Hemorrhoids Treatment Market Report Scope & Overview:

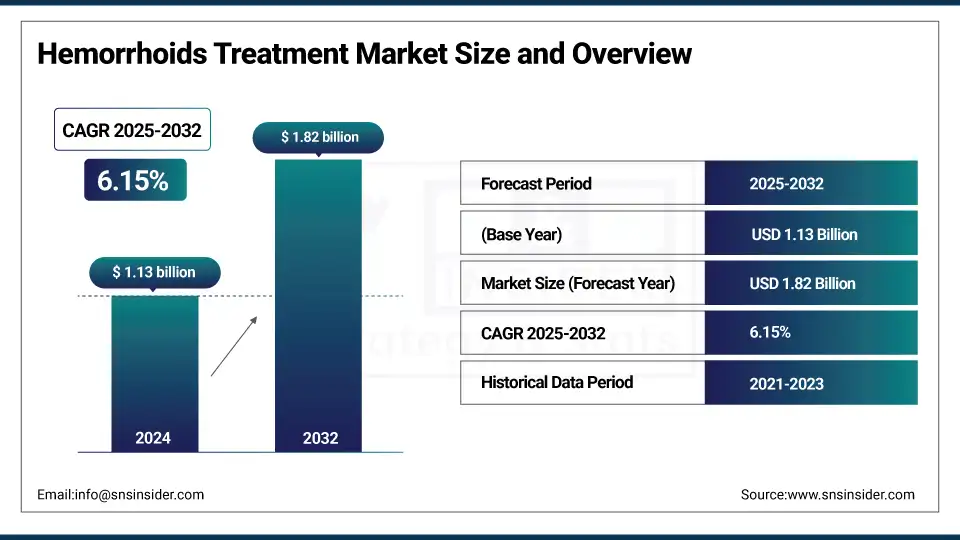

The Hemorrhoids Treatment Market size was valued at USD 1.13 billion in 2024 and is expected to reach USD 1.82 billion by 2032, growing at a CAGR of 6.15% over 2025-2032.

The global burden of anorectal disorders is continuously increasing due to the growing incidence of obesity, sedentary lifestyle, and constipation is responsible for the ongoing penetration of the hemorrhoids treatment market share. The growing geriatric population, particularly in the U.S., where hemorrhoids mostly affect older adults, is driving market demand. In addition, increasing knowledge and easy access to over-the-counter (OTC) drugs, and technological advancements in non-surgical treatments such as infrared coagulation and rubber band ligation, are anticipated to propagate the growth of the global hemorrhoids therapy market over the forecast period.

To Get more information On Hemorrhoids Treatment Market - Request Free Sample Report

Church & Dwight strengthened its position in the hemorrhoids treatment market in April 2024 with the launch of a new hemorrhoid cream that provides dual-action pain relief and anti-inflammatory properties.

The regulatory approvals for newer topical agents and improved surgical devices drive the hemorrhoids treatment market growth. One instance is Sebela Pharmaceuticals, which has opened new indications for rectal therapies. In addition, increasing focus of companies such as Bayer and GlaxoSmithKline on R&D investments for anti-inflammatory and pain-relief formulations is leading to further innovations in the hemorrhoids treatment landscape.

Rapid e-commerce infrastructure growth is expected to boost drug availability in the market. Augmented healthcare spending in the U.S. encourages treatment penetration, with supportive reimbursement schemes for hemorrhoids treatment, complemented by authoritative verification of safety and effectiveness by regulatory authorities. Preference for outpatients is climbing, and so too are market dynamics leading the conversation towards less invasive practices. Based on the hemorrhoids treatment market trend, hemorrhoids treatment market analysis, oral and topical solutions are expected to hold a significant share of the market due to their less expensive cost and ease of usage (Oral analgesics like Acetaminophen & Topical (analgesics or NSAID) continue to impact a huge patient population for providing symptomatic relief.

Boston Scientific Corporation announced in January 2024 clinical trials of a minimally invasive device designed for the elimination of internal hemorrhoids, reflecting foundational hemorrhoids treatment market trends leading toward procedural innovation and better patient compliance.

