Inflight Entertainment and Connectivity Market Report Scope & Overview:

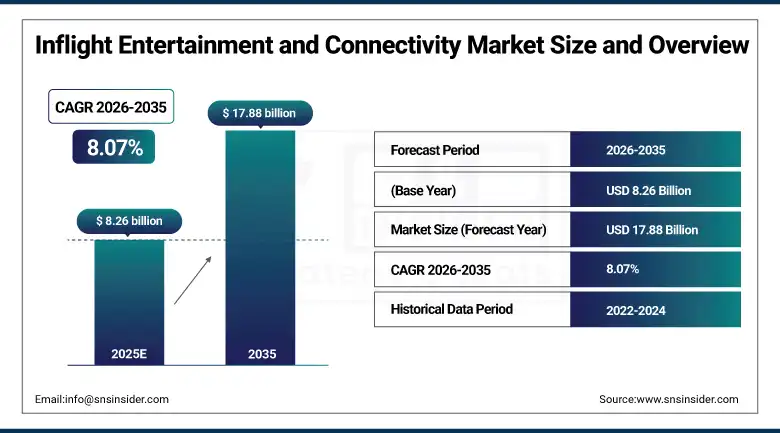

The global Inflight Entertainment and Connectivity Market size is valued at USD 8.26 Billion in 2025 and is projected to reach USD 17.88 Billion by 2035, growing at a CAGR of 8.07% during the forecast period 2026–2035.

Insights on Inflight Entertainment and Connectivity Market report Provide a detailed study of market dynamics, technological innovations, and the integration of advanced connectivity and digital entertainment solutions across commercial and business aircraft platforms. The growth of the market is driven by factors such as rising global air passenger traffic, increasing airline investments in passenger experience enhancement, surging demand for high-speed inflight Wi-Fi and streaming services, advancements in satellite communication technologies, and the rapid adoption of wireless and bring-your-own-device (BYOD) entertainment systems.

The deployment of inflight entertainment and connectivity systems has surpassed 38,000 aircraft installations globally in 2025.

Market Size and Forecast:

-

Market Size in 2025: USD 8.26 Billion

-

Market Size by 2035: USD 17.88 Billion

-

CAGR: 8.07% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Inflight Entertainment and Connectivity Market - Request Free Sample Report

Inflight Entertainment and Connectivity Market Trends:

-

Rising global air passenger traffic and airline investments are driving demand for advanced inflight entertainment and connectivity solutions.

-

Growing adoption of inflight Wi-Fi, streaming, and real-time messaging is enhancing passenger experience and airline ancillary revenues.

-

Next-generation satellite technologies such as LEO and multi-orbit networks are improving bandwidth, latency, and global coverage.

-

Increasing deployment of wireless IFE and BYOD platforms is driving lightweight and cost-efficient onboard entertainment solutions.

-

AI-driven content personalization, targeted advertising, and onboard e-commerce are accelerating IFEC innovation.

-

Rising aircraft retrofit and line-fit installations are boosting adoption across existing and new aircraft fleets.

U.S. Inflight Entertainment and Connectivity Market Insights:

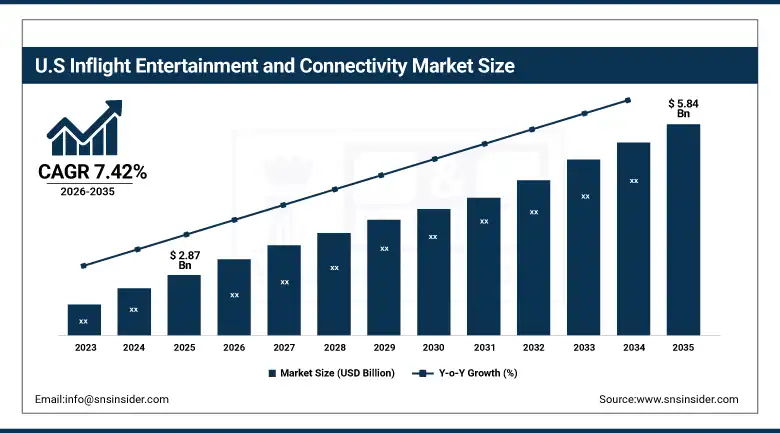

The United States Inflight Entertainment and Connectivity Market is projected to grow from USD 2.87 Billion in 2025 to USD 5.84 Billion by 2035, at a CAGR of 7.42%. Growth will be driven by several factors including the growth of air traffic, increased investment in fast inflight Internet access and premium entertainment solutions by airlines, robust presence of IFEC system providers, fast adoption of next-generation satellite technologies, and extensive retrofit and line fit activities for commercial and business aircraft.

