Data Sovereignty & Localization Market Report Scope & Overview:

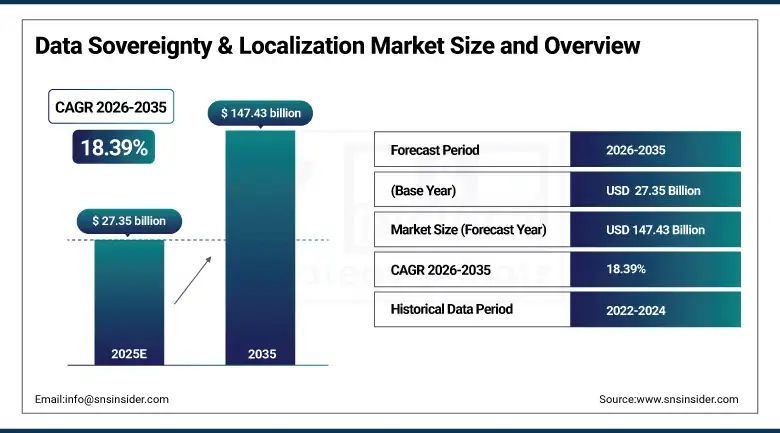

The Data Sovereignty & Localization Market size was valued at USD 27.35 Billion in 2025 and is projected to reach USD 147.43 Billion by 2035, growing at a CAGR of 18.39% during 2026–2035.

The Data Sovereignty & Localization Market is growing due to rising data protection regulations, increasing concerns over data privacy and security, and stricter government mandates on data residency. Organizations are investing in compliance solutions to meet laws such as GDPR-like frameworks. Rapid cloud adoption, cross-border data restrictions, and geopolitical tensions are further driving demand for localized data infrastructure, governance tools, and secure data management systems across highly regulated industries like BFSI, healthcare, and government sectors.

Data Sovereignty & Localization Market Size and Forecast:

-

Market Size in 2025: USD 27.35 Billion

-

Market Size by 2035: USD 147.43 Billion

-

CAGR: 18.39% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Data Sovereignty & Localization Market - Request Free Sample Report

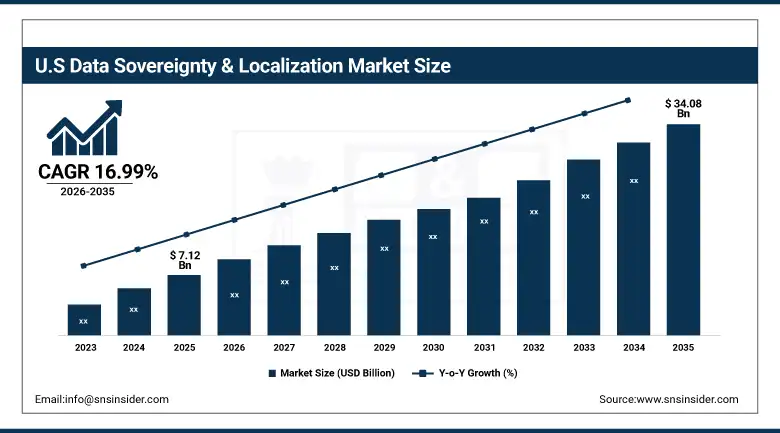

The U.S. Data Sovereignty & Localization Market was valued at USD 7.12 Billion in 2025 and is projected to reach USD 34.08 Billion by 2035, growing at a CAGR of 16.99% during 2026–2035. The U.S. market is driven by U.S. companies managing data residency requirements imposed by GDPR, the EU-U.S. Data Privacy Framework, and the localization requirements of India, Saudi Arabia, and Indonesia, alongside U.S. federal procurement rules restricting government cloud use to approved providers.

Data Sovereignty & Localization Market Highlights:

-

The proliferation of national data localization laws with countries including Saudi Arabia, Indonesia, Vietnam, and Turkey all enacting or strengthening data residency requirements in 2024 and 2025 is continuously expanding the compliance surface that enterprises must address, sustaining market growth independent of any single regulatory event.