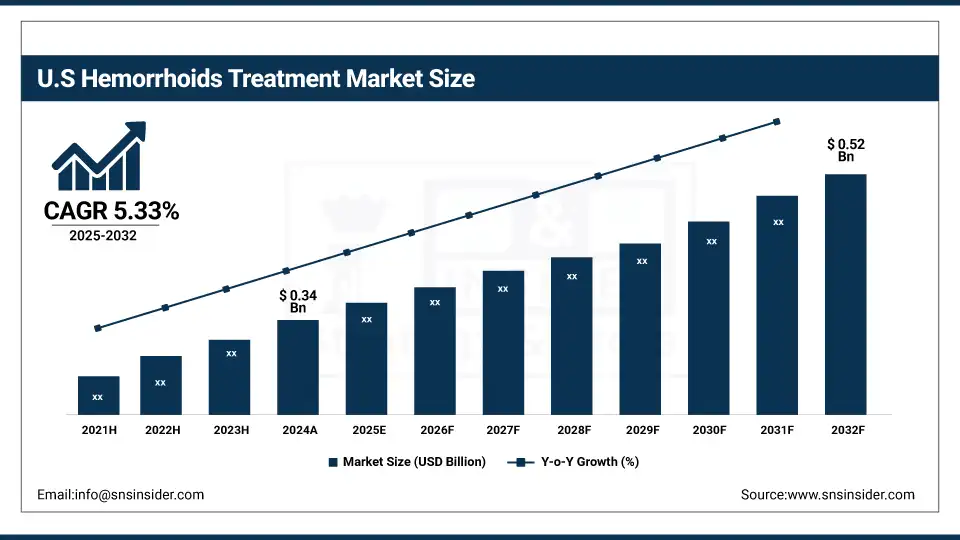

The U.S. hemorrhoids treatment market size was valued at USD 0.34 billion in 2024 and is expected to reach USD 0.52 billion by 2032, growing at a CAGR of 5.33% over 2025-2032. In the U.S., harrowing level of piles nationwide, attacks nearly 1 in 20 Americans annually, and results in an estimated 10 million doctor consultations for hemorrhoid-related troubles. High demand for OTC drugs and easy availability of less invasive surgical procedures further deepen the dominance. Despite its smaller population, Canada is also experiencing growth due in part to the expansion of preventive care and retail pharmacy.

Market Dynamics:

Drivers:

-

Increasing Treatment Demand, Advancing Technologies, and Rising Healthcare Investments Propel Market Expansion

The hemorrhoids treatment market is majorly driven by the growing demand on account of the increasing incidence of constipation, obesity, unhealthy eating habits, and sedentary lifestyles. This generates ongoing product demand as over 75% of the population in developed nations will experience hemorrhoids at some point in their life. Treatment options like non-invasive devices, bioactive creams, and suppository delivery system enhancements have increased the number of patients who can be treated effectively while increasing comfort and driving adoption. Novel formulations that are fast-acting with minimal side effects have piqued the interest of companies like Taro Pharmaceuticals and Teva. Additionally, substantial R&D spend is being done to introduce corticosteroid-sparing drugs and natural herbal combinations, suiting the rising trend of milder prescriptions.

In 2023, gastrointestinal therapeutics were a leading driver of the 12% overall increase in pharma R&D pipelines, according to Pharma Intelligence. The development of such technologies is influenced by the regulatory approvals, the latest being FDA approval for radio frequency-based radiosurgery systems provides a safe and effective outpatient option in hemorrhoid treatment. Besides, hospitals and ambulatory centers are observed to be buying more value-proctology devices, which in turn boosts the sales in the procedural volume growth. These factors, along with improved insurance coverage in many countries, are propelling the demand for hemorrhoids treatment and widening patient access across the Rx prescription and over-the-counter OTC segment.

Restraints:

-

Social Stigma, Limited Awareness, and an Inconsistent Regulatory Landscape Hinder Market Growth

Even with this robust demand, the hemorrhoid treatment market is inhibited by key growth restraints such as low disease awareness, a considerable lag in diagnosis, and an enduring social stigma regarding anorectal diseases. Embarrassment will lead to many putting off visiting a doctor, while others will simply ignore symptoms because they believe it is 'better the devil you know'. Consequently, the early treatment window, the one in which non-surgical treatments tend to be most effective, is best of easily escaped.

Additionally, a lack of standard regulations and over-the-counter (OTC) product classification in different countries can impede the market to a certain extent. Such is the case with some herbal or topical agents that have not been clinically validated or do not meet rigorous regulatory standards for efficacy, making them difficult to trust and adopt by physicians. Supply issues in 2022 were blamed for shortages of the crucial corticosteroid-based hemorrhoid treatments, with key active pharmaceutical ingredients (APIs) coming from manufacturing plants that have been hit by interruptions to manufacturing in Asia. Moreover, out-of-pocket expenditure is higher due to reimbursement gaps for new treatments such as laser therapy or RF ablation, making these treatments less than optimal. Hemorrhoids, which are not a life-threatening disease compared to chronic diseases, have consequently received low-level funding over the years in terms of Public Health Programmes.

Segmentation Analysis:

By Treatment Type

Pharmacological treatments were the most frequently prescribed hemorrhoids treatment in 2024, as a result of being over-the-counter commercial features for creams, suppositories, and oral medication to manage Phase I-Grade II hemorrhoids. A lot of this prevalence was driven by their affordability, ability to self-administer, and mass-dispensability over-the-counter.

Most notable are non-surgical procedures, which report the fastest growth as growing numbers of patients require treatment for conditions such as rubber band ligation, infrared coagulation, and sclerotherapy that all offer specific benefits, recovery time, and complication rates in an ambulatory setting.

By Route of Administration

Topical treatments accounted for the maximum share in 2024, at 46%, as patients opt for quick relief treatments including creams, ointments, and gels, especially concerning external hemorrhoids. Local application, along with symptom targeting, leads to its major domination.

