Gum Rosin Market Report Scope & Overview:

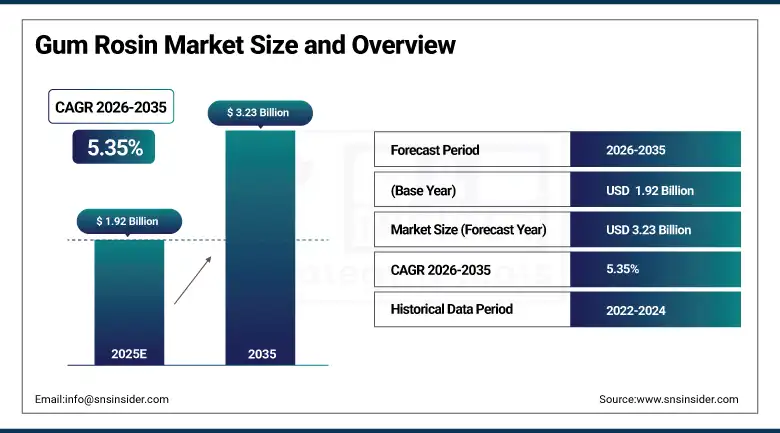

The Gum Rosin Market was valued at USD 1.92 billion in 2025 and is expected to reach USD 3.23 billion by 2035, growing at a CAGR 5.35% of from 2026-2035.

The gum rosin market is driven by rising demand from adhesives, sealants, printing inks, rubber, and personal care applications. Growth in construction, packaging, automotive, woodworking, and publishing industries, along with increasing population, disposable incomes, and evolving consumer preferences, continues to expand its industrial and consumer end-use base.

The market is experiencing steady growth supported by gum rosin’s superior tackifying properties, thermal stability, and formulation compatibility. Increasing adoption of sustainable and natural resins, advancements in processing technologies, lightweight product trends, and investments in eco-friendly manufacturing infrastructure are shaping favourable long-term growth prospects.

Gum rosin demand increased globally in 2025 by 4.5%, driven by rising consumption in adhesives, rubber compounding, and the growing shift toward bio-based resins across industrial manufacturing.

Market Size and Forecast:

-

Market Size in 2025: USD 1.92 Billion

-

Market Size by 2035: USD 3.23 Billion

-

CAGR: 5.35%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Gum Rosin market - Request Free Sample Report

Trends in the Gum Rosin Market

-

Rising substitution of petroleum-based resins with bio-based gum rosin across adhesives, inks, and rubber applications

-

Increasing demand for modified rosin derivatives (hydrogenated, polymerized, esterified) to enhance thermal stability and performance

-

Growing use of gum rosin in pressure-sensitive and hot-melt adhesives driven by packaging and construction growth

-

Expansion of sustainable pine resin sourcing and certified forestry practices

-

Technological advancements improving rosin purity, consistency, and downstream processing efficiency

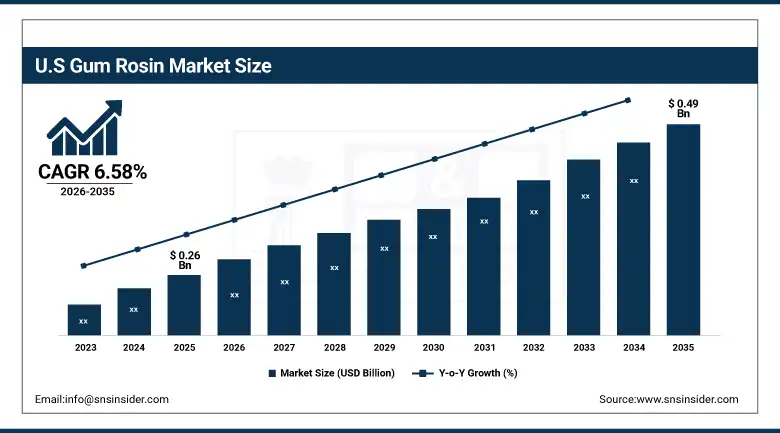

U.S. Gum Rosin Market Insights:

The U.S. Gum Rosin Market is projected to grow from USD 0.26 Billion in 2025 to USD 0.49 Billion by 2035, at a CAGR of 6.58%. The growth is driven by rising demand from adhesives, packaging, construction, and rubber industries, increased preference for bio-based resins, technological advancements, and expanding manufacturing and infrastructure investments.

