ELISpot and FluoroSpot Assay Market Report Scope & Overview:

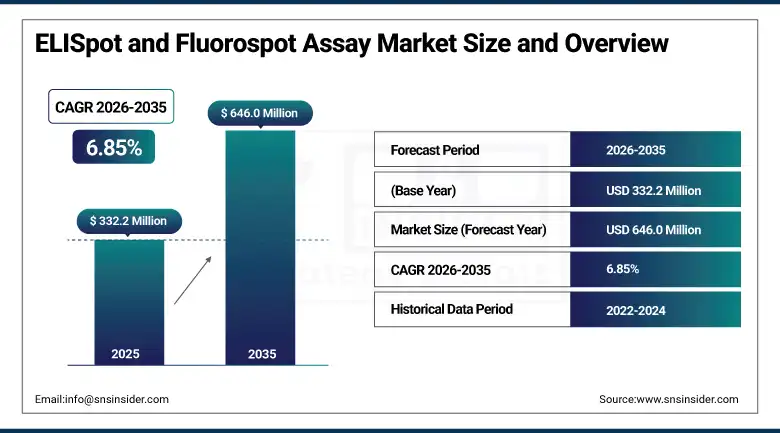

The ELISpot and FluoroSpot Assay Market was valued at USD 332.2 Million in 2025 and is expected to reach USD 646.0 Million by 2035, growing at a CAGR of 6.85% from 2026–2035.

The global ELISpot and FluoroSpot assay market is advancing as a cornerstone platform for single-cell-level immune response quantification whose unmatched sensitivity in detecting cytokine-secreting cells at frequencies as low as 1 in 300,000 makes it the preferred methodology for tuberculosis diagnostics, vaccine immunogenicity assessment, cancer immunotherapy monitoring, and autoimmune disease characterization. ELISpot’s enzyme-linked detection produces visible colored spots corresponding to individual cytokine-secreting cells, while FluoroSpot’s fluorescence-based multiplex extension enables simultaneous quantification of up to three cytokines per well from the same cell population. Rising global tuberculosis burden, accelerating immuno-oncology clinical trial activity, and the expansion of T-cell-based therapeutic development programmes collectively sustain above-average market growth.

In April 2024, U-CyTech Biosciences launched an enhanced FluoroSpot assay kit for simultaneous three-color IFN-γ, IL-2, and TNF-α detection from a single well, enabling comprehensive poly-functional T-cell characterization in vaccine immunogenicity and cancer immunotherapy clinical trials from a single assay setup. The product advancement addressed the growing demand from clinical trial sponsors for multiplexed cytokine profiling that characterizes the quality of T-cell responses beyond single-cytokine ELISpot quantification, providing richer immune response data within the same specimen and timeline constraints.

Market Size and Forecast

-

Market Size in 2026E: USD 354.9 Million

-

Market Size by 2035: USD 646.0 Million

-

CAGR: 6.85% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On ELISpot and Fluorospot Assay Market - Request Free Sample Report

ELISpot and FluoroSpot Assay Market Trends

-

FluoroSpot multiplex adoption is accelerating as clinical trial sponsors require simultaneous multi-cytokine profiling from single specimens to characterize T-cell poly-functionality comprehensively.

-

AI-powered automated spot counting systems are replacing manual microscopy reading, improving inter-laboratory consistency and reducing analysis time significantly.

-

High-throughput ELISpot automation is enabling 96-well plate processing at scales compatible with large clinical trial immunogenicity sample batches.

-

Immuno-oncology checkpoint inhibitor trial activity is generating growing demand for ELISpot tumour-infiltrating lymphocyte and neoantigen-specific T-cell monitoring.

-

Standardization initiatives including CIMT and Cancer Immunotherapy Trials Network protocols are improving ELISpot inter-laboratory reproducibility for regulatory submission.

