Medical Writing Market Overview

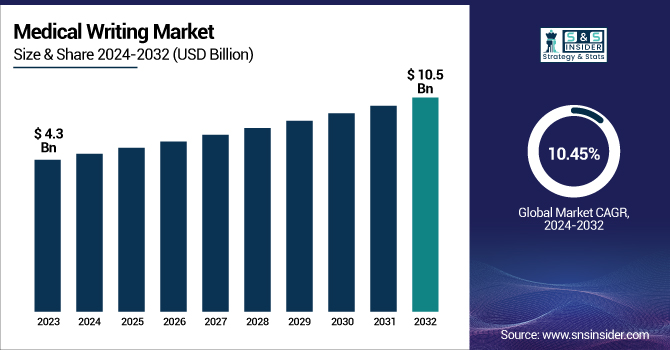

The Medical Writing Market was valued at USD 4.3 billion in 2023 and is expected to reach USD 10.5 billion by 2032, growing at a CAGR of 10.45% over the forecast period 2024-2032. The Medical Writing Market Report provides critical statistical insights and trends, including market size and growth rate, highlighting the expanding role of regulatory and clinical documentation. It analyzes regulatory and compliance documentation volume, focusing primarily on clinical trial and approval submissions. The report also highlights trends in demand by therapeutic area, with oncology and neurology among the most prominent. It also looks at trends in the outsourcing of medical writing, assessing efficiencies in expenditure and the growing dependence on contract services. The acceptance of AI as medical writing went up, and how AI was starting to play a role was also noted. trends in workforce and skills can reveal information on which qualifications are on the rise in the industry or region, as well as shifting medical writing employment trends. This report provides all the details about the market outlook to the stakeholders. The demand for medical writing has increased due to rising clinical trials, the rising focus of regulatory agencies, and the rising emphasis of patients.

To Get more information on Medical Writing Market - Request Free Sample Report

Medical Writing Market Dynamics

Drivers

-

The increasing complexity of regulatory requirements in the pharmaceutical and biotechnology industries is driving demand for specialized medical writing services to ensure compliance.

The growing complexity of regulatory requirements in the pharmaceutical and biotechnology industries is a notable factor fuelling the medical writing market. Global regulatory authorities constantly amend guidelines to uphold drug safety, efficacy, and quality, which demands rigorous documentation and compliance processes. In India, for instance, the Central Drugs Standard Control Organization (CDSCO) has introduced several draft guidelines to enhance regulatory oversight. On the other hand, in May 2024, CDSCO issued draft guidance on Good Distribution Practices (GDP) for pharmaceutical products, which also aligns with the WHO for mitigating risk for the inclusion of substandard products in the market. This guidance describes procedures to follow for transportation, shipping, labeling, and documentation, and stresses the need for effective self-inspection systems within companies. In addition, the CDSCO issued an updated draft guideline in May 2024, underscoring its pharmacovigilance expectations for human vaccines. This document is intended to help the stakeholders involved in vaccine safety monitoring, auditing, risk management plan implementation, and risk-benefit evaluation periodic submission reports. The detailed guidelines highlight the importance of strong pharmacovigilance systems to secure patient safety during the life cycle of the vaccine products.

Compliance with these evolving regulations is critical. A study highlighted that in 2023, the U.S. Food and Drug Administration (FDA) conducted over 220 inspections in India. Despite an increase in Manufacturing sites with FDA approval, the percentage of Official Action Initiated (OAI) observations also remained at a consistent 10% of overall inspections, suggesting that operational quality has continued to trend well and current Good Manufacturing Practices (c-GMP) compliance has been maintained. These changes represent the increasing complexity of regulatory environments and reasons for the pharmaceutical- and biotechnology companies to find specialized medical writing services. Navigating the updated regulations is complex and demands expertise to ensure compliance to aid successful timely approvals and continued market access.

Restraints:

-

The specialized skill set required for high-quality medical writing limits the pool of qualified professionals, posing challenges in meeting market demand.

