Liquid Fertilizer Market Report Scope & Overview:

The Liquid Fertilizer Market size was valued at USD 2.95 Billion in 2025 and is projected to reach USD 4.47 Billion by 2035, growing at a CAGR of 4.25% during 2026-2035.

The Liquid Fertilizer Market analysis highlights the increasing demand for efficient and environmentally friendly crop nutrition solutions. Rising adoption of precision agriculture and fertigation techniques is boosting liquid fertilizer usage across cereals, fruits, vegetables, and oilseeds.

In 2025, over 60% of large-scale farms in North America and Europe used precision agriculture, with liquid fertilizers favored for variable-rate application and real-time nutrient delivery

Liquid Fertilizer Market Size and Forecast:

-

Market Size in 2025: USD 2.95 Billion

-

Market Size by 2035: USD 4.47 Billion

-

CAGR: 4.25% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Liquid Fertilizer Market - Request Free Sample Report

Liquid Fertilizer Market Trends

-

Increasing use of precision farming techniques drives demand for targeted liquid fertilizer application, improving crop yields and reducing nutrient wastage.

-

Growing adoption of eco-friendly biofertilizers supports sustainable agriculture, reducing chemical dependency and enhancing soil fertility across various crop types.

-

Development of advanced liquid fertilizer formulations, including micronutrient blends and controlled-release solutions, enhances efficiency and crop nutrient uptake.

-

Emerging economies in Asia-Pacific and Latin America are witnessing higher consumption, driven by increasing farm mechanization and agricultural modernization.

-

Fertigation and drip irrigation integration with liquid fertilizers improves nutrient absorption, reduces labor, and promotes precise, timely application in farming.

The U.S. Liquid Fertilizer Market size was valued at USD 0.50 Billion in 2025 and is projected to reach USD 0.79 Billion by 2035, growing at a CAGR of 4.69% during 2026-2035. Liquid Fertilizer Market growth is driven by increasing adoption of precision agriculture and efficient nutrient management practices. Corn, soybean, and wheat cultivation drive significant demand for liquid fertilizers across the country.

Liquid Fertilizer Market Growth Drivers:

-

Enables next-generation electronics production, reinforcing investments and fueling Liquid Fertilizer Market growth.

Farmers globally are shifting toward liquid fertilizers because they offer faster uptake, easier fertigation integration, and more precise nutrient management than traditional solids. As arable land becomes scarcer and yield pressures grow, the application of liquid nutrient solutions on high‑value crops is accelerating to meet food security demands. This trend is especially pronounced in regions adopting drip irrigation and precision farming technologies, where liquid forms allow better timing and dosing. In 2025, global fertilizer consumption is forecast at about 205 million tonnes of nutrients.

Global fertilizer consumption is forecast at 205 million tonnes of nutrients in 2025, driven by liquid fertilizers' precision and compatibility with modern irrigation systems

Liquid Fertilizer Market Restraints:

-

High Costs and Technical Complexities Restrict the Growth of the Liquid Fertilizer Market

While liquid fertilizers provide agronomic benefits, their adoption is challenged by higher upfront costs for specialized equipment, storage, and distribution systems compared to granular fertilizers. In many developing regions, the lack of infrastructure for fertigation and insufficient cold‑chain or mixing facilities inhibits uptake. Farmers with smaller landholdings often hesitate to invest in the required equipment, and transportation of liquid products adds complexity and cost. Combined with volatile input prices, these factors slow penetration of liquid formulations. In 2025, production of nitrogen nutrients is expected at approximately 116 million tonnes.

Liquid Fertilizer Market Opportunities:

-

Rising Demand for Hybrid Imaging Devices Creates Growth Opportunities in the Liquid Fertilizer Market

With increasing emphasis on sustainable farming, environmentally friendly liquid fertilizers enriched with micronutrients and bio‑based compounds offer strong growth potential. This opens doors for manufacturers to diversify products and enter underserved markets such as horticulture and precision applications. Government subsidies and soil health initiatives further support adoption of innovative liquid formulations. As emerging markets modernize irrigation systems and prioritize nutrient‑use efficiency, this segment is poised to expand. In 2025, specialty fertilizer imports to India alone are projected at about 140,000 tonnes.

In 2025, India’s specialty fertilizer imports are projected at 140,000 tonnes, driven by sustainable farming and government soil health initiatives

Liquid Fertilizer Market Segment Analysis

-

By type, nitrogen led the market with a 42.30% share in 2025, while micronutrients registered the fastest growth with a CAGR of 7.60%.

