Maritime Security Market Report Scope & Overview:

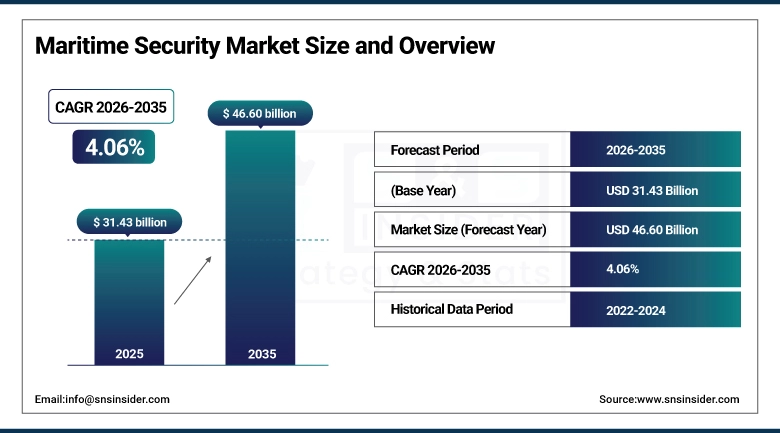

The Maritime Security Market size was valued at USD 31.43 Billion in 2025 and is projected to reach USD 46.60 Billion by 2035, growing at a CAGR of 4.06% during 2026–2035.

The sea carries roughly 90% of world trade by volume that single fact makes maritime security investment non-discretionary for the governments and industries that depend on global commerce. A disrupted shipping lane, a compromised port terminal, or an attacked offshore platform does not create a local problem it creates a supply chain problem felt across continents.

Market Size and Forecast:

-

Market Size in 2025: USD 31.43 Billion

-

Market Size by 2035: USD 46.60 Billion

-

CAGR: 4.06% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Maritime Security Market - Request Free Sample Report

Key Maritime Security Market Trends:

-

Unmanned systems surface vessels, underwater vehicles, and drones are increasingly being integrated into maritime surveillance and patrol operations, reducing the personnel cost and risk profile of monitoring large maritime zones while extending the detection coverage that manned patrols cannot sustain continuously.

-

Maritime cybersecurity has moved from a peripheral concern to a primary budget line as port management systems, vessel navigation networks, and cargo tracking platforms have all demonstrated vulnerability to intrusions that can disrupt operations without any physical attack on infrastructure.

-

The Red Sea shipping disruption that began in late 2023 has accelerated commercial shipping company investment in vessel hardening, communications security, and real-time threat intelligence services that were previously considered discretionary by operators not transiting high-risk zones.

-

Automatic Identification System data fusion with radar, satellite imagery, and Vessel Monitoring System feeds is creating a maritime domain awareness capability that allows operators to detect anomalous vessel behavior patterns dark ship transits, spoofed identities, unusual routing at a scale that manual monitoring cannot match.

-

Port and terminal operators are accelerating investment in integrated security platforms that connect physical access control, cargo scanning, perimeter surveillance, and cybersecurity monitoring through a single operational interface, driven by regulatory pressure from the ISPS Code compliance requirements and insurance premium incentives.

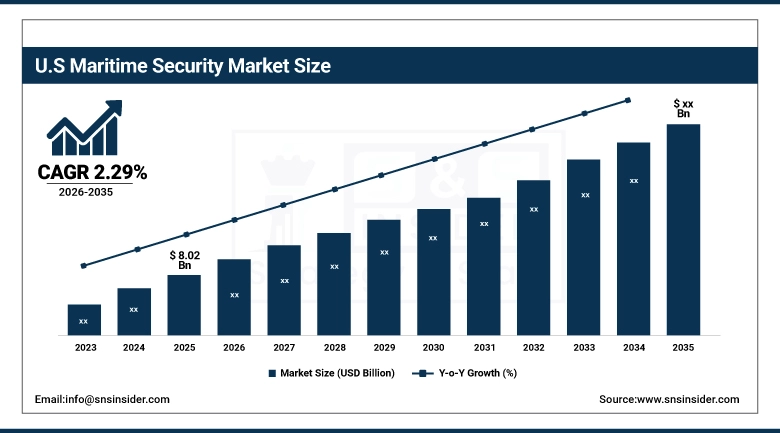

The U.S. Maritime Security Market was valued at USD 8.02 Billion in 2025, growing at a CAGR of 2.29% through 2035. The United States operates the world’s largest naval force and one of its most extensive port security infrastructures, with Department of Homeland Security, U.S. Coast Guard, and U.S. Navy investment driving baseline procurement across surveillance, access control, and port screening technologies.

