Flight Management Systems Market Report Scope & Overview:

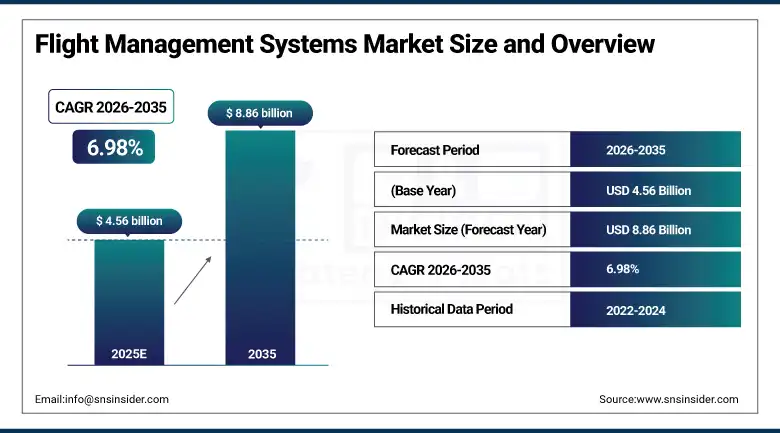

The Flight Management Systems (FMS) Market is valued at USD 4.56 billion in 2025 and is projected to reach around USD 8.86 billion by 2035, expanding at a CAGR of 6.98% during 2026–2035.

The Flight Management Systems (FMS) Market is witnessing steady expansion driven by the rapid modernization of global aviation fleets, increasing demand for fuel-efficient flight operations, and the growing integration of digital avionics systems across commercial and defense aircraft. Rising emphasis on automated flight planning, real-time navigation optimization, and reduction of pilot workload is accelerating the adoption of advanced FMS platforms, particularly AI-enabled and satellite-linked systems.

Additionally, Boeing’s 2025 Commercial Market Outlook projects the delivery of over 42,000 new commercial aircraft by 2043, which directly reinforces long-term demand for integrated flight management systems across global fleets.

In parallel, regulatory and technological advancements are accelerating innovation in avionics systems. In 2024, the U.S. Federal Aviation Administration (FAA) continued expanding approval pathways for next-generation integrated flight deck and avionics upgrades, supporting increased deployment of connected and software-defined flight management architectures across both commercial and defense aviation sectors, marking a clear shift toward highly automated, data-driven flight operations.

Flight Management Systems (FMS) Market Size and Forecast

-

Market Size in 2025: USD 4.56 Billion

-

Market Size by 2035: USD 8.86 Billion

-

CAGR: 6.98% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Flight Management Systems Market - Request Free Sample Report

Flight Management Systems Market Trends

-

Rising adoption of AI-enabled flight management systems is improving route optimization accuracy, fuel efficiency, and overall flight safety across commercial and defense aviation.

-

Increasing demand for fuel-efficient and eco-optimized flight operations is accelerating the deployment of advanced digital flight planning and performance management systems.

-

Rapid integration of satellite-based navigation (GNSS), real-time data links, and predictive analytics is enhancing situational awareness and reducing flight deviations.

-

Growing modernization of global aircraft fleets and avionics suites is boosting adoption of next-generation integrated and software-defined flight management systems.

-

Increasing retrofit programs across aging aircraft fleets are accelerating aftermarket demand for upgraded FMS platforms with enhanced automation capabilities.

-

Rising focus on autonomous aviation and reduced pilot workload is driving innovation in AI-assisted and highly automated flight management architectures.

-

Expanding use of cloud-connected avionics ecosystems and digital twin–based flight optimization is improving operational efficiency and maintenance forecasting.

U.S. Flight Management Systems (FMS) Market Size Outlook:

