Hepatitis B Treatment Market Report Scope & Overview:

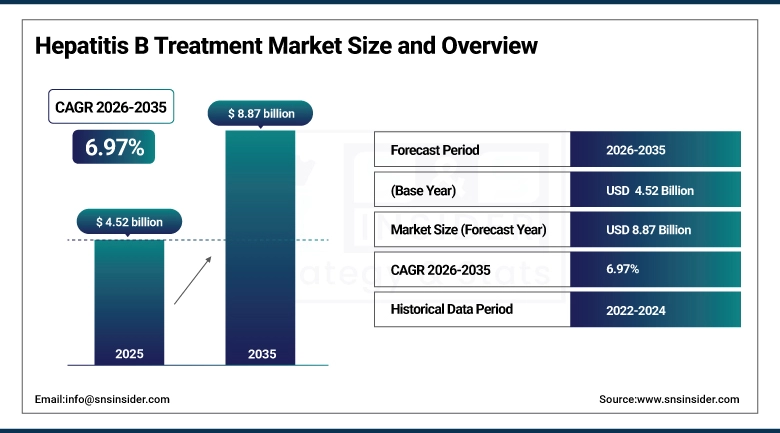

The Hepatitis B Treatment Market Size is valued at USD 4.52 Billion in 2025 and is projected to reach USD 8.87 Billion by 2035, growing at a CAGR of 6.97% during the forecast period 2026–2035.

The Hepatitis B Treatment Market analysis report provides a comprehensive overview of therapeutic advancements, disease management trends and treatment adoption patterns. Rising chronic hepatitis prevalence, expanding antiviral pipelines and improved healthcare access are expected to drive market growth during the forecast period.

Hepatitis B treatment demand covered over 32 million diagnosed patients in 2025, driven by expanding screening programs and long-term antiviral therapy adoption.

Hepatitis B Treatment Market Size and Forecast:

-

Market Size in 2025: USD 4.52 Billion

-

Market Size by 2035: USD 8.87 Billion

-

CAGR: 6.97% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Hepatitis B Treatment Market - Request Free Sample Report

Hepatitis B Treatment Market Trends:

-

Growing focus on early diagnosis and preventive healthcare is accelerating demand for timely hepatitis B treatment and long-term disease management.

-

Rising adoption of oral antiviral therapies is improving patient compliance and supporting sustained treatment adherence.

-

Expansion of novel therapies, including RNA-based and immune-modulating drugs, is reshaping the treatment landscape.

-

Increasing government-led screening, vaccination and awareness programs are strengthening treatment uptake.

-

Improved access to hospital and retail pharmacies, including online channels is enhancing therapy availability.

-

Advancements in personalized medicine and combination therapies are gaining traction to improve clinical outcomes and reduce resistance.

U.S. Hepatitis B Treatment Market Insights:

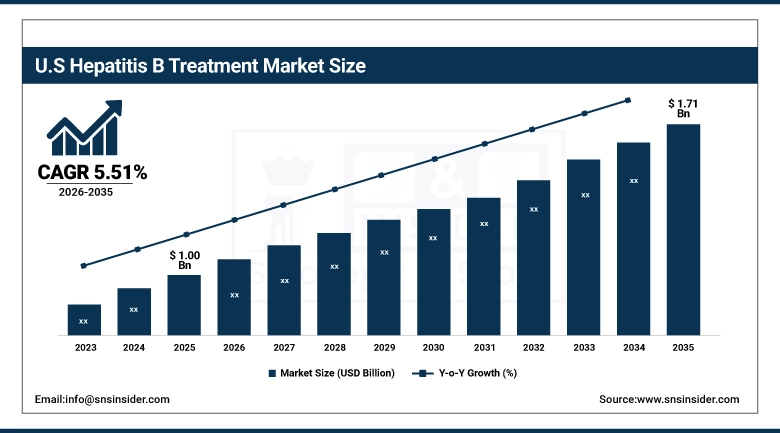

The U.S. Hepatitis B Treatment Market is projected to grow from USD 1.00 Billion in 2025 to USD 1.71 Billion by 2035, at a CAGR of 5.51%. Market growth is supported by strong screening programs, widespread antiviral adoption, favorable reimbursement policies, and continued investment in advanced and long-term hepatitis B therapies.

Hepatitis B Treatment Market Growth Drivers:

-

Expanding hepatitis B screening programs and long-term antiviral therapy adoption driving sustained treatment market growth.