-

Software is both the dominant and fastest-growing component, as data governance and compliance platforms are the first-line investment organizations make when confronting new localization requirements, ahead of hardware infrastructure buildout and consulting engagement.

-

Cloud deployment is the fastest-growing mode, driven by hyperscaler investments in local cloud regions specifically designed to satisfy data residency requirements, including AWS, Azure, and Google Cloud sovereign cloud offerings launched or expanded in multiple countries in 2024 and 2025.

-

Healthcare is the fastest-growing end-user industry, driven by the intersection of patient data privacy requirements, cross-border health data exchange restrictions, and the rapid digitalization of health records creating new data residency obligations for providers and health technology companies.

-

Asia Pacific is the fastest-growing regional market, driven by China’s Personal Information Protection Law enforcement acceleration, India’s data protection rules finalization, and the enactment of localization requirements across Southeast Asian markets including Indonesia and Vietnam.

Data Sovereignty & Localization Market Drivers:

-

Expanding National Data Localization Legislation, Geopolitical Tension Over Data Access, and Hyperscaler Sovereign Cloud Buildouts Are Simultaneously Creating Compliance Demand and Enabling Market Infrastructure

The legislative pipeline for data localization requirements has not slowed since GDPR demonstrated in 2018 that a comprehensive national data framework could be enforced against multinationals at meaningful scale. Brazil’s LGPD, China’s PIPL and Data Security Law, India’s DPDP Act, Saudi Arabia’s PDPL, and Indonesia’s PDP Law have all passed and begun generating compliance investment. Each new law creates residency obligations that organizations must satisfy through data routing controls, local infrastructure investment, and compliance management processes. Geopolitical tension has intensified this: the Schrems II ruling in 2020 and the ongoing legal vulnerability of the EU-U.S. Data Privacy Framework keep the data transfer compliance question permanently active for every European organization with U.S. cloud infrastructure. The hyperscalers have responded by making sovereign cloud a major product investment: Microsoft’s EU Data Boundary, Google Cloud’s Sovereign Cloud programs, and AWS’s European Sovereign Cloud all represent multi-billion dollar commitments to data residency guarantees, each generating associated software, consulting, and managed service market revenue.

Data Sovereignty & Localization Market Restraints:

-

Conflicting Jurisdictional Requirements, Implementation Complexity in Multi-Cloud Environments, and the Cost of Localized Infrastructure Are Limiting Adoption Speed, Particularly for Mid-Market Organizations

Data localization compliance is not technically simple even when the legal requirement is clear. An organization managing personal data subject to five national frameworks must maintain an architecture that correctly classifies each data element by its applicable requirement, routes it to the right storage location, and documents the processing basis for each regulator’s audit. The requirements conflict: some frameworks require data to stay within national borders, others allow transfer with adequate protection measures, others create explicit prohibitions on specific transfer destinations, and definitions of “personal data” and “sensitive data” vary enough that a single classification schema does not map cleanly across all of them. For mid-market organizations, the cost of building and maintaining localized data architecture can be prohibitive. Cloud-based compliance platforms have reduced the cost barrier, but organizations in financial services, healthcare, and telecommunications still face implementation timelines and consulting costs that create genuine adoption friction.

Data Sovereignty & Localization Market Opportunities:

-

Sovereign AI Infrastructure, Automated Compliance Management, and Government Cloud Modernization Create Growth Pathways That Are Just Beginning to Scale

The intersection of data sovereignty and AI has produced a new subcategory: sovereign AI infrastructure compute, storage, and model deployment systems keeping AI training data and model outputs within a defined national jurisdiction. France, Germany, the UAE, and Saudi Arabia all announced sovereign AI initiatives in 2024 and 2025 that include explicit data residency components, recognizing that AI systems trained on national data are strategic assets that should not be subject to foreign legal jurisdiction. Each sovereign AI program generates data localization technology procurement additive to existing compliance-driven demand. Automated compliance management platforms that track regulatory changes across jurisdictions, map data flows to applicable requirements, and generate audit documentation without manual intervention are addressing the staff-intensive operational problem that grows in proportion to the number of jurisdictions an organization operates in. Government cloud modernization programs across the EU, GCC states, and the ASEAN region are generating large-scale procurement for compliant cloud infrastructure, creating multi-year contract opportunities for both hyperscaler sovereign cloud offerings and domestic infrastructure providers.

