Insulation Market Report Scope & Overview:

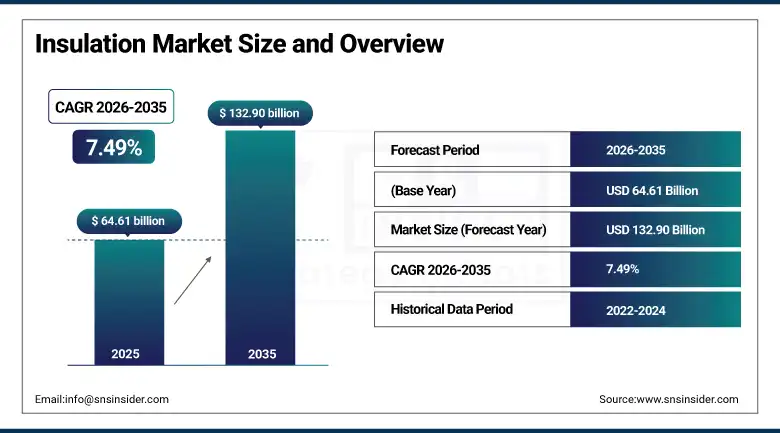

The Insulation Market was valued at USD 64.61 Billion in 2025 and is expected to reach USD 132.90 Billion by 2035, growing at a CAGR of 7.49% from 2026–2035.

The global insulation market is experiencing exceptional commercial growth driven by the convergence of stringent building energy efficiency regulations, the global construction sector’s accelerating adoption of green building standards, and the electrification of transportation creating new thermal management requirements in electric vehicles, aircraft, and rail systems. Insulation is the most cost-effective building decarbonisation measure available, delivering energy savings of 25 to 50% in residential and commercial buildings and creating a financial return on investment that building owners, government regulators, and institutional investors simultaneously prioritise.

Rockwool International launched a new range of high-performance mineral wool insulation boards for commercial building facade and roof applications in 2024, achieving enhanced fire resistance ratings and thermal performance coefficients that exceed standard product specifications. The launch targeted the growing European building renovation market’s demand for non-combustible, high-performance insulation solutions that simultaneously satisfy the EU Energy Performance of Buildings Directive’s tightening thermal performance requirements and the fire safety standards that post-Grenfell regulatory reform has elevated across European construction practice.

Size and Forecast

-

Market Size in 2026E: USD 69.45 Billion

-

Market Size by 2035: USD 132.90 Billion

-

CAGR: 7.49% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Insulation Market - Request Free Sample Report

Insulation Market Trends

-

Rising adoption of aerogel insulation for applications requiring ultra-thin, high-performance thermal barriers is creating premium market segments across industries.

-

Growing demand for bio-based and recycled content insulation materials including cellulose, hemp, sheep wool, and recycled glass fibre.

-

Increasing integration of insulation within prefabricated building panel systems and modular construction is creating industrial-scale procurement patterns creating new commercial relationships between insulation manufacturers and off-site construction platform developers.

-

Rising EV production is creating new thermal management insulation requirements in battery pack enclosures, motor housings, and power electronics cooling systems.

-

Expanding government building retrofit programmes funded by IRA, REPowerEU, and national energy efficiency investment are creating large-scale public procurement demand for insulation materials.

U.S. Insulation Market Outlook

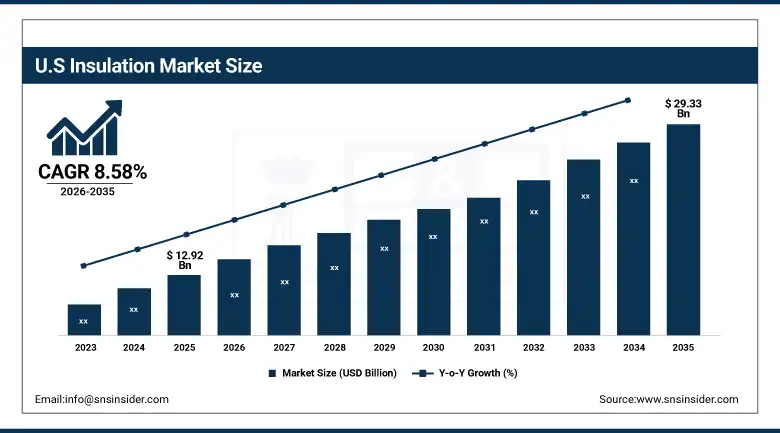

The U.S. Insulation Market was valued at approximately USD 12.92 Billion in 2025 and is expected to reach approximately USD 29.33 Billion by 2035, growing at a CAGR of approximately 8.58%.

