GLP-1 Receptor Agonist Market Report Scope & Overview:

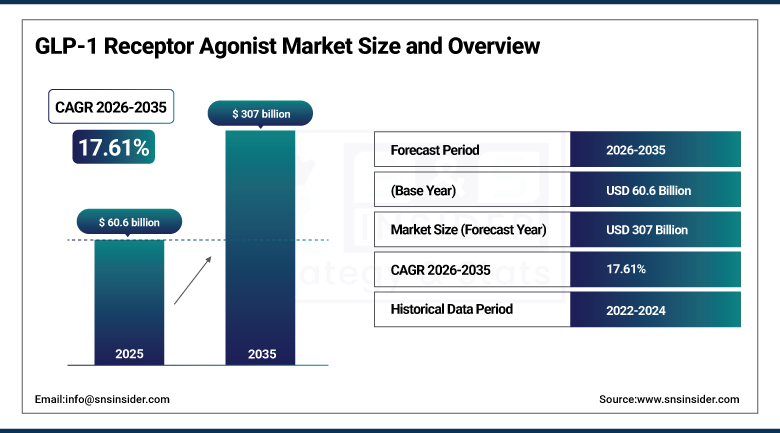

The GLP-1 Receptor Agonist Market was estimated at USD 60.6 billion in 2025 and is expected to reach USD 307 billion by 2035 and grow at a CAGR of 17.61% over the forecast period of 2026-2035.

The GLP-1 Receptor Agonists Market is witnessing growth because of the increasing incidences of Type 2 Diabetes and obesity, the rising need for efficacious weight management solutions, cardioprotective effects, expansion in the areas of clinical use, high acceptance rates of medicines such as Semaglutide, and innovations in the pharma industry.

Novo Nordisk's Ozempic and Wegovy combined generated USD 18.8 billion in 2023 revenue, making it the best-selling pharmaceutical product launch of the past decade. The International Diabetes Federation projects that the global diabetes population will reach 783 million by 2045, creating a growing clinical market for GLP-1 therapies that extends across the entire forecast period.

Market Size and Forecast

-

Market Size in 2025: USD 60.6 Billion

-

Market Size by 2035: USD 307 Billion

-

CAGR: 17.61% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on GLP-1 Receptor Agonist Market - Request Free Sample Report

GLP-1 Receptor Agonist Market Trends

-

Oral GLP-1 formulations led by Novo Nordisk's Rybelsus and Eli Lilly's orforglipron in development are expanding the patient population who will accept GLP-1 therapy by removing the injection barrier that constrains current market penetration.

-

Dual and triple receptor agonist development targeting GIP, GLP-1, and GCG receptors simultaneously is demonstrating superior weight loss and metabolic outcomes compared to single-receptor GLP-1 agents in clinical trials.

-

Manufacturing capacity expansion by Novo Nordisk and Eli Lilly with billions in active peptide production facility investment is working to resolve supply shortages that have limited GLP-1 market penetration despite strong prescription demand.

-

Biosimilar semaglutide development is advancing toward regulatory review by multiple pharmaceutical companies, with FDA biosimilar pathways potentially enabling lower-cost GLP-1 access within the forecast period.

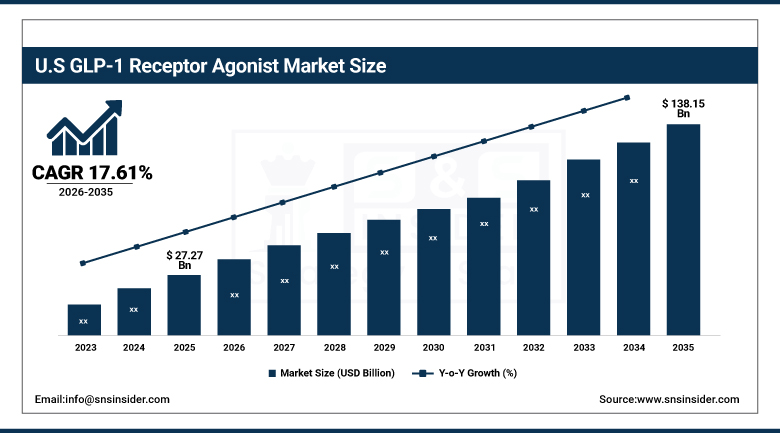

U.S. GLP-1 Receptor Agonist Market was valued at USD 27.27 billion in 2025 and is expected to reach USD 138.15 billion by 2035, growing at a CAGR of 17.61% from 2026-2035.