Data Sovereignty & Localization Market Segment Highlights:

-

By Component: Dominant Software (48.60% in 2025, CAGR 19.15%); Fastest-Growing Software (CAGR 19.15%)

-

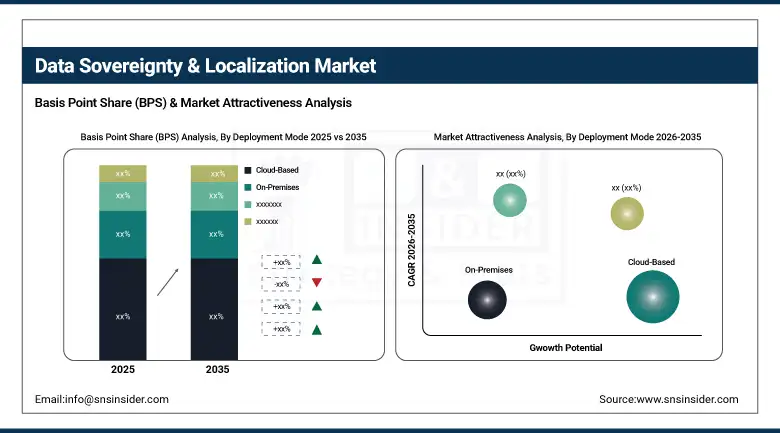

By Deployment Mode: Dominant Cloud-Based (38.60% in 2025, CAGR 21.42%); Fastest-Growing Cloud-Based (CAGR 21.42%)

-

By Application: Dominant Data Governance & Compliance Management (31.44% in 2025, CAGR 17.48%); Fastest-Growing Data Localization & Residency Control (26.81% in 2025, CAGR 19.22%)

-

By End-User Industry: Dominant BFSI (27.86% in 2025, CAGR 17.75%); Fastest-Growing IT & Telecommunications (18.90% in 2025, CAGR 19.41%)

Data Sovereignty & Localization Market Segment Analysis:

Software Leads and Drives Fastest Component Growth

Software leads and grows fastest simultaneously because data governance and compliance platform investment is the first response organizations make when confronting new localization requirements. Before hardware is procured or consulting engagements scoped, organizations need to know what data they hold, where it resides, and which regulatory frameworks apply all software-driven. Services grow slowest as cloud infrastructure increasingly substitutes for on-premises investment in meeting residency requirements.

Cloud-Based Deployment Leads and Drives Fastest Growth

Cloud leads and grows fastest because hyperscaler sovereign cloud programs designed with region-locked infrastructure, local encryption key management, and contractual data boundary guarantees have resolved the fundamental contradiction between cloud economics and data localization law that previously pushed organizations toward on-premises alternatives. On-Premises grows more slowly as sovereign cloud absorbs demand that previously required owned infrastructure. Hybrid grows strongly as organizations manage the transition between legacy on-premises and cloud-based residency alternatives.

Data Governance & Compliance Leads Applications; Data Localization & Residency Control Drives Fastest Growth

Data governance leads as the foundational capability all other localization compliance depends on. Data localization and residency control is growing fastest because direct legislative mandates requiring data to remain within specific national jurisdictions are the most technically demanding compliance requirement, generating the highest per-organization spend on geographic data boundary enforcement infrastructure.

BFSI Leads End-User Industries; IT & Telecommunications Drives Fastest Growth

BFSI leads because financial institutions faced sector-specific localization requirements including India’s RBI payment data localization mandate and China’s financial data rules, giving the sector a longer compliance investment history. IT and Telecom grows fastest because the sector both operates as data infrastructure for customers with residency requirements and manages its own operating data across global networks that sovereignty frameworks specifically regulate.

