Electrophysiology Market Report Scope & Overview

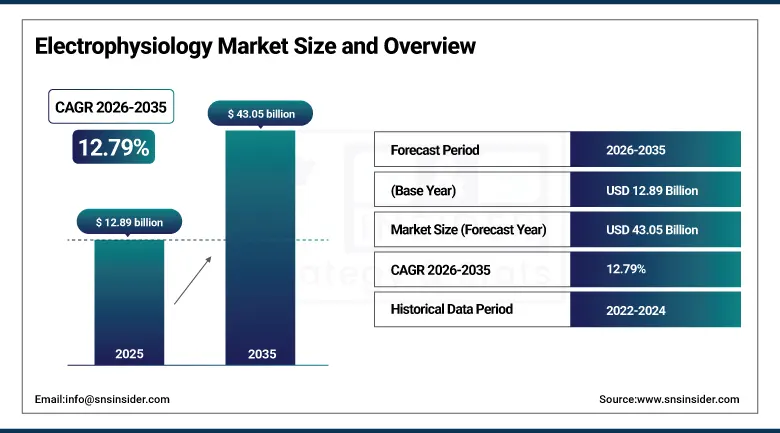

The Electrophysiology Market was valued at USD 12.89 billion in 2025 and is expected to reach USD 43.05 billion by 2035, growing at a CAGR of 12.79% from 2026–2035.

The global electrophysiology market is experiencing a period of remarkable clinical and commercial growth driven by the convergence of a rapidly rising cardiac arrhythmia burden across ageing global populations, the transformative advancement of catheter ablation technology that is enabling curative rather than merely palliative treatment of a growing range of cardiac rhythm disorders, and the progressive shift of complex cardiac electrophysiology procedures from specialist tertiary care centres to a broader network of community hospitals, ambulatory cardiac care centres, and outpatient electrophysiology laboratories equipped with increasingly user-friendly and automated mapping and ablation platforms. The global prevalence of atrial fibrillation, the most common cardiac arrhythmia and the primary indication driving electrophysiology procedure volume growth, is estimated at between 33 and 44 million affected individuals globally and is growing at rates substantially above overall population growth as the combination of demographic ageing and the increasing prevalence of AF-predisposing risk factors including hypertension, diabetes, obesity, and sleep apnoea creates an expanding patient pipeline that cardiac electrophysiology services across all markets are actively working to address.

The September 2025 FDA clearance of Abbott’s latest generation ablation catheters with enhanced lesion precision and procedural efficiency capabilities reflects the continuous technology improvement investment that major electrophysiology equipment manufacturers are deploying to maintain competitive positioning in a market where clinical differentiation on procedural success rates, safety profiles, and operator experience quality is becoming the primary criterion by which electrophysiology programmes select and remain loyal to their preferred equipment platforms.

Electrophysiology Market Size And Forecast

-

Market Size In 2026E: USD 14.54 Billion

-

Market Size By 2035: USD 43.05 Billion

-

CAGR: 12.79% From 2026 To 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Electrophysiology Market - Request Free Sample Report

Electrophysiology Market Trends

-

Rapid commercial adoption of pulse field ablation technology across electrophysiology programmes in North America, Europe, and increasingly Asia Pacific, driven by the technology’s demonstrated advantages in pulmonary vein isolation for atrial fibrillation treatment including near-complete elimination of the phrenic nerve palsy and oesophageal injury risks associated with thermal ablation modalities, dramatically shorter procedure times relative to cryoablation, and superior tissue selectivity that enables precise cardiac myocyte ablation without collateral injury to adjacent anatomical structures.

-

Progressive expansion of three-dimensional electroanatomical mapping system adoption across a broader range of hospital electrophysiology laboratory settings beyond the academic and quaternary care centres where these systems initially gained clinical traction, driven by the systems’ demonstrated contributions to procedure success rates, their ability to enable less experienced operators to perform complex ablation procedures with greater safety, and their essential role as the platform enabling the advanced substrate characterisation that next-generation ablation strategies for persistent atrial fibrillation and ventricular tachycardia require.

