Defense Semiconductor Market Report Scope & Overview:

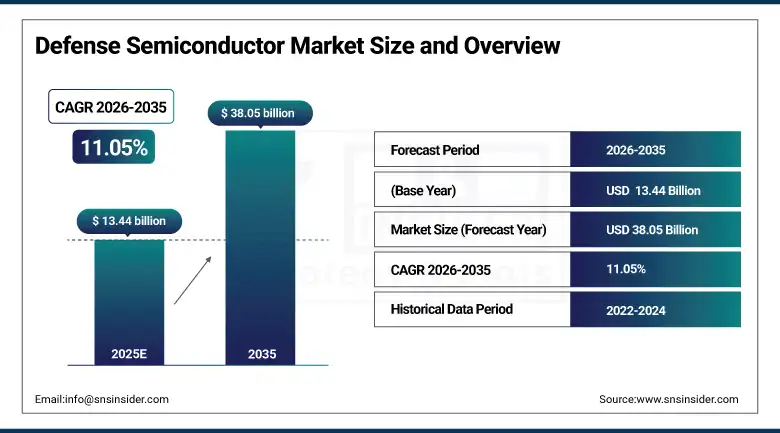

The Defense Semiconductor Market size was valued at USD 13.44 Billion in 2025 and is projected to reach USD 38.05 Billion by 2035, growing at a CAGR of 11.05% during 2026-2035.

The defense semiconductor market is expanding driven by ongoing growth in military spending globally, a generational change in weapons platforms towards unmanned and electronics-intensive systems, and a high level of government intervention aimed at ensuring access to homegrown semiconductor supply chains for critical defense applications. Geopolitical risks in Eastern Europe, the Indo-Pacific region, and the Middle East are prompting allied countries to accelerate modernization beyond their originally planned timelines, thereby boosting near-term spending on radar systems, electronic warfare systems, satellite communications systems, and precision munitions, all of which heavily use specialized semiconductors.

Market Size and Forecast:

-

Market Size in 2025: USD 13.44 Billion

-

Market Size by 2035: USD 38.05 Billion

-

CAGR of 11.05% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Defense Semiconductor Market - Request Free Sample Report

Key Defense Semiconductor Market Trends

-

Widespread adoption of Gallium Nitride-based transmit/receive modules in active electronically scanned array radars, replacing legacy Gallium Arsenide at every major new-start and upgrade program across fighter aircraft, naval destroyers, and ground-based air defense batteries.

-

Accelerated investment in electronic warfare semiconductors, driven by documented lessons from Ukraine regarding GPS jamming and drone-based electronic attacks, with program offices in the U.S., Europe, and the Gulf states expanding EW budgets at double-digit annual rates through 2025.

-

Domestic sourcing mandates stemming from the U.S. CHIPS and Science Act and equivalent European and Asian legislation are reshaping supplier qualification requirements, making trusted foundry status a baseline procurement criterion for an expanding range of defense programs.

-

Proliferation of autonomous platforms and loitering munitions under initiatives such as the U.S. Replicator program is generating sustained demand for low-power embedded processors and edge AI inference chips capable of reliable operation under jamming and contested environments.

-

Hardware cybersecurity devices, including root-of-trust modules, secure processing enclaves, and post-quantum cryptographic accelerators, are earning dedicated budget lines within major platform programs as Zero Trust architecture mandates propagate across military networks.