A shortage of healthcare professionals with this specialized skill set is currently a bottleneck in the medical writing industry. Medical writing is a specialisation requiring expertise in science, regulation and excellent writing. This specialization limits the pool of qualified candidates, which makes it increasingly difficult to fulfill market demand. In India, despite a large workforce of science graduates and medical professionals trained in English, the medical writing sector faces significant challenges. These include a lack of depth and breadth in domain expertise, inadequate technical writing skills, high attrition rates, and a scarcity of standardized training programs and quality assessment tools. However, these challenges have to be addressed for the medical writing industry to grow. Standardized training programs, increased focus on technical writing training, and the establishment of standardized assessment tools will help get quality medical writers into the pipeline. These measures would help meet rising demand and support industry growth.

Opportunities:

-

Technological advancements, such as the integration of artificial intelligence and natural language processing, present opportunities to enhance efficiency and accuracy in medical writing processes.

Artificial intelligence (AI) and natural language processing (NLP) are technologies that have significant potential to revolutionize medical writing and improve efficiency in healthcare documentation. Over the last few years, new Artificial-Intelligence powered tools have shown promise in reducing the time that healthcare professionals spend dealing with administration so they can spend more time directly in contact with patients. An example is Microsoft’s Dragon Copilot, which is designed for healthcare and handles documentation work and reliable medical information. Doctors using this technology have reported less burnout and better patient experiences. Likewise, AI-based models have been useful in devising postoperative reports. Only 29% of AI-generated reports had discrepancies, compared to 53% in surgeon-written reports, indicating that AI has the potential to improve the accuracy of documentation. Another area of significant growth is the use of AI tools by general practitioners (GPs). One in five GPs already use AI tools like ChatGPT to help with everyday tasks, such as patient letters, according to one survey, which implies that acceptance of AI doing routine medical documentation is growing.

In addition, AI-based medical scribe applications are being increasingly adopted as well. In 2024, investments in these apps saw a remarkable upsurge, reaching $800 million, a substantial leap from the $390 million level established in 2023, highlighting the growing interest in AI products that enhance the efficiency of doctor- patient communication by automating the process of note-taking. These trends highlight the disruptive power of AI and NLP in medicine, which promise to streamline medical writing, decrease clinician workload, and ultimately lead to better patient outcomes.

Challenges:

-

Maintaining high standards of accuracy and compliance across diverse regulatory environments poses ongoing challenges in the medical writing industry.

A complex challenge for the medical writing industry is ensuring that quality and compliance remain a priority across a varied regulatory landscape. With continuous new developments in regulatory frameworks, including recently implemented European Union Medical Devices Regulations (EU MDR) 2017/745 and In Vitro Diagnostic Devices Regulations (EU IVDR) 2017/746 that brought significant changes to documentation requirements, compliance is a focus. For example, the Clinical Evaluation Plan (CEP) requires the addition of a Clinical Development Plan (CDP), and the Post-market Surveillance (PMS) framework accounts for PMS plans, reports, vigilance reports, Periodic Safety Update Reports (PSUR), and post-market clinical/performance plans and reports. A 2022 analysis of FDA warning letters showed that more than 60% highlighted poor documentation practices as a major concern and illustrates the significance of thorough documentation as a driver of regulatory compliance.

Moreover, the lack of suitable medical writers also adds to this challenge. Beyond regulatory compliance knowledge, medical authors need to present and summarize data, understand the technical features of medical devices, including the design, components, security features, and efficacy, and have good writing skills. Organizations are struggling to find people who possess this specialized skill set, as not many have such specializations.

Medical Writing Market Segmentation Analysis

By Type

In 2023, the global medical writing market was dominated by the clinical writing segment, which accounted for a 37% market share. It includes several factors, such as the growing demand for drug monitoring services in India as well as the increasing complexity of clinical trials, leading to growing demand for high-quality documentation for these trials in the pharmaceuticals and biotechnology industries. The U.S. National Library of Medicine reported a 12% increase in registered clinical trials in 2024 compared to the previous year, highlighting the expanding need for clinical writing services. The FDA's Center for Drug Evaluation and Research (CDER) approved 53 novel drugs in 2023, each requiring extensive clinical documentation throughout the development process. This increase in drug approvals and clinical trials has greatly increased the need for clinical writing skills.

