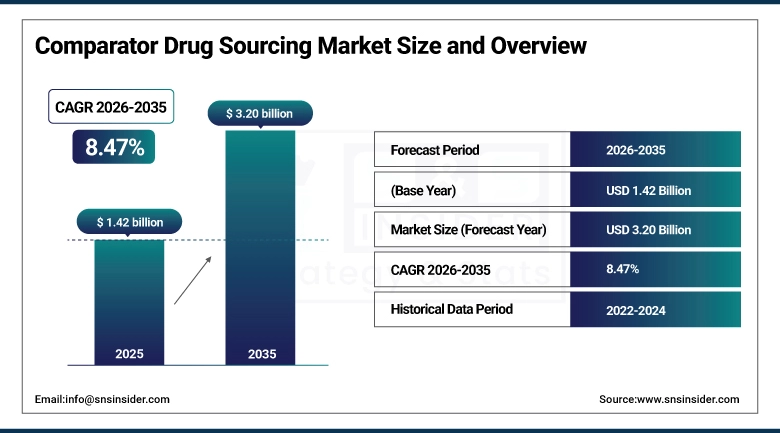

The Comparator Drug Sourcing Market was valued at USD 1.42 Billion in 2025 and is expected to reach USD 3.20 Billion by 2035, growing at a CAGR of 8.47% from 2026–2035.

The Comparator Drug Sourcing Market is exhibiting robust growth because of the increase in complexity and size of clinical trials being conducted worldwide, resulting in a higher need for effective and reliable comparator drug sourcing. The increasing number of pipeline drugs in the field of oncology, rare diseases, and biologics is contributing towards an increased procurement rate for drugs from various therapy areas. Outsourcing of clinical trial activities by Contract Research Organizations and biotech firms is making the sourcing process efficient and leading to market growth. Another factor favoring market growth is that of regulation of clinical trials.

According to the World Health Organization (WHO) International Clinical Trials Registry Platform (ICTRP), there are over 450,000 registered clinical trials globally across all phases and therapeutic areas, reflecting the vast scale of ongoing clinical research and the corresponding need for comparator drug procurement. Similarly, the U.S. National Institutes of Health lists over 500,000 registered studies, further highlighting the extensive global clinical trial activity that requires consistent access to reference and comparator drugs to ensure trial validity, regulatory compliance, and reliable outcome benchmarking.

Comparator Drug Sourcing Market Size and Forecast

-

Market Size in 2026E: USD 1.54 Billion

-

Market Size by 2035: USD 3.20 Billion

-

CAGR: 8.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

Comparator Drug Sourcing Market Trends

-

Rising clinical trial activities and increasing drug development pipelines are driving the comparator drug sourcing market.

-

Growing adoption of outsourcing strategies by pharmaceutical and biotechnology companies is boosting market growth.

-

Expansion of global clinical research, especially multi-country trials, is fueling demand for reliable comparator drug supply.

-

Increasing focus on cost efficiency, regulatory compliance, and supply chain transparency is shaping adoption trends.

-

Advancements in cold chain logistics, digital tracking systems, and sourcing platforms are enhancing supply reliability and traceability.

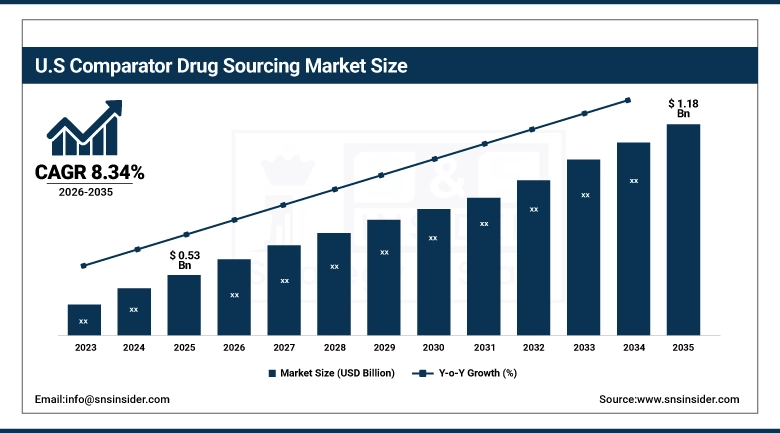

U.S. Comparator Drug Sourcing Market Outlook

The U.S. Comparator Drug Sourcing Market was valued at approximately USD 0.53 Billion in 2024 and is expected to reach approximately USD 1.18 Billion by 2032, growing at a CAGR of approximately 8.34%.

