Elastography Imaging Market Report Scope & Overview:

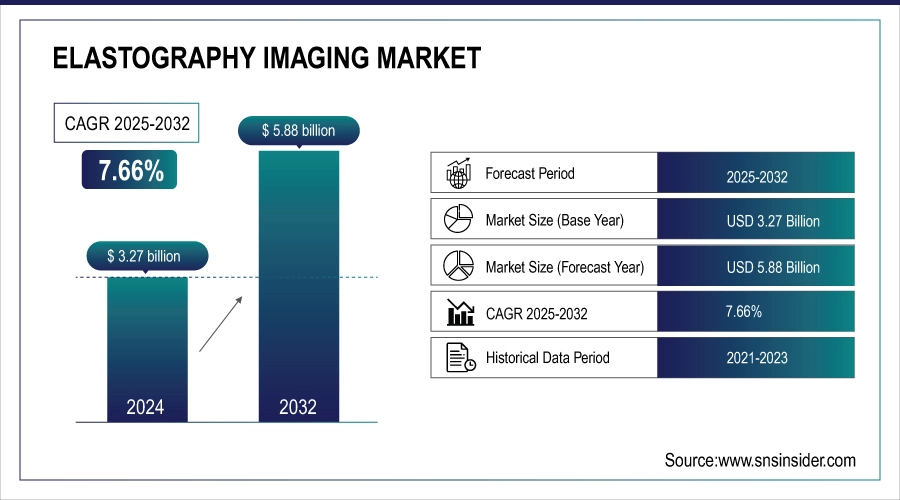

Elastography Imaging Market size was valued at USD 3.27 billion in 2024 and is expected to reach USD 5.88 billion by 2032, growing at a CAGR of 7.66% over the forecast period of 2025-2032.

The increasing need for non-invasive diagnostics will be a significant driving factor for the elastography imaging market, since conventional techniques like biopsies are invasive, painful, and include risks of bleeding and infection. In contrast, elastography provides risk-free, real-time, and radiation-free ability to measure tissue stiffness, so it is particularly convenient for diagnosing liver diseases, cancer, and musculoskeletal problems. Its instant results without anesthetics and recovery time are a concept well accepted currently, and even in demand from hospitals and diagnostic centers, in tune with the worldwide change that the diagnostic test should be patient-friendly, quick, and with no risk.

To Get more information On Elastography Imaging Market - Request Free Sample Report

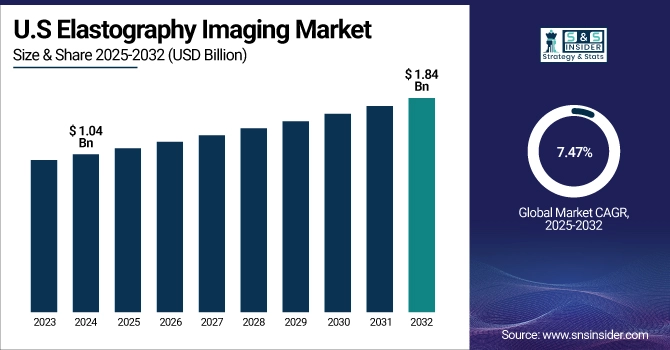

The U.S. Elastography Imaging Market was valued at USD 1.04 billion in 2024 and is expected to reach USD 1.84 billion by 2032, growing at a CAGR of 7.47% from 2025-2032.

The global elastography imaging market is dominated by the U.S. Elastography is employed in both hospitals and diagnostic centers as a safe and non-invasive method for the diagnosis and follow-up of these diseases. Strong insurance population, high health care spending, and major imaging companies like GE Healthcare and Siemens also fuel its growth.

For instance, the Biden-Harris Administration announced that 21.3 million people selected an Affordable Care Act Health Insurance Marketplace plan during the 2024 Open Enrollment Period.

All these factors together make the United States the biggest and the fastest growing market for elastography imaging.

Market Dynamics:

Drivers

-

Rising Technological Advancements in Imaging Systems are driving the Elastography Imaging Market growth.