Expanding hepatitis B screening programs are a major driver of Hepatitis B Treatment Market growth. Increased early diagnosis through government-led awareness initiatives and routine testing is identifying a larger treated patient population. As hepatitis B requires long-term antiviral therapy, improved detection directly translates into sustained treatment demand. Enhanced access to healthcare facilities, reimbursement support and standardized treatment guidelines are further encouraging therapy initiation, adherence and continuity across both developed and emerging healthcare systems.

Hepatitis B treatment uptake increased by over 7% in 2025, driven by expanded screening coverage and rising initiation of long-term antiviral therapy among newly diagnosed patients.

Hepatitis B Treatment Market Restraints:

-

High treatment costs and limited healthcare access in emerging regions are restraining Hepatitis B market growth.

High treatment costs and limited healthcare access pose significant restraints for the Hepatitis B Treatment Market. Antiviral therapies often require long-term administration, making them expensive for patients in low- and middle-income regions. Limited hospital infrastructure, inadequate insurance coverage and uneven distribution of medical facilities further restrict treatment accessibility. These challenges hinder therapy initiation and adherence, particularly in rural and underserved areas, slowing market growth. Consequently, affordability and healthcare inequities remain major barriers for expanding the Hepatitis B treatment landscape.

Hepatitis B Treatment Market Opportunities:

-

Growing pipeline of novel antiviral and immune-based therapies offers significant opportunities for advanced Hepatitis B treatment solutions.

Growing pipeline of novel antiviral and immune-based therapies presents a major opportunity for the Hepatitis B Treatment Market. Advances in RNA-based drugs, capsid assembly modulators and combination therapies are expanding treatment options and improving patient outcomes. Pharmaceutical companies are investing in innovative formulations to enhance efficacy, reduce resistance and support long-term disease management. This shift toward next-generation therapies helps drive market differentiation, improve patient adherence and create new avenues for sustained growth in the hepatitis B treatment landscape.

Novel antiviral therapies accounted for 28% of Hepatitis B treatment developments in 2025, driven by demand for effective long-term management.

Hepatitis B Treatment Market Segmentation Analysis:

-

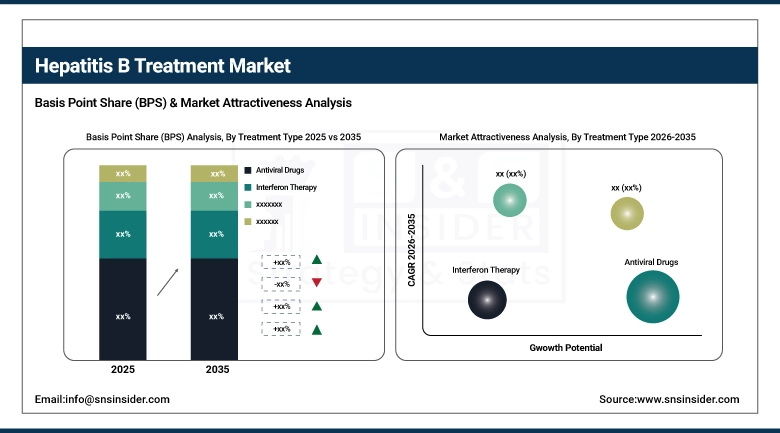

By Treatment Type, Antiviral Drugs held the largest market share of 52.36% in 2025, while Emerging & Novel Therapies are expected to grow at the fastest CAGR of 9.12% during 2026–2035.

-

By Drug Class, Nucleos(t)ide Analogues accounted for the highest market share of 48.87% in 2025, while RNA Interference (RNAi) Therapies are projected to expand at the fastest CAGR of 9.55% during the forecast period.

-

By Disease Type, Chronic Hepatitis B dominated with a 61.45% share in 2025, while Decompensated Cirrhosis is anticipated to record the fastest CAGR of 8.90% through 2026–2035.

-

By Route of Administration, Oral held the largest share of 69.33% in 2025, while Injectable is expected to grow at the fastest CAGR of 8.65% during 2026–2035.

-

By End-User, Hospitals accounted for the largest share of 57.12% in 2025, while Liver Care Centers are forecasted to register the fastest CAGR of 9.02% during 2026–2035.