Gum Rosin Market Growth Drivers:

• Expanding Industrial Applications Accelerating Gum Rosin Consumption

Gum rosin demand is being strengthened by adhesives and sealants contributing over 40% of total usage, supported by rising output in packaging and building materials. Rubber compounding accounts for nearly one-quarter of consumption, driven by increasing tire production and industrial rubber goods. Printing inks and surface coatings together represent around one-fifth of demand, reflecting steady growth in packaging and labelling. Furthermore, more than two-thirds of tackifier formulations now incorporate bio-based resins, reinforcing long-term adoption across industrial manufacturing.

Gum Rosin Market Restraints:

-

Raw Material Price Volatility and Availability Challenges Limiting Growth

Market growth is restrained by volatility in raw material prices, as gum resin production depends on pine tapping, which is highly influenced by climatic conditions, seasonal variations, and labour availability. Fluctuations in resin yield impact cost stability and supply consistency. In addition, synthetic tackifiers account for nearly 40% of the global tackifier market, offering predictable pricing and uniform quality, which limits gum resin adoption in price-sensitive applications despite rising interest in natural materials.

Gum Rosin Market Opportunities:

-

Increasing Preference for Sustainable and Modified Resins Creating New Opportunities

Opportunities in the gum rosin market are driven by rising adoption of sustainable, bio-based materials across industrial applications. Modified gum rosin derivatives are gaining traction due to improved thermal stability and formulation compatibility. Growing use of low-VOC adhesives, inks, and coatings in packaging and construction, along with advancements in processing technologies, is expanding application scope and supporting long-term market growth.

Gum Rosin Market Segment Analysis:

-

By Product Type: In 2025, natural gum rosin led the market with around 70% share, while modified gum rosin (hydrogenated, polymerized, disproportionated) is expected to be the fastest-growing segment during 2026–2035.

-

By Grade: In 2025, WG and WW grades accounted for the largest share at approximately 45%, owing to their use in high-quality adhesives and inks, while specialty grades are projected to register the highest CAGR during 2026–2035.

-

By Application: In 2025, adhesives and sealants dominated the market with nearly 38% share, while rubber and tire manufacturing is anticipated to be the fastest-growing application segment during 2026–2035.

-

By End-Use Industry: In 2025, packaging and construction industries together accounted for about 44% of total demand, while automotive and rubber industries are expected to witness the fastest growth during 2026–2035.

-

By Form: In 2025, solid gum rosin held the dominant share of approximately 85%, while liquid and derivative-based forms are projected to grow at the highest CAGR during 2026–2035.

-

By Distribution Channel: In 2025, direct sales dominated the gum rosin market with a share of approximately 63%, while distributors and traders are projected to register the highest CAGR during 2026–2035.

By Product Type: Natural Gum Rosin Leads as Modified Gum Rosin Emerges as Fastest-Growing Segment

Natural gum rosin dominates the product type segment due to its wide availability, cost-effectiveness, and extensive use in adhesives, rubber compounding, inks, coatings, and paper sizing. Its renewable origin and strong tackifying properties make it a preferred choice across traditional industrial applications, particularly where sustainability and performance balance are required.

Modified gum rosin is the fastest-growing product type, driven by increasing demand for high-performance materials. Hydrogenated, polymerized, and disproportionated rosins offer improved thermal stability, oxidation resistance, and formulation compatibility, supporting their rising adoption in specialty adhesives, printing inks, coatings, rubber products, and low-VOC, eco-friendly formulations.

By Grade: WG and WW Grades Dominate While Specialty Grades Show Rapid Growth

WG and WW grades lead the market owing to their high purity, lighter colour, and consistent quality, making them suitable for premium adhesives, inks, coatings, and rubber applications. Their reliability and performance characteristics support widespread industrial adoption.

Specialty and higher-purity grades are witnessing faster growth as manufacturers increasingly focus on product performance, colour stability, and regulatory compliance. These grades are gaining traction in specialty chemicals, electronics, and advanced industrial applications.

By Application: Adhesives and Sealants Dominate as Rubber Applications Grow Rapidly

Adhesives and sealants dominate the application segment due to gum rosin’s superior tackifying properties, which enhance bonding strength and processing efficiency. Strong demand from packaging, construction, and woodworking industries continues to support this segment’s leadership.