-

By crop type, cereals and grains dominated the market with 38.90% in 2025, while fruits and vegetables showed the fastest growth with a CAGR of 8.40%.

-

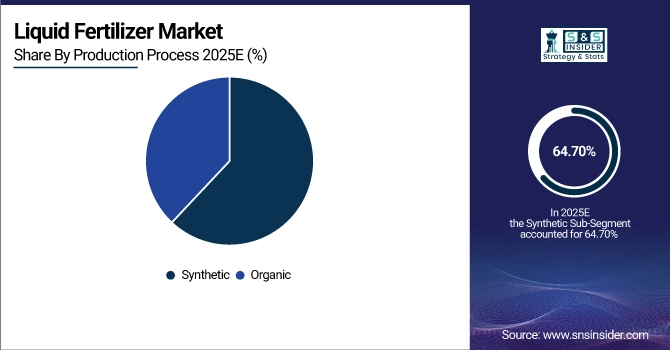

By production process, synthetic fertilizers led with 64.70% in 2025, while organic fertilizers registered the fastest growth with a CAGR of 9.20%.

-

By mode of application, fertigation led the market with 40.80% in 2025, while foliar application showed the fastest growth with a CAGR of 8.90%.

-

By compound, non-complex fertilizers held 58.10% in 2025, while complex fertilizers were the fastest-growing segment with a CAGR of 7.10%.

By Production Process, Synthetic Lead While Organic Registers Fastest Growth

Synthetic liquid fertilizers dominate the market because they are cost-effective, widely available, and deliver consistent nutrient levels for large-scale farming. Advanced formulations of NPK blends and urea solutions are widely used in cereals, grains, and commercial vegetable cultivation. However, organic liquid fertilizers are registering the fastest growth as farmers increasingly adopt sustainable agricultural practices, focusing on soil health, environmental safety, and organic certification. This trend is particularly strong in Europe and Asia-Pacific. In 2025, global production of organic liquid fertilizers is projected at 6.8 million tonnes.

By Type, Nitrogen Leads Market While Micronutrients Registers Fastest Growth

Nitrogen-based liquid fertilizers continue to dominate the global market due to their essential role in boosting crop yields, especially for cereals, grains, and oilseeds. Farmers prefer nitrogen solutions because they provide rapid nutrient uptake, higher efficiency, and compatibility with fertigation systems. Meanwhile, micronutrient-enriched liquid fertilizers are witnessing the fastest growth as awareness of soil health and nutrient balance rises. These products address deficiencies in zinc, boron, and iron, enhancing crop quality. In 2025, global nitrogen fertilizer production is projected at approximately 116 million tonnes.

By Crop Type, Cereals & Grains Dominate While Fruits & Vegetables Shows Rapid Growth

Cereals and grains account for the largest share of liquid fertilizer consumption due to their extensive cultivation and high nutrient requirements. Major crops like wheat, corn, and rice benefit from liquid nitrogen and multi-nutrient solutions applied via irrigation systems. Fruits and vegetables are the fastest-growing segment, driven by the need for improved yield, fruit quality, and precision nutrient management. High-value horticultural crops increasingly rely on foliar sprays and fertigation for optimal results. In 2025, U.S. liquid fertilizer consumption for cereals is estimated at 45 million tonnes.

By Production Process, Synthetic Lead While Organic Registers Fastest Growth

Synthetic liquid fertilizers dominate the market because they are cost-effective, widely available, and deliver consistent nutrient levels for large-scale farming. Advanced formulations of NPK blends and urea solutions are widely used in cereals, grains, and commercial vegetable cultivation. However, organic liquid fertilizers are registering the fastest growth as farmers increasingly adopt sustainable agricultural practices, focusing on soil health, environmental safety, and organic certification. This trend is particularly strong in Europe and Asia-Pacific. In 2025, global production of organic liquid fertilizers is projected at 6.8 million tonnes.

By Mode of Application, Fertigation Lead While Foliar Registers Fastest Growth

Fertigation remains the leading application method for liquid fertilizers due to its efficiency, ability to deliver nutrients directly through irrigation systems, and ease of integration in precision agriculture. It is widely applied in cereals, grains, and high-value crops. While, Foliar application is growing fastest because it allows rapid correction of nutrient deficiencies, enhances crop quality, and minimizes wastage. Farmers increasingly combine foliar sprays with fertigation to maximize efficiency. In 2025, global fertigation-applied liquid fertilizer consumption is projected at 72 million tonnes.