-

By Distribution Channel, Hospital Pharmacies held the largest share of 54.45% in 2025, while Online Pharmacies are expected to grow at the fastest CAGR of 9.25% during 2026–2035.

By Treatment Type, Antiviral Drugs Dominate While Emerging & Novel Therapies Expand Rapidly:

Antiviral Drugs segment dominated the market due to its proven efficacy, widespread adoption and long-term use in managing both acute and chronic hepatitis B patients. With strong physician preference and established treatment guidelines, antiviral drugs accounted for over 16 million treated patients in 2025.

Emerging & Novel Therapies are the fastest-growing segment, reflecting increasing investments in RNA-based, immune-modulating and capsid assembly therapies. In 2025, around 4.2 million patients received novel therapies, highlighting the shift toward advanced treatment options.

By Drug Class, Nucleos(t)ide Analogues Dominate While RNA Interference (RNAi) Therapies Expand Rapidly:

Nucleos(t)ide Analogues segment dominated the market due to their high antiviral potency, oral administration convenience and long-term safety profile. These therapies have become standard care for chronic hepatitis B management, treating over 15 million patients in 2025.

RNA Interference (RNAi) Therapies are the fastest-growing segment, driven by technological innovation, improved efficacy and targeted viral suppression. In 2025, 3.8 million patients were enrolled in RNAi-based therapy programs, demonstrating the increasing adoption of next-generation antiviral treatments across clinical and research settings.

By Disease Type, Chronic Hepatitis B Dominates While Decompensated Cirrhosis Expands Rapidly:

Chronic Hepatitis B segment dominated the market due to its high prevalence and long-term treatment requirements, with over 18 million diagnosed patients receiving therapy in 2025. The segment benefits from continuous monitoring and guideline-driven antiviral therapy adoption.

Decompensated Cirrhosis is the fastest-growing segment as advanced liver disease management improves, supported by novel therapies and combination regimens. Around 2.5 million patients with decompensated cirrhosis received specialized treatment in 2025, highlighting the rising clinical focus on severe hepatitis B complications.

By End-User, Hospitals Dominate While Liver Care Centers Expand Rapidly:

Hospitals segment dominated the market as the primary point for diagnosis, treatment initiation and long-term therapy management, with more than 17 million patients receiving treatment through hospital facilities in 2025. Comprehensive monitoring and infrastructure support make hospitals the preferred treatment setting.

Liver Care Centers are the fastest-growing segment, focusing on specialized hepatitis management, advanced therapies and patient adherence programs. In 2025, around 3.5 million patients were treated in liver care centers, highlighting the rising demand for specialized, focused hepatitis B care.

By Distribution Channel, Hospital Pharmacies Dominate While Online Pharmacies Expand Rapidly:

Hospital Pharmacies segment dominated the market due to centralized supply chains, insurance coverage and accessibility for long-term therapy, dispensing treatments to over 16.5 million patients in 2025.

Online pharmacies are the fastest-growing segment, driven by digital health adoption, convenience and direct-to-patient delivery models. In 2025, 3.7 million patients accessed hepatitis B therapies through online platforms, reflecting evolving healthcare trends and the increasing role of e-pharmacies in expanding treatment reach.

Hepatitis B Treatment Market Regional Analysis:

North America Hepatitis B Treatment Market Insights:

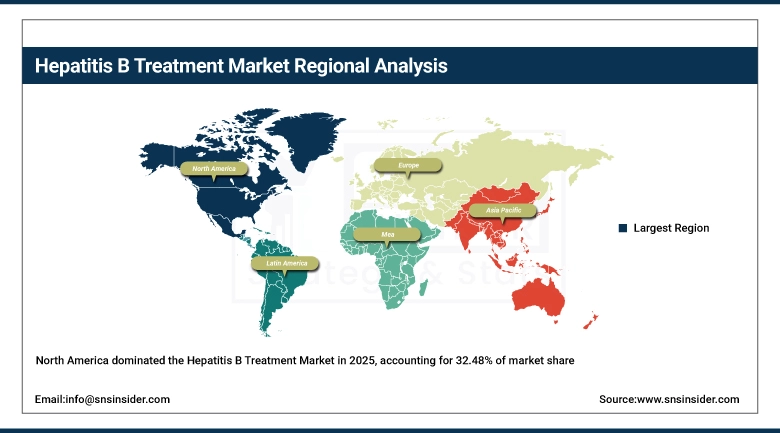

North America dominated the Hepatitis B Treatment Market, accounting for 32.48% of the market share in 2025. Strong healthcare infrastructure, widespread screening programs and early adoption of advanced antiviral therapies are key growth drivers. High awareness levels, favorable reimbursement policies and the presence of leading pharmaceutical companies further support market leadership. Additionally, robust clinical research activity and access to novel treatment options position North America as a central hub for hepatitis B treatment innovation and long-term disease management.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Hepatitis B Treatment Market Insights:

The U.S. Hepatitis B Treatment Market is driven by high disease awareness, widespread screening programs and early adoption of advanced antiviral therapies. Strong healthcare infrastructure, favorable insurance coverage and robust clinical research activity support long-term treatment adherence, reinforcing the country’s dominant position in the North American hepatitis B treatment landscape.

Asia-Pacific Hepatitis B Treatment Market Insights:

The Asia-Pacific Hepatitis B Treatment Market is the fastest growing region, projected to expand at a CAGR of 8.65% during the forecast period. Growth is driven by high disease prevalence, expanding government-led screening initiatives and improving access to antiviral therapies across China, India, Southeast Asia and South Korea. Increasing healthcare investments, rising awareness and growing availability of affordable treatments are accelerating therapy adoption, positioning Asia-Pacific as a key growth engine for the hepatitis B treatment market.

China Hepatitis B Treatment Market Insights:

China’s Hepatitis B Treatment Market is driven by high disease prevalence, expanding national screening programs and improving access to antiviral therapies. Strong government healthcare initiatives, rising awareness and increasing availability of affordable generic and advanced treatments position China as a major growth contributor within the Asia-Pacific hepatitis B treatment market.

Europe Hepatitis B Treatment Market Insights:

The Europe Hepatitis B Treatment Market is growing due to rising disease awareness, improved screening programs and strong public healthcare systems. Countries such as Germany, the UK, France and Italy are leading contributors, supported by favorable reimbursement policies and access to advanced antiviral therapies. Increasing focus on early diagnosis, long-term disease management and expanding hospital and specialty clinic networks reinforces Europe’s role as a key regional market.

Germany Hepatitis B Treatment Market Insights:

Germany is a key Hepatitis B treatment market, supported by strong healthcare infrastructure, high disease awareness and robust screening programs. Widespread access to antiviral therapies, favorable reimbursement policies and emphasis on early diagnosis and long-term disease management strengthen Germany’s position within the European hepatitis B treatment landscape.

Latin America Hepatitis B Treatment Market Insights:

The Latin America Hepatitis B Treatment Market is witnessing steady growth driven by rising disease awareness, expanding vaccination and screening programs and improving healthcare access. Countries such as Brazil, Mexico and Argentina are key contributors, supported by increasing availability of antiviral therapies and government-led initiatives to strengthen hepatitis prevention and long-term treatment coverage.

Middle East and Africa Hepatitis B Treatment Market Insights:

The Middle East & Africa Hepatitis B Treatment Market is expanding due to increasing disease awareness, improving screening initiatives and rising healthcare investments. Growing access to antiviral therapies and government-led public health programs in countries such as Saudi Arabia, the UAE and South Africa are supporting gradual treatment adoption and regional market growth.

Hepatitis B Treatment Market Competitive Landscape:

Gilead Sciences, Inc., headquartered in Foster City, California, is a biopharmaceutical leader specializing in antiviral therapies for HIV, hepatitis and other viral infections. In the hepatitis B treatment market, Gilead dominates with nucleotide analogues such as Viread (tenofovir disoproxil fumarate) and Vemlidy (tenofovir alafenamide), recommended for chronic HBV management. Strong research and development, access programs and pediatric and adult treatment expansions have helped Gilead maintain leadership. Strategic collaborations, patient support programs and a focus on long-term therapy adherence strengthen its position in the antiviral market.

- In May 2025, Gilead announced final Phase 3 MYR301 data showing that prolonged treatment with bulevirtide helped many with chronic HDV maintain undetectable viral levels nearly two years after therapy ended, advancing viral hepatitis research.

GlaxoSmithKline plc (GSK), headquartered in London, UK, is a major pharmaceutical company operating across vaccines, specialty medicines and consumer healthcare. In hepatitis B treatment, GSK has significantly influenced the market through antiviral products such as Zeffix (lamivudine) and licensing agreements for Viread (tenofovir) in key territories. The company also invests in next-generation therapies, including investigational agents such as bepirovirsen, targeting chronic HBV. Strong R&D capabilities, strategic partnerships and access programs enable GSK to deliver effective HBV treatments while expanding its footprint in antiviral care.