Rubber and tire manufacturing represents the fastest-growing application, driven by rising automotive production and infrastructure development. Gum rosin improves adhesion between rubber compounds and fillers, enhancing durability, strength, and performance in tires and industrial rubber products.

By End-Use Industry: Packaging and Construction Lead While Automotive Gains Momentum

Packaging and construction industries account for the largest share of gum rosin consumption, supported by steady growth in building activities, infrastructure development, and demand for adhesive-based solutions.

The automotive industry is emerging as a high-growth end-use segment due to increasing vehicle production, replacement tire demand, and the need for lightweight, durable rubber components that benefit from gum rosin-based formulations.

By Form: Solid Gum Rosin Dominates as Derivative-Based Forms Expand

Solid gum rosin dominates the market due to ease of handling, storage stability, and suitability for bulk industrial processing. It remains the preferred form for traditional adhesive, rubber, and ink formulations.

Derivative-based and liquid forms are growing rapidly as manufacturers seek formulation flexibility, improved dispersion, and enhanced performance, particularly in advanced adhesives, coatings, and specialty chemical applications.

By Distribution Channel: Direct Sales Lead as Distributors & Traders Emerge as Fastest-Growing Segment

Direct sales dominate the distribution channel segment in the gum rosin market due to long-term supply agreements with large adhesive, rubber, ink, and paper manufacturers. Producers prefer direct sales to ensure consistent quality, stable pricing, and reliable bulk supply, particularly for industrial-scale applications.

Distributors and traders represent the fastest-growing distribution channel, driven by rising demand from small and mid-sized manufacturers and expanding consumption in emerging markets. Their ability to offer flexible order volumes, regional reach, and diversified sourcing supports faster adoption across fragmented end-user industries.

Gum Rosin Market Regional Analysis:

North America Gum Rosin Market Insights:

North America Gum Rosin Market Valued at USD 0.65 billion in 2025 and projected to reach USD 0.90 billion during 2026–2035, North America holds a significant share of the global gum rosin market. Strong demand from adhesives, rubber, paper sizing, and printing inks continues to drive growth. Well-developed construction and automotive industries remain major end users, while rising disposable incomes and increasing awareness of sustainability are accelerating the adoption of bio-based resins. Ongoing investments in eco-friendly manufacturing and regulatory support further contribute to steady market expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Gum Rosin Market Insights:

Europe represents a significant market for gum rosin, supported by strict environmental regulations and a strong focus on sustainable, bio-based materials. Demand is driven by adhesives, rubber, printing inks, and paper applications, along with a well-established construction and automotive industry base. Increasing adoption of low-VOC formulations and circular economy initiatives across key economies such as Germany, the UK, and France continues to support steady market development.

Asia-Pacific Gum Rosin Market Insights:

Asia-Pacific is the fastest growing region, expected to grow at a CAGR of 8.24%. Rapid industrialization and expansion of construction, packaging, automotive, and rubber industries are increasing demand for adhesives and rubber compounds, thereby driving consumption. Abundant pine resources and growing manufacturing capacity enable cost-efficient production, while rising adoption of bio-based materials and infrastructure investments further support sustained market growth.

Latin America Gum Rosin Market Insights:

Latin America is an emerging gum rosin market, driven by growing industrialization and rising demand from construction, adhesives, and automotive sectors. Expanding pine resin production and increasing focus on sustainable alternatives continue to support regional market growth.

Middle East & Africa Gum Rosin Market Insights:

The Middle East & Africa gum rosin market is gradually expanding, supported by growth in construction, infrastructure, and packaging industries. Rising use of adhesives and coatings, along with increasing industrial investments, is driving demand, though limited local production and import dependence remain key challenges.

Gum Rosin Market Competitive Landscape:

Wuzhou Pine Chemicals Ltd., headquartered in China, is one of the leading producers of gum rosin and rosin derivatives globally. The company supplies high-quality rosin products for adhesives, rubber compounding, inks, coatings, and paper sizing applications. Its vertically integrated operations, strong raw material sourcing, and consistent product quality support large-scale industrial demand across domestic and international markets.

-

In March 2024: The company expanded its refined gum rosin production capacity to meet rising demand from adhesive and rubber manufacturers.

-

In October 2024: Wuzhou Pine Chemicals strengthened its export portfolio by introducing higher-purity rosin grades for specialty chemical applications.