The United States is the world's dominant GLP-1 receptor agonist market by an enormous margin, with over 45% of global GLP-1 revenues generated domestically despite representing less than 5% of the world's diabetes and obesity patient population. The explanation lies in U.S. drug pricing, commercial insurance coverage breadth, and the aggressive commercial operations that Novo Nordisk and Eli Lilly have built around their GLP-1 products.

Express Scripts (Evernorth) reports that GLP-1 drugs became the fastest-growing pharmacy benefit expenditure category in U.S. employer health plans, with average spending per member increasing 380% between 2020 and 2023.

GLP-1 Receptor Agonist Market Segment Analysis

-

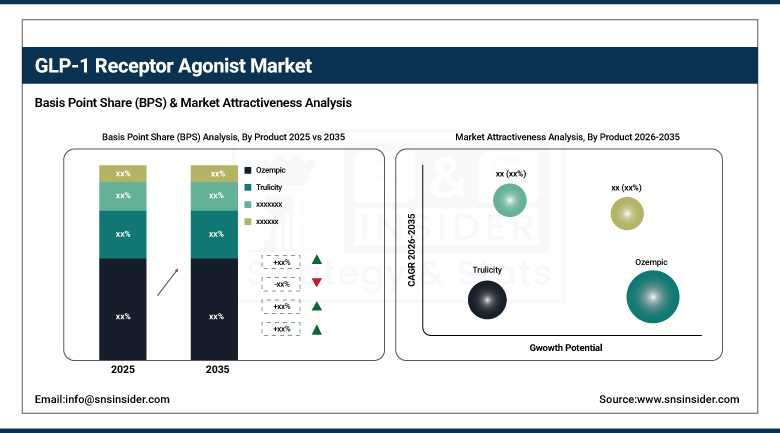

By Product, Ozempic dominated with ~35.12% share in 2025; Mounjaro and Zepbound (tirzepatide) growing fastest (CAGR).

-

By Application, Type 2 Diabetes Mellitus dominated the GLP-1 Market in 2025; Obesity segment growing at the fastest CAGR.

-

By Route of Administration, Parenteral dominated with the largest share in 2025; Oral growing fastest (CAGR).

-

By Distribution Channel, Hospital Pharmacies dominated in 2025; Retail and Online Pharmacies growing fastest.

By Product: Ozempic dominates, Tirzepatide products growing fastest

Ozempic (semaglutide 0.5mg/1mg/2mg weekly subcutaneous injection) dominated the GLP-1 receptor agonist market with approximately 35.12% market share in 2025, driven by its combination of robust clinical efficacy data, early market entry, broad diabetes label, established prescriber relationships, and expanded off-label use for weight management before Wegovy's commercial scale-up. Ozempic's once-weekly injection schedule, its demonstrated 1.5-1.8% HbA1c reduction, and the SUSTAIN cardiovascular outcomes trial data showing 26% reduction in major cardiovascular events in T2DM patients with established cardiovascular disease collectively built a clinical case that endocrinologists and cardiologists find compelling for guideline-aligned prescribing. Novo Nordisk's investment in prescriber education and patient support programs, combined with copay assistance initiatives that reduce out-of-pocket costs for commercially insured patients, has sustained Ozempic's prescription volume even as the market has expanded.

Mounjaro (tirzepatide for T2DM) and Zepbound (tirzepatide for obesity) from Eli Lilly are growing at the fastest CAGR, driven by the dual GLP-1/GIP receptor agonist mechanism that has consistently demonstrated superior weight loss outcomes versus semaglutide in head-to-head clinical comparisons. The SURPASS-2 trial showing tirzepatide achieving significantly greater HbA1c reduction and weight loss than semaglutide in T2DM patients, and the SURMOUNT trials showing up to 22% average body weight reduction in obese patients, have established tirzepatide as the clinical performance leader in the class. As Eli Lilly scales tirzepatide manufacturing capacity, its market share trajectory is upward and it is expected to challenge Novo Nordisk's revenue leadership within the forecast period.

By Application: T2DM dominates, Obesity growing fastest

Type 2 Diabetes Mellitus maintained the dominant application position in the GLP-1 Receptor Agonist Market in 2025, driven by the large established prescriber base, comprehensive insurance coverage for diabetes indications, and the longer clinical history of GLP-1 therapy in diabetes management that has built physician comfort and treatment guideline endorsement. The American Diabetes Association's Standards of Care recommending GLP-1 receptor agonists as preferred second-line agents after metformin and as first-line in patients with high cardiovascular risk create guideline-driven prescription demand that sustains diabetes application dominance.