The United States is the world’s most commercially significant insulation retrofit market, where the Inflation Reduction Act’s home energy efficiency tax credits and the Weatherization Assistance Programme’s federal funding create the most comprehensive government incentive infrastructure for residential insulation investment of any national market. Approximately 70% of U.S. homes were built before modern energy codes, creating an extraordinary retrofit opportunity whose aggregate commercial potential is progressively being converted into actual procurement by the IRA’s financial incentives.

Johns Manville expanded its spray foam insulation product range in 2025 with new closed-cell polyurethane formulations achieving R-6.5 per inch thermal resistance and Class II vapour retarder properties, targeting the commercial building envelope and residential attic insulation retrofit markets whose demand for high-R-value thin-profile insulation is growing with the IRA incentive programme’s acceleration of energy efficiency investment across the U.S. existing building stock.

Insulation Market Segment Analysis

-

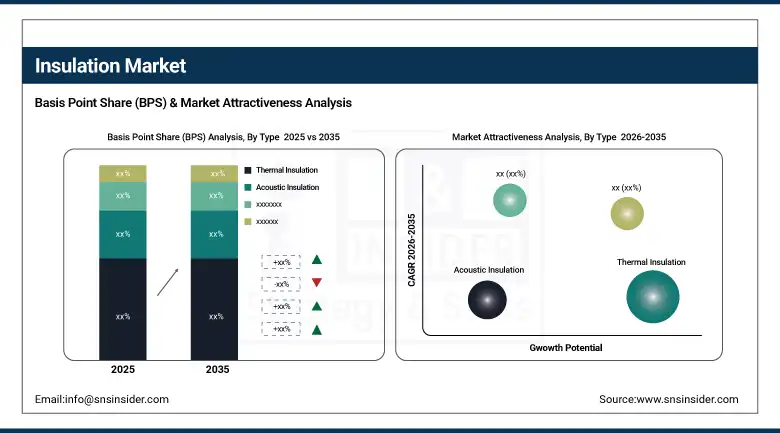

By Type, the Thermal Insulation segment dominated the Insulation Market with 47.80% share in 2025, while the Acoustic Insulation segment is the fastest growing with a CAGR of 9.20%.

-

By Material, the Fiberglass segment dominated the Insulation Market in 2025, while the Polyurethane Foam segment is the fastest growing.

-

By End User, the Building & Construction segment dominated the Insulation Market with 52.10% share in 2025, while the Transportation segment is the fastest growing with a CAGR of 8.80%.

By Type, thermal insulation dominates, acoustic grows fastest

Thermal insulation retained the dominant type position with 47.80% of the insulation market in 2025. Its commercial primacy reflects the foundational role of heat flow control in building energy performance, where the relationship between insulation R-value and heating and cooling energy consumption is direct, measurable, and precisely calculable in financial terms that building owners and their investors can evaluate against investment cost with confidence. The global building sector’s energy consumption, representing approximately 40% of total final energy use in most developed economies, creates an extraordinary commercial opportunity for thermal insulation investment whose building code mandate in new construction and financial incentive support in existing building retrofit collectively sustain the most structurally reliable demand pool of any insulation type.

Acoustic insulation is the fastest-growing type at a CAGR of 9.20% because the commercial and human health consequences of noise pollution exposure in urban environments are receiving growing regulatory and consumer attention that is progressively translating into building specification requirements and consumer purchase motivation. Office buildings whose open-plan workplace design creates acoustic privacy challenges are investing in ceiling, wall, and floor acoustic insulation solutions whose employee productivity and recruitment attraction benefits justify investment independent of regulatory mandate. The transportation sector’s acoustic insulation requirements in EV interiors, aircraft passenger cabins, and high-speed rail carriages are simultaneously creating industrial acoustic insulation demand that compounds with building application growth.

By End User, building & construction dominates, transportation grows fastest

Building and construction retained the dominant end user position with 52.10% of the insulation market in 2025. The sector’s commercial leadership reflects the dual demand streams of new construction and retrofits that collectively generate the highest-volume and most geographically distributed insulation procurement of any end use category. New construction’s building code-mandated insulation creates a baseline procurement requirement that grows proportionally with construction activity volume, while the retrofit market’s conversion of the existing building stock’s 1.7 billion under-insulated residential and commercial buildings into insulation-compliant properties creates a decades-long demand pipeline whose conversion rate accelerates with each successive tightening of government incentive programmes and energy efficiency regulatory requirements.