U.S. Defense Semiconductor Market Size Outlook

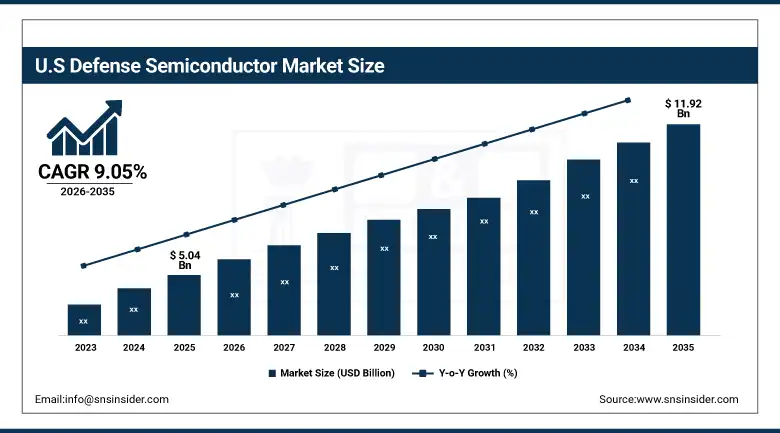

The U.S. Defense Semiconductor Market was valued at 5.04 Billion in 2025 and is expected to reach 11.92 Billion by 2035, growing at a CAGR of 9.05% from 2026-2035. The U.S. market is 83.14% of the North American market and is driven by the Trusted Foundry ecosystem of Defense Microelectronics Activity, DoD R&D spending through DARPA and Microelectronics Commons, and close ties between government labs and the commercial semiconductor industry.

Defense Semiconductor Market Growth Drivers:

-

Defense Semiconductor Demand Surges Globally as Geopolitical Tensions Accelerate Electronics-Intensive Platform Modernization and Multi-Domain Warfare Adoption

The main driver of the global defense semiconductor market growth remains the concurrent acceleration of military modernization programs in NATO-aligned and Indo-Pacific nations in response to a security environment that has worsened significantly since 2022. Unlike past military buildups, the current programs are inherently biased towards electronics-based systems, including next-generation AESA radar systems, networked air defense systems, electronic warfare systems, and precision-guided munitions with multi-mode seekers, all of which rely fundamentally on the performance of semiconductors. Germany, in its formal commitment in 2024 to maintain defense expenditures in excess of 2% of GDP, has set aside significant funds for upgrading the avionics of Eurofighter aircraft and procuring IRIS-T SLM air defense systems, both of which rely in significant part on radar and signal processing chips. Poland’s concurrent procurement of M1A2 SEPv3 main battle tanks and F-35A fighters adds years of sustainment and upgrade expenditures on electronics.

Defense Semiconductor Market Restraints:

-

Defense Semiconductor Market Growth Constrained by Long Qualification Timelines, Workforce Shortages, Export Control Complexity, and Limited Dedicated Foundry Capacity

The global defense semiconductor market operates under a set of fundamental constraints that influence the rate of growth compared to the commercial semiconductor industry. In qualification cycles for MIL-SPEC and space-grade parts, three to five years are typical, during which time the commercial industry can advance two complete generations of technology. There exists a fundamental tension in program management teams that seek to leverage advancements in commercial technology but cannot afford qualification risk in life-critical systems. Export controls, such as US ITAR and EAR regulations and the controlled items list in the Wassenaar Arrangement, impose regulatory overhead on sales into allied nations and complicate international program structures, affecting smaller organizations without dedicated compliance staff.

Defense Semiconductor Market Opportunities:

-

Autonomous Platform Proliferation, Space Domain Expansion, and Heterogeneous Integration Unlock Multi-Billion Dollar Growth Opportunities for Defense Semiconductor Suppliers Through 2035

There are a number of structurally significant growth opportunities within the marketplace. The first is the autonomous and unmanned systems opportunity, which is the most immediate and volume-driven. The U.S. Replicator Initiative and similar programs have the potential to create a new stream of procurements for affordable attritable systems that require perception, processing, and communications semiconductors of a scale and cost structure previously unseen in the DoD. The Space Development Agency's Transport Layer constellation of satellites, of which several have been awarded in 2024, represents a new steady-state requirement for radiation-hardened processors and power management devices refresh cycles faster than the conventional geosynchronous orbit.