The Obesity application segment is growing at the fastest CAGR and represents the most significant structural market expansion opportunity in the GLP-1 class's commercial history. The addressable obesity patient population conservatively estimated at 800 million people globally with BMI above 30, and considerably more when including the overweight population with comorbidities that justify pharmacotherapy dwarfs the T2DM market. The clinical case for long-term obesity pharmacotherapy has been strengthened by SELECT trial cardiovascular outcome data, growing insurance coverage mandates, and the demonstrated durability of weight loss maintenance in patients who remain on GLP-1 therapy.

By Route of Administration: Parenteral dominates, Oral growing fastest

Parenteral (subcutaneous injection) delivery held the dominant route of administration position in 2025, reflecting that all high-dose, high-efficacy GLP-1 formulations currently approved for obesity management require injection for the delivery of drug quantities sufficient to achieve therapeutic plasma concentrations. Novo Nordisk's FlexPen auto-injector and Eli Lilly's single-use pen devices have made once-weekly self-injection practical for most patients, with injection site reactions generally mild and transient. The clinical performance of injectable GLP-1 agents is well-established and documented in extensive trial databases that have accumulated over a decade of commercial experience. For patients who are already self-injecting insulin, the addition of a GLP-1 injection presents no new behavioral challenge and is straightforwardly accepted in clinical practice.

Oral GLP-1 currently represented by Rybelsus (oral semaglutide 7mg/14mg daily) for T2DM and advanced by Eli Lilly's orforglipron in late-stage trials — is growing at the fastest route of administration CAGR because it fundamentally removes the injection barrier that constrains GLP-1 therapy adoption in the substantial patient population for whom daily or weekly self-injection is a genuine disincentive to treatment initiation or maintenance. Rybelsus has demonstrated meaningful HbA1c reduction and weight loss, though somewhat less than injectable semaglutide at current approved doses. The development of next-generation oral GLP-1 agents with improved bioavailability enabling the higher systemic drug exposures needed to match injectable efficacy is the key technical milestone that will determine how much of the injectable market oral formulations can ultimately capture.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

22% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

36% |

|

Latin America |

Brazil |

50% |

North America GLP-1 Receptor Agonist Market Insights

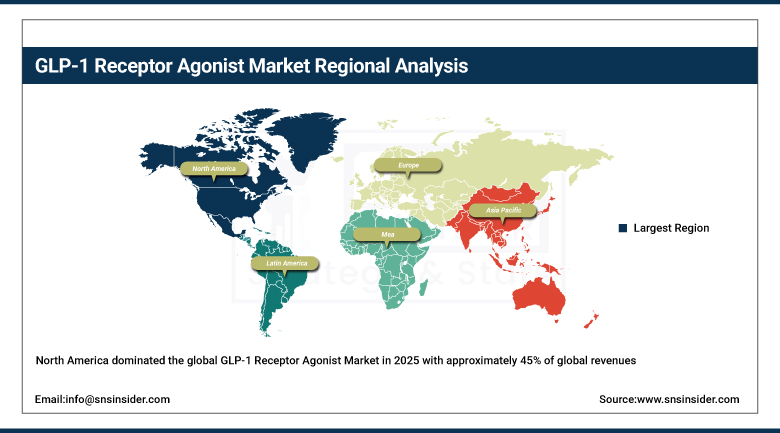

North America dominated the global GLP-1 Receptor Agonist Market in 2025 with approximately 45% of global revenues, anchored entirely by the United States' unique drug pricing environment and the commercial investment that Novo Nordisk and Eli Lilly have made in building GLP-1 prescribing across endocrinology, primary care, cardiology, and bariatric medicine. The U.S. health insurance landscape creates both the opportunity and the constraint: commercial insurance covering GLP-1 for diabetes generates large, well-reimbursed prescription volumes, but coverage for obesity indications varies widely, with Medicare explicitly prohibited from covering weight loss drugs until the Treat and Reduce Obesity Act passes a legislative gap that excludes tens of millions of Medicare beneficiaries from covered GLP-1 obesity access. Private employer plan GLP-1 coverage for obesity has become a major benefits policy debate, with large employers balancing the cost of GLP-1 coverage against documented workforce health and productivity benefits.

