Cyber Warfare Market Report Scope & Overview:

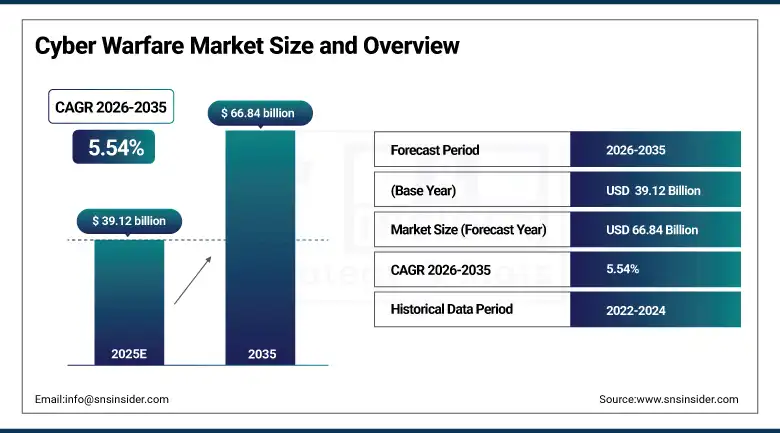

The Cyber Warfare Market size was valued at USD 39.12 Billion in 2025 and is projected to reach USD 66.84 Billion by 2035, growing at a CAGR of 5.54% during 2026–2035.

The cyber warfare landscape is growing, driven by escalating geopolitical tensions, a rise in state-sponsored cyberattacks, and the increasing vulnerabilities of critical infrastructures such as energy grids, defense networks, and financial systems. Worldwide, governments are investing heavily in advanced cybersecurity, AI-driven threat detection, and offensive cyber capabilities. The expansion of digital spaces, cloud computing, and the Internet of Things has widened the attack surface, thereby amplifying the demand for robust cyber defense strategies. Furthermore, stricter data protection laws and the imperative of national security are further propelling the market's growth.

Cyber Warfare Market Size and Forecast:

-

Market Size in 2025: USD 39.12 Billion

-

Market Size by 2035: USD 66.84 Billion

-

CAGR: 5.54% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Cyber Warfare Market - Request Free Sample Report

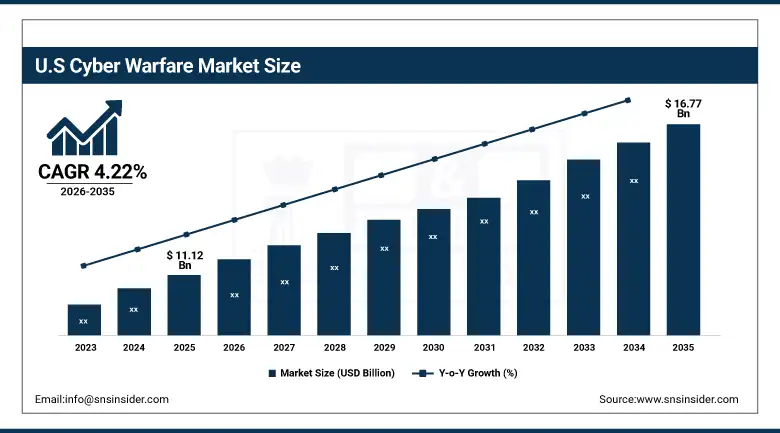

The U.S. Cyber Warfare Market was valued at USD 11.12 Billion in 2025 and is projected to reach USD 16.77 Billion by 2035, growing at a CAGR of 4.22% during 2026–2035. The United States operates the world’s largest institutionalized military cyber force, with U.S. Cyber Command’s Cyber Mission Force comprising over 6,000 personnel organized into national mission teams, combat mission teams, and cyber protection teams. Classified programs represent a significant undisclosed share of total U.S. cyber warfare investment, and unclassified budget growth has been consistent across recent congressional cycles sustained by bipartisan recognition of cyber as a core military competency.

Cyber Warfare Market Highlights:

-

State-sponsored cyber-attack frequency and sophistication are rising across every major geopolitical contest, with Russia, China, Iran, and North Korea all maintaining active cyber operations programs that span espionage, destructive attacks, financial crime, and information operations against adversary government and private sector targets.