By Compound, Non-complex Lead While Complex Grow Fastest

Non-complex liquid fertilizers, such as single-nutrient urea or potassium nitrate solutions, dominate the market due to their cost-effectiveness, ease of application, and high availability. They are widely used for staple crops and large-scale agriculture. Complex or multi-nutrient liquid fertilizers, which combine multiple macro- and micronutrients in one formulation, are experiencing the fastest growth as farmers seek efficient solutions to improve soil fertility, crop health, and yield quality. In 2025, global production of complex liquid fertilizers is estimated at 14 million tonnes.

Liquid Fertilizer Market Regional Analysis:

Asia-pacific Liquid Fertilizer Market Insights

In 2025 Asia-Pacific dominated the Liquid Fertilizer Market and accounted for 45.36% of revenue share, this leadership is due to the extensive cereal cultivation, rising irrigation adoption, and government support boost demand. Farmers in countries like India and China are increasingly shifting to liquid formulations for higher nutrient efficiency and faster uptake. With improved infrastructure and growing penetration of fertigation systems, adoption rates continue to climb across both large commercial farms and smallholders. In 2025, the Asia‑Pacific liquid fertilizer volume consumption is around 20.6 million metric tons.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Liquid Fertilizer Market Insights

China, as part of the Asia‑Pacific, stands out with large‑scale cereal and rice production and rapid modernization of fertilizer practices. Liquid fertilizer adoption is driven by policy emphasis on yield improvement and nutrient‑use efficiency. The country is also increasing its use of advanced farming technologies like fertigation and precision irrigation to support high‑intensity cropping systems. In 2025, China’s nitrogen fertilizer consumption is estimated at 24.8 million metric tons of nutrient equivalent.

North America Liquid Fertilizer Market Insights

North America is expected to witness the fastest growth in the Liquid Fertilizer Market over 2026-2035, with a projected CAGR of 4.85% due to advanced farming systems, precision irrigation, and large‑scale commercial operations foster strong liquid fertilizer use for major crops like corn and soybeans. Farmers leverage liquid formulations to enhance nutrient uptake and align with sustainable input‑use strategies. At the same time, import and trade dynamics influence availability and pricing, affecting adoption in some areas. In 2025, the U.S. imported about 5.8 million tons of nitrogen nutrients.

U.S. Liquid Fertilizer Market Insights

The U.S. market is characterized by high commercialization, heavy use of irrigation, and growing interest in sustainable nutrient systems. Large cereal acreage and export‑oriented crops drive demand for liquid fertilizers. Innovation in fertigation-compatible products and logistics enhancements are further supporting uptake. In 2025, U.S. fertilizer production (nitrogen nutrient) was 15.1 million short tons.

Europe Liquid Fertilizer Market Insights

In 2025, Europe emerged as a promising region in the Liquid Fertilizer Market, due to strong regulation on nutrient use, high irrigation infrastructure, and a push for eco‑friendly formulations. Countries such as Germany, France and Italy are investing in precision agriculture, boosting adoption of liquid nutrient solutions. Meanwhile, smaller farms are gradually shifting away from granular fertilizers towards liquid forms thanks to efficiency benefits. In 2025, Germany’s liquid fertilizer market consumption per hectare improved by 70 % over the last 55 years.

Germany Liquid Fertilizer Market Insights

Germany, as a core European agricultural nation, exhibits advanced fertigation systems, precision farming, and sustainable nutrient management. This makes it a key country for liquid fertilizer adoption in Europe. Farm cooperatives and public‑private partnerships support transitions to liquid technologies in key crop zones.

Latin America (LATAM) and Middle East & Africa (MEA) Liquid Fertilizer Market Insights

The Liquid Fertilizer Market is experiencing moderate growth in the Latin America (LATAM) and Middle East & Africa (MEA) regions, due to the expanding high‑value crop sectors (fruits & vegetables), increasing irrigation adoption, and government initiatives in emerging markets. However, infrastructure and logistics challenges, such as limited fertigation systems and distribution networks, moderate faster uptake. Additionally, many smaller farms remain hesitant due to high upfront costs for liquid systems. In 2025, MEA production/trade volume of fertilizer (not specific to liquid only) accounts for about 5 % of global nitrogen consumption.