Defense Semiconductor Market Segmentation Analysis

-

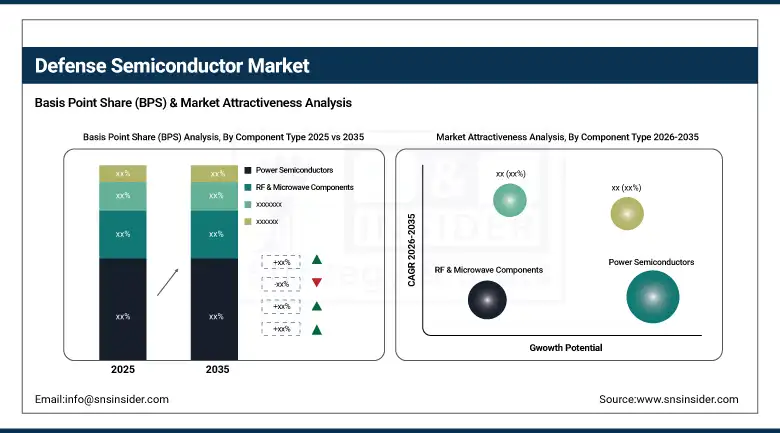

By Component Type, Power Semiconductors dominated with 30.68% in 2025, and Power Semiconductors is also expected to grow at the fastest CAGR of 12.80% from 2026 to 2035.

-

By Application, Radar & Surveillance Systems dominated with 27.34% in 2025, and Electronic Warfare is expected to grow at the fastest CAGR of 13.10% from 2026 to 2035.

-

By Platform / End-Use, Aerospace (Aircraft, UAVs, Satellites) dominated with 32.45% in 2025, and Cybersecurity & Intelligence is expected to grow at the fastest CAGR of 12.40% from 2026 to 2035.

-

By Type / Technology, Digital Semiconductors dominated with 29.63% in 2025, and RF & Power Semiconductors is expected to grow at the fastest CAGR of 12.22% from 2026 to 2035.

By Component Type, Power Semiconductors Lead Defense Semiconductor Market While RF & Microwave Components Sustain Strong Momentum Through 2035

In 2025, Power Semiconductors led the component segment reflecting the central role of wide-bandgap GaN and SiC devices in radar transmitters, electronic warfare power amplifiers, propulsion converters for naval and land platforms, and airborne power management systems. From 2026 to 2035, Power Semiconductors are also projected to grow at the fastest CAGR driven by accelerating adoption of all-electric propulsion architectures in naval vessels and armored ground vehicles, the shift to GaN-based T/R modules across AESA radar upgrades, and expanding use of SiC converters in directed-energy weapon power conditioning systems.

By Application, Radar and Surveillance Systems Dominate While Electronic Warfare Set for Fastest Growth in Defense Semiconductor Market 2026 to 2035

In 2025, Radar & Surveillance Systems commanded the largest application share as active electronically scanned array technology became the de facto standard across new-generation fighters, destroyers, and ground-based air defense batteries. Each AESA radar unit contains hundreds to thousands of T/R modules incorporating GaN transistors, low-noise amplifiers, and phase shifters, making fleet-wide upgrades from mechanically scanned legacy radars a multi-year, high-volume semiconductor replacement cycle. The documented role of GPS jamming and drone-based electronic attacks in the Ukraine conflict accelerated EW program funding globally, with demand for adaptive, wideband RF signal processing semiconductors rising sharply.

By Platform / End-Use, Aerospace Leads Defense Semiconductor Market While Cybersecurity and Intelligence Segment Poised for Fastest Growth 2026 to 2035

Aerospace platforms including aircraft, UAVs, and satellites dominated and supported by the intensive semiconductor content of modern combat aircraft avionics, the growing military UAV fleet from strategic HALE platforms to tactical loitering munitions, and the Space Development Agency's proliferated LEO satellite constellations. Zero Trust architecture mandates propagating across DoD networks are driving demand for hardware root-of-trust devices, secure enclaves, and hardware-enforced cryptographic accelerators that verify platform integrity at boot and runtime, a function requiring purpose-built silicon rather than software solutions.

By Type / Technology, Digital Semiconductors Lead Defense Semiconductor Market While RF and Power Semiconductors Show Fastest Momentum Through 2035

Digital Semiconductors led the technology segment in 2025 driven by the growing digitization of formerly analog radar, communications, and avionics functions and the adoption of FPGAs and DSPs as the standard architecture for mission computers where software upgrade flexibility over long platform lifetimes is a core procurement requirement.