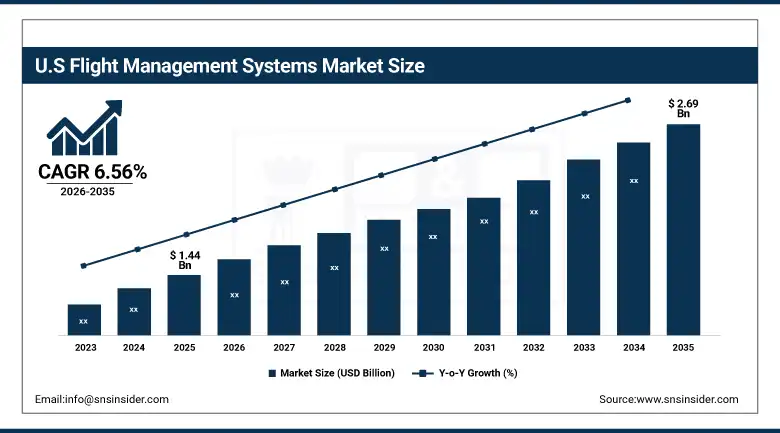

The U.S. Flight Management Systems (FMS) Market is estimated at USD 1.44 billion in 2025 and is projected to reach around USD 2.69 billion by 2035, growing at a CAGR of 6.56% from 2026–2035. The U.S. Flight Management Systems Market remains the global leader, backed by its very advanced aviation eco-system, the dominance of major avionics manufacturers such as Honeywell Aerospace, Collins Aerospace (RTX Corporation), Boeing Digital Aviation, Garmin, and high adoption of cutting-edge flight deck solutions in commercial as well as defense aviation. Regular upgrading of airframe fleet, combined with robust avionics upgrades driven by FAA support and performance-based navigation (PBN) systems is one of the key factors fuelling the demand for FMS solutions.

Supporting this trend, the Federal Aviation Administration (FAA) has been actively advancing initiatives such as NextGen air traffic modernization programs, which emphasize satellite-based navigation, data-linked flight operations, and enhanced automation in flight planning systems to improve airspace efficiency and safety.

In addition, Boeing’s 2025 Commercial Market Outlook highlights that North America will continue to account for a significant share of global aircraft deliveries, reinforcing sustained demand for integrated and AI-enabled flight management systems across both commercial and defense aviation segments.

Flight Management Systems Market Segment Highlights

• By Component, Flight Management Computers (FMC) dominated the Flight Management Systems Market with 34.36% share in 2025; Software Systems are the fastest growing segment

• By Aircraft Type, Commercial Aircraft dominated the Flight Management Systems Market with 57.45% share in 2025; Military Aircraft are the fastest growing segment

• By Fit Type, Line Fit (OEM-installed) dominated the Flight Management Systems Market with 62.85% share in 2025; Retrofit (Aftermarket) is the fastest growing segment

• By Technology, Conventional FMS dominated the Flight Management Systems Market with 41.24% share in 2025; GPS-enabled / Satellite-based FMSis the fastest growing segment.

• By Application, Navigation & Route Optimization dominated the Flight Management Systems Market with 38.51% share in 2025; Mission Planning (Defense UAVs & Military aircraft) is the fastest growing segment

By Component, Flight Management Computers (FMC) segment dominates the Flight Management Systems Market, Software Systems segment expected to grow fastest

In 2025, the Flight Management Computers (FMC) segment maintained its dominant position in the Flight Management Systems Market, accounting for 34.36% of total revenue. This dominance is primarily attributed to its critical role as the core processing unit of all flight planning, navigation, and performance optimization functions across commercial and defense aircraft.

The Software Systems segment is projected to record the highest CAGR during the 2026–2035 forecast period. This growth is driven by the rapid transition toward AI-enabled flight optimization, predictive routing, and cloud-connected avionics ecosystems.

By Aircraft Type, Commercial Aircraft segment dominates the Flight Management Systems Market, Military Aircraft segment expected to grow fastest

The Commercial Aircraft segment held the largest share of 57.45% in the Flight Management Systems Market in 2025, The growth is driven by the large global aircraft fleet, high aircraft deliveries, and wide use of sophisticated navigation and fuel management systems. Fleet replacement activities by leading airlines and Original Equipment Manufacturers (OEMs), including Boeing and Airbus, and the emphasis on efficiency have solidified the position of this sector in global aviation systems.

The Military Aircraft segment is expected to register the highest CAGR during the 2026–2035 forecast period. Growth is fueled by rising defense modernization programs, increased investment in next-generation combat aircraft, and integration of advanced mission planning and autonomous navigation capabilities.

By Fit Type, Line Fit (OEM-installed) segment dominates the Flight Management Systems Market, Retrofit (Aftermarket) segment expected to grow fastest

The Line Fit (OEM-installed) segment maintained the highest market share of 62.85% in 2025, backed up by robust incorporation of Flight Management Systems in the process of assembling new airplanes by OEMs. This domination has been achieved owing to the long-term supply contracts signed between avionics companies and airplane manufacturers for the installation of advanced FMS systems in new generation airplanes.