Goldman Sachs Research estimates that GLP-1 obesity drug prescriptions could reach 30 million Americans by 2028 if coverage barriers are resolved, representing USD 150+ billion in additional annual market potential beyond current diabetes-only prescribing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe GLP-1 Receptor Agonist Market Insights

Europe represents a substantial but price-controlled GLP-1 market where national health technology assessments determine coverage and reimbursement at drug prices that are dramatically below U.S. levels. Germany, the UK, France, and Scandinavia are the primary European GLP-1 markets, with strong diabetes prescribing supported by national guideline recommendations and health insurance coverage. Novo Nordisk a Danish company headquartered in Copenhagen has particularly strong European market relationships and has invested in prescriber education programs across European diabetes specialist networks that sustain its market leadership position in its home region. The UK's NHS has begun evaluating GLP-1 obesity coverage, with NICE's appraisal of semaglutide for obesity resulting in conditional approval for use through specialist weight management services a restrictive but meaningful coverage expansion that will grow over time as service capacity expands.

Asia Pacific GLP-1 Receptor Agonist Market Insights

Asia Pacific is the fastest-growing regional GLP-1 Receptor Agonist Market, driven by Japan's strong diabetes pharmacotherapy culture and well-developed GLP-1 prescribing base, China's enormous diabetes patient population with growing access to premium diabetes treatments, and India's rapidly expanding pharmaceutical market. Japan was one of the first markets outside the U.S. and Europe to approve and broadly adopt GLP-1 therapy, with Japanese prescribers known for their comfort with GLP-1 in T2DM management. China represents the single largest diabetes patient population globally an estimated 141 million adults with diabetes and the ongoing premium tier pharmaceutical market expansion is creating growing GLP-1 access for urban, commercially insured Chinese patients. South Korea's National Health Insurance Service has expanded GLP-1 reimbursement conditions, sustaining growing prescription volumes in a market with high diabetes awareness and strong specialist prescribing culture.

The Chinese government's 14th Five-Year Plan for healthcare specifically identifies diabetes management as a chronic disease prevention priority, with investment in guideline-based pharmacotherapy programs that are driving adoption of evidence-based GLP-1 therapy in public healthcare settings

Middle East & Africa and Latin America GLP-1 Receptor Agonist Market Insights

The Middle East represents a commercially interesting GLP-1 market because the Gulf states combine high rates of type 2 diabetes and obesity the UAE's adult obesity rate exceeds 37%, among the world's highest with high-income consumer populations and expanding private health insurance coverage. Saudi Arabia, UAE, and Kuwait are the primary Gulf GLP-1 markets, with both Novo Nordisk and Eli Lilly having established regional commercial operations and prescription support programs. The combination of high disease burden and commercial insurance or out-of-pocket payment capability makes Gulf markets commercially attractive despite their small absolute size. In Africa, GLP-1 access is currently limited primarily to private healthcare patients in South Africa, Nigeria, and Kenya, constrained by cost barriers that are not addressable without biosimilar entry or government subsidy programs.

GLP-1 Receptor Agonist Market Growth Drivers:

-

Rising global metabolic disease burden and expanding GLP-1 clinical indications driving extraordinary pharmaceutical market growth

The GLP-1 receptor agonist market's 17.61% CAGR reflects forces that are building in magnitude rather than plateauing. The diabetes and obesity epidemics keep growing with each year of sedentary lifestyle and caloric excess in developing nations whose middle classes are expanding rapidly. The clinical evidence base for GLP-1 therapy keeps expanding into new indication categories cardiovascular risk reduction, potential Alzheimer's benefit, heart failure management, sleep apnea, and kidney disease protection are all active investigation areas. Manufacturing capacity is catching up to demand, progressively lifting the supply constraints that have prevented GLP-1 prescriptions from being filled at the rate physicians would like to write them. Oral formulations are removing the injection barrier. Biosimilar development is beginning, though patent protection will sustain originator pricing through much of the forecast period.

GLP-1 Receptor Agonist Market Restraints:

-

High drug costs and manufacturing supply constraints limiting GLP-1 receptor agonist accessibility for patients globally

GLP-1 receptor agonists' commercial success has created its own constraint: demand so far exceeds production capacity that patients with legitimate prescriptions cannot reliably obtain their medication. Wegovy and Ozempic shortages reported by Novo Nordisk in 2023 and 2024 reflected production capacity that had not scaled in anticipation of the obesity indication approval's commercial impact. Building large-scale peptide manufacturing infrastructure takes 3-5 years and billions in capital expenditure — not a constraint that can be resolved quickly regardless of investment commitment. The cost barrier is equally structural: at USD 1,000-1,300 per month without insurance, GLP-1 drugs are affordable only to a small fraction of the global population who could benefit clinically, concentrating commercial market growth in the wealthy minority of the total addressable patient population.

