Homeopathy Market Report Scope & Overview:

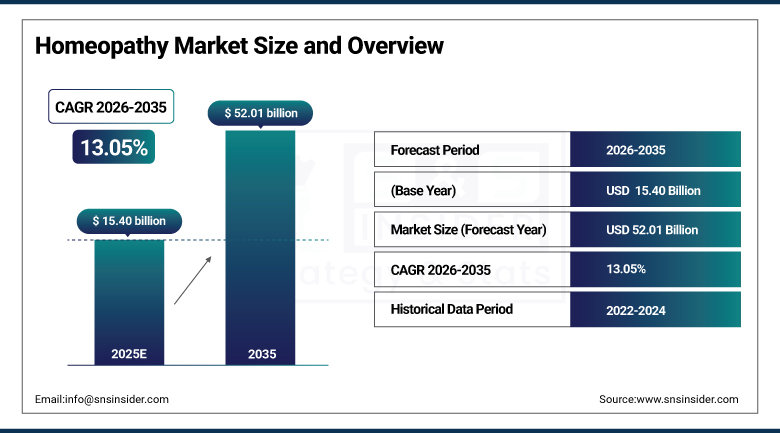

The Homeopathy Market was valued at USD 15.40 Billion in 2025 and is expected to reach USD 52.01 Billion by 2035, growing at a CAGR of 13.05% from 2026–2035.

Homeopathy is one of the most popularly practiced forms of alternative medicine with around 500 million users across over 80 countries in the world. One of the major underlying principles of the practice is that natural substances taken in very high dilutions can trigger the body's self-healing mechanism. Homeopathic remedies are created by taking natural sources such as plants, minerals, and animals and subjecting them to a process known as serial dilution and succussion. Homeopathy is gaining popularity alongside the general trend of using natural and non-toxic medicines that produce no side effects whatsoever. This goes hand in hand with the general trend towards moving away from relying on pharmaceuticals for dealing with chronic and everyday health problems by health-conscious consumers in the world. There are two major market environments in which homeopathy operates.

India has over 200,000 registered homeopathic practitioners and more than 200 medical colleges offering homeopathy degrees. The Ministry of AYUSH formally recognizes homeopathy as a mainstream healthcare system, creating a regulated commercial framework that no other country fully matches in institutional depth.

Market Size and Forecast

-

Market Size in 2026E: USD 17.24 Billion

-

Market Size by 2035: USD 52.01 Billion

-

CAGR: 13.05% from 2026 to 2035

-

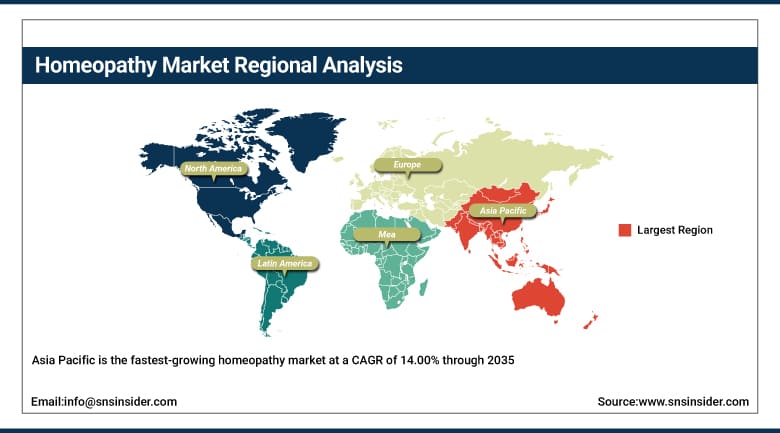

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get More Information On Homeopathy Market - Request Free Sample Report

Homeopathy Market Trends

-

Consumer demand for natural, minimally processed health products is driving homeopathy adoption as buyers reduce their dependence on conventional OTC pharmaceuticals for everyday ailment management and preventive health support.

