Freighter Aircraft Market Report Scope & Overview:

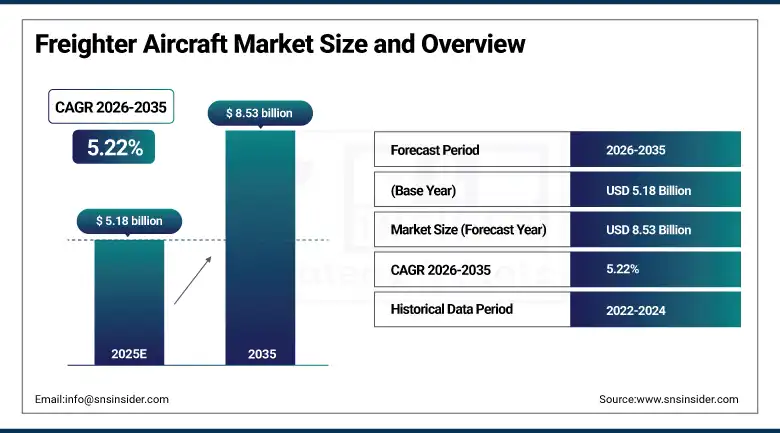

The Freighter Aircraft Market was valued at USD 5.18 billion in 2025 and is expected to reach USD 8.53 billion by 2035, growing at a CAGR of 5.22% from 2026-2035.

The Freighter Aircraft Market is forecasted to grow at a constant rate during 2026–2035 due to the growing adoption of e-commerce across the globe, increasing requirement of P2F conversion, expanding cold chain transportation of pharmaceuticals & perishables, growing cross border trade, and preference for wide body aircraft. Being the largest shareholder, North America is expected to continue dominating the market, while Asia-Pacific will become the fastest-growing region in terms of CAGR over the forecast period.

Supporting this trend, the International Air Transport Association (IATA) reported that global air cargo demand grew 10.8% year-on-year in February 2025, marking the strongest growth since mid-2021. Boeing also announced in 2025 that it expects demand for 2,800 new and converted freighters by 2042, underscoring long-term fleet expansion needs.

In addition, Airbus has been actively expanding its freighter portfolio. In July 2023, Airbus launched the A350F program, securing orders from CMA CGM Air Cargo and Air France-KLM, exemplifying the industry’s commitment to next-generation, fuel-efficient wide-body freighters.

Freighter Aircraft Market Size and Forecast

-

Market Size in 2025: USD 5.18 Billion

-

Market Size by 2035: USD 8.53 Billion

-

CAGR: 5.22% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Freighter Aircraft Market - Request Free Sample Report

Freighter Aircraft Market Trends

-

E-commerce boom is the single largest driver, with Amazon, Alibaba, and other platforms fueling demand for dedicated freighters.

-

Passenger-to-Freighter (P2F) conversions dominate, offering cost-effective fleet expansion and accounting for over half of new freighter supply.

-

Cold chain logistics is expanding rapidly, driven by pharmaceuticals, biologics, and perishables.

-

Fleet modernization is accelerating, with airlines replacing aging aircraft with fuel-efficient wide-body freighters like Boeing 777F and Airbus A350F.

-

OEM innovation continues, with Airbus launching the A350F and Boeing projecting demand for 2,800 freighters by 2042.

-

Express parcel and courier services (FedEx, UPS, DHL) are expanding fleets to meet rising same-day and next-day delivery expectations.

-

Sustainability pressures are pushing manufacturers toward lower-emission engines and lightweight designs.

-

Infrastructure growth in emerging markets (India, Middle East, Africa) is enabling regional freighter demand.

-

Strategic alliances between OEMs, conversion firms, and logistics operators are reshaping competitive dynamics.

U.S. Freighter Aircraft Market Size Outlook:

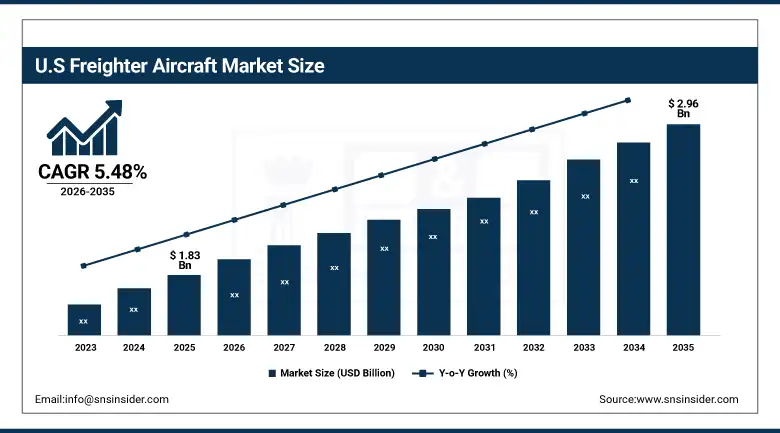

The U.S. Freighter Aircraft Market was valued at USD 1.83 billion in 2025 and is expected to reach USD 2.96 billion by 2035, growing at a CAGR of 5.48% from 2026-2035. The U.S. Market is anticipated to witness steady growth in the period from 2026 to 2035, backed by rising e-commerce shipments, growth in express delivery operations, and increasing P2F conversions. The United States market will continue to dominate North America, thanks to the efforts made towards fleet renewal by FedEx, UPS, and Amazon Air. Cold chain logistics, primarily pharmaceuticals and perishable cargo, will ensure steady CAGR growth over the forecast period.

Supporting this trend, the International Air Transport Association (IATA) reported that U.S. air cargo demand rose 8.6% year-on-year in February 2025, reflecting strong momentum in e-commerce and express logistics. Boeing further projected that North America will require 920 new and converted freighters by 2042, underscoring the region’s long-term fleet expansion needs.

In addition, major U.S. operators have been actively expanding fleets. In 2025, Amazon Air added converted Boeing 767 freighters, while FedEx and UPS announced modernization programs to replace aging aircraft with more fuel-efficient wide-body freighters.

Freighter Aircraft Market Segment Highlights

-

By Freighter Type, Passenger-to-Freighter (P2F) Converted Aircraft dominated the Freighter Aircraft Market with 46.28% share in 2025; and it also has fastest growing (CAGR).

-

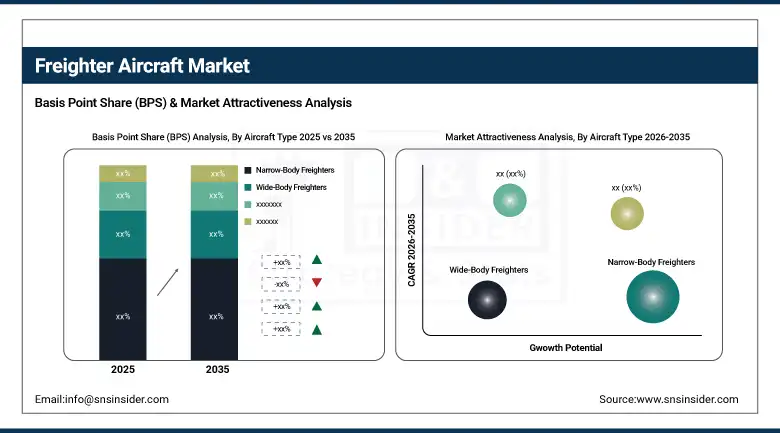

By Aircraft Type, Narrow-Body Freighters dominated the Freighter Aircraft Market with 39.53% share in 2025; Wide-Body Freighters fastest growing (CAGR).

-

By Engine Type, Turbofan dominated the Freighter Aircraft Market with 64.77% share in 2025; and it also has fastest growing (CAGR).

-

By Application, Commercial Cargo dominated the Freighter Aircraft Market with 69.68% share in 2025; E-commerce Logistics fastest growing (CAGR).

-

By Payload Capacity, Large (>80 tonnes) dominated the Freighter Aircraft Market with 39.53% share in 2025; it has also fastest growing (CAGR).

By Freighter Type, Passenger-to-Freighter (P2F) Converted Aircraft segment dominates the Freighter Aircraft Market, and is also expected to grow the fastest

The Passenger-to-Freighter (P2F) Converted Aircraft category will continue to dominate the market which is 46.28% share, owing to its cost effectiveness and quicker availability than a brand-new freighter aircraft. It consists of passenger aircraft that have been converted into cargo planes, allowing operators to expand rapidly. There has been a massive increase in conversions due to the strong demand from e-commerce logistics, express delivery and regional freight applications.

Passenger-to-Freighter (P2F) category will also experience the highest growth rates in the market, attributed to growing demand for air cargo shipments across the globe. Aging passenger aircraft that can be converted for use in air cargo shipping will contribute to higher growth rates in the coming years.