Inflight Entertainment and Connectivity Market Growth Drivers:

-

Increasing adoption of high-speed in-flight digital transformation programs and rising passenger demand for seamless onboard connectivity are driving strong demand for advanced Inflight Entertainment and Connectivity (IFEC) systems.

Amongst other aspects like the fast-paced increase in the number of commercial fleet sizes, along with increased focus on improving passengers’ experience will play an important role in driving growth for the IFEC market. Introduction of future-proof technologies like high throughput satellite (HTS), low latency LEO satellites, personalization powered by AI and cloud video platforms is adding to real-time experiences and driving efficiencies in the process, thus increasing adoption in the market. Implementation of retrofit IFEC technology in narrow-body and wide-body fleet sizes, without the requirement of changing the whole cabin system, is one more aspect that drives the growth.

Over 72% of newly introduced commercial aircraft in 2025 will have connectivity-enabled IFEC systems embedded or line fit.

Inflight Entertainment and Connectivity Market Restraints:

-

High installation cost of advanced Inflight Entertainment and Connectivity (IFEC) systems along with expensive satellite bandwidth and integration expenses are limiting widespread adoption across airline fleets, particularly in cost-sensitive and low-cost carrier segments.

The large amount of capital needed in implementing advanced IFEC solutions such as high-speed satellite connectivity services, onboard infrastructure equipment, seat back entertainment systems, and continual content licensing is one of the main constraints for the industry. Besides that, there are ongoing costs associated with bandwidth usage, upgrading systems, adhering to security requirements, and maintaining them, which further raise the overall cost of implementing connectivity solutions.

Inflight Entertainment and Connectivity Market Opportunities:

-

Rapid expansion of high-speed in-flight connectivity and increasing airline focus on passenger digital engagement are creating strong growth opportunities for the IFEC Market.

As more and more emphasis is being laid on making cabins fully connected using next-generation satellite systems, along with the increased need for personalizing streaming, integrating e-commerce functionalities, and providing real-time travel services, there are emerging new revenue channels for airlines and IFEC solution providers. Hybrid connectivity solutions that combine GEO, LEO, and air-to-ground communications systems are paving the way for continuous global coverage and reliable services.

In 2025, over 61% of all the money spent by global airlines on their digital transformation initiatives will be allocated to making their cabins fully connected.

Inflight Entertainment and Connectivity Market Segmentation Analysis:

-

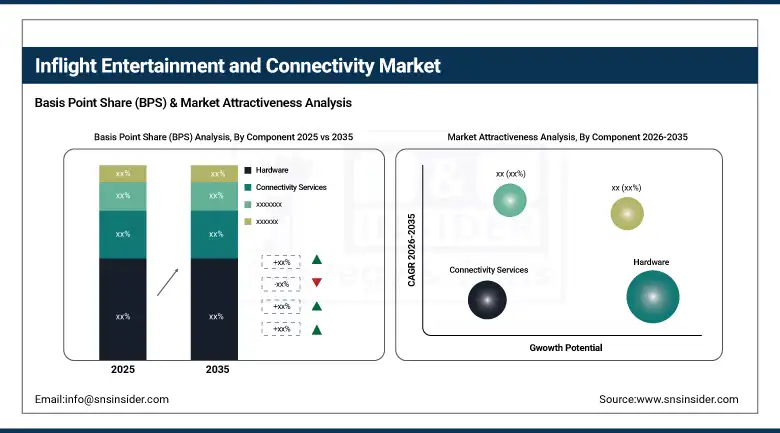

By Component, Hardware dominated with 34.36% share in 2025, while Connectivity Services are expected to grow at the fastest CAGR of 8.96% during 2026–2035.

-

By Connectivity Type, Satellite-Based Connectivity held the largest market share of 57.45% in 2025, while Hybrid Connectivity is projected to grow at the fastest CAGR of 10.91% during 2026–2035.

-

By Aircraft Type, Narrow-Body Aircraft accounted for the largest share of 40.85% in 2025, while Business Jets are expected to grow at the fastest CAGR of 9.14% during 2026–2035.

-

By Offering, Internet Connectivity dominated with a 36.24% market share in 2025, while E-commerce / Onboard Retailing is projected to grow at the fastest CAGR of 9.34% during 2026–2035.

-

By Fit Type, Retrofit segment held the largest share of 58.14% in 2025, while Line Fit installations are expected to grow at the fastest CAGR of 9.74% during 2026–2035.