-

Online pharmacy platforms and direct-to-consumer health websites are expanding homeopathic product access to consumer segments in markets where homeopathy lacks established retail pharmacy distribution.

-

Product innovation in combination remedy formulations targeting stress, sleep disruption, seasonal allergy, and digestive discomfort is driving faster segment growth than traditional single-ingredient homeopathic dilutions in most markets.

-

Regulatory recognition of homeopathy is expanding in Asia Pacific as Thailand, South Korea, and several Southeast Asian nations create formal registration frameworks that improve international brand market access.

-

Alternative medicine integration within private healthcare networks is growing as wellness clinics, integrative medicine centers, and corporate employee health programmes add homeopathy to their service and product offerings.

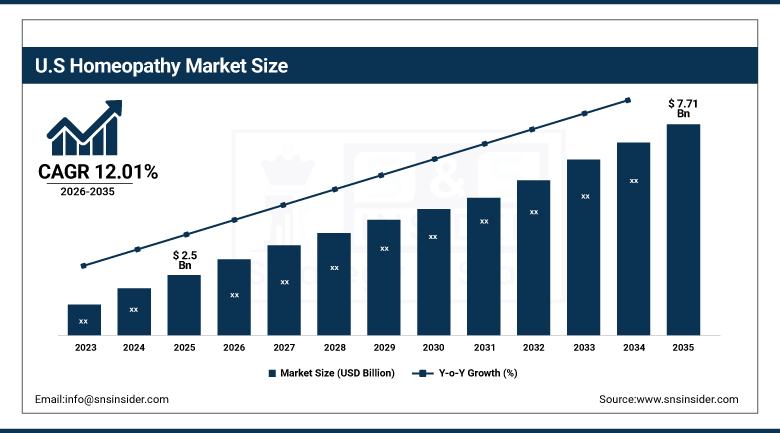

The U.S. Homeopathy Market Outlook

The U.S. Homeopathy Market was valued at approximately USD 2.5 Billion in 2025 and is expected to reach approximately USD 7.71 Billion by 2035, growing at a CAGR of 12.01%.

The U.S. is the second largest market for homeopathic drugs globally in terms of revenues. OTC homeopathic remedies for symptoms such as cough, cold, pain, sleep aid, and pediatric use can be found at major retail outlets like CVS, Walgreens, and Walmart as well as natural food stores. Hyland’s Homeopathic and Boiron are the leading brands. The FDA regulation of homeopathic products under the OTC drug paradigm has been increasingly progressive. The FDA’s risk-based regulatory strategy enhanced product regulation without taking out commercialized products from store shelves.

Hyland's introduced its first children's multivitamin collection in April 2025, offering three sugar-free gummy formulas targeting brain and eye health, digestive support, and immunity. This launch reflects the brand's expansion beyond traditional single remedies into the broader children's wellness supplement market.

Homeopathy Market Segment Analysis

-

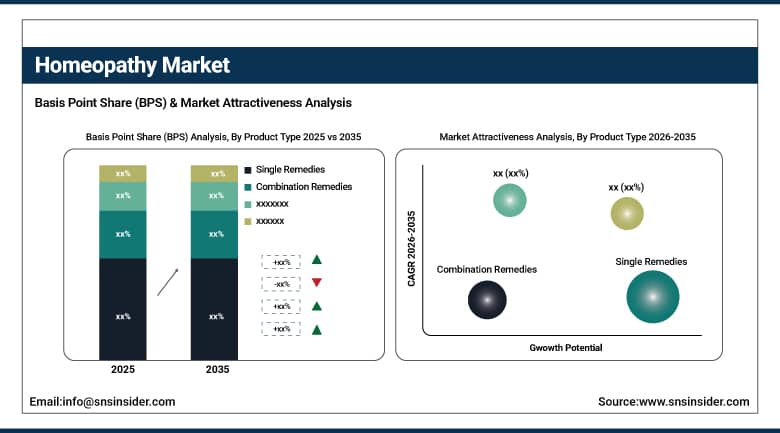

By Product Type, Single Remedies dominated with approximately 60.1% share in 2025; Combination Remedies are the fastest-growing at a CAGR of 14.14%, driven by consumer preference for symptom-targeted multi-ingredient formulations suited to OTC self-selection.

