Nitinol-Based Medical Device Market Report Scope & Overview:

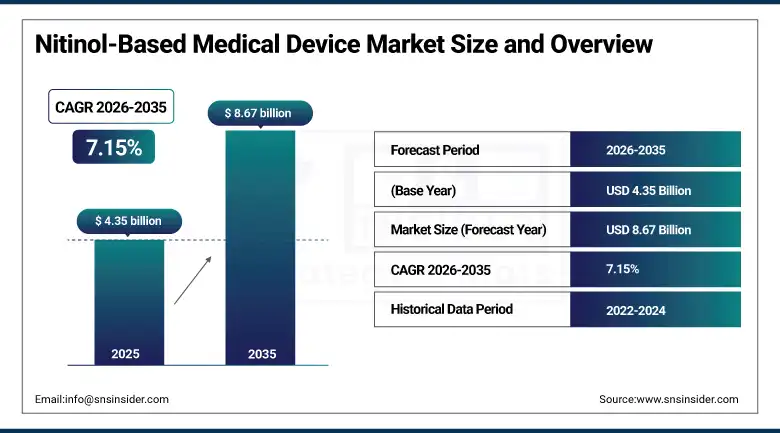

The Nitinol-Based Medical Device Market was valued at USD 4.35 Billion in 2025 and is expected to reach USD 8.67 Billion by 2035, growing at a CAGR of 7.15% from 2026–2035.

The global nitinol-based medical device market is advancing on the foundation of minimally invasive procedure adoption, whose clinical and commercial superiority over open surgery is progressively expanding the range of conditions and patient populations that interventional device-based treatment serves effectively. Nitinol, the nickel-titanium alloy whose unique shape memory and superelastic properties enable medical devices to navigate tortuous anatomical pathways, expand to conform to vessel or luminal geometry, and return to pre-programmed shapes after deformation, has become the material of choice for the interventional cardiology, neurovascular, urological, and peripheral vascular device categories whose clinical performance depends on mechanical characteristics that no alternative biocompatible material can replicate at equivalent cost.

Boston Scientific launched a next-generation nitinol peripheral stent platform in 2025 with improved radial strength and durability for long-segment arterial disease, addressing challenging atherosclerotic lesions requiring flexible, fatigue-resistant stents that maintain vessel patency under repeated arterial motion and deformation.

Nitinol-Based Medical Device Market Size and Forecast

-

Market Size in 2026E: USD 4.66 Billion

-

Market Size by 2035: USD 8.67 Billion

-

CAGR (2026 to 2035): 7.15%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Nitinol-Based Medical Device Market - Request Free Sample Report

Nitinol-Based Medical Device Market Trends

-

Rising demand for minimally invasive surgical procedures is driving the nitinol-based medical device market.

-

Growing adoption across cardiovascular, orthopedic, and neurovascular applications is boosting market growth.

-

Expansion of aging populations and increasing prevalence of chronic diseases is fueling device usage.

-

Increasing focus on flexibility, biocompatibility, and shape-memory properties is shaping adoption trends.

-

Advancements in stents, guidewires, filters, and orthopedic implants using nitinol alloys are enhancing performance and patient outcomes.

U.S. Nitinol-Based Medical Device Market Outlook

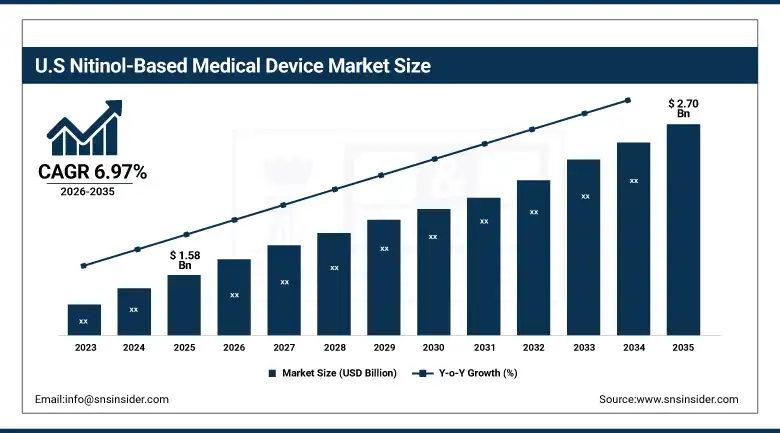

The U.S. Nitinol-Based Medical Device Market was valued at approximately USD 1.58 Billion in 2025 and is expected to reach approximately USD 2.70 Billion by 2033, growing at a CAGR of approximately 6.97%.

