Hybrid Aircraft Market Report Scope & Overview:

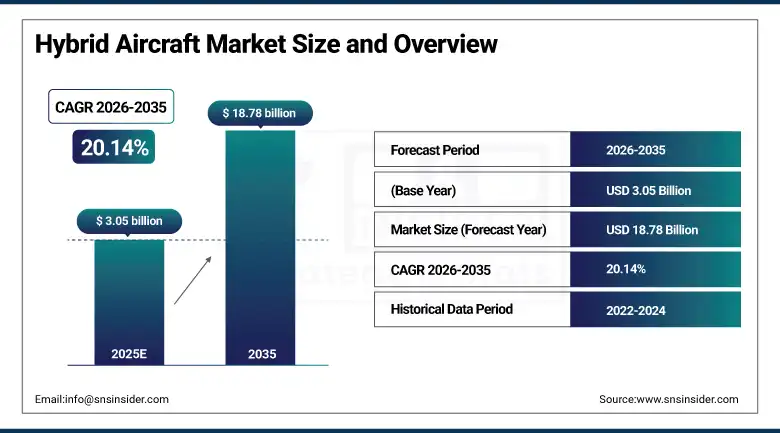

The Hybrid Aircraft Market was valued at USD 3.05 billion in 2025 and is expected to reach USD 18.78 billion by 2035, growing at a CAGR of 20.14% from 2026–2035.

The Hybrid Aircraft Market is witnessing rapid growth due to the increasing need for airlines to adopt greener alternatives as a result of increased pressure from the airline industry to lower carbon emissions, enhance fuel efficiency, and adopt sustainable means of propulsion. The need for decarbonization in aviation, which includes net-zero aviation goals set by international aviation authorities like IATA and ICAO, is driving this trend.

The increasing demand for short-haul regional connectivity and urban air mobility solutions is further fueling market expansion, particularly in densely populated urban regions. Supporting this trend, the International Energy Agency (IEA) highlights that aviation accounts for nearly 2–3% of global CO₂ emissions, reinforcing the urgency for sustainable aviation solutions.

In terms of recent developments, in June 2025, Rolls-Royce Holdings plc and easyJet announced successful hydrogen combustion engine ground testing as part of their zero-emission aviation initiative, while in September 2025, Ampaire Inc. conducted commercial demonstration flights of its hybrid-electric aircraft under the Eco Caravan program, highlighting the rapid progress toward commercialization of hybrid propulsion technologies.

Hybrid Aircraft Market Size and Forecast

-

Market Size in 2025: USD 3.05 Billion

-

Market Size by 2035: USD 18.78 Billion

-

CAGR: 20.14% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Hybrid Aircraft Market - Request Free Sample Report

Hybrid Aircraft Market Trends

-

Rising emphasis on aviation decarbonization and net-zero emission targets is accelerating adoption of hybrid-electric propulsion technologies across commercial and regional aircraft segments.

-

Increasing investments in advanced air mobility (AAM) and eVTOL ecosystems are driving development of next-generation hybrid aircraft for urban and short-haul transportation.

-

Rapid advancements in high-density batteries, hydrogen fuel cells, and energy management systems are improving flight efficiency and extending operational range.

-

Growing demand for short-range and regional connectivity solutions is boosting deployment of hybrid aircraft for cost-efficient and low-emission operations.

-

Expanding government funding, regulatory support, and public-private partnerships are accelerating R&D and commercialization of hybrid aviation technologies.

-

Rising integration of distributed propulsion systems and lightweight composite materials is enhancing aircraft performance, safety, and fuel efficiency.

