Nucleotide Market Report Scope & Overview:

Get More Information on Nucleotide Market - Request Sample Report

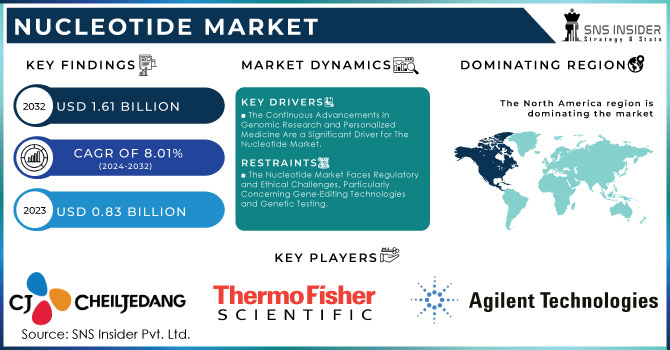

The Nucleotide Market Size was valued at USD 702.38 Million in 2023 and is expected to reach USD 1,319.80 Million by 2032, growing at a CAGR of 7.26% over the forecast period of 2024-2032.

The nucleotide market is evolving rapidly, driven by advancements in biotechnology and pharmaceuticals. Raw material analysis and pricing trends shape production costs, with fluctuations in ribose and phosphates influencing supply chains. Navigating the regulatory landscape and compliance requirements is crucial, as global authorities enforce stringent quality standards. Rising investments and funding analysis highlight growing interest in nucleotide-based innovations. A detailed product pipeline and R&D analysis reveal breakthroughs in RNA therapeutics, vaccines, and precision medicine. The impact of synthetic biology and genetic engineering is revolutionizing synthesis, making production more efficient and expanding applications in synthetic genomics. Our report provides exclusive insights into these key factors, offering a data-driven perspective on the dynamic nucleotide industry.

The US Nucleotide Market Size was valued at USD 207.40 Million in 2023 and is expected to reach USD 378.65 Million by 2032, growing at a CAGR of 6.92% over the forecast period of 2024-2032.

The U.S. nucleotide market is expanding rapidly, driven by advancements in biotechnology, pharmaceuticals, and food science. Increasing demand for RNA-based therapeutics and gene editing technologies, supported by organizations like the National Institutes of Health (NIH) and Biomedical Advanced Research and Development Authority (BARDA), is fueling growth. The presence of major players such as Thermo Fisher Scientific and Agilent Technologies strengthens research and development efforts. Additionally, the rising use of nucleotides in infant nutrition and functional foods, as recognized by the U.S. Food and Drug Administration (FDA), further boosts market demand. Strong regulatory frameworks and government funding contribute to the country’s dominance in nucleotide innovation and production.

Market Dynamics

Drivers

-

Advancements in Personalized Medicine and Nucleotide-Based Therapies Drive the Growth of the Nucleotide Market

The increasing adoption of personalized medicine is a key driver of the nucleotide market, as nucleotides serve as essential building blocks for developing targeted therapies. Advances in RNA-based drugs, mRNA vaccines, and antisense oligonucleotides are fueling the demand for high-quality nucleotides. In the U.S., organizations like the National Institutes of Health (NIH) and the Food and Drug Administration (FDA) are funding research into nucleotide-based treatments for cancer, neurodegenerative disorders, and rare genetic diseases. The rise of next-generation sequencing (NGS) and gene therapy innovations is further propelling the demand for nucleotides in diagnostics, drug discovery, and genetic modification. Companies such as Moderna and Pfizer continue to invest in synthetic nucleotides for advanced therapeutic solutions, increasing market growth. The rapid expansion of companion diagnostics and precision medicine approaches is also contributing to the increased usage of nucleotides, as they enable gene expression analysis, biomarker discovery, and molecular diagnostics. With pharmaceutical and biotech companies focusing on nucleotide-based formulations, the market is expected to see significant expansion in the coming years.

Restraints

-

High Production Costs and Complex Manufacturing Processes Restrain the Growth of the Nucleotide Market

The production of nucleotides involves complex biochemical synthesis, enzymatic modifications, and purification processes, leading to high operational costs. The need for specialized fermentation technology, advanced bioprocessing equipment, and stringent quality control further escalates expenses. Enzymes required for nucleotide synthesis are difficult to source and costly, making large-scale production financially challenging. Companies must invest in state-of-the-art production facilities and high-purity raw materials, increasing capital expenditure. Additionally, maintaining Good Manufacturing Practices (GMP) and pharmaceutical-grade nucleotide standards adds to compliance costs. Smaller biotech firms struggle to compete due to limited scalability and high entry barriers. The price volatility of raw materials, including ribose sugars, phosphate derivatives, and nitrogenous bases, further impacts profit margins. Manufacturers must navigate supply chain disruptions, geopolitical restrictions, and trade policies, increasing market uncertainty. Research institutions also face funding constraints when working on nucleotide-based applications. These financial burdens limit the widespread adoption of nucleotides in functional foods, pharmaceuticals, and genetic research. Cost-effective synthesis technologies and innovative production strategies are required to overcome these market challenges.