-

Growing adoption of wearable cardiac monitoring and ambulatory electrocardiography devices for arrhythmia detection and post-ablation rhythm monitoring that are expanding the diagnostic funnel feeding electrophysiology procedure volumes by identifying previously undiagnosed paroxysmal arrhythmias in symptomatic patients whose rhythm disorder episodes were not captured by standard 12-lead ECG or short-duration holter monitoring, creating a growing pipeline of diagnosed patients who are candidates for catheter ablation evaluation.

-

Increasing development of robotic catheter navigation systems for electrophysiology procedures that provide more consistent and precisely controllable catheter positioning than manual manipulation, reduce radiation exposure for operators across high-volume procedure caseloads, and enable remote or teleoperated procedure capability that could eventually enable specialist electrophysiology expertise to be delivered to patients at geographically remote sites through robotically controlled catheter systems operated by operators at distant locations.

-

Rising focus on electrophysiology laboratory workflow optimisation and digital integration including real-time procedure guidance software, AI-powered arrhythmia substrate analysis tools, automated procedure documentation systems, and remote cardiac monitoring integration that collectively improve procedure throughput, reduce per-case resource utilisation, and generate the clinical outcome data that enables electrophysiology programme benchmarking and quality improvement investment justification.

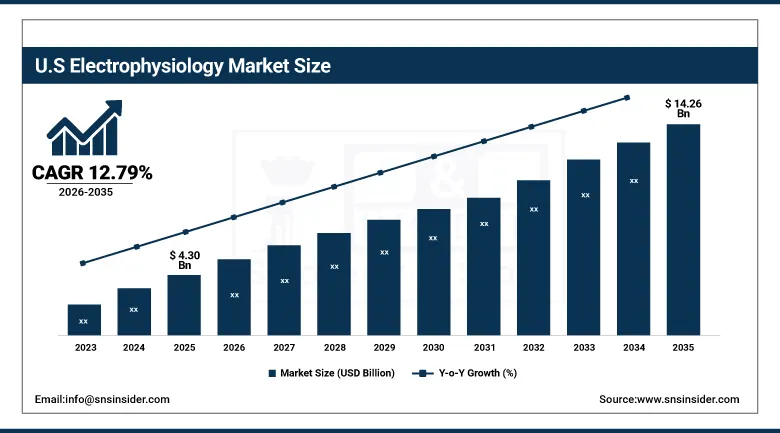

U.S. Electrophysiology Market Outlook

The U.S. electrophysiology market was valued at USD 4.30 billion in 2025 and is expected to reach USD 14.26 billion by 2035, growing at a CAGR of 12.79% from 2026–2035, anchored by the country’s over 1,200 fully equipped electrophysiology laboratories, the highest per-capita concentration of trained cardiac electrophysiologists globally, extensive Medicare and commercial insurance coverage for catheter ablation procedures, and the world’s most commercially active market for adopting and diffusing electrophysiology technology innovation across a broad network of academic, community, and freestanding cardiac care facilities.

The expanding U.S. ambulatory cardiac surgery centre channel for electrophysiology procedures, where appropriately selected catheter ablation cases are being shifted from hospital inpatient settings to lower-cost outpatient facilities whose procedure efficiency advantages and patient satisfaction outcomes are increasingly well documented, is creating both a commercial distribution shift opportunity for electrophysiology equipment companies whose ambulatory-optimised product configurations can address the specific operational requirements of this fast-growing delivery setting and a reimbursement policy pressure point for Medicare as payer organisations evaluate the cost-effectiveness of outpatient versus inpatient ablation reimbursement structures.