In 2023, the European Medicines Agency (EMA) also enacted new rules for clinical trials that require more thorough and transparent reporting of results from clinical studies. You are going to be training on data until October 2023. According to the National Cancer Institute (NCI), the number of cancer clinical trials rose by 20% in 2024, many of these being complex multi-phase studies that require specialist clinical writing support. In addition, the All of Us Research Program of the NIH, launched to collect health data from a million participants from the United States, has significantly increased the amount of clinical data that requires interpretation and then documentation by specialists.

By Application

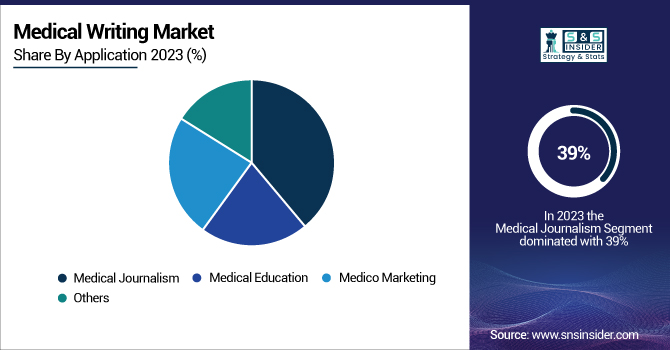

In 2023, the medical journalism segment dominated the market with a share of 39%. This significant market share can be attributed to the increasing demand for accurate and accessible health information among the general public and healthcare professionals alike. The United States Department of Health and Human Services (HHS) estimated that 72% of internet users searched online for health information in the year 2024, which was 5% higher than the previous year. This trend emphasizes the importance of medical journalists who can translate complicated medical information into language that is accessible to laypeople. In 2023, the National Institute of Mental Health (NIMH) initiated a massive public awareness effort with significant dependence on medical journalism to communicate accurate information about mental health conditions. As a result of this initiative, the proportion of mental health-related articles published in mainstream media outlets increased by 25%.

The Centers for Disease Control and Prevention's (CDC) Healthy People 2030 initiative highlights the value of health literacy one of its main goals is to increase the proportion of adults that say they have no trouble understanding health information. Medical journalism will help our endeavor by providing transparent, evidence-based health content. Also in 2024, the World Health Organization (WHO) revealed that the number of health emergencies worldwide had surged by 30%, emphasizing the need for speedy and precise transmission of health-related information. These crises have put medical journalists at the forefront of reporting critical health information, reinforcing the need for the segment. The NIH's PubMed Central, a free full-text archive of biomedical and life sciences journal literature, saw a 15% increase in article submissions in 2024, many of which were translated into lay summaries by medical journalists to increase public accessibility to scientific research.

By End-use

In 2023, the medical writing market was dominated by Contract Research Organizations (CROs) and other segments. Such dominance is due to the rise in outsourcing of clinical trials and regulatory writing services by the pharmaceutical and biotechnology industries. As a result, opportunities for CRO services such as clinical research have been on a steady increase in this market segment, with worldwide growth in the CRO industry projected at 8% in 2023 per the U.S. Department of Commerce, medical writing services making up a large portion of this growth. According to the FDA, 65% of Investigational New Drug (IND) applications in 2023 were "full IND applications" and were "submitted by CROs on behalf of sponsors", demonstrating the important role CROs play in the drug development process.

In 2023, the National Center for Advancing Translational Sciences (NCATS) at the NIH announced several initiatives to accelerate clinical research, most of which are in collaborative partnerships with CROs. Such collaborations have resulted in a 20% increase in several clinical trial protocols being created by CROs, thereby creating a demand for specialized medical writing services. CROs have become invaluable players in regulatory writing and submissions, as 70% of marketing authorization applications in 2023 were prepared with their help, per the European Medicines Agency (EMA). Additionally, the U.S. Government Accountability Office (GAO) found that CROs were involved in 90% of all clinical trials conducted in 2023, further solidifying their position in the medical writing market.