U.S. Hybrid Aircraft Market Size Outlook:

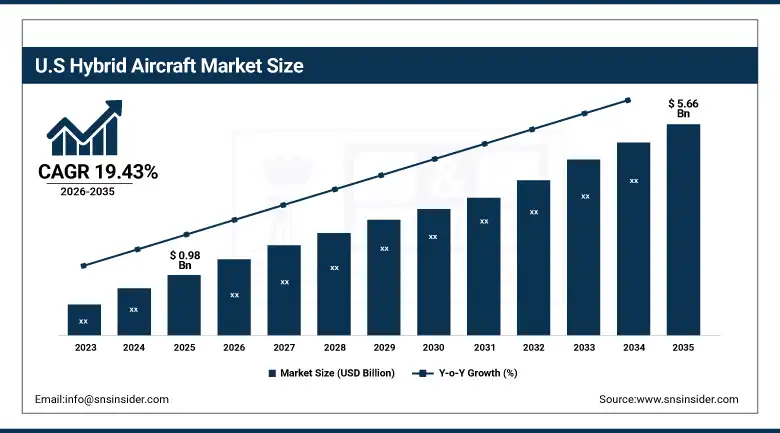

The U.S. Hybrid Aircraft Market was valued at USD 0.98 billion in 2025 and is expected to reach USD 5.66 billion by 2035, growing at a CAGR of 19.43% from 2026–2035. The U.S. market is regarded as one of the largest in the world owing to its robust capability of carrying out aerospace research and development activities, existence of prominent players in the sector including The Boeing Company, GE Aerospace, and RTX Corporation, and substantial investment by the government in green and sustainable aviation technologies

Supporting this trend, the Federal Aviation Administration (FAA) continues to advance certification frameworks for electric and hybrid aircraft, enabling faster commercialization and deployment across regional and urban air mobility segments.

In addition, in 2023, Ampaire Inc. expanded commercial flight trials of its hybrid-electric Eco Caravan, while GE Aerospace and NASA progressed hybrid-electric propulsion testing under the Electrified Powertrain Flight Demonstration (EPFD) program, highlighting accelerating innovation in the U.S. hybrid aviation ecosystem.

Hybrid Aircraft Market Segment Highlights

-

By Aircraft Type, Fixed-Wing Hybrid Aircraft dominated the Hybrid Aircraft Market with 38.36% share in 2025; Advanced Air Mobility (AAM) / eVTOL Hybrid Aircraft fastest growing CAGR

-

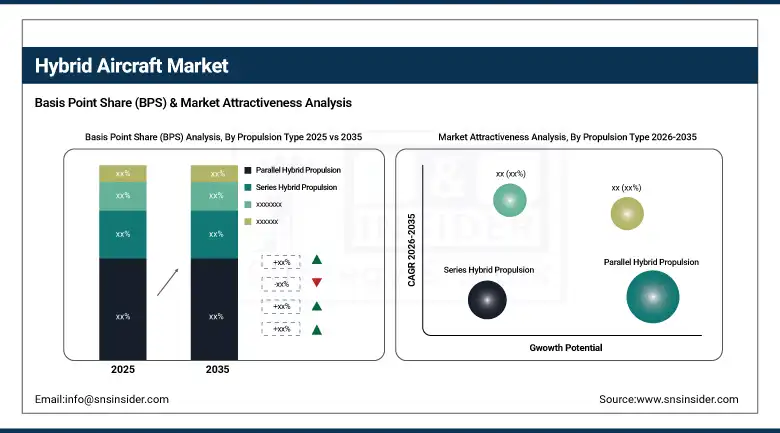

By Propulsion Type, Parallel Hybrid Propulsion dominated the Hybrid Aircraft Market with 41.45% share in 2025; Distributed Hybrid Propulsion Systems fastest growing CAGR.

-

By Energy Source, Battery-Powered Hybrid Systems dominated the Hybrid Aircraft Market with 46.15% share in 2025; Fuel Cell-Based Hybrid Systems (Hydrogen) fastest growing CAGR.

-

By Range, Short-Range (< 500 km) dominated the Hybrid Aircraft Market with 48.24% share in 2025; Long-Range (> 1,500 km) fastest growing CAGR.

-

By Application, Commercial Aviation dominated the Hybrid Aircraft Market with 34.61% share in 2025; Urban Air Mobility (UAM) fastest growing CAGR.

By Aircraft Type, Fixed-Wing Hybrid Aircraft segment dominates the Hybrid Aircraft Market, Advanced Air Mobility (AAM) / eVTOL Hybrid Aircraft segment expected to grow fastest

In 2025, the Fixed-Wing Hybrid Aircraft segment maintained its dominant position in the Hybrid Aircraft Market, accounting for 38.36% of total revenue. This category includes regional aircraft, business jets, and narrow-body platforms that use hybrid propulsion technology. The reason for its dominance is mainly the possibility of converting already existing fixed-wing aircraft into hybrids, which will enable OEMs and users to improve the fuel efficiency of their fleets without replacing the whole fleet.