The United States is the world’s largest nitinol-based medical device market, driven by the high prevalence of cardiovascular and peripheral vascular disease across a population where approximately 50% of adults carry chronic disease diagnoses and where access to advanced interventional therapy is supported by the world’s most comprehensive medical device reimbursement infrastructure. Medtronic, Boston Scientific, Abbott, Cook Medical, and Edwards Lifesciences collectively serve the majority of the U.S. nitinol device market through established hospital and interventional cardiology suite procurement relationships whose depth of clinical evidence, physician training infrastructure, and technical support capability create durable commercial advantages that newer entrants must invest years to replicate.

Medtronic expanded its nitinol-enabled endovascular platform in 2025 with upgraded delivery systems improving navigability and precision for complex peripheral interventions, addressing rising demand for treatment of critical limb-threatening ischaemia in ageing and diabetic patients, a fast-growing U.S. indication nitinol devices.

Nitinol-Based Medical Device Market Segment Analysis

-

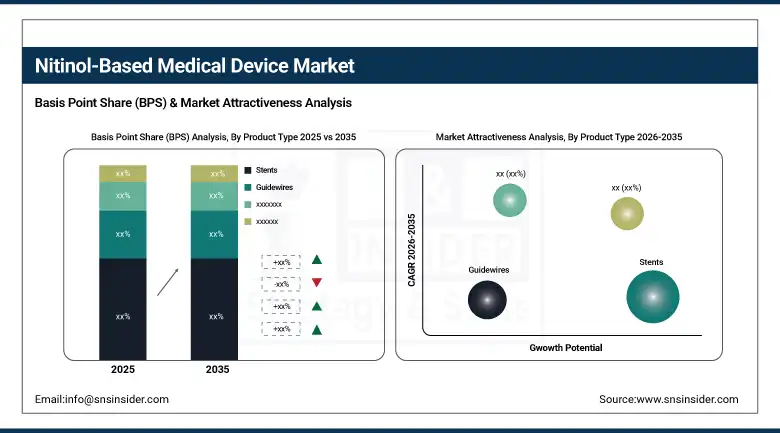

By Product Type, Stents segment dominated the Nitinol-Based Medical Device Market in 2025 with 41% share; Retrieval Devices segment is the fastest growing segment.

-

By Application, Cardiovascular segment dominated the market in 2025 with 56% share; Urology segment is the fastest growing segment.

-

By End User, Hospitals segment dominated the market in 2025 with 63% share; Ambulatory Surgical Centers segment is the fastest growing segment.

By Product Type, stents segment dominated the nitinol-based medical device market, retrieval devices segment is the fastest growing

The Stents segment dominated the Nitinol-Based Medical Device Market in 2025 owing to high incidences of cardiovascular diseases and increasing use of minimally invasive techniques like angioplasty. These stents are highly favored owing to their superior biocompatibility, shape memory and superelastic nature, making them highly flexible and effective in offering vessel support. Moreover, increasing aging population, higher prevalence of coronary artery disease, and the rising demand for advanced vascular interventional medical devices also contributed to the increasing adoption of stents.

The Retrieval Devices segment is the fastest growing owing to the rising demand for minimally invasive techniques to retrieve foreign objects, blood clots, and medical implants from the body. The increasing number of incidents of stroke and vascular obstruction is driving the demand for nitinol-based retrieval devices, like clot retriever devices and filter retriever devices. In addition, advancing technology related to device safety and efficiency is further fuelling the demand for these devices.