-

Software solutions are the fastest-growing component, driven by demand for AI-augmented threat detection, automated incident response platforms, and offensive cyber tools that can be deployed and updated faster than hardware-dependent systems allow.

-

Defensive cyber warfare accounts for more than 80% of the market by value, reflecting the structural reality that more organizations have an immediate defensive requirement than participate in offensive cyber operations, which are restricted to national intelligence and military establishments.

-

Critical infrastructure protection is the fastest-growing application, driven by documented attacks on energy grids, water systems, and transportation networks in multiple countries and the regulatory frameworks that these events have prompted governments to enact.

-

Asia Pacific is the fastest-growing regional market, reflecting the scale of Chinese and North Korean state-sponsored cyber operations, the reciprocal defensive investment this prompt in Japan, South Korea, Australia, and India, and the growth of indigenous cyber capability in multiple regional middle powers.

Cyber Warfare Market Drivers:

-

Escalating State-Sponsored Cyber Operations, Critical Infrastructure Vulnerability, and Military Cyber Force Expansion Are Sustaining Defense Budget Allocation to Cyber Warfare Capability Across All Major Military Powers

The case for cyber warfare investment does not depend on projections of future threat escalation it is grounded in the operational record of the past two years. The 2024 Salt Typhoon intrusion into U.S. telecommunications networks compromised senior government communications and demonstrated that adversaries have persistent access to infrastructure civilian cybersecurity investment had not secured. The Volt Typhoon campaign, disclosed in 2024, focused on pre-positioning within U.S. power grids, water systems, and transportation networks suggesting preparation for disruptive attacks timed to a future crisis. North Korean operators generated hundreds of millions of dollars through cryptocurrency exchange attacks in 2024, funding weapons programs that conventional sanctions have failed to contain. Each of these incidents generated budget supplementals and accelerated procurement programs that translate directly into cyber warfare market revenue.

In March 2025, the U.S. Cyber Command announced the expansion of its Hunt Forward Operations program, deploying teams to partner nations at their invitation to hunt for adversary malware pre-positioned on critical infrastructure networks. The program has operated in more than thirty countries since its establishment and generates real-time threat intelligence that feeds back into U.S. defensive cyber program development.

Cyber Warfare Market Restraints:

-

Talent Shortages, Attribution Complexity, and the Legal Ambiguity Surrounding Offensive Cyber Operations Are Creating Friction That Limits the Speed and Scale of Military Cyber Capability Expansion

Cyber warfare capability is more human capital-intensive than almost any other military domain. Building a cyber operator capable of conducting advanced persistent threat-level operations takes years of training and produces people who are highly compensable in the civilian security industry. Military pay scales and service commitment requirements make retention a consistent challenge, and the compensation gap has widened as private sector cybersecurity salaries have risen. The attribution problem creates restraint on the offensive side: a significant cyber-attack almost always generates immediate questions about responsibility, and the inability to demonstrate attribution publicly complicates deterrence communication and domestic political authorization for response. Most nations lack clear legal frameworks governing what constitutes an armed attack in cyberspace, creating persistent uncertainty about the legal basis for offensive responses to intrusions that cause economic damage without physical harm.

Cyber Warfare Market Opportunities:

-

AI-Augmented Cyber Operations, Zero Trust Architecture Adoption, and Allied Nation Cyber Capability Investment Create Growth Pathways That Are Independent of Any Single National Defense Budget

AI-driven endpoint detection and response tools are identifying attack patterns faster than human analysts can review alerts, behavioral analytics platforms are detecting compromised credentials before attackers can pivot to high-value targets, and large language models are being applied to malware analysis and vulnerability research in ways that compress time from discovery to patch. U.S. Cyber Command acknowledged in 2024 that AI tools are integrated into operational defensive cyber workflows, the first official confirmation that machine learning has crossed from research into deployed military cyber operations. Zero trust architecture mandates requiring no network connection be trusted by default are generating sustained procurement demand across government and private sector organizations, driven by federal policy requiring U.S. civilian agencies to reach defined zero trust maturity levels by fiscal year 2026. Allied nation cyber capability investment from Estonia, Finland, South Korea, and Australia also generates recurring market demand for tools, training, and advisory services.