Data Sovereignty & Localization Market Regional Analysis:

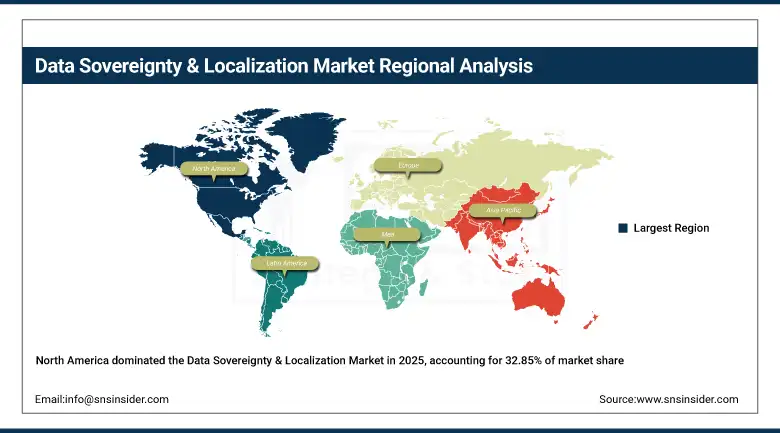

North America Data Sovereignty & Localization Market Insights

North America dominated in 2025 at USD 8.98 Billion (32.85%), projected to reach USD 44.38 Billion by 2035 at a CAGR of 17.36%. The region’s leadership reflects the concentration of hyperscaler cloud providers Microsoft, Amazon, Google investing heavily in sovereign cloud infrastructure to satisfy global enterprise and government data residency requirements, generating both product development spending and managed service revenue in their home market. U.S. federal cloud procurement rules and state-level data privacy law proliferation add domestic compliance demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Data Sovereignty & Localization Market Insights

The United States leads North American demand as the headquarters market for the world’s largest cloud providers building sovereign cloud infrastructure and as an enterprise market facing complex outbound data residency obligations imposed by foreign jurisdictions on data held about their citizens.

Europe Data Sovereignty & Localization Market Insights

Europe held a 27.40% share in 2025 at USD 7.49 Billion, growing to USD 38.11 Billion by 2035 at a CAGR of 17.70%. Europe is simultaneously the world’s most active data sovereignty regulatory environment producing GDPR, the EU Data Act, the Data Governance Act, and the AI Act, all carrying data residency implications and the primary export source for data localization regulatory philosophy that other regions are adapting. The EU-U.S. Data Privacy Framework’s ongoing legal vulnerability and Germany’s sovereign cloud programs both sustain enterprise compliance investment regardless of framework status.

Germany Data Sovereignty & Localization Market Insights

Germany leads European data sovereignty investment through the Gaia-X federated cloud initiative, sovereign cloud requirements for critical infrastructure operators under BSI’s C5 framework, and a Mittelstand industrial economy whose cross-border data flows create complex GDPR compliance requirements generating sustained software and services demand.

Asia Pacific Data Sovereignty & Localization Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 20.70%, rising from USD 6.74 Billion in 2025 to USD 44.15 Billion by 2035. The region’s growth leadership reflects simultaneous implementation of major localization frameworks China’s PIPL enforcement acceleration since 2024, India’s DPDP Rules under consultation in 2025, Indonesia’s PDP Law in force, and Vietnam’s cybersecurity data localization requirements being implemented each creating compliance demand from the multinationals operating in each market.

China Data Sovereignty & Localization Market Insights

China leads Asia Pacific through the world’s most actively enforced national data localization framework, requiring domestic data storage and cross-border transfer approvals for sensitive categories, generating large-scale compliance investment from both foreign multinationals operating in China and Chinese companies managing outbound data flows.

Latin America and Middle East & Africa Data Sovereignty & Localization Market Insights

Latin America held an 8.15% share in 2025 at USD 2.23 Billion, growing at a CAGR of 17.64% to USD 11.28 Billion by 2035. Brazil leads through LGPD compliance investment from its large financial and retail sectors. Middle East & Africa held a 6.95% share in 2025 at USD 1.90 Billion, growing at a CAGR of 17.51% to USD 9.51 Billion by 2035. Saudi Arabia leads through its PDPL enforcement and Vision 2030 national cloud infrastructure programs specifying data residency requirements for government cloud and AI systems. Saudi Arabia leads MEA through its actively enforced Personal Data Protection Law, Vision 2030 national cloud requirements mandating data residency for government and strategic sector data, and significant procurement activity from the National Data Management Office establishing compliance infrastructure across government entities.