The Retrofit (Aftermarket) segment is projected to witness the highest CAGR during 2026–2035, motivated by rising fleet modernization efforts and mandatory improvements to the avionics on planes. Airlines have been working to install more sophisticated FMS on their old planes, in an effort to reduce fuel consumption, integrate into the increasingly complex air traffic control systems, and prolong the lifespan of their planes.

By Technology, Conventional FMS dominated the Flight Management Systems Market with; GPS-enabled / Satellite-based FMS is the fastest growing segment.

The Conventional FMS segment maintained the highest market share of 41.24% in 2025, given its extensive installation on existing aircraft, high reliability, and ongoing incorporation within certified avionics systems. The extensive installed base in both civilian and military aviation will ensure its continued utility, especially in mid-life aircraft that have few opportunities for complete avionics system upgrades.

The GPS-enabled / Satellite-based FMS segment is projected to register the highest CAGR during the 2026–2035 forecast period,

By Application, Navigation & Route Optimization dominated the Flight Management Systems Market; Mission Planning (Defense UAVs & Military Aircraft) is the fastest growing segment.

The Navigation & Route Optimization segment maintained the highest market share of 38.51% in 2025, due to its primary role in helping perform effective flight-path planning, fuel management, and maintaining adherence to worldwide aviation regulations. It is still one of the basic software applications used by all types of airplanes, and it is widely used by commercial airlines for cutting costs.

The Mission Planning (Defense UAVs & Military Aircraft) segment is expected to register the highest CAGR during the 2026–2035 forecast period.

Flight Management Systems Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

35.43% |

|

Europe |

Germany |

25.14% |

|

Asia Pacific |

China |

22.75% |

|

Middle East & Africa |

UAE |

9.04% |

|

Latin America |

Brazil |

7.64% |

North America Flight Management Systems Market Insights

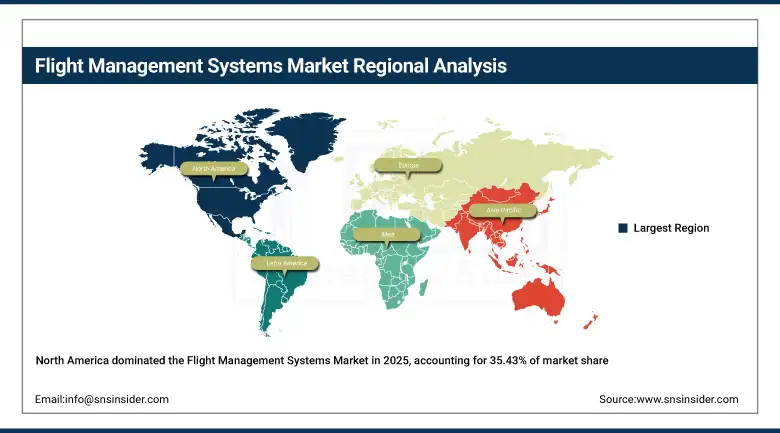

The North America region has taken the lead position in the global Flight Management System market in 2025 with a revenue share of 35.43%, owing to its high levels of development in the aviation sector, presence of major players, and adoption of future generation flight deck solutions. In the North American region, the United States is performing exceptionally well in terms of performance with a share of within the region.

Supporting this dominance, the Federal Aviation Administration (FAA) continues to advance its NextGen Air Transportation System modernization program, which emphasizes performance-based navigation (PBN), satellite-based flight operations, and real-time data connectivity to improve airspace efficiency and reduce operational delays.

In addition, major U.S. airline groups such as Delta Air Lines and United Airlines have accelerated fleet-wide avionics upgrades, integrating AI-enabled flight optimization and fuel efficiency systems into modern cockpit architectures, reinforcing North America’s position as the global innovation hub for advanced Flight Management Systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Flight Management Systems Market Insights

The Asia Pacific region is estimated to have the highest CAGR of 8.07% between 2026 and 2035 due to fast growth in commercial aviation fleet sizes, delivery of aircraft, and robust development of aviation infrastructure. Countries like China, India, Japan, South Korea, and those from Southeast Asia will lead the growth. China alone makes up demand in the Asia Pacific region owing to its aircraft purchasing initiatives.