Transportation is the fastest-growing end use at a CAGR of 8.80% because the electrification of road, rail, and air transport is creating new insulation requirements that did not exist in conventional vehicle architectures. Battery electric vehicles require thermal management insulation in battery packs, motor housings, and power electronics assemblies whose temperature sensitivity and fire safety requirements demand insulation materials with performance specifications that differ fundamentally from conventional automotive insulation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Insulation Market Insights

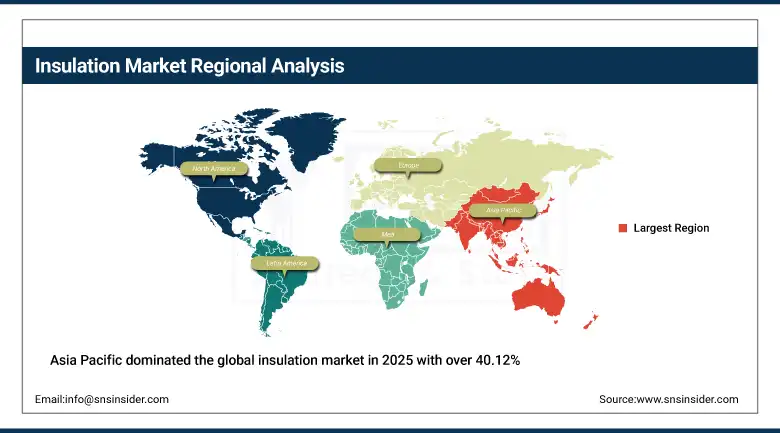

Asia Pacific dominated the global insulation market in 2025 with over 40.12% revenue share, driven by the region’s combination of the world’s largest construction activity volume, rapidly tightening building energy efficiency regulations across China, Japan, South Korea, and India, and the expanding industrial sector’s insulation requirements across manufacturing, petrochemical, and process industries.

China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary construction scale, progressive building energy standard tightening, and the government’s ambitious carbon neutrality commitment whose building energy efficiency improvement trajectory creates structural thermal insulation demand that grows with each successive building code revision.

India and Southeast Asia represent the most commercially significant emerging market growth opportunities within Asia Pacific, where rapid urbanisation, growing commercial construction investment, and progressive building energy code development are creating first-time systematic insulation specification requirements across markets where thermal insulation has historically been underspecified relative to the climate conditions that energy-efficient building design requires. India’s Bureau of Energy Efficiency’s progressive Energy Conservation Building Code tightening is creating increasing insulation specification requirements that domestic and international insulation manufacturers are positioning to serve.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Insulation Market Insights

North America is the fastest-growing regional insulation market at a CAGR of 8.63%, driven by the United States’ IRA energy efficiency incentive programme, Canada’s national building code energy performance tightening, and the commercial building sector’s LEED and ENERGY STAR certification investment.

Canada contributes approximately 17.5% of North American revenues through its national energy code tightening programme, the federal government’s Greener Homes Grant that provided CAD 5,000 for building envelope upgrades including insulation, and the commercial building sector’s progressive adoption of LEED and BOMA BEST certification standards that create structured insulation performance requirements across new and renovated commercial property.

Europe Insulation Market Insights

Europe is a technically sophisticated insulation market where the EU Energy Performance of Buildings Directive’s recast requirements, the REPowerEU energy security investment programme, and national renovation wave strategies across Germany, France, the Netherlands, and the Nordic countries collectively create the most comprehensive regulatory and financial support infrastructure for insulation market growth of any global region.

Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, driven by its large existing building stock whose KfW renovation funding programme has been one of Europe’s most commercially significant insulation retrofit demand creators, supporting billions of euros in annual energy efficiency renovation investment across residential and commercial properties.

MEA & Latin America Insulation Market Insights

The Middle East and Africa and Latin America are growing insulation markets where climate extremes, expanding construction activity, and progressive building energy code development are creating growing demand for thermal and acoustic insulation.

Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through Vision 2030’s construction investment, the extreme desert climate’s compelling case for thermal insulation in reducing cooling energy consumption, and the commercial building sector’s growing adoption of green building standards whose insulation performance criteria are progressively elevating specification quality above minimum code requirements.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its active construction market, growing commercial building sector’s sustainability investment, and the industrial sector’s insulation requirements across its significant petrochemical, mining, and food processing industries.

Market Dynamics

Growth Drivers: Building energy efficiency regulation creating mandatory insulation performance requirements and EV thermal management creating new industrial insulation demand

Tightening building energy efficiency regulation is the insulation market’s most commercially certain structural growth driver. Each successive revision of building energy codes across major construction markets creates a higher mandatory insulation performance threshold that new construction must achieve, creating specification uplift that increases per-building insulation procurement value while sustaining the compliance-driven demand that distinguishes insulation from discretionary building material categories. The trajectory of building code tightening across all major construction markets globally is consistently toward higher performance requirements that reflect the policy priority of building sector decarbonisation, creating a regulatory tailwind that sustains insulation demand growth through economic cycle variation.