-

By End User, Commercial Airlines dominated with 83.51% share in 2025, while Business Aviation is expected to grow at the fastest CAGR of 9.64% during 2026–2035.

By Component, Hardware Dominates while Connectivity Services Grow Rapidly:

Hardware segment dominated the market because of extensive usage of seat-back entertainment, in-flight onboard server and antenna installations, as well as networking within aircraft cabins, driven by ongoing cabin modernization activities in airplanes worldwide and growing importance of customer experience management. This segment’s strong presence both in new aircraft deliveries and retrofit projects made it the leading one in the IFEC segment.

The Connectivity Services Segment is the fastest-growing one as a result of growing need of airlines in broadband connectivity in-flight, as well as growing penetration of satellite-based connectivity services.

By Connectivity Type, Satellite-Based Connectivity Dominates while Hybrid Connectivity Grows Rapidly:

The Satellite-Based Connectivity segment was dominant in the market since it had the ability to cover a wide geographical area, hence providing a more reliable alternative for long-distance flights that could not be accessed by ground-based connectivity technologies. The significant presence of this technology in commercial aircrafts has been attributed to ongoing developments in high-throughput satellite technology alongside the push by airlines for seamless in-flight internet services.

Hybrid Connectivity is the fastest-growing segment as more airlines integrate their networks with GEO, LEO, and air-to-ground technologies. The development is being facilitated by the need for reliable and seamless connectivity in flights.

By Aircraft Type, Narrow-Body Aircraft Dominates while Business Jets Grow Rapidly:

Narrow-Body Aircraft segment dominated the market on account of extensive use in short- and medium-range commercial flights, especially as a result of low-cost airlines and expansion plans of narrow-body aircraft fleets in developing air travel destinations. The heavy manufacturing volumes associated with the production of narrow-body aircraft ensure that it remains the predominant choice for IFEC system integration worldwide.

Business Jets are the fastest-growing segment in the market on account of growing demand for luxurious in-flight communication and entertainment systems from corporate and private aviation sectors.

By Offering, Internet Connectivity Dominates while E-commerce / Onboard Retailing Grows Rapidly:

Internet Connectivity segment dominated the market because of the high emphasis that airlines have on ensuring uninterrupted internet access for their customers during flights. Integration of this segment in long and short haul aircrafts has enabled it to become a key component of IFEC systems.

E-commerce / Onboard Retailing is the fastest-growing segment. This can be attributed to growing trends of monetization of cabin using the connectivity platform provided by airlines.

By Fit Type, Retrofit Dominates while Line Fit Grows Rapidly:

Retrofit segment dominated the market because of the huge existing fleet of aging aircraft that would need to be updated with IFEC systems to fulfill today’s consumer demands. There has been increased emphasis on retrofitting aircraft to enhance their longevity and integrate sophisticated systems in a seamless manner without having to replace the entire fleet.

Line Fit is the fastest-growing segment because of the increasing penetration of IFEC systems at the time of production of aircraft, fueled by increasing airline demands for integrated digital aircraft cabins right out of the factory.

By End User, Commercial Airlines Dominate while Business Aviation Grows Rapidly:

Commercial Airlines segment dominated the market because of the large size of their global aircraft fleets and their constant investments in improving passengers' experiences using in-flight entertainment and connectivity services. Competition in airlines to enhance customer satisfaction and provide differentiated services has been a significant factor for the implementation of IFEC.

Business Aviation is the fastest-growing segment since there has been an increased need for sophisticated IFEC solutions among users of private jets and corporate business flights. Productivity and safety considerations have been motivating this trend.

Inflight Entertainment and Connectivity Market Regional Analysis:

North America Inflight Entertainment and Connectivity Market Insights:

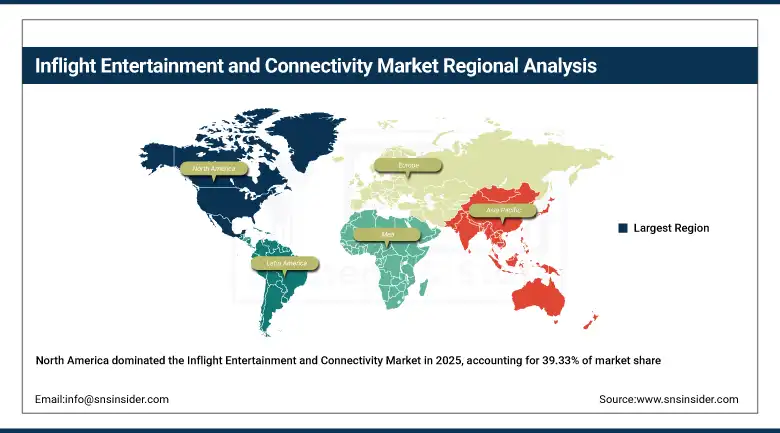

The North America Inflight Entertainment and Connectivity (IFEC) Market is dominant, holding a 39.33% share in 2025, underpinned by robust aviation infrastructure, a high uptake of digital cabin solutions, and the presence of dominant airline and connectivity service providers. The region has gained an edge due to the early adoption of cutting-edge satellite communications systems and high-throughput connectivity solutions, alongside the robust development of passenger experience enhancements within its commercial aircraft fleet. The extensive use of streaming media platforms, internet access, and personalized content delivery using AI-driven systems ensures robust market growth in both narrow-body and wide-body aircraft.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Inflight Entertainment and Connectivity Market Insights:

The U.S. Inflight Entertainment & Connectivity Market is driven by rapid airline digitization efforts, high consumer demand for seamless connectivity services, and continuous investments towards advanced in-flight digital infrastructure. Early adoption of cutting-edge connectivity systems, such as hybrid satellite networking and cloud-based entertainment platforms, backed by close collaboration between airlines and technology firms, has provided a robust boost to the country's inflight connectivity space.

Asia-Pacific Inflight Entertainment and Connectivity Market Insights:

The Asia-Pacific IFEC Market is the fastest-growing region, projected to expand at a CAGR of 9.12% during 2026–2035. This market is driven by the fast growth of commercial aviation aircraft, the growing number of air passengers, and considerable investments made into digitalization programs. There are several nations that include China, India, Japan, and South Korea that are making huge efforts towards improving their cabin experience systems and building connectivity infrastructure for domestic and international routes. The growing demand for cheap broadband connectivity systems and better passenger comfort are expected to drive the adoption of innovative IFEC solutions along with LCC market expansion, increased air travel needs of the middle-class population, and airport construction.

China Inflight Entertainment and Connectivity Market Insights:

The Chinese IFEC Market is driven by fast growth in commercial aviation fleet, active support of government towards development of aviation infrastructure, and growing focus towards enhancing passenger experience using digital cabin technologies. Domestic carriers are implementing advanced connectivity systems and satellite communication technology as well as content localization to enhance their services. Aviation digitalization and smart operation trends will further drive the adoption of intelligent solutions for entertainment and connectivity.

Europe Inflight Entertainment and Connectivity Market Insights:

Drivers of the Europe Inflight Entertainment and Connectivity (IFEC) Market include the presence of aggressive airline digital transformation programs, high-level importance of enhancing passenger experience, and growing adoption of next-gen IFEC technologies. The most prominent aviation destinations including UK, France, and Germany are increasingly focused on implementation of state-of-the-art connectivity systems, hybrid satellite networks, and cloud-based entertainment solutions in their fleets. Growing cooperation of airlines, aviation OEMs, and technology suppliers in developing IFEC products is promoting rapid introduction of such solutions within both short- and long-haul fleets. Upgrades in aircraft cabins and rising cross-border connectivity demands are also contributing to expansion of the regional market.

Germany Inflight Entertainment and Connectivity Market Insights:

Germany is one of the leading countries in Europe with regards to its robust aerospace manufacturing sector and highly developed aviation technology landscape. Increasing adoption of high-speed connectivity systems, AI-based passenger experiences solutions, and in-flight streaming services are being witnessed within the commercial and business aviation segments of the country. Growing investments in aviation research & development and strategic partnerships of airlines with technology vendors are driving the process of digitization of onboard IFEC products.

Latin America Inflight Entertainment and Connectivity Market Insights:

The Latin American IFEC market is expanding owing to an increase in air traffic passengers, growth in airliner fleet size, and improved focus towards enhancing passenger experience through airlines operating in the region. Countries including Brazil, Mexico, and Chile are making efforts towards improving cabin connectivity systems as well as installing in-flight entertainment solutions which are cost-effective. Satellites-based connectivity systems and retrofitted IFEC are slowly becoming trends in this region.

Middle East & Africa Inflight Entertainment and Connectivity Market Insights:

The Middle East and Africa IFEC Market is witnessing growth owing to rapid growth in international flights, airliner fleet expansions, and investments in improving passenger experiences through advanced IFEC solutions. Countries such as the UAE, Saudi Arabia, and South Africa are actively incorporating advanced cabin connectivity and satellite broadband solutions along with advanced entertainment systems for premium passengers. The presence of major international airline hubs in the region and investment in new aviation infrastructure solutions is helping drive the market.