-

By Form, Tablets and Pills held the largest share of approximately 41.3% in 2025; Tablets and Pills are also the fastest-growing form.

-

By Application, Analgesics & Anti-Inflamatory dominated with approximately 26.9% share in 2025; Respiratory Disorders is the fastest-growing segment at a CAGR of 14.41%.

-

By End User, Home Users and Consumers dominated with approximately 63.7% share in 2025; Alternative Medicine Centers are the fastest-growing end user at a CAGR of 14.08% as integrative health clinics expand consultation services.

-

By Distribution Channel, Retail Pharmacies dominated with approximately 51.4% share in 2025; Online Pharmacies are the fastest-growing channel as digital health retail expands global consumer reach.

By Product Type, single remedies dominate, combination remedies grow fastest

Single Remedy accounted for about 64.87% share in the homeopathy market in 2025. Single remedy refers to products containing only one homeopathic active ingredient in a specific potency and formulated to treat symptoms characteristic of the corresponding classical indication. The popularity of single remedies is explained by the time-proven tradition in homeopathic medicine when each practitioner prescribes only one remedy tailored to the symptoms experienced by the patient. Being more familiar to the market in general, single remedy is a format with the longest commercial history in well-established homeopathic countries such as Germany, France, India, and Brazil.

Combination remedies will grow rapidly at a CAGR of 13.58% during 2025-2035. Combination remedies are products consisting of several homeopathic active ingredients and treating specific symptom clusters including cold and flu, seasonal allergy, difficulties sleeping, and problems with digestion. Unlike other types of remedies, combination remedies do not require professional guidance in selection, as they are sold directly to consumers. Therefore, combination remedies are best suited for over-the-counter sale in retail settings where clear indication-based labeling facilitates the customer's purchase decision.

By End User, home users dominate, alternative medicine centers grow fastest

The home users & consumers accounted for about 43.52% of the share of the total revenue of the homeopathy market in 2025. The homeopathic tradition has a very long history as a practice that is applied by individuals for themselves in self-care mode to manage their general health on their own. OTC homeopathic remedies are being extensively used for teething, common cold symptoms, motion sickness, insomnia, and daily stress across millions of homes in Europe, India, North America, and Latin America.

Alternative Medicine Centersemerged as the fastest-growing category of the end-users' segment with a CAGR of 13.77%. The growth in this segment is attributable to an increase in the number of Integrative medicine clinics, Naturopathic health clinics, and Functional Medicine practices where homeopathic therapy is used as one among the several forms of treatment offered for patients. Such patients typically suffer from chronic illness that cannot be managed through conventional means.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.68% |

|

Europe |

Germany |

24.22% |

|

Asia Pacific |

India |

47.71% |

|

Middle East & Africa |

South Africa |

23.81% |

|

Latin America |

Brazil |

46.45% |

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Homeopathy Market Insights

North America was estimated to be one of the leading the homeopathy market around the world in 2025 with approximately 18.55% of total revenue share. The U.S., as the largest OTC homeopathy market in the world, represents approximately 87.68% of the North American market revenue share. The U.S. market features good OTC distribution via pharmacy chain stores, health food stores, and online channels. The most popular brands in the market are Hyland's and Boiron. The consumer healthcare segment in the U.S. has a high inclination towards natural products especially after the increase in holistic health practices post-pandemic times. Canadians have a highly developed naturopathic and integrative medicine industry which leads to higher consumption of homeopathic medicines in Canada on a per capita basis. FDA regulation changes have increased the clarity in the U.S. homeopathy market. Those products that comply with the existing safety and quality standards continue to maintain their market positions. New products face better-defined approval processes.