Opportunities

-

Growing Investments in Nucleotide-Based Vaccines and RNA Therapeutics Create New Growth Prospects for the Nucleotide Market

The success of mRNA vaccines for COVID-19, developed by Pfizer-BioNTech and Moderna, has demonstrated the potential of nucleotide-based therapeutics in treating infectious diseases, cancers, and rare genetic disorders. Government organizations such as Biomedical Advanced Research and Development Authority (BARDA) and the National Institutes of Health (NIH) are increasing investments in RNA-based drugs, self-amplifying RNA vaccines, and nucleotide analogs. The demand for oligonucleotide therapeutics, including small interfering RNAs (siRNAs) and antisense molecules, is growing due to their applications in personalized medicine and gene therapies. Companies are expanding their nucleotide synthesis capabilities to support the development of next-generation vaccines and precision medicine solutions. The ongoing research into long-lasting mRNA formulations, lipid nanoparticle delivery systems, and stable nucleotide analogs further enhances market potential. Advances in DNA and RNA synthesis technologies are improving cost-efficiency and production scalability. As clinical trials expand and FDA approvals increase, the nucleotide market will benefit from new treatment modalities and commercial applications, driving sustained growth in the pharmaceutical and biotech sectors.

Challenge

-

Intellectual Property Barriers and Patent Restrictions Limit Innovation in the Nucleotide Market

The nucleotide industry is dominated by patent-protected technologies and proprietary synthesis processes, restricting innovation among smaller biotech firms, academic researchers, and emerging manufacturers. Leading companies such as Thermo Fisher Scientific, Merck KGaA, and Agilent Technologies hold exclusive rights to advanced nucleotide synthesis techniques, genetic sequencing platforms, and proprietary enzymatic modifications, limiting competition. High licensing fees and strict intellectual property (IP) enforcement policies create challenges for startups and research institutions seeking to develop novel nucleotide-based applications. Additionally, complex patent landscapes, ongoing legal disputes, and restrictive patent extensions hinder the adoption of new synthesis methods and biotechnological advancements. This limits market entry for new players, slowing down the development of cost-effective and innovative nucleotide solutions. Companies must navigate IP negotiations, licensing agreements, and regulatory approvals to commercialize new nucleotide-based technologies. Collaboration between biotech firms, academic institutions, and government agencies is essential to overcoming these patent-related challenges and fostering a more competitive nucleotide market.

Segmental Analysis

By Product

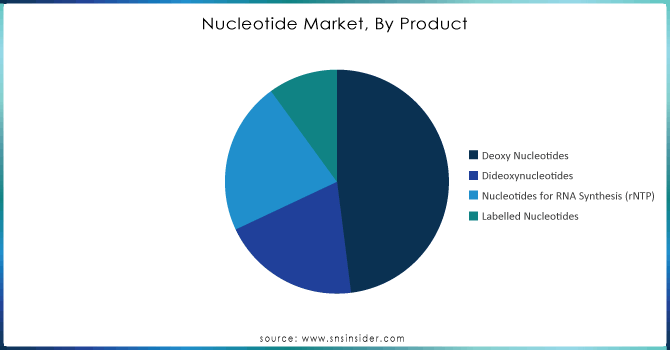

Deoxy nucleotides dominated the nucleotide market in 2023, holding a market share of 41.5% due to their essential role in DNA replication, sequencing, and genetic engineering. Their widespread application in polymerase chain reaction (PCR), next-generation sequencing (NGS), and synthetic biology has significantly contributed to market expansion. The National Institutes of Health (NIH) and the U.S. Food and Drug Administration (FDA) have emphasized the increasing role of deoxy nucleotides in gene therapy, vaccine development, and personalized medicine. The success of mRNA-based vaccines, such as COVID-19 vaccines developed by Moderna and Pfizer-BioNTech, has accelerated research in genetic and molecular medicine, further increasing demand for deoxy nucleotides. Additionally, CRISPR-Cas9 gene editing advancements require high-purity deoxy nucleotides for precise modifications, supporting their market growth. With continued investments from biotechnology firms, academic institutions, and pharmaceutical companies, deoxy nucleotides remain the preferred choice for genetic research, molecular diagnostics, and therapeutic applications. Growing R&D initiatives in cancer genomics, hereditary disease studies, and synthetic DNA production further drive the segment’s strong market presence, solidifying its leading position in the nucleotide industry.