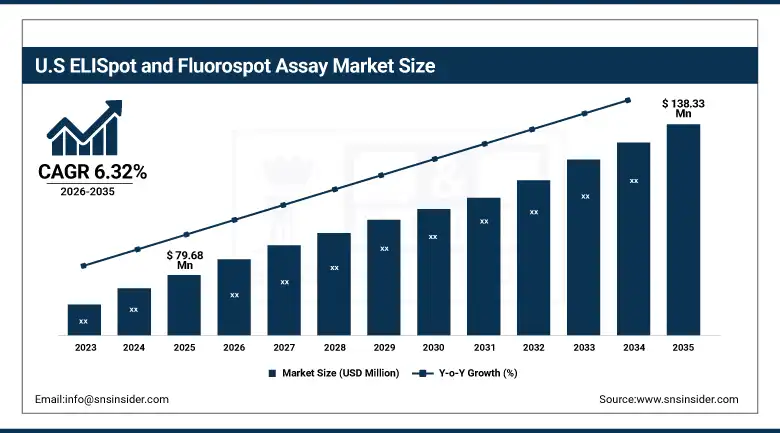

The U.S. ELISpot and FluoroSpot Assay Market Outlook

The U.S. ELISpot and FluoroSpot Assay Market was valued at approximately USD 79.68 Million in 2025 and is expected to reach approximately USD 138.33 Million by 2035, growing at a CAGR of approximately 6.32%.

The United States dominates North American revenues through its high government and private investment in immunology and infectious disease research, its concentration of immuno-oncology clinical trial activity, and its established tuberculosis latent infection diagnostic infrastructure using QuantiFERON-TB and T-SPOT.TB assays whose ELISpot-based technology sustains commercial demand. Becton Dickinson, Mabtech, and Oxford Immunotec maintain commercial leadership through U.S. FDA-cleared diagnostic product offerings and CRO service partnerships with major pharmaceutical sponsors.

In 2024, Becton Dickinson advanced its BD Horizon multiplex cytokine detection platform to include ELISpot-compatible workflow integration, enabling academic and pharmaceutical laboratory users to combine flow cytometry-based immune phenotyping with ELISpot functional T-cell quantification within a unified analytical framework. The integration addressed the growing immunology research demand for multiparameter immune profiling that characterises both the phenotype and functional cytokine secretion capacity of antigen-specific T-cell populations in vaccine and cancer immunotherapy studies.

ELISpot and FluoroSpot Assay Market Segment Analysis

-

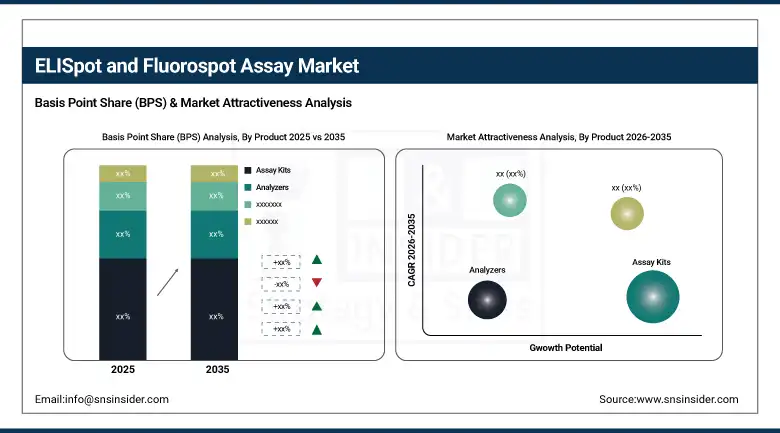

By Product, assay kits segment dominated the ELISpot and FluoroSpot assay market with approximately 49.6% share in 2025, while the analyzers segment is the fastest growing with a CAGR of approximately 8.4% driven by demand for automated high-throughput imaging.

-

By Assay Type, ELISpot Assay segment dominated the market with approximately 70.2% share in 2025, while the FluoroSpot assay segment is the fastest growing with a CAGR of approximately 9.1% driven by multiplex cytokine detection capability.

-

By Application, diagnostic applications segment dominated the ELISpot and FluoroSpot assay market with approximately 65.4% share in 2025, while the research applications segment is the fastest growing driven by immunological research, vaccine development, and cancer immunotherapy studies.

-

By End User, hospitals & clinical laboratories segment dominated the ELISpot and FluoroSpot assay market with approximately 47.3% share in 2025, while the pharmaceutical & biotechnology companies segment is the fastest growing with a CAGR of approximately 8.6%.

By Product, assay kits dominate, analyzers grow fastest

Assay kits retained the dominant product position with approximately 49.6% of the ELISpot and FluoroSpot assay market in 2025. Their commercial primacy reflects the recurring consumable procurement that each ELISpot and FluoroSpot instrument installation generates, where laboratories consume multiple assay kits per week across tuberculosis diagnostic testing, vaccine immunogenicity monitoring, and immunological research programmes whose test volumes create sustained annual reagent procurement that substantially exceeds the one-time instrument capital investment. The well-validated, pre-titrated antibody pairs and optimised protocol documentation that commercial assay kits provide relative to in-house reagent preparation create specification preference across clinical diagnostic laboratories whose regulatory compliance requirements demand lot-to-lot consistency documentation and technical support that DIY reagent combinations cannot match.