The United States comparator drug sourcing market is driven by its unparalleled concentration of pharmaceutical and biotechnology clinical trial activity, the most extensive CRO and clinical trial supply management service provider ecosystem globally, and the FDA's rigorous comparator product authenticity and chain-of-custody requirements whose compliance demands create consistent demand for specialist comparator sourcing expertise.

The accelerating adoption of immuno-oncology combination regimens whose clinical trials require simultaneous comparator sourcing of checkpoint inhibitors at large-scale doses per patient is creating the most commercially significant individual therapy area demand driver in the U.S. comparator drug sourcing market.

In April 2024, BAP Pharma opened its new U.S. headquarters in Somerset, New Jersey, in a 28,000 square foot state-of-the-art facility providing advanced clinical trial supply management, comparator drug sourcing, and pharmaceutical packaging services for clinical trial sponsors across North America.

Comparator Drug Sourcing Market Segment Analysis

-

By Sourcing Type, centralised sourcing segment dominated the comparator drug sourcing market in 2025 with 61.8% share; local/regional sourcing segment is the fastest growing segment.

-

By Molecule Type, small molecules segment dominated the market in 2025 with 52.4% share; cell & gene therapies segment is the fastest growing segment.

-

By Clinical Phase, phase iii segment dominated the market in 2025 with 38.6% share; phase i segment is the fastest growing segment.

-

By Therapy Area, oncology segment dominated the market in 2025 with 41.9% share; rare diseases segment is the fastest growing segment.

-

By End User, pharmaceutical & biopharmaceutical companies segment dominated the market in 2025 with 46.3% share; contract research organizations segment is the fastest growing segment.

By Sourcing Type, centralized sourcing dominates the comparator drug sourcing market, while local/regional sourcing is the fastest-growing segment

Centralised sourcing dominated the Comparator Drug Sourcing Market owing to its capability to make the process of sourcing smoother, maintain a standardized quality of drugs, and lower sourcing cost. Centralized sourcing becomes the preference for pharmaceutical companies to better manage the global network of suppliers and maintain compliance with stringent regulations. Centralized sourcing also helps in standardizing clinical trials and increases negotiating power with suppliers.

Local/Regional sourcing is the fastest-growing segment owing to the increasing preference for adaptable, flexible, and responsive supply chains. The local/regional sourcing method helps decrease dependency on global supply chains and helps save time in sourcing. Local/regional sourcing also ensures effective compliance with regional regulatory norms. Local/regional sourcing is preferred for clinical trials for its faster response.

By Molecule Type, small molecules dominate the comparator drug sourcing market, while cell and gene therapies are the fastest-growing segment

Small molecules dominated the Comparator Drug Sourcing Market due to the extensive use of these molecules in clinical trials, high efficiency, and robust production procedures. They are relatively easy to manufacture, distribute, and deliver, unlike biological drugs. Their widespread presence across all therapy areas coupled with their long track record in drug development makes them extremely desirable. Their reliable performance during clinical trials also adds credibility, solidifying their dominance in comparator sourcing activities.

Cell and gene therapies are the fastest-growing segment due to their rapid evolution in terms of precise medicines along with rising investments in novel therapies. Such therapies have been gaining popularity for complex and rare diseases where the unmet medical need has been identified. Rising pipeline development along with rising research funding is another driving factor behind the growing demand for such therapies.

By Clinical Phase, phase III dominates the comparator drug sourcing market, while phase I is the fastest-growing segment

Phase III dominated the Comparator Drug Sourcing Market because of the large volume requirement for testing in Phase III and because Phase III plays a significant role in the approval process. In Phase III, there is an immense demand for the availability of comparators since the pharmaceutical industry emphasizes stability, quality, and compliance in Phase III. Phase III is expensive and complicated, adding to the importance of efficient sourcing.