By Application, cardiovascular segment dominated the nitinol-based medical device market, urology segment is the fastest growing

The Cardiovascular segment dominated the Nitinol-Based Medical Device Market in 2025 owing to the huge worldwide burden of heart disease such as coronary artery diseases, peripheral artery diseases, and aortic aneurysm. Nitinol-based devices find widespread applications in stents, guidewires, and grafts owing to their elasticity and capacity to accommodate complex vascular architecture. An increase in risk factors owing to the rise in unhealthy lifestyle patterns and geriatric population, along with the popularity of minimally invasive cardiac procedures, contributed to growth. Technological innovations in the field of cardiovascular interventions aided the segment's leadership position.

The Urology segment is the fastest growing in the market owing to the increase in the incidence rate of kidney stones, urinary disorders, and prostatic diseases. Nitinol-based medical devices such as ureteral stents, basket retrievers, and guidewires are frequently employed owing to their flexibility and durability, along with their minimally invasive nature. Growing awareness about early diagnosis and technological advancements in the field of minimally invasive urological procedures helped the segment grow.

By End User, hospitals segment dominated the nitinol-based medical device market, ambulatory surgical centers (ASCS) segment is the fastest growing

The Hospitals segment dominated the Nitinol-Based Medical Device Market in 2025 owing to a large number of surgical and intervention procedures being conducted at hospitals. Hospitals have the necessary infrastructure and expertise along with specialist departments that can undertake complex cardiovascular and urological interventions. Furthermore, with a rise in the number of patients admitted to hospitals for chronic illnesses and emergencies, demand in this segment increased considerably. Also, coverage by insurance policies and the increasing use of minimally invasive medical devices have been major factors contributing to the growth of this segment.

The Ambulatory Surgical Centers (ASCs) segment is the fastest growing due to increased preference among patients and healthcare providers for low-cost and less complicated outpatient-based minimally invasive surgery procedures. Ambulatory surgical centers offer a faster turnaround and lower costs, and the need to reduce hospitalization time is increasing the adoption of minimally invasive surgery devices. Increasing development of medical infrastructure and rising preference for outpatient treatment are the factors driving the segment growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

Japan |

32.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Nitinol-Based Medical Device Market Insights

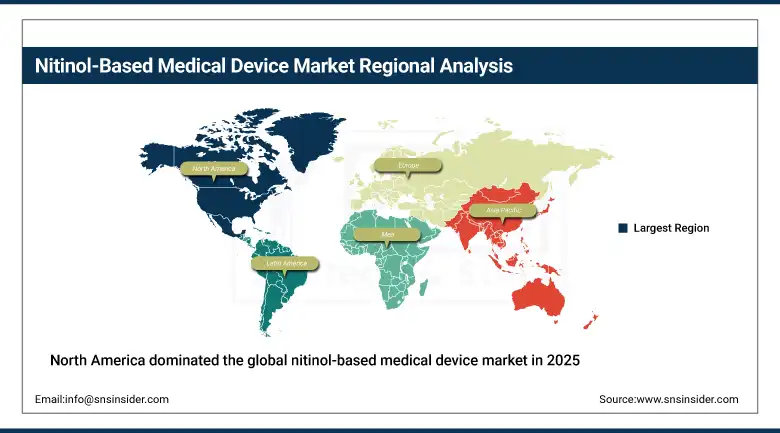

North America dominated the global nitinol-based medical device market in 2025, with the United States accounting for approximately 87.4% of North American revenues and representing the world’s largest national market for nitinol-based interventional devices. The region’s market leadership is grounded in its extraordinary combination of high cardiovascular and peripheral vascular disease prevalence, the world’s most comprehensive medical device reimbursement coverage, and the headquarters concentration of the market’s leading device manufacturers whose R&D investment, clinical evidence development, and physician relationship infrastructure define global device standards.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system whose interventional cardiology and vascular surgery programmes provide consistent clinical procedure volumes that sustain nitinol device procurement, and whose medical device regulatory pathway through Health Canada provides a commercially important approval route for new device introductions whose Canadian regulatory clearance often precedes or parallels FDA authorisation.