By Aircraft Type, Narrow-Body Freighters segment dominates the Freighter Aircraft Market, while Wide-Body Freighters are expected to grow the fastest

The Narrow-Body Freighters market segment continues to hold the lead in the Freighter Aircraft Market with 39.53% market share, mainly owing to its frequent utilization for short and regional freight operations. Such aircraft are commonly employed for e-commerce deliveries due to their operational flexibility, cost-effectiveness, and suitability for frequent flights. The capability of these aircraft to connect secondary destinations enhances their penetration in the market.

The Wide-Body Freighters market segment is anticipated to record the fastest growth, driven by growing demand for long-haul cargo services and rising volume of global shipments. The ability of these aircraft to carry larger payloads, increased range, and efficiency in intercontinental transportation of bulk cargo makes them highly sought after in the Freighter Aircraft Market.

By Engine Type, Turbofan segment dominates the Freighter Aircraft Market and is also expected to grow the fastest

The Turbofan segment commands dominance within the Freighter Aircraft Market with 64.77% share in market due to their extensive application in narrow and wide-body freighters for long-range transportation. Their benefits include high thrust and enhanced efficiency when it comes to large aircrafts and efficient performance over long distances. Their dependability and capacity to carry heavy cargo load makes them the choice of many commercial operators.

Looking forward, the Turbofan segment is also expected to grow at the fastest pace, supported by advancements in engine technology, fuel efficiency improvements, and increasing demand for long-haul cargo transportation. Continuous innovation in engine design and sustainability initiatives is further driving adoption across modern freighter fleets.

By Application, Commercial Cargo segment dominates the Freighter Aircraft Market

The Commercial Cargo segment dominates the Freighter Aircraft Market with 69.68% share in market, driven by strong demand from global trade, manufacturing supply chains, and logistics providers. This segment includes transportation of general cargo, industrial goods, pharmaceuticals, and perishable items across domestic and international routes. The expansion of global supply chains and increasing reliance on air freight for time-sensitive shipments continue to support its leadership.

By Payload Capacity, Large (>80 tonnes) segment dominates the Freighter Aircraft Market

The Large Payload (>80 tonnes) segment maintains its dominant position in the Freighter Aircraft Market with 39.48% share, driven by its critical role in long-haul cargo transportation and bulk freight movement. These aircraft are widely used for transporting heavy industrial goods, machinery, and high-volume shipments across international markets. Their ability to maximize cargo capacity and optimize cost per unit makes them highly valuable for major cargo operators.

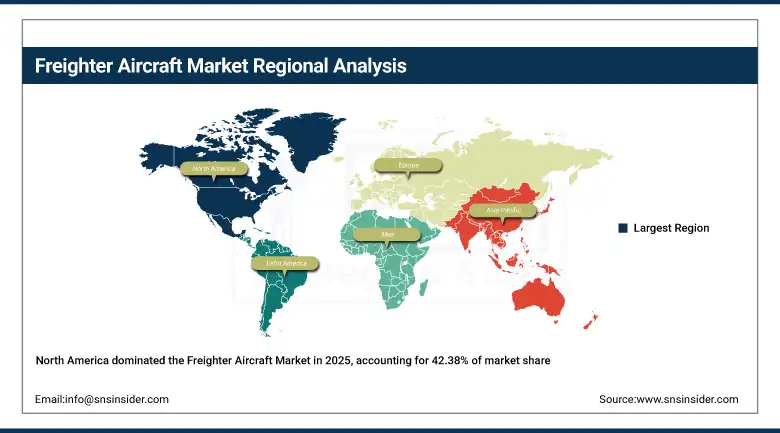

Freighter Aircraft Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

42.38% |

|

Europe |

Germany |

20.17% |

|

Asia Pacific |

China |

26.59% |

|

Middle East & Africa |

UAE |

6.11% |

|

Latin America |

Brazil |

4.75% |

North America Freighter Aircraft Market Insights

North America is at the forefront of this market with a 42.38% market share in the global Freighter Aircraft Market, thanks to its advanced air cargo network, prominent freighters’ presence, and efficient logistics system. This is bolstered by the region’s high adoption rate of passenger-to-cargo conversion aircraft, frequent upgrading of its fleet, and rising demand for e-commerce and express cargo services. The United States is leading regional growth with the likes of FedEx, UPS, and Amazon Air as its key players.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, North America continues to witness strong momentum in air cargo demand and freighter fleet expansion. According to industry data, air cargo transports over USD 6 trillion worth of goods annually, representing nearly 35% of global trade by value, with North America playing a central role in high-value shipments.