By Technology

TaqMan Allelic Discrimination dominated the nucleotide market in 2023, accounting for a market share of 45.2%, driven by its high specificity, accuracy, and efficiency in genotyping and molecular diagnostics. This technology is widely used in genetic testing, pharmacogenomics, and clinical diagnostics, making it the preferred method for single nucleotide polymorphism (SNP) analysis and mutation detection. The Centers for Disease Control and Prevention (CDC) and NIH utilize TaqMan-based assays for infectious disease monitoring, hereditary disorder screening, and oncology research. Its role in COVID-19 variant tracking and personalized medicine initiatives has further strengthened its dominance. Pharmaceutical companies increasingly use TaqMan assays for biomarker identification and precision medicine applications, enhancing drug development processes. Additionally, government funding and academic research on genetic predisposition to diseases and forensic DNA analysis are fueling demand. As advancements in gene expression analysis, real-time PCR, and molecular epidemiology continue to grow, TaqMan Allelic Discrimination remains a cornerstone in genetic research and diagnostic applications, ensuring its leadership in the nucleotide market.

By Application

Diagnostics research dominated the nucleotide market in 2023, securing a market share of 37.9%, driven by the rising prevalence of infectious diseases, genetic disorders, and cancer. The increasing demand for high-precision molecular diagnostics and early disease detection has propelled the segment’s growth. The U.S. Food and Drug Administration (FDA) and NIH actively support advancements in next-generation sequencing (NGS), polymerase chain reaction (PCR), and nucleic acid-based diagnostic assays, strengthening their adoption in clinical and research settings. Nucleotides play a crucial role in biomarker discovery, prenatal genetic screening, and forensic DNA analysis, making them indispensable in modern healthcare. Government initiatives promoting precision medicine and liquid biopsy technologies have further accelerated the expansion of nucleotide-based diagnostic research. The use of nucleotide probes and primers in pandemic response efforts, such as COVID-19 and emerging viral diseases, has demonstrated the critical role of nucleotides in global health surveillance and epidemic control. With increasing investments in personalized medicine, disease diagnostics, and advanced genetic screening, the segment continues to hold a dominant position in the nucleotide market.

Need any customization research on Nucleotide Market - Enquiry Now

Regional Analysis

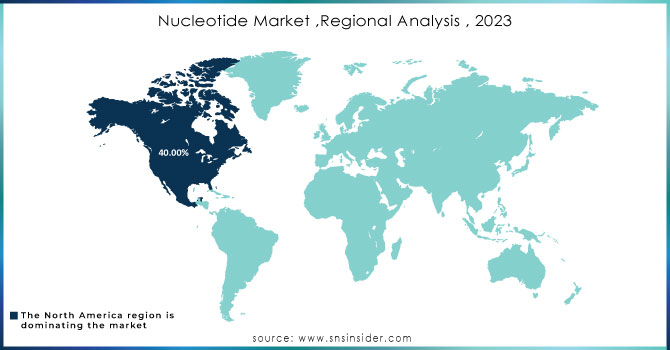

North America dominated the nucleotide market in 2023, holding a market share of 38.7%, driven by the region’s strong biotechnology and pharmaceutical industries, high R&D investments, and advanced healthcare infrastructure. The presence of leading companies such as Thermo Fisher Scientific, Merck KGaA, and New England Biolabs has fueled innovations in nucleotide-based diagnostics, therapeutics, and genetic research. The National Institutes of Health (NIH) and the U.S. Food and Drug Administration (FDA) have actively supported gene therapy, personalized medicine, and molecular diagnostics, increasing the demand for nucleotides. The United States led the market, accounting for over 80% of North America’s share, owing to its strong presence in next-generation sequencing (NGS), CRISPR gene editing, and mRNA vaccine production. The success of COVID-19 vaccines by Pfizer-BioNTech and Moderna, which rely on nucleotide synthesis, significantly boosted the market. Additionally, the U.S. government allocated $7 billion to the Advanced Research Projects Agency for Health (ARPA-H) to enhance biomedical and genomic research. Canada followed as the fastest-growing nation due to rising investments in synthetic biology and molecular diagnostics, while Mexico’s pharmaceutical sector expansion contributed to regional growth.