According to the U.S. Centers for Disease Control and Prevention (CDC), heart disease causes 695,000 deaths annually in the U.S. The American Heart Association (AHA) reports a stroke occurs every 40 seconds, with 87% ischemic strokes where nitinol stent retrievers used.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Nitinol-Based Medical Device Market Insights

Europe is the world’s second-largest nitinol-based medical device market, where the European CE marking regulatory pathway provides a commercially important approval route for new nitinol device introductions whose notified body review process has historically moved faster than FDA approval for certain device categories. Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, driven by its high interventional cardiology and endovascular procedure volume, its well-funded hospital infrastructure, and the presence of major medical device distributors whose relationships with cardiac catheterisation laboratories sustain consistent nitinol device procurement across the country’s extensive hospital network.

According to the European Society of Cardiology (ESC), cardiovascular diseases cause over 1.7 million deaths annually in the EU, accounting for about 32% of all deaths. The European Commission (Eurostat health data) shows that EU hospitals perform millions of interventional procedures annually, with cardiovascular interventions (PCI and endovascular therapies) forming one of the largest surgical categories.

Asia Pacific Nitinol-Based Medical Device Market Insights

Asia Pacific is the fastest-growing regional nitinol-based medical device market at a CAGR of 7.84% through 2035, driven by the rapidly growing clinical procedure volumes for cardiovascular and neurovascular interventional therapy across China, India, Japan, South Korea, and Southeast Asia whose expanding healthcare infrastructure, growing physician training in interventional techniques, and rising cardiovascular disease burden are collectively creating above-average procedure volume growth. Japan accounts for approximately 32.6% of Asia Pacific revenues through its sophisticated clinical standards, well-funded hospital infrastructure, and strong domestic manufacturing presence in medical device components including nitinol raw materials.

The World Health Organization reports over 10 million cardiovascular deaths annually in Asia, with more than 80% occurring in low- and middle-income countries. In India, cardiovascular diseases account for about 28% of total deaths, alongside rapid growth in catheter-based interventions in tertiary hospitals. In China, over 330 million people are affected by cardiovascular diseases, supported by the expansion of PCI-capable hospitals in tier-2 and tier-3 cities.

MEA & Latin America Nitinol-Based Medical Device Market Insights

The Middle East and Africa and Latin America are growing nitinol-based medical device markets where expanding healthcare infrastructure investment, rising cardiovascular disease burden, and growing physician training in interventional techniques are creating structured demand for minimally invasive device therapy. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its well-funded healthcare system whose world-class cardiac centres at institutions including King Faisal Specialist Hospital and King Abdulaziz Medical City perform high-volume interventional cardiology programmes whose device procurement includes the full range of nitinol-based coronary, peripheral, and structural heart intervention consumables.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large hospital infrastructure, active interventional cardiology community, and the SUS universal healthcare system’s coverage of cardiac interventional procedures that creates consistent clinical procedure volumes sustaining nitinol device procurement across public and private hospital sectors.

According to the Pan American Health Organization, cardiovascular diseases cause approximately 31% of all deaths in Latin America highlighting major regional burden and rising public health concern across countries there.

Market Dynamics

Growth Drivers: Minimally invasive adoption, rising cardiovascular burden, and expanding clinical evidence driving nitinol device market growth globally.

The structural growth driver for the nitinol-based medical device market is the convergence of demographic ageing creating growing cardiovascular disease prevalence and the clinical community’s expanding adoption of minimally invasive nitinol-device-enabled therapies whose superior patient outcomes and economic efficiency relative to open surgery are progressively displacing traditional surgical approaches across both new and established clinical indications. Each new clinical guideline endorsement for an interventional therapy enabled by nitinol devices immediately creates commercial demand across the practice settings where the guideline applies, creating step-change volume increases for specific device categories that compound with the broader procedure volume growth trend.

Restraints: Regulatory complexity, high precision manufacturing costs, and nickel hypersensitivity concerns limiting broader nitinol device adoption.

Regulatory approval requirements for novel nitinol device applications create commercial timeline uncertainty that increases development cost and delays market entry for new clinical indications. The FDA’s PMA pathway for high-risk devices and the EU MDR’s clinical evaluation requirements both demand substantial clinical evidence whose generation in investigational device trials extends the time from device concept to commercial availability, creating capital efficiency challenges for smaller device innovators whose development programmes depend on investor confidence in regulatory pathway timing and outcome.

Nickel hypersensitivity concerns affect approximately 15% of the general population and create patient eligibility questions for nitinol devices in applications where long-term nickel ion release from alloy surfaces could create adverse clinical reactions.