Additionally, major operators such as FedEx and UPS are advancing automation and network optimization strategies, while maintaining strong revenue outlooks despite fuel cost pressures, reflecting the resilience and scale of North America’s cargo aviation ecosystem.

Asia Pacific Freighter Aircraft Market Insights

The Asia-Pacific region is currently the most rapidly developing region, with a Compound Annual Growth Rate (CAGR) of 6.14%, driven by the high pace of industrialization, export-driven economies, and international business activities. The market is fueled by the growth of demand for air freight in China, India, and Southeast Asia, as well as investments in infrastructure development at airports and the development of cargo fleets. China outperforms other regional players owing to its supremacy in the manufacturing industry and a highly developed logistics environment for e-commerce businesses.

Supporting this growth, Asia-Pacific is expected to account for siginificant of incremental global freighter aircraft demand over the next decade, significantly contributing to overall fleet expansion. The region handles a substantial portion of global air cargo, with Asia-Pacific airlines carrying nearly 40% of total international air freight volumes. Rising cargo volumes linked to e-commerce exports have driven double-digit growth rates of 10%–15% in air cargo demand across key markets such as China and Southeast Asia.

Europe Freighter Aircraft Market Insights

Europe is the second-largest region for the global Freighter Aircraft Market on account of its extensive air cargo infrastructure, robust intra-trade activities, and highly developed logistic systems. Major cargo centers in the region include nations such as Germany, UK, France, and Netherlands, while the major airports include Frankfurt Airport, Paris Charles de Gaulle Airport, and Amsterdam Schipol Airport. High usage of wide body freighters and passenger-to-freighter conversion aircraft in Europe further enhance its market share.

Supporting this position, the European Union continues to invest heavily in transport and logistics infrastructure through initiatives such as the Trans-European Transport Network (TEN-T), aimed at improving cross-border connectivity and freight efficiency. Additionally, rising demand for time-sensitive cargo, including pharmaceuticals and high-value goods, is strengthening the role of air freight across the region.

In addition, regulatory frameworks focused on sustainability, including the EU Emissions Trading System (EU ETS) and “Fit for 55” initiatives, are encouraging fleet modernization and adoption of fuel-efficient freighter aircraft, reinforcing Europe’s steady growth trajectory in the global freighter aircraft market.

Middle East & Africa and Latin America Freighter Aircraft Market Insights

The Middle East & Africa is an emerging market for the Freighter Aircraft Market, considering the favorable geographical positioning of the region as it links Asia, Europe, and Africa. The countries such as United Arab Emirates, Qatar, and Saudi Arabia have become transit centers for cargo transportation on account of their high-end airports and well-established network of airlines. The region of Latin America is witnessing stable growth in the global Freighter Aircraft Market due to increased foreign trade, cargo transportations, and better aviation facilities. The countries of Brazil, Mexico, and Chile contribute towards the growth of this market.

Supporting this position, major carriers in the region continue to expand their cargo fleets and invest in advanced logistics capabilities, including dedicated cargo terminals and digital cargo management systems. The development of free trade zones and logistics corridors is further enhancing cargo throughput and regional connectivity.

In addition, increasing demand for air cargo services in sectors such as oil & gas, pharmaceuticals, and e-commerce, along with government-led diversification strategies, is reinforcing the region’s role as a key growth engine in the global freighter aircraft market.

Freighter Aircraft Market Growth Drivers:

-

Rising global e-commerce demand and time-sensitive logistics driving adoption of freighter aircraft

The basic change in the dynamic nature of world trade in favor of speedier delivery of consignments as compared to conventional bulk deliveries constitutes the strongest structural force behind the growth of the freighter aircraft market. There is an increasing demand for faster delivery of goods and efficient logistics due to which logistics companies and airlines have started developing their own fleets of cargo aircraft. The need for speedy delivery of valuable cargo, medicines, and perishable items adds another dimension to this trend.

Supporting this growth, global air cargo handles goods valued at over USD 6 trillion annually, representing approximately 35% of world trade by value. Additionally, e-commerce-driven air cargo volumes have been growing at double-digit rates in key markets, prompting major operators to accelerate passenger-to-freighter conversions and invest in wide-body freighters.

Freighter Aircraft Market Restraints:

-

High capital costs and operational constraints associated with freighter aircraft limiting adoption, particularly for smaller operators

One of the major constraints on the growth of the market is the huge financial burden involved in owning and operating freighter aircraft. New wide-body freighters have to be purchased at the cost of huge amounts of money, whereas even conversions of existing passenger aircrafts into freighters are associated with heavy costs, including those of maintenance. In addition, costs of fuel fluctuation, crew training, and other costs of operations must also be considered. Small operators and carriers in developing markets struggle to grow their cargo capacity and fleets.