In January 2025, the European Union activated its new Cyber Solidarity Act, creating a pan-European cyber reserve force of pre-contracted private cybersecurity providers who can be deployed to member states experiencing significant cyber incidents

Cyber Warfare Market Segment Highlights:

-

By Component: Dominant Software (41.37% in 2025, CAGR 6.41%); Fastest-Growing Software (CAGR 6.41%)

-

By Warfare Type: Dominant Defensive Cyber Warfare (81.63% in 2025, CAGR 5.23%); Fastest-Growing Offensive Cyber Warfare (18.37% in 2025, CAGR 6.82%)

-

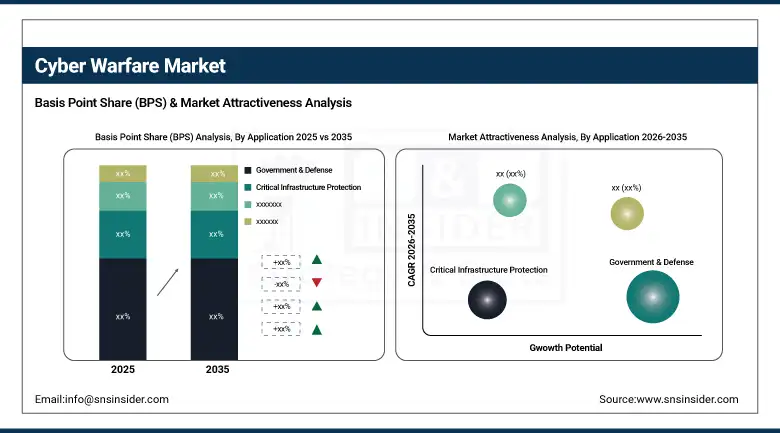

By Application: Dominant Government & Defense (36.72% in 2025, CAGR 4.74%); Fastest-Growing Critical Infrastructure Protection (24.18% in 2025, CAGR 6.27%)

-

By End-User: Dominant Defense & Military Organizations (34.62% in 2025, CAGR 5.93%); Fastest-Growing BFSI & Corporate Enterprises (21.47% in 2025, CAGR 6.25%)

Cyber Warfare Market Segment Analysis:

Software Leads and Drives Fastest Growth Among Components

Software’s simultaneous leadership on both share and growth rate reflects a structural shift in how cyber warfare capability is built: the most operationally consequential capabilities intrusion tools, threat detection platforms, AI-driven analytics, and command-and-control infrastructure are software-defined and software-updated, making hardware a declining proportion of total investment even as it grows in absolute terms. Services (30.17%, USD 11.80B, CAGR 5.44%) holds stable as the persistent technical workforce and advisory demand that organizations cannot build internally. Hardware (28.46%, USD 11.13B, CAGR 4.25%) grows slowest as software-defined capability reduces per-function hardware dependence.

Defensive Cyber Warfare Leads; Offensive Drives Faster Growth

Defensive dominance reflects the structural asymmetry of the market: every networked organization has a defensive requirement, while offensive operations are authorized only for a narrow set of national military and intelligence actors. OCW is growing faster because nations conducting offensive operations are accelerating investment, driven by demonstrated utility in intelligence collection, deterrence, and battlefield support.

Government & Defense Leads Applications; Critical Infrastructure Protection Drives Fastest Growth

Government and defense lead as the primary institutional home of both offensive and defensive investment. Critical infrastructure is growing fastest because documented attacks on power infrastructure, telecommunications, and hospital networks in 2024 created both regulatory mandates and genuine risk awareness driving operational technology security and incident response investment.

Defense & Military Organizations Lead End-Users; BFSI & Corporate Enterprises Drive Fastest Growth

. Military end-users lead as cyber has become an integral warfighting domain with consistent budget growth. BFSI and corporate enterprises are growing fastest because breaches at major financial data aggregators and payment processors throughout 2024 made board-level cybersecurity investment a governance expectation rather than a discretionary IT spending decision.