Foreverest Resources Ltd., based in China, is a prominent supplier of gum rosin, wood rosin, and rosin derivatives serving global adhesive, ink, coating, and rubber industries. The company is known for its broad product portfolio, stable pine resin sourcing network, and focus on sustainable forestry practices, enabling reliable supply of bio-based resins.

-

In May 2024: Foreverest Resources enhanced its supply chain operations to support growing international demand for natural tackifiers.

-

In November 2024: The company launched customized gum rosin grades tailored for pressure-sensitive adhesives and rubber processing applications.

Arakawa Chemical Industries, Ltd., headquartered in Japan, is a major specialty chemicals manufacturer with a strong presence in gum rosin and rosin derivative markets. The company focuses on high-performance rosin-based resins used in adhesives, printing inks, coatings, and electronic materials, supported by advanced R&D and stringent quality standards.

-

In February 2024: Arakawa introduced upgraded rosin ester products designed to improve thermal stability and adhesion performance.

-

In August 2024: The company increased investment in bio-based resin development to support sustainability-driven demand from automotive and packaging industries.

Gum Rosin Market Key Players

-

Wuzhou Pine Chemicals Ltd.

-

Arakawa Chemical Industries, Ltd.

-

DRT (Les Dérivés Résiniques et Terpéniques)

-

Eastman Chemical Company

-

Mangalam Organics Limited

-

Guangdong Komo Co., Ltd.

-

Guilin Songquan Forest Chemical Co., Ltd.

-

Anhui Hualin Pine Chemical Industry Co., Ltd.

-

Xinhui Hengxin Chemical Co., Ltd.

-

Deqing Genyuan Chemical Co., Ltd.

-

Meilong Chemical Co., Ltd.

-

Jiangxi Feishang Forestry Co., Ltd.

-

Fudong Chemical Co., Ltd.

-

Pine Chemical Group (PCG)

-

Resitol Chemical Industry Ltd.

-

Saptagir Camphor Ltd.

-

Indonesia Pinus Resin Industry (Perhutani Group)

-

Harima Chemicals Group, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.92 Billion |

| Market Size by 2035 | USD 3.23 Billion |

| CAGR | CAGR of 5.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Natural Gum Rosin, Modified Gum Rosin: Hydrogenated Rosin, Polymerized Rosin, Disproportionated Rosin, Maleated Rosin, Rosin Esters) • By Grade (WW Grade, WG Grade, N Grade, M Grade, K Grade) • By Application (Adhesives & Sealants, Rubber & Tire Manufacturing, Printing Inks, Paints & Coatings, Paper Sizing, Soaps & Detergents, Specialty Chemicals) • By End-Use Industry (Packaging, Construction, Automotive, Paper & Pulp, Consumer Goods, Electronics & Electrical Insulation, Footwear & Furniture) • By Form (Solid Gum Rosin, Liquid Rosin & Derivatives) • By Distribution Channel (Direct Sales, Distributors & Traders |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Wuzhou Pine Chemicals Ltd., Foreverest Resources Ltd., Arakawa Chemical Industries, Ltd., DRT (Les Dérivés Résiniques et Terpéniques), Eastman Chemical Company, Kraton Corporation, Mangalam Organics Limited, Guangdong Komo Co., Ltd., Guilin Songquan Forest Chemical Co., Ltd., Anhui Hualin Pine Chemical Industry Co., Ltd., Xinhui Hengxin Chemical Co., Ltd., Deqing Genyuan Chemical Co., Ltd., Meilong Chemical Co., Ltd., Jiangxi Feishang Forestry Co., Ltd., Fudong Chemical Co., Ltd., Pine Chemical Group (PCG), Resitol Chemical Industry Ltd., Saptagir Camphor Ltd., Indonesia Pinus Resin Industry (Perhutani Group), Harima Chemicals Group, Inc. |

Frequently Asked Questions

Adhesives and sealants lead the Gum Rosin Market, with rubber and tire manufacturing growing rapidly.

Asia-Pacific is the fastest-growing region in the Gum Rosin Market, with a CAGR of 8.24%.

The Gum Rosin Market is expected to grow at a CAGR of 5.35% during 2026–2035.

The Gum Rosin Market was valued at USD 1.92 billion in 2025.

The Gum Rosin Market is projected to reach USD 3.23 billion by 2035.

Get in Touch