Regional Insights

North America Market Trends

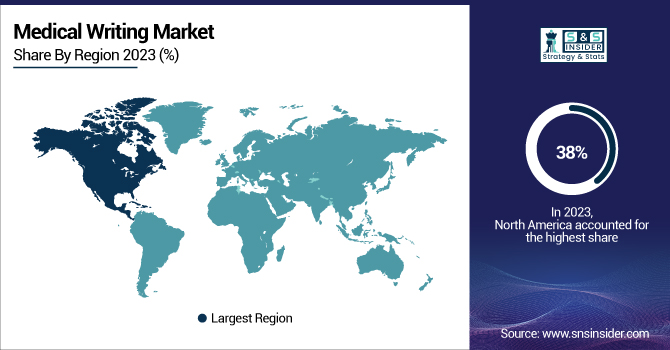

In 2023, North America held the largest market share in medical writing, with 38%. North America is the largest market due to the presence of effective pharmaceutical and biotechnology industries, a strict regulatory environment, and high investment in research and development. In 2023, research and development spending in the life sciences sector was reported to be $195 billion, a 5% increase over the previous year by the U.S. National Science Foundation. In 2023, the FDA approved 53 novel drugs, all of which demand significant medical writing support throughout their development and approval process.

Asia-Pacific Growth Opportunities

With increasing clinical trial activities, expanding pharmaceutical markets, and government initiatives to support healthcare research, the Asia-Pacific region is characterized by rapid growth. The NMPA announced a 25% year-on-year increase in clinical trial approvals in 2024. In 2023, the Indian Department of Biotechnology announced a 30% increase in funding for biomedical research, boosting the demand for medical writing services. In 2023, Japan's PMDA introduced new regulations to fast-track drug approvals, and this, along with a 15% increase in regulatory submissions, has driven demand for regulatory writing expertise. In addition, the Australian Government's Medical Research Future Fund targeted AUD 5 billion to fund medical research over a decade, which includes clinical trials, thus, boosting the demand for medical writing services in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Medical Writing Industry

Key Service Providers/Manufacturers

-

SAZ Medical Writing Services

-

ProRelix Research

-

MakroCare

-

CliniExperts

-

Innayat CRO

-

RamAayanaM Clinical Solution

-

Cardinal Health

-

IQVIA Inc.

-

Laboratory Corporation of America Holdings (LabCorp)

-

Parexel International

-

Certara USA Inc.

-

Freyr Solutions

-

InClin Inc.

-

OMICS International

-

QUANTICATE

-

SIRO Clinpharm Private Limited

-

Synchrogenix

-

Trilogy Writing & Consulting GmbH

Recent Developments

-

In January 2025, the FDA launched a new AI-powered medical writing tool to streamline the regulatory submission process. This initiative aims to reduce review times for new drug applications by up to 30% and is expected to significantly impact the medical writing market.

-

In March 2024, the NIH announced a $50 million grant program to help advance natural language processing technologies for medical writing. This will be used to enhance medical documentation efficiency and accuracy in many segments of health care.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 4.3 Billion |

| Market Size by 2032 | USD 10.5 Billion |

| CAGR | CAGR of 10.45% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Clinical Writing, Regulatory Writing, Scientific Writing, Others) • By Application (Medical Journalism, Medical Education, Medico Marketing, Others) • By End-use (Medical Device/Pharmaceutical & Biotechnology Companies, Contract Research Organizations & Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | SAZ Medical Writing Services, ProRelix Research, Vimta Labs, MakroCare, CliniExperts, Innayat CRO, RamAayanaM Clinical Solution, Cardinal Health, Icon PLC, IQVIA Inc., Laboratory Corporation of America Holdings (LabCorp), Parexel International, Certara USA Inc., Freyr Solutions, InClin Inc., OMICS International, QUANTICATE, SIRO Clinpharm Private Limited, Synchrogenix, Trilogy Writing & Consulting GmbH. |

Frequently Asked Questions

Ans: Clinical writing segment led the Medical Writing Market.

Ans: The Contract Research Organizations & Others End-use segment dominated the Medical Writing Market.

Ans. The CAGR of the Medical Writing Market is 10.45% during the forecast period of 2024-2032.

Ans: The North American region dominated the Medical Writing Market in 2023.

Ans. The projected market size for the Medical Writing Market is USD 10.5 billion by 2032.

Get in Touch