GLP-1 Receptor Agonist Market Opportunities:

-

Expanded cardiovascular indications and biosimilar development creating transformative GLP-1 receptor agonist market opportunities

The cardiovascular indication expansion following SELECT trial approval for semaglutide in cardiovascular risk reduction in obese non-diabetic patients is qualitatively important because it changes who prescribes GLP-1 drugs. When a cardiologist's primary clinical mandate is preventing heart attacks and strokes, and a drug demonstrates 20% reduction in major cardiovascular events, that drug becomes a cardiovascular medicine rather than a metabolic medicine. Cardiologists prescribing GLP-1 for cardiovascular indication patients adds an entirely new prescriber base to what was previously an endocrinology and primary care domain. Biosimilar development is the medium-term democratization opportunity Biocon Biologics, Samsung Bioepis, and other biosimilar developers are advancing semaglutide biosimilar programs that, upon patent expiry, could reduce drug costs by 70-85% and dramatically expand patient access in both developed markets with coverage barriers and developing markets with affordability constraints.

Recent Developments:

-

2025: Eli Lilly received FDA approval for tirzepatide (Zepbound) as a treatment for moderate-to-severe obstructive sleep apnea in adults with obesity the first pharmacotherapy approved for this indication expanding tirzepatide's approved uses beyond metabolic conditions into a respiratory indication affecting over 30 million Americans and supported by SURMOUNT-OSA trial data showing 63% reduction in apnea-hypopnea index.

-

2025: Novo Nordisk announced positive Phase 3 ESSENCE trial results for semaglutide in early Alzheimer's disease, reporting statistically significant slowing of cognitive and functional decline a breakthrough data package that could establish GLP-1 therapy as a neuroprotective agent and open an addressable market of 6.5 million Alzheimer's patients in the U.S. alone.

GLP-1 Receptor Agonist Market Key Players

-

Novo Nordisk A/S (Ozempic, Wegovy, Rybelsus, Victoza, Saxenda)

-

Eli Lilly and Company (Mounjaro, Zepbound, Trulicity)

-

AstraZeneca PLC (Byetta, Bydureon BCise)

-

Sanofi SA

-

GlaxoSmithKline plc

-

Pfizer Inc.

-

Amgen Inc. (MariTide)

-

Boehringer Ingelheim GmbH

-

Zealand Pharma A/S

-

Hanmi Pharmaceutical Co., Ltd.

-

Structure Therapeutics Inc.

-

Altimmune Inc.

-

Carmot Therapeutics (Roche)

-

Viking Therapeutics Inc.

-

Biohaven Pharmaceuticals

-

Inventiva SA

-

Oramed Pharmaceuticals Inc.

-

Haisco Pharmaceutical Group

-

Jiangsu Hengrui Medicine Co., Ltd.

-

Hua Medicine Ltd.

GLP-1 Receptor Agonist Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 60.6 Billion |

| Market Size by 2035 | USD 307 Billion |

| CAGR | CAGR of 17.61% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ozempic, Trulicity, Mounjaro, Wegovy, Rybelsus, Saxenda, Victoza, Zepbound, Other Products) • By Application (Type 2 Diabetes Mellitus, Obesity) • By Route of Administration (Parenteral, Oral) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novo Nordisk A/S (Ozempic, Wegovy, Rybelsus, Victoza, Saxenda), Eli Lilly and Company (Mounjaro, Zepbound, Trulicity), AstraZeneca PLC (Byetta, Bydureon BCise), Sanofi SA, GlaxoSmithKline plc, Pfizer Inc., Amgen Inc. (MariTide), Boehringer Ingelheim GmbH, Zealand Pharma A/S, Hanmi Pharmaceutical Co., Ltd., Structure Therapeutics Inc., Altimmune Inc., Carmot Therapeutics (Roche), Viking Therapeutics Inc., Biohaven Pharmaceuticals, Inventiva SA, Oramed Pharmaceuticals Inc., Haisco Pharmaceutical Group, Jiangsu Hengrui Medicine Co., Ltd., Hua Medicine Ltd. |

Frequently Asked Questions

Ans: North America dominated the GLP-1 Receptor Agonist Market with approximately 45% share in 2025.

Ans: The Obesity application segment is expected to register the fastest CAGR in the GLP-1 Receptor Agonist Market.

Ans: Ozempic dominated with approximately 35.12% share in 2025; Mounjaro and Zepbound are the fastest growing.

Ans: The GLP-1 Receptor Agonist Market was valued at USD 60.6 billion in 2025.

Ans: The GLP-1 Receptor Agonist Market is expected to grow at a CAGR of 17.61% from 2026 to 2035.

Get in Touch