Report Insights

North America Defense Semiconductor Market Insights

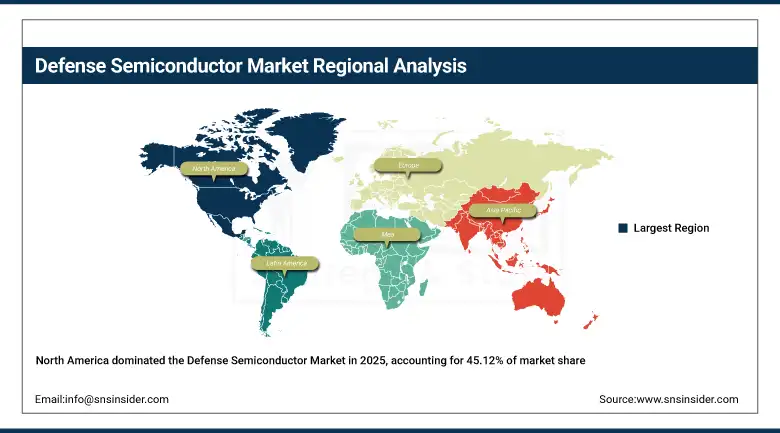

In 2025, North America accounted for the highest share of 45.12% of the global Defense Semiconductor market, valued at USD 6.06 Billion, and is expected to grow at a CAGR of 9.30% by 2035. This is due to the enormous scale of procurement machinery of the U.S. Department of Defense, the concentration of the world's most sophisticated defense electronics primes, and the maturity of the domestic trusted foundry ecosystem enabled by the Defense Microelectronics Activity's Trusted Foundry Program. The contribution of Canada to the Defense Semiconductor market was valued at USD 1.02 Billion, accounting for 16.86% of the total Defense Semiconductor market share of North America. This is due to its contribution to NORAD modernization, RCAF aircraft sustainment, and joint F-35 program participation.

Get Customized Report as per Your Business Requirement - Enquiry Now

In North America, the United States dominated the Defense Semiconductor market in 2025, Strong demand from the F-35 program, the Next Generation Jammer, the Army's Integrated Visual Augmentation System, and the Space Development Agency's satellite constellations drove procurement across every major component segment.

Europe Defense Semiconductor Market Insights

In 2025, Europe held a 20.47% share of the global Defense Semiconductor market at USD 2.75 Billion, growing at a CAGR of 9.55% through 2035. The region's market is structurally driven by Eurofighter Typhoon avionics upgrade cycles, the KNDS MGCS next-generation tank program, MBDA missile family electronics refreshes, and the Nordic and Baltic states' accelerated procurement of ground-based air defense systems. Germany, Poland, and Sweden materially increased defense electronics budgets through 2024 in direct response to the security environment in Eastern Europe..

In Europe, Germany dominated the Defense Semiconductor market in 2025, driven by its role as the continent's largest defense spender after the United Kingdom, its commitment to sustained 2%-plus GDP defense spending, and the high electronics content of its priority procurement programs including the Eurofighter Typhoon modernization, Tiger attack helicopter upgrades, and the MGCS land combat system development program.

Asia Pacific Defense Semiconductor Market Insights

Asia Pacific is expected to grow at the fastest CAGR of 13.72% from 2026 to 2035 in the global Defense Semiconductor market, with the region valued at USD 3.34 Billion in 2025. Japan's decision to double defense spending as a percentage of GDP, operationalized through 2024-2025 budgets, translated directly into accelerated procurement of AESA radars, EW systems, and precision-guided munitions across its air and maritime self-defense forces. South Korea's defense electronics industry has matured to the point where domestically designed radar and missile seeker systems from companies including LIG Nex1 and Hanwha Systems are being exported to third markets, generating both domestic consumption and export-driven semiconductor demand..

In Asia Pacific, Japan dominated the Defense Semiconductor market from 2025 onward, driven by its status as the region's most mature defense electronics ecosystem, its acceleration of defense spending to the 2% of GDP threshold, and the high semiconductor intensity of its priority modernization programs.