Analyzers are the fastest-growing product segment at approximately 8.4% CAGR because the progressive replacement of manual microscopy-based spot counting with automated imaging systems equipped with AI-powered spot recognition software eliminates the inter-reader variability, fatigue-related counting errors, and throughput limitations of manual reading that constrain ELISpot laboratory capacity expansion. Each automated ELISpot reader installation that replaces or supplements manual reading creates instrument procurement at USD 15,000 to USD 80,000 per system depending on throughput capacity, representing a commercial conversion from pure reagent purchasing to combined instrument and reagent revenue.

By Application, diagnostics dominate, research grows fastest

Diagnostic applications retained the dominant position with approximately 65.4% of the ELISpot and FluoroSpot assay market in 2025. The clinical diagnostic adoption of ELISpot technology is led by the T-SPOT.TB assay, Oxford Immunotec’s FDA-cleared tuberculosis diagnostic whose ELISpot format detects IFN-γ-secreting T-cells specific to Mycobacterium tuberculosis antigens, providing latent TB diagnosis with superior sensitivity and specificity relative to conventional tuberculin skin testing in immunocompromised patient populations. The T-SPOT.TB assay’s clinical utility across pre-employment screening, transplant recipient evaluation, immunotherapy initiation assessment, and outbreak investigation creates a large and recurring diagnostic test volume that sustains diagnostic application market leadership.

Research applications are the fastest-growing segment because the immuno-oncology field’s expansion of T-cell-based cancer immunotherapy, vaccine development, and cellular therapy characterization creates growing demand for ELISpot and FluoroSpot as the gold-standard T-cell functional assay for clinical trial immunological endpoints. Each immuno-oncology Phase II and III clinical trial that specifies ELISpot or FluoroSpot as a primary or secondary immunological endpoint creates reagent procurement across the centralized immunology laboratory supporting the study’s biomarker analysis programme, generating above-average per-study commercial value relative to standard diagnostic test volumes.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.0% |

|

Europe |

Germany |

24.7% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America ELISpot and FluoroSpot Assay Market Insights

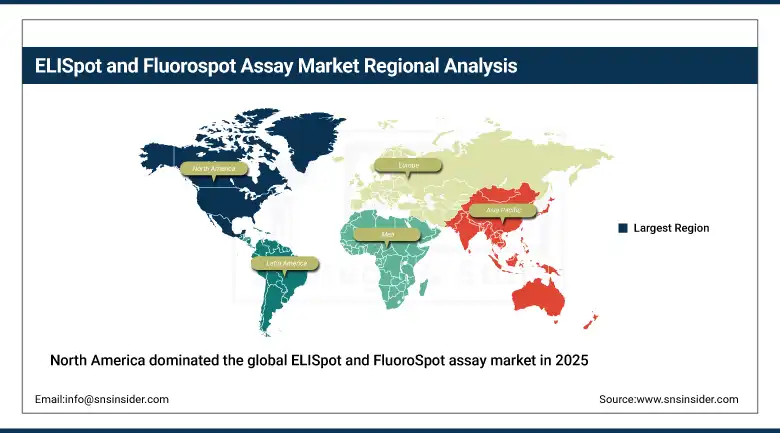

North America dominated the global ELISpot and FluoroSpot assay market in 2025 with a 36.25% share, driven by well-developed healthcare infrastructure, robust immunology research funding, and high adoption of precision diagnostic technologies. The United States accounts for approximately 83.0% of North American revenues through Oxford Immunotec’s T-SPOT.TB clinical diagnostic penetration, NIH and BARDA funding for vaccine immunogenicity research, and the concentration of immuno-oncology clinical trial activity at National Cancer Institute-designated comprehensive cancer centres.

Canada contributes supplementary North American revenues through its growing immunology research programme at university medical centres, the public health sector’s tuberculosis control programme’s ELISpot diagnostic adoption, and the pharmaceutical industry’s Vancouver and Toronto biotech cluster’s growing demand for FluoroSpot multiplex assays in vaccine immunogenicity and cellular therapy clinical trial programmes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe ELISpot and FluoroSpot Assay Market Insights

Europe is the world’s most technically advanced ELISpot and FluoroSpot assay market through its leadership in T-cell immunology research, the commercial origin of FluoroSpot technology at Mabtech’s Stockholm operations, and the German and Dutch infectious disease research networks whose tuberculosis and HIV immunology programmes create sustained assay consumption. Germany accounts for approximately 24.7% of European revenues through its large university hospital immunology research programmes, Robert Koch Institute’s tuberculosis epidemiology work, and Mabtech and AID Diagnostics’ domestic commercial presence.