Phase I is the fastest-growing segment because of the increasing demand for early-stage drug development and growing investment in novel drugs. Increasing efforts of biotech companies in the research and development of drugs at initial stages contribute to the increasing demand for comparator drugs in early stages. Moreover, fast approvals and high R&D expenditures in the industry further drive the market for Phase I comparator drugs.

By Therapy Area, oncology dominates the comparator drug sourcing market, while rare diseases is the fastest-growing segment

Oncology dominated the Comparator Drug Sourcing Market owing to the massive global prevalence of cancer diseases and a wide array of oncology drug development programs being conducted. The trials in oncology necessitate a huge amount of comparator drugs, while innovations in immunotherapy and targeted drugs have increased demand. Moreover, high regulatory emphasis and heavy investments in research have made oncology the most dominant therapy area within the market.

Rare diseases are the fastest-growing segment owing to increased emphasis on orphan drug development and regulatory incentives. Better diagnostics are allowing for the early diagnosis of patients suffering from rare diseases. Pharmaceutical firms are increasing their investments in rare disease therapy areas. The need for specialized comparator drug sourcing and patient recruitment is contributing to fast growth in the segment.

By End User, pharmaceutical and biopharmaceutical companies dominate the market, while contract research organizations are the fastest-growing segment

Pharmaceutical and biopharmaceutical companies dominated the Comparator Drug Sourcing Market due to their significant clinical trial processes and drug development pipelines. These entities need comparator drugs throughout their research process and hence need reliable sources from where they can obtain comparator drugs efficiently. The availability of robust financial muscle and global procurement capabilities makes them dominant in the market. Increasing investments in innovative medicines will boost their dominant status in the market.

Contract Research Organizations are the fastest-growing segment owing to the growing practice of outsourcing clinical trials activities among pharmaceutical firms. The contract research organizations offer specialized expertise in carrying out clinical trials and sourcing and logistics of comparator drugs. They provide an efficient and cost-effective solution for the rising global demand for clinical research services. In addition, the increasing complexities associated with clinical trials have resulted in a shift towards adopting the services of CROs.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

India |

34.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Comparator Drug Sourcing Market Insights

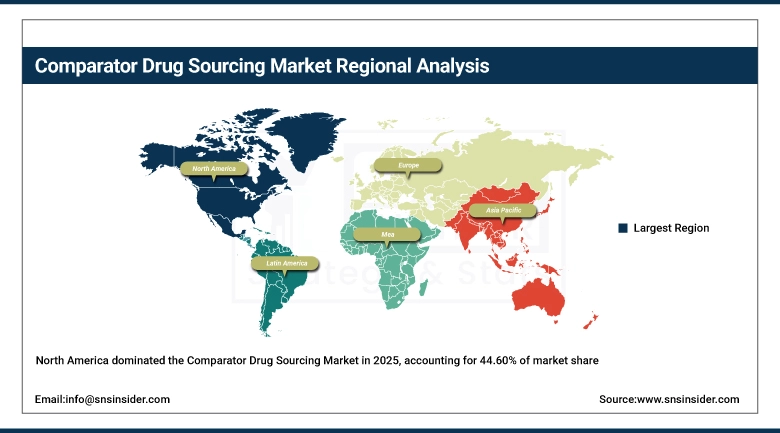

North America dominated the global Comparator Drug Sourcing Market in 2025, accounting for 44.60% of total market revenue, driven by the world's largest clinical trial activity concentration, its comprehensive pharmaceutical and CRO industry ecosystem, and the stringent regulatory framework whose comparator product authenticity and supply chain documentation requirements create consistent demand for specialist sourcing expertise.

The United States accounts for approximately 82.5% of North American revenues through the concentration of major pharmaceutical sponsors whose global trial programmes require sophisticated comparator sourcing management, the CRO industry's well-developed comparator procurement capabilities, and the FDA's requirement that comparators be sourced from FDA-regulated supply channels.