Freighter Aircraft Market Opportunities:

-

Expansion of e-commerce logistics networks and emerging market trade creating strong growth opportunities

The growing popularity of global e-commerce and the involvement of emerging countries in the conduct of international business have provided a great opportunity for the development of the freighter aircraft industry. The increasing need for timely and effective services in delivering products has led to increased dedicated capacity of air cargo logistics firms and efficient investment in the operation of freighter fleets. Air cargo volumes are also increasing in emerging markets in the Asia-Pacific, Latin America, and Africa regions due to better infrastructural and digital connectivity.

Recent Developments:

-

2026: Boeing expanded its freighter aircraft portfolio with increased production and global deliveries of the 777 Freighter and 767-300BCF, while advancing development of the 777-8 Freighter to meet rising long-haul cargo demand. The company also strengthened its Boeing Converted Freighter (BCF) program, supporting growing airline demand for cost-efficient passenger-to-freighter (P2F) solutions across global markets.

-

2025: Airbus reported strong commercial traction for its A350F freighter program, with multiple global orders from major cargo operators seeking next-generation fuel-efficient aircraft. The company also expanded its A320/A321 Passenger-to-Freighter (P2F) conversion programs through partnerships, enhancing capacity for narrow-body cargo aircraft to support booming e-commerce and regional logistics demand.

-

2025: ST Engineering accelerated its freighter conversion capabilities through its aviation asset management division, expanding global P2F conversion capacity for A320/A321 and Boeing 737 aircraft. The company strengthened partnerships with airlines and leasing companies, enabling faster turnaround times and increased output to meet rising global demand for converted freighters.

-

2025: Elbe Flugzeugwerke GmbH (EFW), a joint venture between Airbus and ST Engineering, expanded its A330 Passenger-to-Freighter (P2F) conversion program with new global conversion sites and increased production slots. The company also secured additional contracts from international carriers, reinforcing its position as a leading provider of wide-body freighter conversion solutions.

Freighter Aircraft Companies are:

-

Boeing

-

ST Engineering

-

Elbe Flugzeugwerke GmbH (EFW)

-

HAECO Group

-

Israel Aerospace Industries (IAI)

-

Precision Aircraft Solutions

-

Lufthansa Technik

-

Collins Aerospace

-

Lockheed Martin

-

Bombardier

-

Embraer

-

Mitsubishi Heavy Industries

-

COMAC (Commercial Aircraft Corporation of China)

-

Antonov Company

-

Textron Aviation

-

ATR Aircraft

-

FedEx Express

-

UPS Airlines

Freighter Aircraft Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.18 Billion |

| Market Size by 2035 | USD 8.53 Billion |

| CAGR | CAGR of 5.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Freighter Type (Passenger-to-Freighter (P2F) Converted Aircraft, OEM Configured Freighters, Others), • By Aircraft Type (Narrow-Body Freighters, Wide-Body Freighters, Regional Freighters, Dedicated Cargo Aircraft, Others), • By Engine Type (Turbofan, Turboprop, Jet Propulsion, Others), • By Application (Commercial Cargo, Military Cargo, E-commerce Logistics, Cold Chain (Pharma, Perishables), Others), • By Payload Capacity (Large (>80 tonnes), Medium (45–80 tonnes), Small (<45 tonnes), Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Boeing, Airbus, ST Engineering, Elbe Flugzeugwerke GmbH (EFW), HAECO Group, Israel Aerospace Industries (IAI), Aeronautical Engineers Inc. (AEI), Precision Aircraft Solutions, Lufthansa Technik, Collins Aerospace, Lockheed Martin, Bombardier, Embraer, Mitsubishi Heavy Industries, COMAC (Commercial Aircraft Corporation of China), Antonov Company, Textron Aviation, ATR Aircraft, FedEx Express, UPS Airlines. |

Frequently Asked Questions

The Freighter Aircraft Market is expected to grow at a CAGR of 5.22% from 2026 to 2035.

The Freighter Aircraft Market was valued at USD 5.18 billion in 2025.

The growth factor is the rapid expansion of global e-commerce and express logistics, which is fueling demand for efficient cargo transport solutions, rising cross-border trade and increasing preference for passenger-to-freighter (P2F).

The Narrow-Body Freighters segment dominated the Freighter Aircraft Market in 2025.

North America dominated the Freighter Aircraft Market in 2025.

Get in Touch