The United Kingdom’s Oxford Immunotec established the ELISpot-based T-SPOT.TB commercial diagnostic market and its academic Jenner Institute and Wellcome Sanger Institute create sustained vaccine and infectious disease research demand. France’s Institut Pasteur network, the Netherlands’ Leiden University Medical Centre, and Switzerland’s Basel immunology research institutes collectively sustain European research application demand at levels that support commercial development of increasingly specialised FluoroSpot multiplex configurations.

Asia Pacific ELISpot and FluoroSpot Assay Market Insights

Asia Pacific is the fastest-growing regional ELISpot and FluoroSpot assay market, driven by the world’s highest tuberculosis burden concentrated in India, China, Indonesia, and the Philippines whose ELISpot-based TB diagnostic adoption for immunocompromised patient populations and healthcare worker screening creates growing clinical test volume. China accounts for approximately 38.5% of Asia Pacific revenues through its large hospital immunology laboratory network’s progressive ELISpot TB diagnostic adoption, growing immuno-oncology clinical trial infrastructure, and vaccine development programme’s immunogenicity monitoring requirements.

India represents the most commercially significant emerging market within Asia Pacific where the enormous latent TB patient population’s clinical management and healthcare worker screening programmes are creating growing clinical ELISpot diagnostic demand, and the growing pharmaceutical and biotech CRO sector’s immunogenicity testing capabilities are expanding research application procurement. Japan and South Korea contribute premium regional demand through their advanced immunology research programmes and growing cellular therapy clinical development activity.

MEA & Latin America ELISpot and FluoroSpot Assay Market Insights

The UAE leads MEA revenues at approximately 22.8% through its advanced hospital immunology laboratory infrastructure, the significant tuberculosis and infectious disease diagnostic testing demand of its large expatriate and migrant worker population, and the growing biomedical research investment at Abu Dhabi and Dubai academic medical centres. Saudi Arabia contributes growing regional demand through its pre-employment TB screening programme for its large migrant workforce and the King Abdullah International Medical Research Centre’s immunology research activities.

Brazil leads Latin American revenues at approximately 43.8% through its large tuberculosis burden creating clinical ELISpot diagnostic demand, the national oncology programme’s growing immuno-oncology clinical trial infrastructure, and the pharmaceutical sector’s Brazil-hosted clinical trial activity whose immunological monitoring programmes create research application ELISpot and FluoroSpot procurement. Mexico and Argentina contribute growing secondary demand through their infectious disease research programmes and expanding pharmaceutical CRO sectors.

Market Dynamics

Growth Drivers: Rising tuberculosis burden requiring sensitive cellular immunodiagnostics and expanding immuno-oncology clinical trial activity driving ELISpot research demand

The ELISpot and FluoroSpot assay market’s most structurally certain growth driver is the global tuberculosis control programme’s growing adoption of ELISpot-based interferon-gamma release assays as the preferred latent TB diagnostic for immunocompromised patient populations. The WHO’s End TB Strategy and national TB elimination programme investment create structured healthcare procurement for clinically validated ELISpot diagnostics whose sensitivity advantages over tuberculin skin testing in BCG-vaccinated and immunosuppressed populations create clinical guideline-driven adoption. Immuno-oncology’s parallel expansion creates research market growth as each new checkpoint inhibitor, CAR-T, and therapeutic vaccine clinical programme specifies ELISpot or FluoroSpot as a primary immunological endpoint whose measurement across trial participant time points generates substantial assay kit consumption.

Restraints: High assay technical complexity and standardization challenges limiting consistent inter-laboratory results for multi-site clinical trial use

ELISpot assay performance is highly sensitive to technical variables including plate coating antibody concentration, cell washing technique, incubation conditions, and spot counting methodology whose variation across laboratories creates inter-site result inconsistency that complicates multi-centre clinical trial immunological endpoint analysis. The requirement for fresh peripheral blood mononuclear cell isolation within four to eight hours of blood collection creates logistical constraints for clinical trial sites without on-site PBMC processing infrastructure, limiting ELISpot adoption to laboratories with cell processing capability and creating a specimen logistics barrier for decentralized trial designs. Standardization initiatives across the immunology research community address but have not fully resolved these consistency challenges across diverse laboratory environments.