From 2026 to 2035, the Advanced Air Mobility (AAM) / eVTOL Hybrid Aircraft segment is projected to record the highest CAGR. The rapid emergence of urban air mobility ecosystems, supported by government-backed pilot projects and private investments, is accelerating the commercialization of hybrid-electric vertical takeoff and landing platforms.

By Propulsion Type, Parallel Hybrid Propulsion segment dominates the Hybrid Aircraft Market, Distributed Hybrid Propulsion Systems segment expected to grow fastest

The Parallel Hybrid Propulsion segment held the largest share of 41.45% in the Hybrid Aircraft Market in 2025, It has been spurred on by the fact that it can easily be incorporated into current aircraft engine structures. Such an aircraft propulsion system is designed to ensure that the use of fuel engine and electric motor is simultaneous, thereby increasing fuel efficiency. It dominates due to the fact that it is technologically less complex compared to other types of propulsion systems.

The Distributed Hybrid Propulsion Systems segment is expected to register the highest CAGR of during the 2026–2035 forecast period. This architecture enables multiple electrically driven propulsors distributed across the aircraft structure, significantly improving aerodynamic efficiency, lift distribution, and redundancy.

By Energy Source, Battery-Powered Hybrid Systems segment dominates the Hybrid Aircraft Market, Fuel Cell-Based Hybrid Systems (Hydrogen) segment expected to grow fastest

The Battery-Powered Hybrid Systems segment accounted for the largest share of 46.15% in the Hybrid Aircraft Market in 2025, due to the technological readiness and versatility of its use in various aircraft types. The use of lithium-ion and future solid-state batteries in hybrid powertrain systems is becoming more common in order to partially electrify air travel. The market segment is positively impacted by developments in the field of energy density, efficiency, and durability.

The Fuel Cell-Based Hybrid Systems (Hydrogen) segment is projected to witness the fastest growth, with a CAGR of from 2026 to 2035. Hydrogen-powered fuel cells offer a compelling long-term solution for zero-emission aviation by enabling significantly higher energy efficiency and eliminating direct carbon emissions during operation.

By Range, Short-Range (< 500 km) segment dominates the Hybrid Aircraft Market, Long-Range (> 1,500 km) segment expected to grow fastest

The Short-Range (< 500 km) segment maintained the highest share of 48.24% in the Hybrid Aircraft Market in 2025, motivated by the direct economic profitability of hybrid-electric technology in short-haul flights. Such aircraft are utilized mainly for regional connectivity services, city-to-city air transportation services, and short-haul transport logistics where battery-operated propulsion helps to cut down fuel usage and emissions. The supremacy of this category is justified by relatively low energy needs that enable the use of existing batteries without any impact on payload capabilities.

The Long-Range (> 1,500 km) segment is projected to register the fastest growth, with a CAGR of during the 2026–2035 forecast period.

By Application, Commercial Aviation segment dominates the Hybrid Aircraft Market, Urban Air Mobility (UAM) segment expected to grow fastest

The Commercial Aviation segment held the largest share of 34.61% in the Hybrid Aircraft Market in 2025, backed up by the significant emphasis that the aviation industry places on minimizing operational costs and meeting sustainability goals. Airline companies are increasingly experimenting with hybrid-electric airplanes for short and medium-haul flights to cut down on fuel usage and meet stringent emissions requirements. This category enjoys substantial passenger traffic, an existing network of routes, and the financial ability of airlines to purchase modern technology airplanes.

The Urban Air Mobility (UAM) segment is expected to register the highest CAGR of during the 2026–2035 forecast period.