- In November 2025, GSK presented new liver pipeline data at AASLD 2025, including bepirovirsen sub‑analysis showing durability of functional cure in chronic hepatitis B patients, promising improved treatment outcomes and reinforcing its ongoing development progress.

Bristol‑Myers Squibb, headquartered in New York, USA, is a biopharmaceutical company recognized for its R&D in oncology, immunology and virology. In hepatitis B treatment, BMS leads with Baraclude (entecavir), a first-line oral antiviral for chronic HBV infection used. Its efficacy in viral suppression and inclusion in international guidelines reinforce BMS’s market presence. Combined with ongoing research for novel liver disease therapies, robust clinical programs and a focus on improving patient outcomes, BMS continues to maintain a strong position in the hepatitis B treatment market.

- In November 2025, Bristol‑Myers Squibb’s BARACLUDE (entecavir) therapy was newly marketed with updated product labeling reflecting its availability as an oral formulation approved for chronic hepatitis B treatment in adults and pediatric patients aged 2+, reinforcing long‑term suppression and broader treatment accessibility in markets.

Hepatitis B Treatment Market Key Players:

-

Gilead Sciences, Inc.

-

GlaxoSmithKline plc (GSK)

-

Bristol‑Myers Squibb Company

-

Merck & Co., Inc.

-

F. Hoffmann‑La Roche Ltd

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Novartis AG

-

AbbVie Inc.

-

Dynavax Technologies Corporation

-

Alnylam Pharmaceuticals, Inc.

-

Arbutus Biopharma Corporation

-

Assembly Biosciences, Inc.

-

VBI Vaccines Inc.

-

Zydus Cadila (Zydus Lifesciences)

-

Cipla Limited

-

Teva Pharmaceutical Industries Ltd.

-

Dr. Reddy’s Laboratories Ltd.

-

Viatris Inc. (Mylan)

-

Accord Healthcare (Intas)

-

Apotex Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.52 Billion |

| Market Size by 2035 | USD 8.87 Billion |

| CAGR | CAGR of 6.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Antiviral Drugs, Interferon Therapy, Combination Therapy, Emerging & Novel Therapies, Others) • By Drug Class (Nucleos(t)ide Analogues, Immune Modulators, Capsid Assembly Modulators, RNA Interference (RNAi) Therapies, Entry Inhibitors, Others) • By Disease Type (Acute Hepatitis B, Chronic Hepatitis B, Compensated Cirrhosis, Decompensated Cirrhosis) • By Route of Administration (Oral, Injectable, Parenteral, Others) • By End-User (Hospitals, Specialty Clinics, Liver Care Centers, Homecare Settings, Research & Academic Institutes, Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Gilead Sciences, Inc., GlaxoSmithKline plc (GSK), Bristol Myers Squibb Company, Merck & Co., Inc., F. Hoffmann La Roche Ltd, Johnson & Johnson (Janssen Pharmaceuticals), Novartis AG, AbbVie Inc., Dynavax Technologies Corporation, Alnylam Pharmaceuticals, Inc., Arbutus Biopharma Corporation, Assembly Biosciences, Inc., VBI Vaccines Inc., Zydus Cadila (Zydus Lifesciences), Cipla Limited, Teva Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Viatris Inc. (Mylan), Accord Healthcare (Intas), Apotex Inc. |

Frequently Asked Questions

The Hepatitis B Treatment Market is valued at USD 4.52 billion in 2025, reflecting the growing demand for antiviral therapies, diagnostic monitoring, and long-term disease management solutions.

The market is projected to reach USD 8.87 billion by 2035, driven by increasing hepatitis B prevalence, advancements in treatment options, and improved healthcare access globally.

The market is expected to grow at a CAGR of 6.97% during the forecast period 2026–2035, indicating steady expansion in the global treatment landscape.

Key growth drivers include the rising global burden of chronic hepatitis B infections, growing awareness about early diagnosis, increasing use of antiviral drugs, and supportive government screening programs.

Common treatment options include antiviral medications such as tenofovir, entecavir, and interferon-based therapies, which help suppress viral replication and reduce liver damage.

Get in Touch