Europe Homeopathy Market Insights

The continent of Europe dominated the market for homeopathy with well-integrated institutions in Germany, France, Switzerland, and UK. In Germany, about 28.4% of the continent's income comes from the fact that there is a well-established history of prescriptive use of homeopathic products by physicians, statutory health insurance payment for homeopathic products in specified areas, and the presence of large-scale manufacturers of homeopathic products like Heel GmbH and Deutsche Homöopathie-Union. Europe's market is more scientifically credible than that of the United States. Doctors in Germany and France prescribe these products on a regular basis as part of conventional medical practice. The regulatory debate over homeopathic claims exists in some European countries such as the exclusion of homeopathic drugs from pharmacy reimbursement in Sweden and exclusion of GP prescribing of homeopathy by the NHS of the UK since 2017. Retail demand is high in the region.

Asia Pacific Homeopathy Market Insights

Asia Pacific is the fastest-growing homeopathy market at a CAGR of 15.53% through 2035. India accounts for approximately 47.71% of Asia Pacific revenues and is the world's single largest homeopathy market by practitioner count and institutional depth. India has over 200,000 registered homeopathic doctors, more than 200 homeopathic medical colleges, and a Ministry of AYUSH providing formal government support to homeopathic practice and product regulation. Major Indian manufacturers including Dr Reckeweg, SBL Pvt. Ltd., and Medisynth operate at commercial scale serving both domestic and export markets across Asia and the Middle East.

MEA & Latin America Homeopathy Market Insights

MEA countries such as the Middle East, Africa, and Latin America present growth opportunities for homeopathic medicines due to increasing consumer preferences for natural healthcare and the development of the retail distribution infrastructure. South Africa ranks first in terms of MEA revenues by taking up about 28.6% share on account of its traditional homeopathic practice culture and advanced health food retail segment. The leading country in Latin America is Brazil, accounting for about 46.45% of region revenues on the basis of its regulated homeopathic dispensary market system and traditional plant medicine usage culture.

Market Dynamics

Growth Drivers: Rising consumer preference for natural health products with minimal side effects and growing chronic disease prevalence are the primary growth drivers for the homeopathy market.

Skepticism among consumers concerning the side effects of medication is on the rise. Growing concerns over antibiotic resistance, pain killer addiction, and negative reactions to medications discussed through various health sources have contributed to a sizable number of consumers considering natural health remedies. These factors benefit homeopathy in several ways. Firstly, consumers see it as a treatment that is both gentle and free from any toxins or side effects associated with conventional pharmaceuticals. The strength of this belief is seen particularly in parents choosing health products for their children and older consumers dealing with multiple chronic illnesses at once. Prevalence rates of chronic illnesses are on the rise in every major market.

Restraints: Scientific controversy over mechanism of action, regulatory restrictions in key Western markets, and limited insurance reimbursement are restraining homeopathy market expansion.

The controversy regarding the effectiveness of homeopathic medications apart from the placebo effect remains one of the greatest business threats to the industry. Major assessments undertaken by the Australian National Health and Medical Research Council and NHS in the UK have found little evidence suggesting that homeopathy proves effective beyond the placebo effect for any health disorder. Such assessments lead to increased pressure on companies marketing such drugs. The insurance cover for such drugs has been curtailed in countries such as Sweden, the UK and parts of Germany. Every such move lowers institutional credibility and impacts demand from prescriber segment. Market regulations differ across countries, which pose additional challenges for cross-border homeopathy products. Product registration norms are different in the EU, the US, India, and the Asia Pacific markets.

Opportunities: Digital health platform expansion, growing sports and wellness segment adoption, and regulatory recognition in new Asian markets are the key homeopathy market growth opportunities.