Opportunities: Neurovascular expansion, structural heart innovations, and Asia Pacific healthcare investment creating high-growth nitinol device opportunities.

Neurovascular clot retrieval for acute ischaemic stroke is the most commercially significant near-term growth opportunity for nitinol-based medical devices. Mechanical thrombectomy using nitinol stent-retriever and aspiration devices has been demonstrated in multiple landmark randomised trials to dramatically improve neurological outcomes for eligible stroke patients, generating guideline recommendations that are progressively expanding treatment availability globally. Each expansion of the stroke treatment time window, treatment centre certification, and patient eligibility criteria creates additional thrombectomy procedure volume whose growth rate substantially exceeds the broader nitinol device market average. Structural heart disease device development, encompassing transcatheter aortic valve replacement, transcatheter mitral valve repair and replacement, left atrial appendage occlusion, and patent foramen ovale closure, represents one of the most commercially valuable application categories for nitinol-based device technology.

Recent Developments:

-

2025: Boston Scientific introduced a next-generation nitinol peripheral stent platform in 2025 featuring improved radial strength and enhanced durability for long-segment arterial disease treatment, targeting the growing clinical demand for interventional therapy of critical limb-threatening ischaemia whose increasing prevalence in ageing and diabetic patient populations is creating one of the fastest-growing nitinol device indications in the peripheral vascular market.

-

2025: Medtronic expanded its nitinol-enabled endovascular platform in 2025 with enhanced delivery system upgrades designed to improve navigability and procedural precision for complex peripheral arterial interventions, targeting interventional radiologists and vascular surgeons whose adoption of endovascular treatment for peripheral artery disease is creating growing demand for devices that combine reliable navigability through tortuous anatomy with the mechanical performance that durable vessel patency requires.

-

2024: Cook Medical received FDA clearance for an enhanced version of its nitinol-based biliary stent system in 2024, expanding the clinical application of nitinol's superelastic properties into malignant biliary obstruction management and providing gastroenterologists and interventional radiologists with a device that maintains bile duct patency more effectively than competing stent alternatives in anatomically challenging pancreatic and hepatic biliary stricture locations.

Nitinol-Based Medical Device Market Key Players

-

Medtronic

-

Boston Scientific

-

Abbott Laboratories

-

Stryker Corporation

-

Cardinal Health

-

Cook Medical

-

C. R. Bard (now part of BD)

-

Terumo Corporation

-

MicroPort Scientific

-

Teleflex Incorporated

-

Conformis, Inc.

-

Merit Medical Systems, Inc.

-

Endologix, Inc.

-

B. Braun Melsungen AG

-

Gore & Associates

-

BD (Becton, Dickinson and Company)

-

Olympus Corporation

-

A. A. Bellucci (or similar niche Nitinol device innovators)

-

Cochlear Limited

-

Olympus Terumo Biomaterials (OTB)

Nitinol-Based Medical Device Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.35 Billion |

| Market Size by 2035 | USD 8.67 Billion |

| CAGR | CAGR of 7.15% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Stents, Guidewires, Retrival device, Catheters, Others) • By Application (Cardiovascular, Urology, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic, Boston Scientific, Abbott Laboratories, Stryker Corporation, Cardinal Health, Cook Medical, C. R. Bard (BD), Terumo Corporation, MicroPort Scientific, Teleflex Incorporated, Conformis Inc., Merit Medical Systems, Endologix Inc., B. Braun Melsungen AG, Gore & Associates, BD (Becton, Dickinson and Company), Olympus Corporation, Cochlear Limited, Olympus Terumo Biomaterials, A. A. Bellucci. |

Frequently Asked Questions

North America dominated the Nitinol-Based Medical Device Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Retrieval Devices dominated the Nitinol-Based Medical Device Market with 38.60% share in 2025.

Minimally invasive adoption, rising cardiovascular burden, and expanding clinical evidence driving nitinol device market growth globally.

The Nitinol-Based Medical Device Market was valued at USD 4.35 Billion in 2025.

The Nitinol-Based Medical Device Market is expected to grow at a CAGR of 7.15% from 2026 to 2035.

Get in Touch