Opportunities: Multiplex FluoroSpot development and digital ELISpot imaging AI integration creating premium analytical capability expanding commercial value

FluoroSpot multiplex technology whose simultaneous three-color cytokine detection from a single well enables poly-functional T-cell characterization that provides significantly richer immune response data than single-cytokine ELISpot measurement represents the most commercially valuable innovation frontier in the assay market. Each clinical trial or research programme that adopts FluoroSpot multiplex in preference to multiple parallel ELISpot single-cytokine assays generates higher per-sample commercial value through premium kit pricing that compensates for the reduced well count versus multiple single-cytokine assays. Digital ELISpot readers equipped with AI-powered spot morphology classification that distinguishes true cytokine secretion spots from artefactual background, identifies spot size and intensity profiles correlating with secretion magnitude, and automatically flags wells with quality concerns create a premium instrument market whose clinical trial regulatory compliance advantages sustain above-commodity pricing.

Recent Developments:

-

2025: BD announced the separation of its Biosciences and Diagnostic Solutions business to enhance strategic focus, repositioning its immunoassay product portfolio including ELISpot-compatible reagents and detection systems under dedicated diagnostic division management with dedicated commercial and development investment.

-

2024: U-CyTech Biosciences launched an enhanced three-colour FluoroSpot assay kit for simultaneous IFN-γ, IL-2, and TNF-α detection from a single well, enabling comprehensive polyfunctional T-cell characterisation in vaccine immunogenicity and cancer immunotherapy studies from a single assay setup.

-

2024: Mabtech AB introduced its IRIS FluoroSpot reader featuring AI-powered spot counting with morphological classification, reducing counting variability and improving detection sensitivity for low-frequency antigen-specific T-cells at the single-spot-per-well threshold that characterises highly specific cellular immune responses.

ELISpot and FluoroSpot Assay Market Key Players are:

-

Mabtech AB

-

Oxford Immunotec Ltd. (PerkinElmer)

-

Becton Dickinson and Company

-

U-CyTech Biosciences BV

-

AID Diagnostika GmbH

-

Bio-Techne Corporation (R&D Systems)

-

Thermo Fisher Scientific Inc.

-

Danaher Corporation (Cytovation)

-

Cellular Technology Limited (CTL)

-

ImmunoSpot (CTL Europe)

-

Lophius Biosciences GmbH

-

Euroimmun AG (Revvity)

-

Sartorius AG (Essen BioScience)

-

BMG Labtech GmbH

-

Biosite AB

-

BioLegend Inc. (PerkinElmer)

-

Lonza Group Ltd.

-

Meridian Bioscience Inc.

-

Cayman Chemical Company

-

Spring Bioscience Inc.

ELISpot and FluoroSpot Assay Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 332.2 Million |

| Market Size by 2035 | USD 646.0 Million |

| CAGR | CAGR of 6.85% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Assay Kits, Analyzers, Ancillary Products) • By Assay Type (ELISpot Assay, FluoroSpot Assay) • By Application (Diagnostic Applications, Research Applications) • By End User (Hospitals & Clinical Laboratories, Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Mabtech AB, Oxford Immunotec Ltd. (PerkinElmer), Becton Dickinson and Company, U-CyTech Biosciences BV, AID Diagnostika GmbH, Bio-Techne Corporation (R&D Systems), Thermo Fisher Scientific Inc., Danaher Corporation (Cytovation), Cellular Technology Limited (CTL), ImmunoSpot (CTL Europe), Lophius Biosciences GmbH, Euroimmun AG (Revvity), Sartorius AG (Essen BioScience), BMG Labtech GmbH, Biosite AB, BioLegend Inc. (PerkinElmer), Lonza Group Ltd., Meridian Bioscience Inc., Cayman Chemical Company, and Spring Bioscience Inc. |

Frequently Asked Questions

The ELISpot and FluoroSpot Assay Market is expected to grow at a CAGR of 6.85% from 2026 to 2035.

The ELISpot and FluoroSpot Assay Market was valued at USD 332.2 Million in 2025.

Rising global tuberculosis burden requiring ELISpot-based interferon-gamma release assays, expanding immuno-oncology clinical trial immunogenicity monitoring, and growing vaccine development programmes are the primary growth factors.

The Assay Kits segment dominated the market with approximately 49.6% share in 2025, while the Analyzers segment is the fastest growing with a CAGR of approximately 8.4%.

North America dominated the ELISpot and FluoroSpot Assay Market in 2025 with a 36.25% share, driven by robust healthcare infrastructure, immunology research funding, and high precision diagnostic adoption.

Get in Touch