Growing improvements in imaging systems are also a key factor driving the elastography imaging market analysis, as advanced shear wave and strain elastography technologies equipped with AI-based algorithms and real-time imaging have been developed lately. They improve the accuracy of diagnosis through a quantitative, repeatable measurement of tissue stiffness, and they are vital for detecting liver fibrosis, cancer, and musculoskeletal diseases. Moreover, the development of portable and point-of-care (POC) elastography devices are revolutionizing clinical practice by providing faster and accessible diagnostics in outpatient clinics, emergency departments, and remote medical centers, and expanding the market out of the hospital toward hospitals.

-

Increasing Investments by Key Players are driving the Elastography Imaging Market growth.

Growing investments by several prominent medical imaging companies, which include GE Healthcare, Philips, Canon Medical, Siemens Healthineers, are a contributing factor to the growth of the elastography imaging market.

For instance, 14 May 2025, Siemens announced a €150 million investment in ultrasound innovation, focusing on strain and shear wave elastography, targeting faster liver and thyroid diagnostics using AI.

Such companies are consistently developing and introducing new advanced elastography systems, offering better imaging, real-time analysis, and connection with AI for better diagnosis. For instance, GE Healthcare also recently added to its portfolio of ultrasound elastography solutions as demand increases for liver and breast imaging. These developments are lowering the barrier to entry and creating more effective elastography and enabling hospitals and diagnostic centers everywhere to reap the benefits of this technology without being invasive.

Restraints:

-

Shortage of skilled professionals is restraining the Elastography Imaging Market growth.

Lack of skilled professionals is one of the major challenging factors for the growth of the elastography imaging market.

For instance, WHO estimates a projected shortfall of 11 million health workers by 2030, mostly in low- and lower-middle-income countries.

Accurately interpreting elastography results relies on the skill of trained radiologists and sonographers since the technology assesses tissue stiffness and subtle changes in images that demand clinical precision. Wherever it is practiced, however, most especially in developing countries and rural areas, there are few specialized training programs, and few specialists. Even if these tools are present, the lack of expert users can result in underuse or misdiagnosis, hampering the effectiveness and acceptance of elastography. This training deficit remains a challenge for the expansion of its use in everyday medical practice globally. Consequently, inadequately trained personnel can misapply technology, produce poor-quality images, or render the results incorrectly, all of which dilute the clinical usefulness of the elastography imaging market trend.

Segmentation Analysis:

By modality

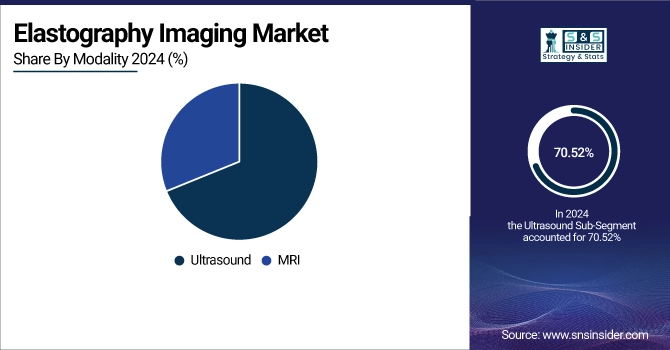

Ultrasound represents the dominant segment in the elastography imaging market, with a 70.52% market share in 2024. Because elastography imaging is cheaper, portable, and easier to use than other imaging tools such as MR elastography, it has the largest share in the elastography imaging market. It avoids radiation and enables real-time imaging, so it is particularly helpful in the staging of liver disease, assessment of breast lesions, and the examination of the thyroid and the prostate. The tool can be adapted for use in large hospitals and small clinics, including in rural and low-resource settings. Moreover, the development of shear wave and strain elastography has resulted in the efficacy of ultrasound surpassing that of many other imaging modalities, leading to its recent widespread use in virtually all medical disciplines. Its low cost, ease-of-use, and prevalence of clinical applications make ultrasound the major modality for elastography imaging around the world.