Maritime Security Market Growth Drivers:

-

Escalating Geopolitical Tensions on Key Shipping Routes, Growing Cargo Theft Sophistication, and Mandatory Compliance Frameworks Are Sustaining Maritime Security Investment Across Government and Commercial End-Markets

The maritime security market runs through two demand structures simultaneously. Government-funded procurement naval capability, coast guard technology, national port security programs is driven by strategic threat assessment and defense budget cycles that move slowly but generate large, long-duration contracts. Commercial investment is driven by a combination of regulatory compliance, insurance requirements, and direct threat exposure. The ISPS Code requires ships and port facilities trading internationally to implement certified security plans, creating a mandatory procurement floor beneath which operators cannot fall without losing access to international ports. Insurance underwriters add pressure through hull war risk premium structures that reward documented security investment, creating a financial incentive that operates independently of regulation. The Red Sea threat environment from late 2023 has been the most acute recent driver missile and drone attacks against commercial shipping compressed the decision timeline for vessel security investment in ways that compliance programs alone never do. Each incident connecting a geopolitical conflict to a critical choke point converts discretionary security investment into urgent operational procurement.

Maritime Security Market Restraints:

-

Budget Constraints in Developing Economies, System Integration Complexity, and the Fragmented Regulatory Landscape Across Flag States Are Limiting Market Expansion Pace

A full installation perimeter surveillance, cargo scanning, access control biometrics, communications encryption, and the software tying them into a common operational picture requires capital that smaller port operators in developing economies frequently cannot access without external funding. Aid programs and multilateral bank financing address some of this gap, but implementation timelines mean that vulnerable ports in West Africa, Southeast Asia, and parts of Latin America remain under-secured relative to their threat environment. The integration challenge compounds the cost: systems purchased over multiple procurement cycles from different vendors running incompatible protocols require expensive middleware to produce a common operational picture. Regulatory fragmentation adds further complexity a vessel calling at twenty countries may encounter twenty different security inspection regimes, creating compliance documentation burdens that absorb resources from operational security capability.

Maritime Security Market Opportunities:

-

AI-Integrated Domain Awareness, Cyber-Physical Security Convergence, and Offshore Energy Infrastructure Protection Are Creating Growth Pathways That Conventional Physical Security Solutions Cannot Address

AI applied to maritime domain awareness data produces detection capability qualitatively different from rule-based anomaly detection. Machine learning models trained on AIS behavioral data identify vessels operating in patterns consistent with smuggling, sanctions evasion, or pre-attack positioning at a sensitivity human analysts cannot match at scale. Satellite-based AIS reception has eliminated the open-ocean coverage gaps that previously limited anomaly detection to coastal zones, making global behavioral surveillance commercially viable. Cyber-physical security convergence creates opportunity for integrated platforms that monitor network intrusions on port operating systems alongside physical perimeter alerts in a single operator interface a capability that neither specialist cyber firms nor conventional physical security integrators provide individually. Offshore energy infrastructure protection is an expanding market segment: the proliferation of floating production vessels, subsea pipeline networks, and offshore wind farm electrical infrastructure has created fixed sea-based assets requiring continuous security monitoring well outside traditional coastal zone boundaries.

Maritime Security Market Segment Analysis:

By Security Type: Port & Critical Infrastructure Security Leads While Cargo & Container Security Drives Fastest Growth Through 2035

Port & Critical Infrastructure Security dominated with a 34.52% share in 2025 at USD 10.85 Billion, while Cargo & Container Security is expected to grow at the fastest CAGR of approximately 6.05% through 2035. Port infrastructure leads because it encompasses the broadest security interventions perimeter control, access management, surveillance, vessel traffic management, and physical asset protection and is the point in the maritime supply chain most scrutinized by regulators. Cargo and container security is growing fastest because containerized trade volume keeps rising, cargo crime sophistication advances in parallel, and non-intrusive inspection technology is expanding from major gateway ports into secondary terminals that previously could not afford the infrastructure.

By System: Surveillance & Tracking Systems Lead While Access Control & Cybersecurity Solutions Drive Fastest Growth Through 2035

Surveillance & Tracking Systems (Radar, AIS, Sonar) dominated with a 31.48% share in 2025 at USD 9.89 Billion, while Access Control & Cybersecurity Solutions are expected to grow at the fastest CAGR of approximately 5.53% through 2035. Surveillance holds the leading share because it provides the foundational domain picture on which all other security decisions depend. Cybersecurity is growing fastest because the digitalization of port operations and vessel navigation has created attack surfaces that did not exist a decade ago, and incidents like the 2017 NotPetya attack on Maersk which disabled terminal operations globally — have made cyber investment a board-level priority for major operators.