Latin America (LATAM) and Middle East & Africa (MEA) Defense Semiconductor Market Insights

In 2025, Latin America and the Middle East & Africa collectively represented smaller but fast-growing portions of the global Defense Semiconductor market. Latin America accounted for a 5.26% share at USD 0.71 Billion with a CAGR of 12.71% through 2035, led by Brazil's Gripen E/F program which includes avionics technology transfer provisions, and ongoing naval modernization programs that carry significant radar and communications chip content. The Middle East & Africa held a 4.27% share at USD 0.57 Billion but carries the highest CAGR of any region at 14.38% through 2035. Saudi Arabia, the UAE, and Qatar are simultaneously upgrading air defense architectures, procuring advanced combat aircraft, and building indigenous defense electronics manufacturing capabilities.

Competitive Landscape

Analog Devices, Inc. is a global semiconductor leader headquartered in Wilmington, Massachusetts, specializing in high-performance data converters, RF signal chain components, and precision analog devices. Its integrated RF transceiver SoC families have become reference designs for defense-grade software-defined radios, phased-array radar front-ends, and adaptive electronic warfare systems across U.S. and allied military programs.

-

Through 2024-2025, Analog Devices secured design wins for its next-generation wideband radar transceiver ICs in U.S. and allied ground-based air defense upgrade programs, with production ramp anticipated through 2026-2027.

Texas Instruments Incorporated, headquartered in Dallas, Texas, operates one of the broadest analog and embedded processing portfolios relevant to defense applications, covering precision data converters for radar signal chains, motor control ICs for electromechanical actuators in guided munitions, power management devices for avionics, and ruggedized microcontrollers for mission-critical embedded applications.

- In 2024, Texas Instruments expanded its HIREL product line with additional MIL-PRF-38535 Class V qualified devices targeting space and high-reliability airborne applications, specifically the next-generation satellite communications and GPS receiver market segments where the restricted field of qualified suppliers commands premium pricing.

Defense Semiconductor Companies are:

-

Intel Corporation

-

Texas Instruments

-

Analog Devices

-

AMD (Xilinx)

-

Microchip Technology

-

Infineon Technologies

-

NXP Semiconductors

-

STMicroelectronics

-

Qualcomm

-

Broadcom

-

Renesas Electronics

-

Maxim Integrated

-

ON Semiconductor

-

Lattice Semiconductor

-

Vishay Intertechnology

-

Raytheon Technologies

-

Lockheed Martin

-

BAE Systems

-

Northrop Grumman

-

Boeing

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.44 Billion |

| Market Size by 2035 | USD 41.62 Billion |

| CAGR | CAGR of 11.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Microprocessors & Microcontrollers, Memory Devices, Analog & Mixed-Signal ICs, RF & Microwave Components, and Power Semiconductors) • By Application (Radar & Surveillance Systems, Communication Systems, Electronic Warfare, Navigation & Avionics, and Missile Guidance & Control) • By Platform / End-Use (Aerospace (Aircraft, UAVs, Satellites), Land Systems (Armored Vehicles, Ground Defense), Naval Systems, and Cybersecurity & Intelligence) • By Type / Technology (Analog Semiconductors, Digital Semiconductors, Mixed-Signal Semiconductors, RF & Power Semiconductors, and Radiation-Hardened Semiconductors) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Texas Instruments, Analog Devices, AMD (Xilinx), Microchip Technology, Infineon Technologies, NXP Semiconductors, STMicroelectronics, Qualcomm, Broadcom, Renesas Electronics, Maxim Integrated, ON Semiconductor, Lattice Semiconductor, Vishay Intertechnology, Raytheon Technologies, Lockheed Martin, BAE Systems, Northrop Grumman, Boeing. |

Frequently Asked Questions

Cybersecurity & Intelligence is the fastest-growing platform segment with a CAGR of 12.40% from 2026 to 2035, driven by Zero Trust architecture mandates and the proliferation of hardware security modules across military networks.

Electronic Warfare is the fastest-growing application segment with a CAGR of 13.10% from 2026 to 2035, driven by accelerated global investment in adaptive EW systems following lessons drawn from recent conflicts.

North America dominated the Defense Semiconductor Market in 2025 with a 45.12% share.

Power Semiconductors dominated the Defense Semiconductor Market with a 30.68% share in 2025.

The Defense Semiconductor Market size was USD 13.44 Billion in 2025 and is expected to reach USD 38.05 Billion by 2035.

Get in Touch