Liquid Fertilizer Market Competitive Landscape:

Yara is a leading crop‑nutrition and fertilizer company with strong global production and supply of nitrogen-based and micronutrient solutions. Nitrogen remains its most important nutrient, accounting for about 58 % of total consumption in its crop‑nutrition business. Yara’s 2025 industry handbook shows steady global nitrogen consumption outside China. While specific liquid fertilizer volumes are not broken out, Yara’s global scale supports substantial liquid fertilizer production. In recent years, global nitrogen (outside China) remains around 100 million tonnes annually.

-

In July 2024, Yara International ASA partnered with PepsiCo Europe to supply low‑carbon fertilizers and advanced precision farming tools across more than 1,000 farms in multiple European countries, supporting sustainable crop production, reduced emissions, and optimized nutrient efficiency.

ICL Group specializes in specialty fertilizers, multis, and niche nutrient solutions, including liquid formats and controlled‑release products. While specific 2025 liquid fertilizer production data isn’t published, ICL emphasizes innovation in next-generation liquid and bio-based systems. The company’s focus on plant biostimulants and efficient delivery systems positions it for growth in the liquid fertilizer space. ICL continues to expand its product portfolio to meet precision agriculture demands. In 2025, ICL ranks among the top firms in the nitrogenous fertilizer market globally.

-

In August 2024, ICL Group Ltd. signed a five‑year distribution agreement worth approximately $170 million with AMP Holdings in China, enabling supply of specialty water‑soluble fertilizers for high-value crops, enhancing market reach, supporting precision agriculture, and promoting efficient nutrient management across major horticultural regions.

EuroChem Group is a major global fertilizer producer with broad nitrogen, phosphate, and specialty nutrient systems, including liquid formulations aimed at precision agriculture. While 2025 liquid fertilizer volume data specific to EuroChem aren’t disclosed, its inclusion in nitrogenous fertilizer market analyses demonstrates its scale. The company’s integrated production network enables supply of high‑efficiency liquid nutrients across multiple geographies. EuroChem continues to invest in technology-driven production and sustainability initiatives. Its global presence strengthens liquid fertilizer availability for various crops and regions.

-

In March 2024, EuroChem Group AG inaugurated a US $1 billion phosphate fertilizer complex in Brazil with 1 million tons annual capacity, and in 2025 implemented AI-driven production systems across operations, improving efficiency, sustainability, and precision nutrient delivery for agricultural markets.

Liquid Fertilizer Market Key Players:

-

Nutrien Ltd.

-

Yara International ASA

-

The Mosaic Company

-

K+S Aktiengesellschaft

-

ICL Group Ltd.

-

CF Industries Holdings, Inc.

-

EuroChem Group AG

-

OCP Group

-

SQM S.A.

-

Coromandel International Limited

-

AgroLiquid

-

Plant Food Company, Inc.

-

FoxFarm Soil & Fertilizer Company

-

Wilbur-Ellis Company LLC

-

Helena Agri-Enterprises, LLC

-

Compo Expert GmbH

-

Nufarm Limited

-

Grupa Azoty S.A.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.95 Billion |

| Market Size by 2035 | USD 4.47 Billion |

| CAGR | CAGR of 4.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Nitrogen, Phosphorus, Potassium, and Micronutrients) • By Crop Type (Cereals & Grains, Fruits & Vegetables, and Oilseeds & Pulses) • By Production Process (Organic and Synthetic) • By Mode of Application (Fertigation, Foliar, Soil, and Others) • By Compound (Complex and Non-complex) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nutrien Ltd., Yara International ASA, The Mosaic Company, K+S Aktiengesellschaft, ICL Group Ltd., CF Industries Holdings, Inc., EuroChem Group AG, Haifa Chemicals Ltd., OCP Group, SQM S.A., Coromandel International Limited, AgroLiquid, Kugler Company, Plant Food Company, Inc., FoxFarm Soil & Fertilizer Company, Wilbur-Ellis Company LLC, Helena Agri-Enterprises, LLC, Compo Expert GmbH, Nufarm Limited, Grupa Azoty S.A. |

Frequently Asked Questions

Asia-Pacific dominated the Liquid Fertilizer Market in 2025.

The Nitrogen segment dominated during the projected period.

Growth is driven by increasing adoption of precision agriculture and efficient nutrient management practices.

The market is valued at USD 2.95 Billion in 2025 and is projected to reach USD 4.47 Billion by 2035.

The Liquid Fertilizer Market is expected to grow at a CAGR of 4.25% during 2026–2035.

Get in Touch