The rectal route will be the fastest growing and is driven by increasing clinician preference for higher efficacy suppositories and rectal foams that provide improved relief from internal hemorrhoids along with enhanced absorption.

By Type

Internal hemorrhoids led the market within 2024, of the total cases treated, there were about 58% internal hemorrhoids because they happen to be more common and cause reasonable bleeding or discomfort that usually need medical or procedural intervention.

The external hemorrhoids segment is the largest and fastest-growing, powered by self-treatment with OTC products and increasing awareness of hygiene and symptom management.

By Distribution Channel

Retail pharmacies & drug stores had the largest portion in 2024, accounting for 48% due to higher consumer convenience of OTC drugs and pharmacist-recommended remedies. This, coupled with the physical presence and availability of newsagents nearby, has made it the most natural go-to channel.

Online pharmacies are the fastest-growing distribution channel supported by growing e-commerce penetration, discrete purchasing options, and doorstep delivery of hemorrhoid medicines and wellness products.

Regional Analysis:

In 2024, North America led the global hemorrhoids treatment market because of its developed healthcare infrastructure, large number of aware people, and major pharmaceutical companies & medical devices in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific is expected to be the fastest-growing region in this market due to the rapidly increasing number of patients, high. Urbanization and a large pool of patients with low. Impossible access to healthcare. Owing to the presence of a large aging population and rising consumption of OTC drugs, China is the market leader. Hemorrhoids afflict as many as 12–15% of adults in urban areas. With rising awareness about anorectal health and cost-effective generic products flooding the space, the Indian market is making significant strides. Growing investments in Japan and South Korea for hospital infrastructure and e-pharmacy platforms fostered international expansion.

Key Players:

Leading hemorrhoids treatment companies include Lupin, Cipla, AMATO Pharmaceutical Products, Church & Dwight Co., Haleon, Sebela Pharmaceuticals, Bayer, Sanofi, Abbott, Sun Pharmaceutical Industries, AstraZeneca, Boehringer Ingelheim, Boston Scientific Corporation, CONMED Corporation, Cook Medical, GlaxoSmithKline, Olympus Corporation, Pfizer, Takeda Pharmaceutical Company, and Glenmark Pharmaceuticals.

Recent Developments:

In April 2024, Innovus Pharmaceuticals launched a new over-the-counter hemorrhoid relief cream formulated with lidocaine and natural botanicals, targeting the growing demand for topical and non-invasive solutions. This product launch strengthens their consumer health portfolio in the gastrointestinal segment.

In February 2024, Medtronic announced the expansion of its minimally invasive surgical hemorrhoid treatment device across select Asia Pacific markets. The initiative aims to improve patient outcomes and cater to the rising incidence of severe hemorrhoidal disease in the region.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.13 billion |

| Market Size by 2032 | USD 1.82 billion |

| CAGR | CAGR of 6.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type [Pharmacological Treatments [Laxatives, NSAIDs, Corticosteroids, Local Anesthetics, Herbals, Others (e.g., flavonoids, vasoconstrictors, astringents)], Non-Surgical Procedures [Rubber Band Ligation, Sclerotherapy, Infrared Coagulation, Cryotherapy], Surgical Procedures [Hemorrhoidectomy, Stapled Hemorrhoidopexy]] • By Route of Administration [Oral, Topical, Rectal] • By Type [Internal Hemorrhoids, External Hemorrhoids] • By Distribution Channel [Hospital Pharmacies, Retail Pharmacies & Drug Stores, Online Pharmacies] |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Lupin, Cipla, AMATO Pharmaceutical Products, Church & Dwight Co., Haleon, Sebela Pharmaceuticals, Bayer, Sanofi, Abbott, Sun Pharmaceutical Industries, AstraZeneca, Boehringer Ingelheim, Boston Scientific Corporation, CONMED Corporation, Cook Medical, GlaxoSmithKline, Olympus Corporation, Pfizer, Takeda Pharmaceutical Company, and Glenmark Pharmaceuticals. |

Frequently Asked Questions

Ans: Aging populations are more prone to constipation and chronic venous insufficiency, leading to increased hemorrhoid incidence and thus driving higher demand for both medical and surgical treatments.

Ans: Topical treatments, suppositories, and non-surgical procedures like rubber band ligation are widely used due to convenience and efficacy in early-stage hemorrhoids.

Ans: Key players include Abbott, Sanofi, Bayer, Church & Dwight, GlaxoSmithKline, Boston Scientific, and Sebela Pharmaceuticals, offering both drug-based and device-assisted treatments.

Ans: Minimally invasive procedures like infrared coagulation, laser therapy, and radiofrequency ablation are gaining traction due to shorter recovery times and reduced postoperative complications.

Ans: North America holds the largest market share due to high healthcare expenditure and awareness, while the Asia-Pacific region is the fastest-growing due to improving access to healthcare and an increasing patient pool.

Get in Touch