Supporting this growth, the Civil Aviation Administration of China (CAAC) has been actively promoting the integration of advanced navigation and satellite-based flight management systems as part of its airspace modernization initiatives. Similarly, India’s DGCA (Directorate General of Civil Aviation) has emphasized modernization of avionics standards in line with global performance-based navigation frameworks, encouraging widespread adoption of digital FMS platforms in both commercial and regional aviation.

Furthermore, rapid expansion of low-cost carriers and increasing domestic air traffic across the region are accelerating demand for fuel-efficient and AI-enabled flight optimization systems.

Europe Flight Management Systems Market Insights

Europe held the second-largest revenue share in the global Flight Management Systems Market, accounting for 25.14% in 2025, supported by strong aerospace manufacturing capabilities, advanced air traffic management infrastructure, and strict regulatory frameworks for aviation safety and efficiency. Key contributors include Germany, France, the United Kingdom, and Spain, which collectively host major avionics OEMs and aircraft manufacturers.

Supporting this position, the European Union Aviation Safety Agency (EASA) has been actively promoting the adoption of advanced satellite-based navigation systems and standardized digital avionics integration across European airspace under its Single European Sky initiative.

In addition, Airbus continues to integrate next-generation flight management technologies, including predictive trajectory optimization and cloud-connected avionics architectures, across its A320 and A350 aircraft families, reinforcing Europe’s strong position in advanced FMS development and deployment.

Middle East & Africa and Latin America Flight Management Systems Market Insights

The MEA and Latin America markets are experiencing consistent growth in the Flight Management System market due to the development of airlines, investments in airport infrastructure, and the integration of avionics technology. The MEA region, for instance, is dominated by the United Arab Emirates, Saudi Arabia, and Qatar, which have emerged as world aviation centers with massive airline expansions.

Supporting this trend, the General Civil Aviation Authority (GCAA) of the UAE and Saudi Arabia’s General Authority of Civil Aviation (GACA) have accelerated digital airspace transformation initiatives, promoting adoption of satellite-based navigation and advanced flight optimization systems as part of national aviation modernization strategies.

In Latin America, Brazil and Mexico are key markets, with aviation authorities such as Brazil’s ANAC (Agência Nacional de Aviação Civil) supporting gradual modernization of airline fleets and increasing integration of upgraded avionics systems to improve operational efficiency and safety across regional and domestic carriers.

Flight Management Systems Market Growth Drivers:

-

Rising global demand for fuel-efficient, automated, and safety-enhancing flight operations is accelerating widespread adoption of advanced Flight Management Systems across commercial and defense aviation fleets

The key factor behind the transformation of aircraft navigation from manual and semiautomated to fully integrated, data-based flight management system architecture is the strongest force shaping the FMS industry. In this context, both commercial and defense enterprises have been showing an increasing preference towards FMS solutions that would provide them with better flight paths, lower fuel costs, timely delivery, and better situation awareness among others. In addition, the growing density of air traffic, increased cost constraints for commercial aviation companies, and new international regulatory requirements necessitate such FMS systems.

In parallel, the Boeing Commercial Market Outlook (2025) forecasts demand for more than 42,000 new commercial aircraft by 2043, directly reinforcing long-term integration of next-generation flight management systems across new aircraft deliveries and retrofit programs.

Additionally, the Federal Aviation Administration (FAA) continues to expand its NextGen modernization program, emphasizing satellite-based navigation, real-time data exchange, and trajectory-based operations, which are significantly increasing adoption of AI-enabled and GPS-integrated FMS platforms across U.S. and global airspace systems.

Flight Management Systems Market Restraints:

-

High acquisition costs, complex integration requirements, and long upgrade cycles of advanced avionics systems are limiting rapid adoption of next-generation Flight Management Systems, particularly among smaller airlines and cost-sensitive operators

The major financial and logistical constraints involved in implementing state-of-the-art Flight Management Systems form a crucial limiting factor for growth within the market, particularly for regional, freight, and military airlines in developing nations. Contemporary Flight Management Systems, especially those that are AI-driven, utilize satellite technology, and incorporate software-defined approaches, necessitate considerable initial capital expenditures, coupled with costly avionics integration procedures, certification protocols, and pilot training initiatives. Moreover, older aircraft may need extensive cockpit modifications to interface with new Flight Management Systems technology.