The use of digital health platforms is changing the way homeopathy is being delivered and consultations take place. Digital consultation services for homeopathy have already been set up in countries such as India, Germany, France, and even the U.S. Such services include video consultation followed by prescription on the computer, as well as delivery of homeopathy remedy packages at home. The digital platform for homeopathy consultation from Dr Batra's was launched in Malaysia in April 2025, bringing its successful India model to a new Southeast Asia market. Digital services will make consultation more accessible to people, reduce consultation costs, and allow consultation even when physical presence is impossible due to geographical distances. Sports and wellness are a relatively untapped area commercially.

Recent Developments:

-

April 2025: Hyland's Homeopathic launched its first children's multivitamin collection with three sugar-free gummy formulas targeting brain and eye health, digestive support, and immunity, extending the brand into the children's wellness supplement category.

-

April 2025: Dr Batra's Healthcare launched its Virtual Homoeopathy Clinic in Malaysia, extending its digital consultation and home delivery model from India into Southeast Asia and establishing a commercial template for regional expansion.

-

2025: Boiron expanded its Arnica Montana topical product range in North American sports and recovery retail, reporting above-average growth as consumer interest in natural sports recovery products grew throughout the year.

Homeopathy Market Key Players are:

-

Boiron SA

-

Hyland's Homeopathic (Standard Homeopathic Company)

-

Heel GmbH

-

SBL Pvt. Ltd.

-

Dr Reckeweg & Co. GmbH

-

Medisynth Chemicals Pvt. Ltd.

-

Schwabe India Pvt. Ltd.

-

Dolisos Laboratories

-

Nelson & Co. Ltd.

-

Helios Homeopathy Ltd.

-

DHU (Deutsche Homöopathie-Union)

-

Dr Batra's Healthcare

-

Weleda AG

-

Homeolab USA

-

Similasan Corporation

-

B&T Homeopathic (Bhargava Phytolab)

-

A. Nelson & Company

-

Bakson Drugs & Pharmaceuticals Pvt. Ltd.

-

Allen Laboratories Ltd.

-

Reckeweg & Co. GmbH

Homeopathy Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.40 Billion |

| Market Size by 2035 | USD 52.01 Billion |

| CAGR | CAGR of 13.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Single Remedies, Combination Remedies) • By Form (Tablets/Pills, Dilutions/Liquids, Ointments/Creams, Others) • By Application (Analgesics & Anti-Inflammatory, Respiratory Disorders, Digestive Disorders, Dermatology, Others) • By End User (Home Users/Consumers, Hospitals, Alternative Medicine Centers, Others) • By Distribution Channel (Retail Pharmacies, Online Pharmacies, Homeopathic Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Boiron SA, Hyland's Homeopathic, Heel GmbH, SBL Pvt. Ltd., Dr. Reckeweg & Co. GmbH, Medisynth Chemicals Pvt. Ltd., Schwabe India Pvt. Ltd., Dolisos Laboratories, Nelson & Co. Ltd., Helios Homeopathy Ltd., DHU (Deutsche Homöopathie-Union), Dr Batra's Healthcare, Weleda AG, Homeolab USA, Similasan Corporation, B&T Homeopathic, A. Nelson & Company, Bakson Drugs & Pharmaceuticals Pvt. Ltd., Allen Laboratories Ltd., Reckeweg & Co. GmbH. |

Frequently Asked Questions

North America dominated the Homeopathy Market in 2025, holding approximately 35.54% of global revenues.

Single Remedies dominated with approximately 64.87% of revenues in 2025.

Rising consumer preference for natural health products with minimal side effects is the primary driver. Growing chronic disease prevalence is also expanding the population seeking complementary health approaches alongside conventional treatment.

The Homeopathy Market was valued at USD 15.39 Billion in 2025.

The Homeopathy Market is expected to grow at a CAGR of 12.94% from 2026 to 2035.

Get in Touch