Electrophysiology Market Segment Analysis

-

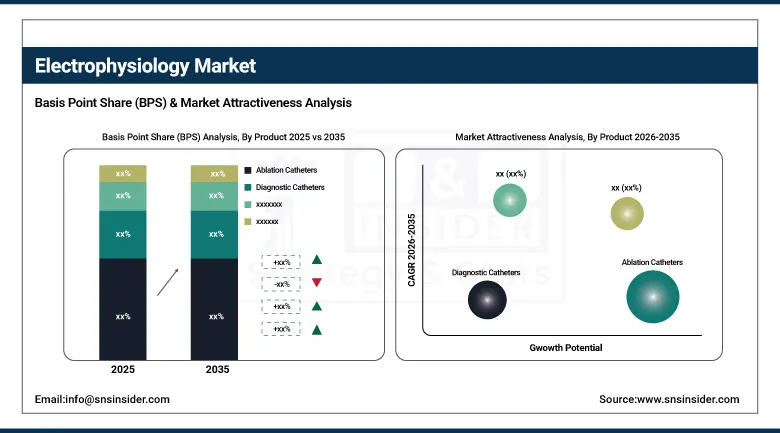

By Product, Ablation catheters dominated the electrophysiology market with approximately 46.82% revenue share in 2025, reflecting their essential role as the primary therapeutic instrument across all catheter ablation procedure categories and the continuous innovation investment that manufacturers including Abbott, Medtronic, Johnson & Johnson MedTech, and Boston Scientific are directing toward new energy delivery, sensing, and contact force capabilities; pulse field ablation systems are the fastest-growing product segment at a CAGR of approximately 17.64% through 2035, driven by the technology’s rapid clinical adoption following commercial launches across major markets.

-

By Technology, Radiofrequency ablation held the largest revenue share at approximately 48% in 2025, reflecting its status as the most widely established ablation energy modality with decades of clinical evidence, extensive operator training infrastructure, and broad indication coverage across atrial fibrillation, ventricular tachycardia, and supraventricular arrhythmia applications; pulse field ablation is the fastest-growing technology segment at the highest CAGR through 2035 driven by demonstrated clinical advantages over both radiofrequency and cryoablation in pulmonary vein isolation safety and efficiency.

-

By Application, Atrial fibrillation dominated the electrophysiology market with approximately 68.57% revenue share in 2025, reflecting its status as the world’s most common sustained cardiac arrhythmia with an estimated 33 to 44 million affected individuals globally and the primary procedure volume driver for catheter ablation across all geographic markets; atrial fibrillation is also the fastest-growing application at a CAGR of approximately 15.92%, driven by growing awareness of ablation’s clinical benefits, expanding patient eligibility criteria, and the development of more effective ablation strategies for persistent and long-standing persistent AF.

-

By End User, Inpatient facilities held the dominant share of approximately 54% in 2025, reflecting their historical role as the primary setting for complex cardiac electrophysiology procedures requiring overnight monitoring and the presence of cardiac surgical backup capability for the management of procedure complications; outpatient facilities are the fastest-growing end user segment at a CAGR of approximately 16.21% through 2035, driven by the demonstrated safety of catheter ablation in appropriately selected outpatient settings and the cost efficiency advantages of ambulatory cardiac procedure delivery relative to inpatient hospitalisation.

Ablation Catheters Lead Product Segment, PFA Grows Fastest

Ablation catheters retained the dominant product position of the electrophysiology market in 2025, a dominance rooted in the catheter ablation procedure’s status as the primary therapeutic intervention across the full spectrum of cardiac arrhythmia treatment indications that collectively define electrophysiology’s clinical and commercial footprint. The ablation catheter segment’s commercial scale reflects both the procedure volume growth that is expanding the total catheters consumed per annum and the progressive technology upgrade cycle that is increasing the average revenue per catheter as operators transition from standard irrigated radiofrequency catheters to advanced contact force-sensing catheters, high-density mapping-integrated catheters, and the new pulse field ablation catheter platforms whose higher per-unit prices reflect their differentiated energy delivery capabilities.

Pulse field ablation systems are the fastest-growing product segment at approximately 17.64% CAGR, as the technology’s demonstration of superior safety margins in pulmonary vein isolation relative to established thermal ablation modalities and its dramatically reduced procedure time versus cryoablation are driving clinical programme investment at a pace that has exceeded commercial launch projections across all major markets.

Atrial Fibrillation Dominates Application, Also Grows Fastest

Atrial fibrillation retained the dominant application position in 2025 and is simultaneously the fastest-growing application at approximately 15.92% CAGR, a dual commercial leadership reflecting both the extraordinary prevalence of AF as the world’s most common sustained cardiac arrhythmia and the progressive expansion of catheter ablation as the preferred treatment approach beyond its initial role as a last-resort rhythm control strategy toward a mainstream first-line or early rhythm control intervention whose clinical superiority over antiarrhythmic drug therapy for maintaining sinus rhythm is increasingly well documented in landmark randomised controlled trials including CABANA and EAST-AFNET 4 whose results are reshaping clinical practice guidelines across cardiology societies globally. Ventricular arrhythmia represents the most clinically complex and commercially valuable secondary application within the electrophysiology market, where catheter ablation of ventricular tachycardia in the context of structural heart disease and the treatment of premature ventricular complexes driving cardiomyopathy require the most advanced substrate mapping capabilities and ablation energy delivery precision that current three-dimensional mapping and ablation platforms at the frontier of the technology can provide.