Flight Management Systems Market Opportunities:

-

Rapid evolution of autonomous flight optimization, AI-driven cockpit intelligence, and cloud-connected avionics ecosystems is creating significant growth opportunities for next-generation Flight Management Systems across global aviation networks

The biggest game-changing opportunity in the Flight Management Systems Market involves moving toward complete intelligence, prediction, and connectivity in flight management, where artificial intelligence and machine learning can optimize flights. The current generation of FMS systems is able to alter flight routes depending on varying weather conditions, congested airspace, fuel savings, and other factors, making airlines more profitable. This revolution is also paving the way for “software-defined avionics,” where the flight management system can be updated without having to replace the entire hardware.

Recent Developments:

-

2026: Honeywell Aerospace expanded its next-generation Primus Epic and Forge avionics ecosystem with enhanced AI-enabled Flight Management System (FMS) capabilities, focusing on predictive flight path optimization, real-time weather integration, and cloud-connected operational data sharing across commercial airline fleets in North America and Asia-Pacific.

-

2026: RTX Corporation (Collins Aerospace) advanced its Pro Line Fusion and integrated FMS suite with expanded satellite-based navigation capabilities and improved trajectory-based operations (TBO) compatibility, supporting next-generation air traffic management standards. The system saw increased deployment across business aviation and military platforms, particularly in upgraded cockpit retrofits and new aircraft deliveries in the U.S. and Europe.

-

2025: Thales Group enhanced its TopFlight Flight Management System portfolio with upgraded GNSS resilience, cybersecurity hardening, and AI-assisted flight optimization modules designed to improve operational reliability in congested airspace environments.

-

2024: Garmin Ltd. expanded certification of its G3000 PRIME and advanced integrated flight deck systems with improved FMS functionality for business jets and regional aircraft, incorporating enhanced automation, synthetic vision integration, and real-time performance optimization tools.

Flight Management Systems Companies are:

-

Honeywell Aerospace

-

RTX Corporation (Collins Aerospace)

-

Thales Group

-

Boeing Digital Aviation (Jeppesen)

-

Airbus (Navblue)

-

Safran Electronics & Defense

-

L3Harris Technologies

-

BAE Systems plc

-

Leonardo S.p.A.

-

Elbit Systems (Universal Avionics)

-

Indra Sistemas S.A.

-

Curtiss-Wright Corporation

-

Astronics Corporation

-

TransDigm Group (Esterline Avionics)

-

Northrop Grumman Corporation

-

SITA

-

Lufthansa Systems (Lido FMS)

-

GE Aerospace

-

Cobham Aerospace Communications

Flight Management Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.56 Billion |

| Market Size by 2035 | USD 8.86 Billion |

| CAGR | CAGR of 6.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Flight Management Computers (FMC), Control Display Units (CDU), Navigation Databases, Software Systems, Others) • By Aircraft Type (Commercial Aircraft, Business Jets, Military Aircraft, Helicopters, UAVs / Drones, Others) • By Fit Type (Line Fit (OEM-installed), Retrofit (Aftermarket)) • By Technology (Conventional FMS, Integrated Modular Avionics (IMA)-based FMS, GPS/Satellite-enabled FMS, AI-assisted / Next-gen FMS) • By Application (Navigation & Route Optimization, Flight Performance Management, Fuel Efficiency Optimization, Air Traffic Management Compliance, Mission Planning (Defense UAVs & Military Aircraft)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell Aerospace, RTX Corporation (Collins Aerospace), Thales Group, Garmin Ltd., Boeing Digital Aviation (Jeppesen), Airbus (Navblue), Safran Electronics & Defense, L3Harris Technologies, BAE Systems plc, Leonardo S.p.A., Elbit Systems (Universal Avionics), Indra Sistemas S.A., Curtiss-Wright Corporation, Astronics Corporation, TransDigm Group (Esterline Avionics), Northrop Grumman Corporation, SITA, Lufthansa Systems (Lido FMS), GE Aerospace, Cobham Aerospace Communications. |

Frequently Asked Questions

The Flight Management Systems Market is expected to grow at a CAGR of 6.98% from 2026 to 2035.

The Flight Management Systems Market was valued at USD 4.56 billion in 2025.

Rising demand for fuel-efficient, automated, and safety-enhancing flight operations, coupled with increasing adoption of AI-enabled navigation and real-time optimization systems across commercial and defense aviation, is the primary growth driver of the Flight Management Systems Market.

The Flight Management Computers (FMC) segment dominated the Flight Management Systems Market in 2025.

North America dominated the Flight Management Systems Market in 2025.

Get in Touch