Cyber Warfare Market Regional Analysis:

North America Cyber Warfare Market Insights

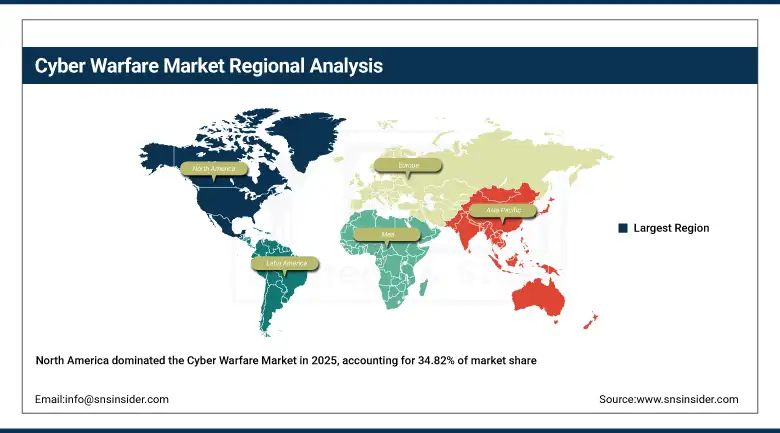

North America dominated the Cyber Warfare Market in 2025, accounting for 34.82% of market share at USD 13.62 Billion, projected to reach USD 21.15 Billion by 2035 at a CAGR of 4.53%. The region’s leadership rests on the scale of the U.S. Cyber Command budget, the classified NSA cybersecurity mission investment, and the depth of the U.S. defense industrial base producing cyber warfare tools and platforms. The 2025 CISA National Cyber Incident Response Plan revision and the Department of Defense’s Cyber Strategy implementation are both generating sustained procurement demand across offensive operations, defensive operations, and civilian critical infrastructure protection programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Cyber Warfare Market Insights

The United States dominates North American demand through U.S. Cyber Command’s Cyber Mission Force, the NSA’s dual intelligence and cybersecurity mandate, and a defense industrial ecosystem that includes every major cyber warfare technology developer, sustaining the world’s largest military cyber investment program.

Europe Cyber Warfare Market Insights

Europe held a 26.31% share in 2025 at USD 10.29 Billion, projected to reach USD 16.66 Billion by 2035 at a CAGR of 4.97%. European cyber warfare investment has been structurally elevated since Russia’s full-scale invasion of Ukraine in 2022, with the documented use of cyber-attacks as part of that conflict including wiper malware, attacks on satellite communications, and persistent intrusions into European government networks in 2024 maintaining political support for sustained cyber defense investment across NATO member defense budgets. The EU Cyber Solidarity Act and the NIS2 Directive implementation are both generating procurement requirements across member state governments and regulated private sector operators.

Germany Cyber Warfare Market Insights

Germany leads European cyber warfare investment through the Bundeswehr’s Cyber and Information Domain Service, the Federal Office for Information Security’s expanded budget, and the recognition that Germany’s industrial critical infrastructure is a documented target of state-sponsored intrusion campaigns with links to both Russian and Chinese operators.

Asia Pacific Cyber Warfare Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 7.26%, rising from USD 8.89 Billion in 2025 to USD 17.90 Billion by 2035. The region hosts the world’s most active cyber threat actors China’s extensive state-sponsored APT programs, North Korea’s financially motivated cyber operations, and various criminal and state-linked groups across Southeast Asia while simultaneously driving reciprocal defensive investment from Japan, South Korea, Australia, India, and Taiwan. Each of these countries has expanded its military and civilian cyber security organizations since 2024, generating both domestic and procurement market demand for cyber warfare tools and services.

China Cyber Warfare Market Insights

China leads Asia Pacific cyber warfare investment through the PLA Strategic Support Force’s network warfare units, the Ministry of State Security’s extensive APT programs, and the domestic cybersecurity industry that serves both military requirements and the civilian security market, making China simultaneously the market’s most active threat actor and one of its largest national markets by investment.