Hybrid Aircraft Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40.33% |

|

Europe |

Germany |

27.14% |

|

Asia Pacific |

China |

22.75% |

|

Middle East & Africa |

UAE |

6.04% |

|

Latin America |

Brazil |

3.74% |

North America Hybrid Aircraft Market Insights

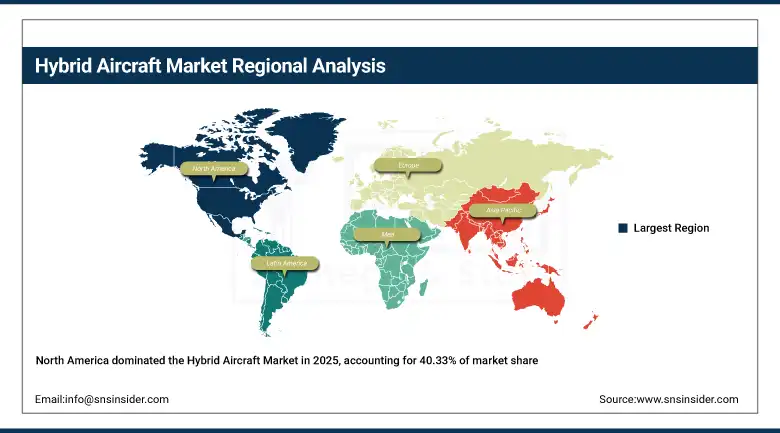

North America held the dominant position in the global Hybrid Aircraft Market with 40.33% revenue share in 2025, driven by its advanced aerospace ecosystem, strong presence of leading OEMs, and extensive government funding for sustainable aviation technologies. The United States leads regional performance with intra-regional share, supported by early-stage adoption of hybrid-electric propulsion systems and large-scale R&D programs. The region benefits from well-established aviation infrastructure, robust defense spending, and active collaboration between aerospace companies and federal agencies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, agencies such as the Federal Aviation Administration (FAA) are actively progressing certification frameworks for electric and hybrid aircraft, enabling smoother commercialization pathways. Additionally, the NASA Electrified Powertrain Flight Demonstration (EPFD) program is accelerating the development of hybrid-electric propulsion technologies through partnerships with industry leaders.

In terms of recent developments, GE Aerospace, in collaboration with NASA, continues advancing hybrid-electric engine testing under the EPFD initiative, while Ampaire Inc. has expanded real-world flight demonstrations of its hybrid-electric Eco Caravan, reinforcing North America’s leadership in hybrid aviation innovation.

Asia Pacific Hybrid Aircraft Market Insights

The Asia Pacific region is anticipated to register the highest CAGR of 22.75% over the forecast period of 2026–2035, Driven by the growth of aviation industry, increased emphasis on sustainability within transportation, and government-supported aerospace programs. Growth will come from China, Japan, India, and South Korea. China has the highest share among other regions because of the demand for air travel in this region. Growth is driven by increased passenger traffic, investments in connectivity, and development of UAM systems in major cities.

Supporting this growth, the Civil Aviation Administration of China (CAAC) is actively promoting electric and hybrid aircraft development as part of its green aviation strategy. Additionally, Japan’s Ministry of Economy, Trade and Industry (METI) is supporting next-generation aircraft propulsion programs through funding and public-private partnerships.

In terms of recent developments, Honda Motor Co., Ltd. is advancing its hybrid-electric aircraft concepts alongside next-generation propulsion research, while regional startups and OEM collaborations are accelerating prototype testing and urban air mobility trials, positioning Asia Pacific as the fastest-evolving hybrid aviation market.

Europe Hybrid Aircraft Market Insights

Europe emerged as the second-biggest market segment for the Global Hybrid Aircraft Market, holding a share of of the overall income generated in the year 2025. This is largely due to strict regulatory measures to ensure decarbonization, along with a high degree of development in aerospace manufacturing in the area. Europe comprises countries like Germany, France, and the UK, which have been taking the lead in hybrid aircraft innovation, owing to their ambitious sustainability goals and R&D collaborations.

Supporting this position, the European Commission continues to fund sustainable aviation programs under initiatives such as Horizon Europe, focusing on hybrid-electric propulsion, hydrogen integration, and next-generation aircraft systems. Additionally, the Clean Aviation Joint Undertaking is accelerating large-scale demonstration projects across the region.

In terms of recent developments, Airbus SE is advancing hybrid-electric propulsion research through its ZEROe and EcoPulse programs, while Rolls-Royce Holdings plc has progressed hybrid and electric propulsion testing initiatives in collaboration with multiple European partners, reinforcing Europe’s position as a global hub for sustainable aviation innovation.