By Application: Port & Harbor Security Leads While Commercial Shipping Security Drives Fastest Growth Through 2035

Port & Harbor Security dominated with a 33.27% share in 2025 at USD 10.46 Billion, while Commercial Shipping Security is expected to grow at the fastest CAGR of approximately 5.54% through 2035. The port application leads for the same structural reasons as the port infrastructure security type. Commercial shipping security is growing fastest because the elevated Red Sea threat environment since 2023 moved vessel security investment from compliance-driven to operationally urgent for liner operators, tanker owners, and bulk carriers transiting high-risk corridors.

By End-User: Government & Defense Authorities Lead While Oil & Gas Companies Drive Fastest Growth Through 2035

Government & Defense Authorities dominated with a 36.14% share in 2025 at USD 11.36 Billion, while Oil & Gas Companies are expected to grow at the fastest CAGR of approximately 6.09% through 2035. Government authorities hold the dominant share because national defense and coast guard programs generate the largest single procurement events — naval surveillance systems and national port security programs funded through defense appropriations carry per-contract values that commercial procurement cannot match. Oil and gas companies are growing fastest because offshore infrastructure in deepwater fields offshore West Africa, Brazil, and Southeast Asia are proliferating in maritime security environments where state protection is unreliable, creating a private sector investment mandate.

Maritime Security Market Regional Analysis:

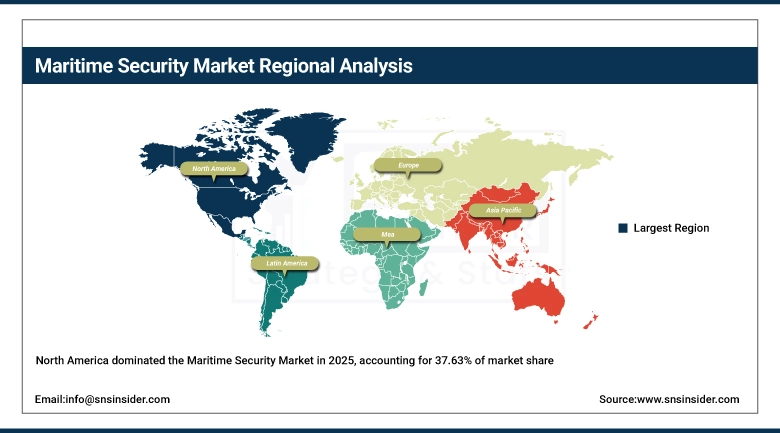

North America Maritime Security Market Insights

North America dominated in 2025 at USD 11.83 Billion (37.63%), projected to reach USD 15.32 Billion by 2035 at a CAGR of 2.65%. The region’s leadership rests on the scale of U.S. federal maritime security programs through DHS, the Coast Guard, and the Navy, alongside port security grant programs that fund terminal upgrades at the country’s busiest container and energy ports. The slower growth rate reflects the maturity of existing infrastructure rather than any reduction in investment commitment.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Maritime Security Market Insights

The United States dominates North American procurement through federal defense and homeland security programs, extensive port security investment at major gateway terminals, and a defense industrial base that both consumers and produces the world’s most sophisticated maritime security systems.

Europe Maritime Security Market Insights

Europe held USD 7.80 Billion (24.82%) in 2025, growing to USD 10.57 Billion by 2035 at a CAGR of 3.12%. The region’s investment reflects the density of its port infrastructure Rotterdam, Antwerp, and Hamburg among the world’s busiest container terminals combined with elevated defense spending following the 2022 Russia-Ukraine conflict, which increased NATO member maritime surveillance and mine countermeasure investment along Baltic and North Sea approaches.

United Kingdom Maritime Security Market Insights

The United Kingdom leads European procurement through its Royal Navy capability programs, intensive port security at Felixstowe, Southampton, and Dover, and its role as the global maritime insurance and threat intelligence hub that generates sustained demand for commercial maritime risk management services.

Asia Pacific Maritime Security Market Insights

Asia Pacific is the fastest-growing region at a CAGR of approximately 7.25%, rising from USD 6.83 Billion in 2025 to USD 13.77 Billion by 2035. Territorial disputes in the South China Sea, piracy pressure in the Strait of Malacca, and the scale of Asia’s container port infrastructure are driving government and commercial security investment simultaneously. Naval modernization in India, Japan, South Korea, and Australia generates sustained procurement demand across the world’s busiest shipping lanes.