The FDA estimates that oncology drug development constitutes over 30% of all ongoing clinical trials, leading to a high demand for the use of comparison drugs in the study and treatment of various types of cancers. The National Institutes of Health (NIH), which operates under the auspices of the National Cancer Institute, indicates that there are roughly 2 million new cases of cancer diagnosed each year in the United States.

Europe Comparator Drug Sourcing Market Insights

Europe held a significant share of the global Comparator Drug Sourcing Market in 2025. Germany, the United Kingdom, France, Switzerland, and the Netherlands are the leading national markets whose pharmaceutical industry, CRO sector, and academic clinical trial infrastructure create consistent comparator sourcing demand. Germany accounts for approximately 28.5% of European revenues through the commercial concentration of ICON, Parexel, and other major CROs whose European headquarters sustain regional comparator procurement capability, and the large domestic pharmaceutical and biotechnology industry whose clinical trial programmes require systematic comparator sourcing support.

According to EURORDIS, rare diseases are estimated to impact about 30 million individuals in Europe, thus stimulating the growth of orphan drug products as well as posing challenges during clinical trials. All these elements combined have made it necessary to provide special sources for obtaining comparator drugs.

Asia Pacific Comparator Drug Sourcing Market Insights

Asia Pacific is the fastest-growing regional Comparator Drug Sourcing Market with a CAGR of approximately 9.03%, driven by the rising number of clinical trials in China, India, South Korea, Japan, and Australia, growing R&D investments by both domestic and international pharmaceutical companies, an expanding patient base for trial enrolment, and progressively favourable regulatory policies that have made Asian clinical trial sites more commercially attractive for international sponsors.

India accounts for approximately 34.8% of Asia Pacific revenues through its large and growing clinical trial sector whose combination of patient availability, English-language medical practice, cost-effective site operations, and ICMR-regulated trial infrastructure creates one of the world's most commercially dynamic emerging clinical trial markets whose comparator sourcing requirements grow with each new international trial protocol opened in the country.

MEA & Latin America Comparator Drug Sourcing Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class healthcare infrastructure, growing clinical trial sector at Dubai and Abu Dhabi teaching hospitals, and strategic importance as a regional hub for pharmaceutical trial supply logistics serving North Africa and Gulf market clinical sites. Saudi Arabia and South Africa contribute growing regional demand through their expanding clinical trial programmes and government health research investment.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its large and well-established clinical trial sector whose CONEP-regulated framework, large patient population, and Anvisa-compliant import procedures create a commercially significant regional comparator sourcing market. Mexico and Argentina contribute growing secondary demand through their expanding pharmaceutical industry and clinical research infrastructure.

Market Dynamics

Growth Drivers: Rising global clinical trial volumes with active control design requirements and increasing outsourcing of clinical supply chain to specialist service providers

The comparator drug sourcing market's growth is driven by the compounding effect of rising global clinical trial investment whose active control design requirements create non-discretionary comparator procurement and the progressive outsourcing of comparator sourcing from in-house pharmaceutical procurement teams to specialist clinical trial supply management organisations whose scale, regulatory expertise, and global sourcing network create efficiency and compliance advantages that internal procurement cannot replicate. Global pharmaceutical R&D investment exceeding USD 250 billion annually sustains clinical trial activity at record levels whose active control study designs, mandated by FDA and EMA for efficacy demonstration against current standard of care, create non-discretionary annual comparator drug procurement whose aggregate value grows proportionally with the expanding trial pipeline.

Restraints: Regulatory import restrictions creating country-specific comparator availability barriers and supply shortages of specific reference products disrupting trial timelines

Regulatory import requirements for comparator drugs vary significantly across countries whose national pharmaceutical registration, import permit, and authorised source requirements may prohibit or delay the import of comparator products from the most commercially accessible supply source for the trial sponsor's centralized procurement infrastructure. Each country-specific import restriction that prevents the use of a centrally procured comparator batch at local trial sites requires either local sourcing of an equivalent comparator from an authorised local market channel or regulatory approval of an import exception pathway whose administrative timeline creates potential trial supply delay.