Data Sovereignty & Localization Market Competitive Landscape:

Microsoft Corporation

Microsoft holds the most comprehensive sovereign cloud product portfolio in the data sovereignty market. Its EU Data Boundary program, completed in January 2025, provides European customers with contractual guarantees that all data processed by Azure, Microsoft 365, Dynamics 365, and Power Platform remains within the European Economic Area. Microsoft’s approach combines contractual data boundary commitments, local encryption key management through Azure Key Vault with customer-managed keys, and dedicated infrastructure in markets with strict localization requirements.

In November 2024, Microsoft launched its Azure Sovereign Cloud for the Gulf Cooperation Council, providing UAE and Saudi Arabia government customers with cloud infrastructure meeting national data residency requirements, with local data centers, local encryption key management, and contractual guarantees that data will not leave national territory without explicit customer authorization.

Amazon Web Services, Inc.

AWS participates in the data sovereignty market through its AWS Sovereign Cloud program and GovCloud regions designed for regulated workloads with strict data residency requirements. Rather than a single boundary product, AWS offers region selection, AWS Control Tower data residency guardrails, Dedicated Local Zones in specific countries, and contractual commitments that together allow customers to construct a residency architecture suited to their specific regulatory obligation profile.

In March 2025, AWS announced expansion of its European Sovereign Cloud, adding data centers in Germany and Spain designed for EU data sovereignty requirements for financial services and healthcare customers, with commitments that all data processing, support access, and operational management would be performed by EU-based personnel.

Data Sovereignty & Localization Market Key Players:

-

Microsoft Corporation

-

Amazon Web Services, Inc.

-

Google LLC

-

IBM Corporation

-

Oracle Corporation

-

SAP SE

-

Alibaba Cloud

-

Salesforce, Inc.

-

Cisco Systems, Inc.

-

VMware, Inc.

-

Thales Group

-

Atos SE

-

Equinix, Inc.

-

Rackspace Technology

-

Hewlett Packard Enterprise (HPE)

-

Dell Technologies Inc.

-

T-Systems International GmbH

-

NetApp, Inc.

-

Iron Mountain Incorporated

-

Hitachi Vantara LLC

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.35 Billion |

| Market Size by 2035 | USD 147.43 Million |

| CAGR | CAGR of 18.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software (Data governance, compliance, encryption, localization platforms), Hardware (Servers, storage systems, security appliances), and Services (Consulting, implementation, managed compliance services)) • By Deployment Mode (On-Premises, Cloud-Based, and Hybrid) • By Application (Data Governance & Compliance Management, Data Localization & Residency Control, Risk Management & Security, and Access Control & Monitoring) • By End-User Industry (BFSI, Government & Public Sector, Healthcare, IT & Telecommunications, and Retail & E-commerce) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation; Amazon Web Services, Inc.; Google LLC; IBM Corporation; Oracle Corporation; SAP SE; Alibaba Cloud; Salesforce, Inc.; Cisco Systems, Inc.; VMware, Inc.; Thales Group; Atos SE; Equinix, Inc.; Rackspace Technology; Hewlett Packard Enterprise (HPE); Dell Technologies Inc.; T-Systems International GmbH; NetApp, Inc.; Iron Mountain Incorporated; Hitachi Vantara LLC. |

Frequently Asked Questions

North America dominated the Data Sovereignty & Localization in 2025

Software (Data governance, compliance, encryption, localization platforms) dominated the Data Sovereignty & Localization in 2025.

The market is driven by stringent data protection regulations, rising data privacy concerns, increasing cloud adoption, and growing demand for localized data storage and compliance solutions.

The Data Sovereignty & Localization size was USD 27.35 Billion in 2025 and is expected to reach USD 147.43 Billion by 2035.

The Data Sovereignty & Localization is expected to grow at a CAGR of 18.39% from 2026–2035.

Get in Touch