Inpatient Facilities Dominate End User, Outpatient Grows Fastest

Inpatient facilities retained the dominant end user position within the electrophysiology market in 2025, reflecting the historical and ongoing clinical convention of performing catheter ablation procedures in hospital settings whose continuous cardiac monitoring capability, cardiac surgical backup availability, and intensive care infrastructure provide the safety margin that the cardiac electrophysiology community has considered appropriate for a procedural specialty where the potential for haemodynamic instability, cardiac perforation, and vascular complications, while low in experienced hands, is not negligible.

Outpatient facilities are the fastest-growing end user at approximately 16.21% CAGR through 2035, driven by the accumulating body of evidence demonstrating that appropriately selected patients undergoing catheter ablation for AF and supraventricular tachycardia can be safely managed in ambulatory surgical settings with same-day discharge, combined with the cost efficiency arguments that have motivated major U.S. health systems, payer organisations, and ambulatory cardiac care platform companies to invest in expanding outpatient electrophysiology laboratory infrastructure.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Electrophysiology Market Insights

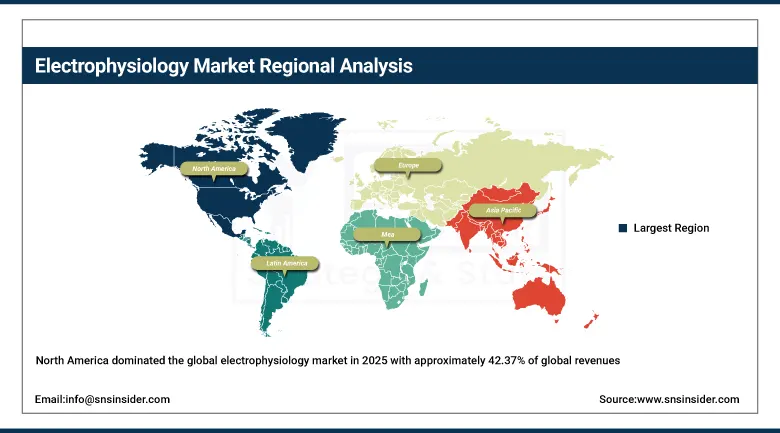

North America dominated the global electrophysiology market in 2025 with approximately 42.37% of global revenues, the United States accounting for approximately 87.4% of North American revenues, driven by the world’s highest per-capita concentration of trained cardiac electrophysiologists, the most extensive electrophysiology laboratory infrastructure, comprehensive Medicare and commercial insurance coverage for catheter ablation procedures, and the most commercially active environment for adopting electrophysiology technology innovations at rapid diffusion rates across both academic and community hospital programmes. Canada contributes approximately 12.6% of North American electrophysiology revenues through a publicly funded healthcare system with strong provincial coverage for catheter ablation procedures and a growing electrophysiology research community whose academic programmes contribute to the clinical evidence base supporting technology adoption decisions across Canadian cardiac centres.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Electrophysiology Market Insights

Europe is a technically sophisticated electrophysiology market characterised by the concentration of significant electrophysiology technology innovation at major European academic cardiac centres including the Bordeaux Heart Rhythm Hospital, Hôpital Laribôissière in Paris, the Heart Center Leipzig, and St. Mary’s Hospital London, whose world-renowned electrophysiology programmes generate the clinical trial evidence and technique development that accelerates technology adoption across European health systems whose national insurance coverage for catheter ablation provides accessible treatment pathways for AF and arrhythmia patients across the continent. Germany accounts for approximately 22.3% of European electrophysiology revenues as the region’s largest national market, with the highest per-capita number of electrophysiology procedures in Europe driven by a statutory health insurance system that provides comprehensive coverage for catheter ablation and a cardiac care infrastructure that has rapidly adopted pulse field ablation technology across leading German academic and community EP centres.