Latin America and Middle East & Africa Cyber Warfare Market Insights

Latin America held an 8.07% share in 2025 at USD 3.16 Billion, growing at a CAGR of 5.91% to USD 5.59 Billion by 2035. Brazil leads through its expanding military cyber command and the cyber security investment driven by documented attacks on Brazilian government networks and financial institutions. Mexico and Colombia are secondary markets growing with digital infrastructure expansion. Middle East & Africa held an 8.06% share in 2025 at USD 3.15 Billion, growing at a CAGR of 5.85% to USD 5.55 Billion by 2035. Israel leads the MEA market through the most sophisticated cyber warfare capability in the region, operated through Unit 8200 and the National Cyber Directorate, alongside a thriving commercial cyber industry that exports technology globally. Israel leads MEA cyber warfare investment through Unit 8200’s intelligence and offensive cyber operations, the National Cyber Directorate’s critical infrastructure protection mandate, and a commercial cybersecurity industry that produces globally deployed offensive and defensive tools, making Israel a cyber power disproportionate to its size.

Cyber Warfare Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin's cyber warfare operations are conducted via its Cyber, Intelligence and Information Solutions division, which furnishes offensive and defensive cyber capabilities, threat intelligence platforms, and network protection systems to governmental and defense clients in the United States and allied nations.

In April 2025, Lockheed Martin secured a contract from the U.S. Space Force to construct a cyber range environment. This environment is intended for testing the resilience of space systems, allowing for the simulation of attack scenarios targeting satellite ground control networks and onboard software. The goal is to pinpoint vulnerabilities prior to their operational deployment.

Northrop Grumman Corporation

Northrop Grumman’s cyber warfare capability is concentrated in its Mission Systems sector, producing signals intelligence systems, electronic warfare platforms, and cyber tools spanning both offensive collection and defensive network protection. Its legacy in cryptographic systems and signals intelligence hardware gives it a technical foundation predating the modern cyber security industry, and established relationships with NSA, GCHQ, and allied signals intelligence agencies provide access to classified program requirements that smaller firms lack the clearance relationships to bid on.

In February 2025, Northrop Grumman announced expansion of its cyber operations center in Annapolis Junction, Maryland, adding secure development and operations capability for classified cyber programs, its second Maryland cyber facility investment in twelve months, reflecting sustained classified program growth.

Cyber Warfare Market Key Players:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Raytheon Technologies Corporation

-

The Boeing Company

-

Airbus Defence and Space

-

Thales Group

-

BAE Systems plc

-

General Dynamics Corporation

-

L3Harris Technologies Inc.

-

Booz Allen Hamilton

-

Leidos Holdings, Inc.

-

SAIC

-

Palantir Technologies Inc.

-

CrowdStrike Holdings

-

Palo Alto Networks

-

ManTech International

-

CACI International

-

Leonardo S.p.A.

-

Saab AB

-

Kratos Defense & Security Solutions

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.12 Billion |

| Market Size by 2035 | USD 66.84 Billion |

| CAGR | CAGR of 5.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, and Services) • By Warfare Type (Offensive Cyber Warfare (OCW) and Defensive Cyber Warfare (DCW)) • By Application (Government & Defense, Critical Infrastructure Protection, Corporate Security, and Cybercrime Prevention) • By End-User (Government Agencies, Defense & Military Organizations, BFSI & Corporate Enterprises, and Healthcare & Critical Infrastructure Operators) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, The Boeing Company, Airbus Defence and Space, Thales Group, BAE Systems plc, General Dynamics Corporation, L3Harris Technologies Inc., Almaz-Antey Corporation, Rostec State Corporation, Israel Aerospace Industries, China Aerospace Science and Technology Corporation, China Aerospace Science and Industry Corporation, Mitsubishi Heavy Industries Ltd., Saab AB, Leonardo S.p.A., Rafael Advanced Defense Systems Ltd., MBDA, Kratos Defense & Security Solutions |

Frequently Asked Questions

North America dominated the Cyber Warfare in 2025

Software dominated the Cyber Warfare in 2025.

Rising geopolitical tensions, increasing state-sponsored cyberattacks, and growing investments in advanced cybersecurity and national defense capabilities are the key drivers of the Cyber Warfare Market.

The Cyber Warfare size was USD 39.12 Billion in 2025 and is expected to reach USD 66.84 Billion by 2035.

The Cyber Warfare is expected to grow at a CAGR of 5.54% from 2026–2035.

Get in Touch