China Maritime Security Market Insights

China leads Asia Pacific through the scale of its coast guard and naval modernization programs, the security requirements of its massive container port network at Shanghai and Ningbo, and its assertive maritime posture that drives reciprocal security investment from neighboring states and U.S. allies throughout the region.

Latin America and Middle East & Africa Maritime Security Market Insights

Latin America held USD 2.61 Billion (8.31%) in 2025, growing at a CAGR of 2.45% to USD 3.32 Billion by 2035. Brazil leads through the security requirements of its deepwater pre-salt oil and gas fields, its Santos container port, and a naval modernization program including submarine development and coastal surveillance. Middle East & Africa held USD 2.36 Billion (7.50%) in 2025, growing at a faster CAGR of 4.43% to USD 3.62 Billion by 2035, driven by Gulf state naval investment and port security at energy trade route choke points. The UAE dominates MEA maritime security through Jebel Ali port security operations, naval modernization programs, and the country’s strategic position at the Arabian Gulf–Indian Ocean junction, where energy cargo transit volumes justify substantial domain awareness and vessel protection investment.

Competitive Landscape for Maritime Security Market:

Lockheed Martin

Lockheed Martin participates in the maritime security market through naval systems, maritime surveillance programs, and undersea warfare technology spanning surface ship combat management, maritime patrol aircraft sensor systems, and littoral zone defense. The company’s maritime security business is embedded within long-term U.S. Navy and allied nation defense procurement relationships that provide both development funding and production contracts for maritime security-relevant platforms.

In February 2025, Lockheed Martin received a contract for additional AN/AQS-22 Airborne Low Frequency Sonar systems for the U.S. Navy’s MH-60S helicopter fleet, extending maritime surveillance and submarine detection capability in the Indo-Pacific theater, with provisions for deliveries to allied Pacific partner nations under U.S. maritime security cooperation programs.

Thales Group

Thales operates across maritime security through naval radar and sonar systems, port security surveillance platforms, vessel tracking software, and cybersecurity solutions for maritime operational technology environments. The company holds a strong position in European naval markets through established relationships with national navies in France, the Netherlands, Australia, and multiple NATO states built on decades of frigate and submarine sensor integration programs.

In April 2025, Thales deployed its SkyView Maritime surveillance system at three major Mediterranean port facilities, providing integrated radar, electro-optical, and AIS fusion across harbor approaches and terminal perimeters to close coverage gaps that legacy single-sensor systems had left exploitable by small vessel intrusion.

Maritime Security Market Key Players:

-

Lockheed Martin

-

Raytheon Technologies

-

Northrop Grumman

-

Thales Group

-

BAE Systems

-

Maritime Security Solutions

-

Harris Corporation

-

Elbit Systems

-

Leonardo S.p.A.

-

General Dynamics

-

Safran Electronics & Defense

-

L3Harris Technologies

-

SAIC

-

Boeing

-

DroneShield

-

Textron Systems

-

Kongsberg Gruppen

-

OSI Maritime Systems

-

Honeywell International

-

Smiths Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 31.43 Billion |

| Market Size by 2035 | USD 46.60 Million |

| CAGR | CAGR of 4.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Security Type (Port & Critical Infrastructure Security, Vessel Security, Coastal Surveillance & Border Security, and Cargo & Container Security) • By System (Surveillance & Tracking Systems (Radar, AIS, Sonar), Screening & Scanning Systems (X-ray, Cargo Inspection), Communication Systems, and Access Control & Cybersecurity Solutions) • By Application (Port & Harbor Security, Offshore Platform Security (Oil & Gas Rigs), Naval & Defense Operations, and Commercial Shipping Security) • By End-User (Government & Defense Authorities, Port Authorities, Shipping & Logistics Companies, and Oil & Gas Companies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin, Raytheon Technologies, Northrop Grumman, Thales Group, BAE Systems, Maritime Security Solutions, Harris Corporation, Elbit Systems, Leonardo S.p.A., General Dynamics, Safran Electronics & Defense, L3Harris Technologies, SAIC, Boeing, DroneShield, Textron Systems, Kongsberg Gruppen, OSI Maritime Systems, Honeywell International, Smiths Group. |

Frequently Asked Questions

North America dominated the Maritime Security Market in 2025.

Port & Critical Infrastructure Security dominated the Maritime Security Market with a 48.36% share in 2025.

Rising maritime trade, increasing piracy and illegal activities, growing geopolitical tensions, and stricter port and border security regulations are driving demand for advanced maritime security solutions.

The Maritime Security Market size was USD 31.43 Billion in 2025 and is expected to reach USD 46.60 Billion by 2035.

The Maritime Security Market is expected to grow at a CAGR of 4.06% from 2026–2035.

Get in Touch