Asia Pacific Electrophysiology Market Insights

Asia Pacific is the fastest-growing regional electrophysiology market at a CAGR of approximately 14.44% through 2035, driven by the rapidly expanding cardiac care infrastructure investment across China, India, Japan, South Korea, and Southeast Asian markets that is enabling the equipment and specialist workforce deployment needed to address the extraordinary and growing burden of cardiac arrhythmia in populations whose ageing demographics, high hypertension prevalence, and rapidly changing lifestyles are creating cardiovascular disease epidemics of enormous clinical and commercial scale. China accounts for approximately 61.7% of Asia Pacific electrophysiology revenues and represents the most commercially consequential growth market in global cardiac electrophysiology, as the country’s combination of over 1.4 billion population with rapidly ageing demographic composition, high hypertension prevalence creating the AF risk environment, rapidly expanding hospital cardiac catheterisation laboratory infrastructure, and government healthcare reform investment in advanced cardiac care capability across tier-two and tier-three cities creates a procedure volume growth trajectory that is progressively making China one of the world’s most important electrophysiology markets by absolute procedural volume.

Latin America And MEA Electrophysiology Market Insights

Latin America and the Middle East and Africa are growing electrophysiology markets where expanding healthcare infrastructure investment, growing specialist cardiologist and electrophysiologist workforce capacity, and government cardiac care programme development are progressively improving access to catheter ablation procedures for patient populations whose cardiac arrhythmia burden is substantial but whose treatment rates have historically been far below those of developed markets due to limited EP laboratory infrastructure and specialist physician availability. Brazil accounts for approximately 44.2% of Latin American electrophysiology revenues through the combination of South America’s most extensive private and public hospital cardiac care network, a trained electrophysiology specialist community whose procedural volumes and technology adoption rates are approaching those of comparable-sized developed market programmes, and a growing medical device market whose domestic manufacturing and international import infrastructure enables the deployment of advanced mapping and ablation platforms across major Brazilian cardiac centres. Saudi Arabia leads Middle East and Africa at approximately 38.4% of the regional total, driven by Vision 2030’s healthcare quality improvement investment creating new cardiac centre infrastructure equipped with advanced electrophysiology mapping and ablation systems.

Market Dynamics

Growth Drivers: Rising global atrial fibrillation prevalence driven by ageing populations expanding the catheter ablation candidate pool, pulse field ablation technology adoption creating equipment upgrade investment cycle, and expanding electrophysiology laboratory infrastructure across Asia Pacific and emerging markets

The primary structural growth drivers for the electrophysiology market are the demographically inevitable expansion of the cardiac arrhythmia patient population as global ageing increases the prevalence of AF-predisposing conditions, creating a growing pipeline of ablation candidates that is supported by the progressive expansion of clinical guideline recommendations for catheter ablation as an earlier intervention than its historical position as a failed-antiarrhythmic-drug therapy warranted. The pulse field ablation technology’s commercial launch across major markets is simultaneously creating a capital equipment upgrade investment cycle of unusual magnitude as electrophysiology programmes invest in new ablation generator systems, proprietary catheter platforms, and associated mapping system upgrades to deploy the technology whose clinical safety advantages in pulmonary vein isolation are driving rapid adoption across programmes previously committed to established radiofrequency or cryoablation platforms.

Restraints: High cost of advanced electrophysiology mapping and ablation systems limiting adoption in budget-constrained markets, specialist electrophysiologist workforce shortage constraining procedure capacity expansion, and radiation exposure concerns creating safety management requirements

A significant restraint on the electrophysiology market is the substantial capital and operating cost of establishing and running a modern electrophysiology laboratory equipped with advanced three-dimensional mapping systems, fluoroscopy and intracardiac echocardiography imaging infrastructure, and the full complement of ablation catheter technologies that comprehensive EP programme capability requires, creating meaningful access barriers in healthcare systems where budget constraints, reimbursement levels, and capital allocation priorities limit investment in specialised cardiac procedure facilities.

Opportunities: Robotic catheter navigation enabling remote procedural access, AI-powered arrhythmia substrate analysis improving ablation success rates, and expanding AF ablation indication coverage creating new patient eligibility

The AI-powered cardiac mapping and ablation guidance opportunity represents the most immediately impactful technology frontier in electrophysiology, as machine learning algorithms trained on three-dimensional mapping datasets are progressively demonstrating the ability to identify optimal ablation target sites, predict lesion quality from catheter tip impedance and temperature parameters, and suggest procedural strategies for complex arrhythmia substrates that less experienced operators struggle to interpret from raw mapping data alone, potentially enabling the technology-assisted democratisation of complex ablation procedure capability beyond the handful of world-leading expert centres where current success rates are concentrated.