Middle East & Africa (MEA) and Latin America Hybrid Aircraft Market Insights

Both the Middle East & Africa (MEA) and Latin America are displaying a consistent level of early adoption growth within the Hybrid Aircraft Market on the back of increased levels of aviation modernization, rising need for efficient fuel aircraft, and slowly adopting UAVs for commercial and military purposes. Although the two markets are behind North America and Europe in terms of maturity levels, they have become important platforms for testing and implementing hybrid UAVs and advanced aviation systems. Countries like the UAE, Saudi Arabia, and Israel are driving hybrid UAV adoptions across MEA, owing to their aviation diversification and modernization policies.

Supporting this growth, the UAE’s Ministry of Energy and Infrastructure has initiated smart aviation mobility programs that include integration of hybrid-electric aircraft into future urban and intercity transport ecosystems, while Israel Aerospace Industries (IAI) continues to expand hybrid UAV deployment for surveillance, border monitoring, and defense intelligence applications, strengthening regional technological capability.

Brazil’s National Civil Aviation Agency (ANAC) has introduced updated regulatory frameworks to support certification and testing of experimental electric and hybrid aircraft, enabling faster commercialization of innovative aviation technologies across both commercial and defense sectors.

Hybrid Aircraft Market Growth Drivers:

-

Rising demand for low-emission, fuel-efficient aviation and next-generation air mobility solutions accelerating global adoption of hybrid aircraft systems

The move towards the decarbonization of the aviation industry worldwide, increasing fuel efficiency, and the adoption of sustainable flights is the basic underlying structure driving the Hybrid Aircraft Market. There is a growing trend among airlines, military agencies, and developers of urban air mobility to adopt aircraft powered by hybrid engines using electricity along with regular or hydrogen energy to save fuel, reduce costs, and meet carbon emission norms. This has been further encouraged by growing fuel price volatility and the net-zero commitment from governments and key aerospace original equipment manufacturers (OEMs).

Supporting this growth, the International Civil Aviation Organization (ICAO) has reaffirmed its long-term global aviation emissions reduction framework under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which targets carbon-neutral growth from 2020 levels and is pushing airlines toward adoption of hybrid-electric propulsion technologies as a transitional decarbonization pathway.

Further strengthening market momentum, NASA’s Advanced Air Mobility (AAM) program has demonstrated through its X-57 Maxwell electric aircraft project and ongoing distributed electric propulsion research that hybrid-electric configurations can reduce energy consumption significantly while improving aerodynamic efficiency and noise reduction.

Hybrid Aircraft Market Restraints:

-

High capital investment requirements for hybrid propulsion systems, advanced avionics integration, and certification complexity limiting large-scale commercialization of hybrid aircraft

A notable barrier that characterizes the Hybrid Aircraft Market is the very high capital intensity entailed by the research and development, certification, and installation of hybrid propulsion technology. Hybrid aircraft development necessitates heavy investments in electric propulsion technology, energy-rich batteries, fuel cell systems, thermal control, and lightweight composites for airframes. Moreover, hybrid propulsion technology, involving the incorporation of both conventional and electric/hydrogen-powered systems, poses added complications in development and higher costs of production per unit than those entailed in developing conventional aircraft. Such constraints have resulted in the limited adoption of hybrid propulsion aircraft only by leading aerospace firms and defense organizations.

Hybrid Aircraft Market Opportunities:

-

Accelerating development of hybrid-electric propulsion architectures, next-generation hydrogen integration, and distributed energy systems creating large-scale commercialization opportunities across regional aviation, eVTOL networks, and unmanned aerial platforms

The biggest disruptor in the Hybrid Aircraft Market will be the fast integration of hybrid propulsion technology innovations into next-generation urban air and regional air mobility ecosystems. Innovations such as high-energy-density batteries, advanced composite materials in airframes, and modular electric propulsion systems have made it possible to develop hybrid aircraft, which are not only energy-efficient but also economically feasible for short commercial flights as well as logistic missions. Simultaneously, the advent of eVTOL air mobility ecosystems and hybrid UAVs is paving way for a whole host of new applications in aviation, ranging from urban air mobility to medical logistics, offshore operations, and military surveillance.