Inflight Entertainment and Connectivity Market Competitive Landscape:

The Panasonic Avionics Corporation is one of the key global firms operating in the field of Inflight Entertainment and Connectivity (IFEC). The IFEC companies produce seat back entertainment consoles and connectivity systems to provide uninterrupted in-flight entertainment systems. They have a wide range of products that include passenger experience ecosystem products, which utilize high-speed connectivity and streaming technology by harnessing the power of the cloud system to provide their services and products to the customers during flights.

-

In February 2025, Panasonic Avionics advanced its next-generation connectivity platform by expanding high-speed broadband services and enhancing cloud-based content delivery systems across major airline fleets, improving global passenger connectivity experience.

Thales Group ranks among the top technology providers in the IFEC market based on their expertise in the design and development of satellite communication systems, avionics, and digital cabin management systems. Thales Group is a pioneer in providing comprehensive solutions for connectivity and entertainment systems through the use of secure satellite networks, data communication services, and passenger engagement tools. The firm’s unique concept of hybrid connectivity systems and cyber-secure aircraft systems makes it one of the pioneers of the connected aircraft business model.

-

In March 2025, Thales expanded its aviation connectivity portfolio by enhancing satellite-based IFEC solutions and integrating advanced secure communication technologies across commercial airline platforms, strengthening global in-flight connectivity capabilities.

Viasat, Inc. is one of the major providers of fast satellite connectivity solutions in the IFEC market. The company focuses on the provision of global broadband connectivity solutions to commercial airlines using advanced high bandwidth satellite communication systems. Such satellite communication systems guarantee access to internet connectivity to passengers during flights. It is evident from the company's significant investments in the development of satellite communication infrastructure.

-

In April 2025, Viasat expanded its in-flight connectivity capabilities through upgraded satellite bandwidth capacity and improved multi-orbit network integration, enhancing uninterrupted broadband access across international airline routes.

Inflight Entertainment and Connectivity Market Key Players:

Some of the Inflight Entertainment and Connectivity Market Companies are:

-

Panasonic Avionics Corporation

-

Thales Group

-

Viasat, Inc.

-

Gogo Inc.

-

Collins Aerospace

-

Safran S.A.

-

Intelsat S.A.

-

Honeywell International Inc.

-

Astronics Corporation

-

Anuvu Operations LLC

-

Lufthansa Systems GmbH

-

Global Eagle Entertainment Inc.

-

Iridium Communications Inc.

-

EchoStar Corporation

-

SITAONAIR

-

Burrana Pty Ltd.

-

Bluebox Aviation Systems Ltd.

-

Kontron AG

-

ThinKom Solutions, Inc.

-

ST Engineering iDirect

Inflight Entertainment and Connectivity Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.26 Billion |

| Market Size by 2035 | USD 17.88 Billion |

| CAGR | CAGR of 8.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Connectivity Services, Content Services, Software & Middleware, Others) • By Connectivity Type (Satellite-Based Connectivity, Air-to-Ground (ATG) Connectivity, Hybrid Connectivity, Others) • By Aircraft Type (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Jets, Business Jets, Others) • By Offering (IFE Hardware, Internet Connectivity, Streaming & Content Services, Live TV Services, E-commerce / Onboard Retailing, Others) • By Fit Type (Line Fit, Retrofit, Others) • By End User (Commercial Airlines, Business Aviation, Government / Defense Aircraft, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Panasonic Avionics Corporation, Thales Group, Viasat, Inc., Gogo Inc., Collins Aerospace, Safran S.A., Intelsat S.A., Honeywell International Inc., Astronics Corporation, Anuvu Operations LLC, Lufthansa Systems GmbH, Global Eagle Entertainment Inc., Iridium Communications Inc., EchoStar Corporation, SITAONAIR, Burrana Pty Ltd., Bluebox Aviation Systems Ltd., Kontron AG, ThinKom Solutions, Inc., ST Engineering iDirect |

Frequently Asked Questions

North America dominated with a 39.33% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 9.12% during 2026–2035.

Hardware dominated with a 34.36% share in 2025, while Connectivity Services are also projected to grow at the fastest CAGR of 8.96% during 2026–2035.

Growth is driven by increasing defense modernization programs, rising adoption of AI-enabled targeting systems, and growing geopolitical tensions.

The market is valued at USD 8.26 Billion in 2025 and is projected to reach USD 17.88 Billion by 2035.

The Inflight Entertainment and Connectivity Market is projected to grow at a CAGR of 8.07% during 2026–2035.

Get in Touch