Recent Developments

-

2025: Abbott announced FDA clearance for its latest generation of ablation catheters in September 2025, designed to improve lesion precision and procedural efficiency in catheter ablation for atrial fibrillation, expanding Abbott’s ablation catheter portfolio in the world’s largest electrophysiology market as the company competes for market leadership in the rapidly growing pulse field ablation segment.

-

2025: Medtronic continued commercial expansion of its PulseSelect pulse field ablation system across U.S. and European electrophysiology programmes, building clinical adoption through structured training programmes, real-world evidence collection, and health economic outcome data generation that supports reimbursement pathway development across national health systems evaluating PFA technology coverage policies.

-

2025: Boston Scientific advanced commercial adoption of its FARAPULSE pulse field ablation system across international markets following FDA approval, establishing clinical training centres and procedural support infrastructure that enables electrophysiology programmes to implement the technology with adequate operator preparation and ongoing clinical support.

-

2025: LUMA Vision Ltd announced FDA clearance in April 2025 for its Verafeye Visualization Platform, a next-generation intracardiac imaging system providing enhanced real-time cardiac anatomical visualisation during electrophysiology procedures that improves catheter navigation precision and anatomical structure identification beyond the capability of existing intracardiac echocardiography platforms.

-

2025: Johnson & Johnson MedTech expanded its electrophysiology portfolio with new high-density mapping catheter configurations and biosense Webster mapping system software updates that improve the resolution and processing speed of real-time electroanatomical map generation for complex atrial and ventricular substrate characterisation procedures.

Electrophysiology Market Key Players

-

Abbott Laboratories

-

Medtronic plc

-

Johnson & Johnson MedTech (Biosense Webster)

-

Boston Scientific Corporation

-

Philips Healthcare

-

Siemens Healthineers AG

-

GE HealthCare

-

Biotronik SE & Co. KG

-

Microport Scientific Corporation

-

Acutus Medical Inc.

-

Farapulse Inc.

-

AtriCure Inc.

-

Stereotaxis Inc.

-

CONMED Corporation

-

MedyRytm SA

-

Cardioinsight Technologies

-

CardioFocus Inc.

-

Rhythmia Medical (Boston Scientific)

-

LUMA Vision Ltd

-

Varian Medical Systems (Siemens)

Electrophysiology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.89 Billion |

| Market Size by 2035 | USD 43.05 Billion |

| CAGR | CAGR of 12.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ablation Catheters, Diagnostic Catheters, Laboratory Devices, Access Devices, Others) • By Technology (Radiofrequency Ablation, Cryoablation, Laser Ablation, Microwave Ablation, Pulse Field Ablation) • By Application (Atrial Fibrillation, Ventricular Arrhythmia, Supraventricular Tachycardia, Others) • By End User (Inpatient Facilities, Outpatient Facilities) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Abbott Laboratories, Medtronic plc, Johnson & Johnson MedTech (Biosense Webster), Boston Scientific Corporation, Philips Healthcare, Siemens Healthineers AG, GE HealthCare, Biotronik SE & Co. KG, Microport Scientific Corporation, Acutus Medical Inc., Farapulse Inc., AtriCure Inc., Stereotaxis Inc., CONMED Corporation, MedyRytm SA, Cardioinsight Technologies. CardioFocus Inc., Rhythmia Medical (Boston Scientific), LUMA Vision Ltd, Varian Medical Systems (Siemens) |

Frequently Asked Questions

The electrophysiology market is expected to grow at a CAGR of 12.79% from 2026 to 2035.

The electrophysiology market was valued at USD 12.89 billion in 2025.

Rising global atrial fibrillation prevalence driven by demographic ageing and AF-predisposing comorbidities expanding the catheter ablation candidate pool.

Ablation catheters dominated with approximately 46.82% revenue share in 2025.

North America dominated the electrophysiology market in 2025, with the United States as the leading national market within the region.

Get in Touch