Recent Developments:

-

2026: Airbus advanced its ZEROe hybrid-hydrogen aircraft program with expanded ground and flight testing of hybrid-electric propulsion architectures for regional aircraft, focusing on short- to medium-haul decarbonization pathways and validating integrated fuel cell–battery energy management systems for future commercial deployment across European routes.

-

2025: Boeing accelerated its Eco Demonstrator hybrid-electric flight-testing program, integrating advanced battery-assisted propulsion modules and sustainable aviation fuel (SAF)–hybrid operational configurations to evaluate fuel burn reduction and emissions performance improvements across next-generation narrow-body aircraft platforms, supporting long-term hybrid certification pathways.

-

2024: NASA progressed its X-57 Maxwell and distributed electric propulsion research initiatives, demonstrating improved aerodynamic efficiency and reduced energy consumption through hybrid-electric aircraft configurations, while providing validated test data to support certification frameworks for advanced hybrid propulsion systems in both civil aviation and urban air mobility applications.

-

2026: Rolls-Royce expanded its Spirit of Innovation hybrid-electric propulsion program with advanced ground testing of turboelectric and battery-assisted engine architectures, focusing on scalable powertrain solutions for regional aircraft and eVTOL platforms, while strengthening partnerships with European aerospace OEMs to accelerate certification pathways for next-generation low-emission hybrid propulsion systems.

Hybrid Aircraft Companies are:

-

Airbus SE

-

RTX Corporation (Pratt & Whitney)

-

General Electric Company (GE Aerospace)

-

Rolls-Royce Holdings plc

-

Safran S.A.

-

Boeing

-

Embraer S.A.

-

BAE Systems plc

-

Zero Avia Inc.

-

Ampaire Inc.

-

Heart Aerospace AB

-

magniX, Inc.

-

Electra.aero

-

VoltAero

-

AURA AERO

-

Vertical Aerospace Group Ltd.

-

Ascendance Flight Technologies

-

Pipistrel Aircraft

-

Wisk Aero

Hybrid Aircraft Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.05 Billion |

| Market Size by 2035 | USD 18.78 Billion |

| CAGR | CAGR of 20.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Aircraft Type (Fixed-Wing Hybrid Aircraft, Rotary-Wing Hybrid Aircraft (Helicopters), Unmanned Aerial Vehicles (Hybrid UAVs), Advanced Air Mobility (AAM) / eVTOL Hybrid Aircraft, Others) • By Propulsion Type (Parallel Hybrid Propulsion, Series Hybrid Propulsion, Turboelectric Hybrid Systems, Distributed Hybrid Propulsion Systems) • By Energy Source (Battery-Powered Hybrid Systems, Fuel Cell-Based Hybrid Systems (Hydrogen), Conventional Fuel + Electric Hybrid Systems, Solar Hybrid Systems, Others) • By Range (Short-Range (< 500 km), Medium-Range (500–1,500 km), Long-Range (> 1,500 km), Others) • By Application (Commercial Aviation, Military & Defense, Urban Air Mobility (UAM), Cargo & Logistics, Surveillance & Reconnaissance) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus SE, RTX Corporation (Pratt & Whitney), General Electric Company (GE Aerospace), Rolls-Royce Holdings plc, Safran S.A., Boeing, Embraer S.A., Textron Inc., BAE Systems plc, ZeroAvia Inc., Ampaire Inc., Heart Aerospace AB, magniX, Inc., Electra.aero, VoltAero, AURA AERO, Vertical Aerospace Group Ltd., Ascendance Flight Technologies, Pipistrel Aircraft, Wisk Aero. |

Frequently Asked Questions

The Hybrid Aircraft Market is expected to grow at a CAGR of 20.14% from 2026 to 2035.

The Hybrid Aircraft Market was valued at USD 3.05 billion in 2025.

Rising global demand for fuel-efficient, low-emission aviation solutions and next-generation sustainable air mobility platforms is the primary growth driver of the Hybrid Aircraft Market.

The Fixed-Wing Hybrid Aircraft segment dominated the Hybrid Aircraft Market in 2025.

North America dominated the Hybrid Aircraft Market in 2025.

Get in Touch