MRI plays a very important role in the elastography imaging market growth as it is the fastest-growing segment with a CAGR of 8.03%. Magnetic Resonance Imaging (MRI) is the fastest-growing segment in the elastography market because it provides very high diagnostic accuracy and non-invasive deep organ exploration not easily accessible to ultrasonography (US) (e.g., liver, brain, and pancreas) as well. Unlike ultrasound, MRI is not constrained by body habitus (e.g., obesity or ascites) and provides high-resolution, 3D images with quantitative measures that can be consistently monitored over time. This makes it especially invaluable in monitoring liver fibrosis stage in chronic liver disease, such as Non-Alcoholic Fatty Liver Disease (NAFLD) and hepatitis, or in neurological diseases like multiple sclerosis. The increasing uptake of high-end MRI systems in developed nations, along with increasing awareness regarding liver health are stimulating the demand.

By application

In 2024, the General Imaging segment dominated the elastography imaging market share with a 34.80%. General imaging rules over the market of elastography imaging as it can be performed on different body organs, including the liver, thyroid, breast, kidneys, and other soft tissues, and is versatile and always clinically in demand. It is clinically used to evaluate liver stiffness in chronic liver diseases, such as NAFLD, which affects greater than 25% of the world’s population, and to distinguish between benign and malignant masses in the breast or thyroid. General imaging modalities are non-invasive, cheap, and are currently included in routine healthcare checks or screening schemes. Given that many diseases are first or follow-up imaging of elastography, general imaging is the basis of early diagnosis.

Breast elastography is expected to witness the fastest growth during the forecast period as it enables early, accurate, and non-invasive diagnosis of breast tumors through the measurement of tissue stiffness, which is usually higher in malignant lumps than in benign lumps. Considering that breast cancer is the most common female cancer worldwide, with more than 2.3 million new cases diagnosed every year, there is increasing pressure to increase early detection. The technology is a painless, radiation-free, and cost-effective alternative to biopsies and is now available in conjunction with standard mammography and ultrasound.

By end-user

Hospitals are the largest and fastest growing market of the elastography imaging market, with 41.30% of market share and the CAGR of 8.05%. They have well-established facilities, large patient quotas, and the capacity to implement new medical innovations. Hospitals are local centers to diagnose and treat of variety of diseases Ð liver diseases, cancerous diseases, and musculoskeletal systems are to name a few, which enjoys from elastography quantitative imaging. They would generally have established radiology departments, with skilled personnel and more financial resources, that can afford to purchase both the US and MRI elastography systems. Furthermore, the increasing prevalence of chronic diseases and the need for non-invasive diagnostic tools have led hospitals to include elastography in their practice for early disease detection and follow-up of diseases.

Regional Analysis:

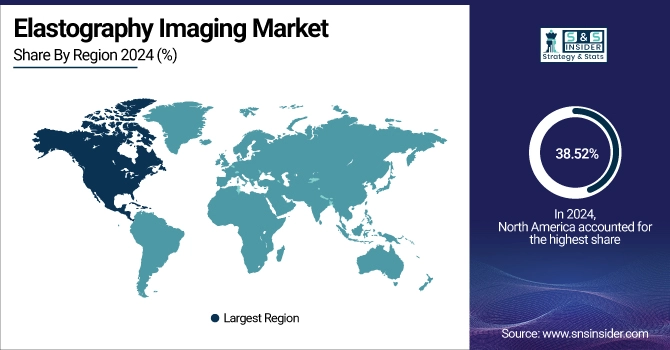

In 2024, the North American region dominated the elastography imaging market and accounted for 38.52% of the overall revenue share. North America dominates the market of elastography imaging, primarily due to the developed health care system with widespread access to novel imaging technologies and high prevalence of chronic diseases (such as liver diseases, breast cancer, and obesity related diseases (ORD)). The U.S. recorded more than USD 1.04 billion revenue in 2024. In the U.S., especially, ultrasound and MR elastography have been adopted broadly in hospitals and diagnostic facilities, aided by favourable reimbursement conditions.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific region is projected to grow with the fastest CAGR of 8.10% over the forecast period. The elastography imaging market in APAC is expected to grow at the highest CAGR during the forecast period, owing to a large population (including a large patient population due to the high prevalence of chronic diseases such as liver diseases, cancer, and diabetes) and increasing awareness about non-invasive diagnostic tools. Rapidly developing countries such as China, India, and South Korea are increasingly focusing on the modernisation of health care, including the integration of ultrasound and MRI elastography systems into public and private hospitals. Government initiatives in healthcare, easier access to medical insurance, and low manufacturing costs contribute to the overall expansion of global and regional market players in the region. With the increasing need for early and accurate diagnosis, mostly in liver and breast imaging, the elastography market in the Asia-Pacific region is projected to show high growth in the coming years.

The availability of advanced imaging systems, established healthcare infrastructure, and high emphasis on preventive healthcare in Europe ensures a robust share in the elastography imaging market. Ultrasound and MRI elastography are widely adopted in Germany, France, and the UK, especially for liver disease, breast cancer, and musculoskeletal diseases. It benefits from strong public funding of healthcare, a favourable regulatory environment (CE mark), and an increasing focus on non-invasive and non-radiating diagnosis.

Latin America is also showing significant growth in the elastography imaging market due to the development of healthcare infrastructure and large patient pool for chronic diseases, and increasing access to advanced diagnostic technologies in the region, especially Brazil, Mexico, and Argentina. Increasing incidence of liver diseases, breast cancer, and other obesity related diseases is compelling the general population to demand early and non-invasive diagnosis like elastography. There is also growing interest from multinational imaging companies as well as state and local governments, seeking to strengthen their cross-sectional imaging capabilities in both urban and semi-urban territories. The breeze of non-radiation, low-cost imaging techniques are getting to the radiologists, while courses are getting better and better, getting to Elastography in a slow and safe way through Latin America.

Similar to Latin America, the Middle East and Africa also shows steady growth in the elastography imaging market in the Middle East & Africa is driven by a combination of rising healthcare investments, increasing awareness of non-invasive diagnostic methods, and a growing burden of chronic conditions such as liver diseases, cancers, and obesity-related disorders. Countries like Saudi Arabia, the UAE, and South Africa are actively modernizing their healthcare systems, establishing new hospitals, and equipping them with advanced imaging technologies, including elastography. Government initiatives aimed at improving early diagnosis and reducing dependence on invasive procedures are further supporting adoption.

Key Market Players:

Elastography Imaging Market companies include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical System, Samsung Medison, Hitachi, Shenzhen Mindray, Bio-Medical Electronics, FUJIFILM Holdings, Resoundant Inc, and other players.

Recent Developments:

-

In early 2024, Resoundant expanded MR Elastography clinical collaborations. Resoundant partnered with academic hospitals in the U.S. and Europe to expand MR elastography use in brain and liver diagnostics.

-

In March 2025, Siemens announced enhanced AI-assisted elastography analysis integrated into its ACUSON Sequoia system, improving real-time liver fibrosis staging. The new AI tools offer automated quantification for improved workflow in large-volume hospital settings.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.27 billion |

| Market Size by 2032 | USD 5.88 billion |

| CAGR | CAGR of 7.66% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By modality (Ultrasound and MRI) • By application (General Imaging, Hepatology,BreastUrology,Cardiology,Orthopedic and Musculoskeletal, and Others) • By End User (Hospitals,AImaging Centers and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical System, Samsung Medison, Hitachi, Shenzhen Mindray, Bio-Medical Electronics, FUJIFILM Holdings, Resoundant Inc and other plyers. |

Frequently Asked Questions

General Imaging segment dominated the elastography imaging Market.

The shortage of skilled professionals is a key restraint in the growth of the elastography imaging market.

The CAGR of the elastography imaging Market is 7.74% during the forecast period of 2025-2032.

The North American region dominated the elastography imaging Market in 2024.

The projected market size for the elastography imaging Market is USD 5.82 billion by 2032.

Get in Touch