Government retrofit incentive programmes are simultaneously accelerating the conversion of the existing building stock’s latent insulation demand into actual procurement by reducing the financial barrier that upgrade cost creates for building owners whose energy savings payback period without incentive support extends beyond their typical investment horizon. The IRA in the U.S., the REPowerEU investment programme, and national renovation wave strategies across EU member states collectively represent the most commercially significant government support infrastructure for insulation market demand acceleration in history, creating a multi-year demand expansion whose commercial impact is progressively visible in insulation sales volume growth across both residential and commercial channels.

Restraints: Raw material cost volatility affecting manufacturing economics and greenwashing concerns about sustainability performance claims

Raw material cost volatility for fiberglass, mineral wool, polyurethane precursors, and polystyrene creates manufacturing margin uncertainty that challenges insulation producers whose customer pricing commitments extend across project delivery timelines during which input costs may change substantially. The petrochemical derivatives market’s sensitivity to crude oil price cycles, natural gas costs’ impact on energy-intensive mineral wool production economics, and the glass market’s demand competition with construction and automotive sectors collectively create a cost environment that requires insulation manufacturers to maintain sophisticated raw material procurement strategies and product pricing disciplines.

The skilled insulation installer workforce shortage is the most operationally significant constraint on retrofit programme execution velocity in North America and Europe, where the pace of government-incentivised retrofit activity is creating installer demand that exceeds current training infrastructure capacity. Each month of delayed installation reduces the financial return capture from government incentives whose programme timelines create urgency that inadequate installer workforce availability cannot satisfy, motivating investment in training programme expansion that progressively improves programme execution capacity.

Opportunities: Bio-based and sustainable insulation material market development and EV battery thermal management insulation creating new industrial application market

Bio-based and recycled content insulation materials represent a growing premium market segment whose commercial development is driven by construction sector sustainability commitments, consumer environmental preference, and the low-embodied-carbon credentials that natural materials deliver relative to petrochemical-derived alternatives. Hemp fibre insulation, sheep wool boards, recycled denim batt, and high-recycled-content cellulose products are each developing commercially viable market positions in premium green building segments whose specifiers prioritise embodied carbon alongside operational energy performance in their material selection criteria.

EV battery thermal management insulation represents one of the most commercially attractive new industrial application markets for insulation manufacturers whose performance-differentiated products create premium pricing opportunities that commodity building insulation markets cannot generate. Aerogel insulation blankets, ceramic fibre thermal barriers, and intumescent fire protection materials for battery pack integration each represent EV-specific insulation requirements whose technical specification creates high commercial value per kilogram of material sold that motivates investment in EV-application product development from building insulation manufacturers seeking industrial application diversification.

Recent Developments:

-

2024: Rockwool International launched a new range of high-performance mineral wool insulation boards for commercial building facade and roof applications in 2024, achieving enhanced fire resistance ratings and improved thermal performance that satisfy EU Energy Performance of Buildings Directive requirements and post-Grenfell fire safety standards across European external wall insulation markets.

-

2025: Johns Manville expanded its spray foam insulation product range in 2025 with new closed-cell polyurethane formulations achieving R-6.5 per inch thermal resistance and Class II vapour retarder properties, targeting the growing U.S. residential retrofit market whose IRA incentive programme is accelerating energy efficiency upgrade investment across the country’s large existing housing stock.

-

2024: Kingspan Group expanded its insulated panel production capacity in North America in 2024 to serve growing demand from commercial and industrial building construction programmes seeking high-performance integrated insulated facade systems that combine thermal performance, fire safety, and architectural aesthetic in a single prefabricated product solution.

Insulation Market Key Players

-

Rockwool International

-

Saint-Gobain

-

Kingspan Group

-

Johns Manville

-

BASF

-

DuPont

-

Knauf Insulation

-

GAF Materials Corporation

-

Huntsman International

-

Armacell International

-

Covestro

-

URSA

-

Recticel

-

Atlas Roofing Corporation

-

Carlisle Companies

-

Cellofoam North America

-

OC Fiberglas

-

Paroc Group

-

Isover

-

Owens Corning

Insulation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 64.61 Billion |

| Market Size by 2035 | USD 132.90 Billion |

| CAGR | CAGR of 7.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Thermal Insulation, Acoustic Insulation, Electrical Insulation, Fire-Resistant Insulation) • by Material (Fiberglass, Mineral Wool, Polyurethane Foam, Polystyrene, Cellulose, Others) • by End User (Building & Construction, Transportation, Industrial, Oil & Gas, HVAC, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Rockwool International, Saint-Gobain, Kingspan Group, Johns Manville, BASF, DuPont, Knauf Insulation, GAF Materials Corporation, Huntsman International, Armacell International, Covestro, URSA, Recticel, Atlas Roofing Corporation, Carlisle Companies, Cellofoam North America, OC Fiberglas, Paroc Group, Isover, Owens Corning |

Frequently Asked Questions

Get in Touch