Opportunities: Decentralised clinical trial comparator home delivery and biosimilar comparator cost reduction creating significant market expansion opportunities

Decentralised and hybrid clinical trial designs whose patient-centric protocols deliver investigational and comparator treatments directly to patient homes are creating entirely new comparator drug supply chain requirements whose last-mile delivery to patient residences, home nursing administration support, and patient-level chain-of-custody documentation require clinical trial supply management capabilities that traditional site-based comparator distribution networks have not been designed to provide. Each decentralised trial protocol that successfully delivers comparator drugs to patient homes expands the geographic accessible patient population for trial enrolment while simultaneously creating new comparator supply chain service requirements whose profitable execution requires investment in patient-level cold-chain packaging, GPS-tracked courier networks, and remote patient interaction platforms.

Recent Developments:

-

2025: Biologic-based clinical trials increased by 18% particularly in oncology and immunology, driving unprecedented demand for cold-chain-enabled comparator drug sourcing solutions and accelerating investment in temperature-controlled global supply chain infrastructure by specialist clinical trial supply organisations.

-

2024: BAP Pharma opened its new U.S. headquarters in Somerset, New Jersey, in a 28,000 square foot facility providing advanced clinical trial supply management, comparator drug sourcing, and pharmaceutical packaging services, expanding capacity to serve growing North American clinical trial supply outsourcing demand.

-

2024: Cencora (formerly AmerisourceBergen) expanded its clinical trial supply services comparator sourcing capability through investment in its World Courier specialty logistics network, enhancing cold-chain comparator distribution capacity across 150 countries for biologic and specialty pharmaceutical clinical trial programmes.

Comparator Drug Sourcing Market Key Players

-

Thermo Fisher Scientific Inc.

-

Clinigen Group plc

-

Inceptua Group

-

Uniphar Clinical

-

Catalent, Inc.

-

Clinical Services International (CSI)

-

BAP Pharma Limited

-

Oximio

-

Bionical Emas

-

Alcura

-

Myonex

-

Cencora, Inc.

-

Sharp Services, LLC

-

ADAllen Pharma

-

RxSolutions division

-

PCI Pharma Services

-

Quotient Sciences

-

Fisher Clinical Services

-

Sourcing4U

-

Global Clinical Supplies Group (GCSG)

Comparator Drug Sourcing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.42 Billion |

| Market Size by 2035 | USD 3.20 Billion |

| CAGR | CAGR of 8.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sourcing Type (Centralised Sourcing, Local/Regional Sourcing) • By Molecule Type (Small Molecules, Biologics & Biosimilars, Cell & Gene Therapies) • By Clinical Phase (Phase I, Phase II, Phase III, Phase IV) • By Therapy Area (Oncology, Neurology, Cardiovascular, Infectious Disease, Immunology, Rare Diseases, Others) • By End User (Pharmaceutical & Biopharmaceutical Companies, Contract Research Organizations, Academic & Research Institutions, Biotechnology Companies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Clinigen Group plc, Inceptua Group, Uniphar Clinical, Catalent, Inc., Clinical Services International (CSI), BAP Pharma Limited, Oximio, Bionical Emas, Alcura, Myonex, Cencora, Inc., Sharp Services, LLC, ADAllen Pharma, RxSolutions division, PCI Pharma Services, Quotient Sciences, Fisher Clinical Services, Sourcing4U, Global Clinical Supplies Group (GCSG). |

Frequently Asked Questions

The Comparator Drug Sourcing Market is expected to grow at a CAGR of 8.47% from 2026 to 2035.

The Comparator Drug Sourcing Market was valued at USD 1.42 Billion in 2025.

Rising clinical trials, biologic growth, outsourcing, decentralised trial models, and Asia Pacific expansion are driving strong demand for comparator drug sourcing globally.

The Small Molecules segment dominated the Comparator Drug Sourcing Market with the largest share in 2025.

North America dominated the Comparator Drug Sourcing Market with 44.60% of global revenue in 2025.

Get in Touch