Moreover, Europe emerged as the fastest-growing region in the nucleotide market, with a significant market share, fueled by increasing investments in biopharmaceutical research, synthetic biology, and genetic engineering. The European Union’s Horizon Europe program, with a €95.5 billion budget, has significantly contributed to advancements in nucleotide-based therapeutics, gene therapies, and precision medicine. Germany led the market, holding over 35% of Europe’s share, driven by the strong presence of biotech firms such as Merck KGaA and Qiagen, as well as government-backed genomic research initiatives. The United Kingdom followed, with extensive support from the Wellcome Trust and UK Biobank, which are heavily involved in genomic sequencing and disease research. The French government’s investments in biotechnology startups have also propelled the region’s growth. Furthermore, the European Medicines Agency (EMA) has streamlined regulations for nucleic acid-based therapies, encouraging market expansion. The rising adoption of nucleotide-based food & beverage additives and animal feed across the European food industry has further accelerated demand, solidifying Europe’s position as the fastest-growing region in the nucleotide market.

Key Players

-

Ajinomoto Co., Inc. (IMP, GMP, Disodium 5'-Ribonucleotide)

-

Biorigin (Nucleotide Yeast Extract, RNA-rich Yeast Extract)

-

Biosynth Ltd. (Cytidine Monophosphate, Uridine Monophosphate)

-

CJ CheilJedang Corp. (5'-IMP, 5'-GMP, Ribonucleotide Mixtures)

-

Daesang Corporation (Disodium 5'-Ribonucleotide, Yeast Extract Nucleotides)

-

DSM Nutritional Products Ltd. (Purine Nucleotides, Pyrimidine Nucleotides)

-

F. Hoffmann-La Roche Ltd. (Research-grade Nucleotides, Synthetic Nucleotides)

-

Jena Bioscience GmbH (ATP Disodium Salt, CTP Sodium Salt)

-

Lallemand Inc. (Yeast RNA, Nucleotide-rich Yeast Extract)

-

MEIHUA HOLDINGS GROUP CO., LTD. (5'-IMP, 5'-GMP, Yeast-derived Nucleotides)

-

Merck KGaA (Adenosine Monophosphate, Guanosine Monophosphate, Nucleotide Solutions)

-

Meridian Bioscience, Inc. (dNTP Mix, PCR-grade Nucleotides)

-

New England Biolabs Inc. (dNTP Set, Modified Nucleotides)

-

Ohly GmbH (RNA Yeast Extract, 5'-Nucleotides)

-

Promega Corporation (dNTP Mix, ATP Solution, Nucleotide Triphosphates)

-

Prosol S.p.A. (Yeast-derived Nucleotides, Free Nucleotides)

-

Star Lake Bioscience (5'-IMP, 5'-GMP, Disodium 5'-Ribonucleotide)

-

Thermo Fisher Scientific Inc. (dNTP Mix, Nucleotide Triphosphates, RNA Nucleotides)

-

Tianjin Zhongrui Pharmaceutical Co., Ltd. (Disodium 5'-GMP, Disodium 5'-IMP)

-

Zhejiang Yaofi Bio-Tech Co., Ltd. (5'-IMP, 5'-UMP, Ribonucleotides)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 702.38 Million |

| Market Size by 2032 | USD 1,319.80 Million |

| CAGR | CAGR of 7.26% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Deoxy Nucleotides, Dideoxy nucleotides, Nucleotides for RNA Synthesis (rNTP), Others) •By Technology (TaqMan Allelic Discrimination, Gene Chips & Microarrays, SNP By Pyrosequencing, Others) •By Application (Pharmaceuticals, Diagnostics Research, Food & Beverage Additive, Animal Feed Additive, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | CJ CheilJedang Corp., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., DSM Nutritional Products Ltd., MEIHUA HOLDINGS GROUP CO., LTD., Star Lake Bioscience, Biorigin, Lallemand Inc., Ohly GmbH, Ajinomoto Co., Inc. and other key players |

Frequently Asked Questions

Companies like Thermo Fisher Scientific, Merck KGaA, and Agilent Technologies are major contributors to the nucleotide market.

Innovations in synthetic biology, gene editing, and next-generation sequencing are transforming the nucleotide market.

Deoxy nucleotides led the nucleotide market in 2023, holding a 41.5% share due to their role in DNA replication and sequencing.

Advancements in biotechnology, personalized medicine, and nucleotide-based therapies are key drivers of the nucleotide market.

The nucleotide market is expected to reach USD 1,319.80 million by 2032, growing at a CAGR of 7.26%.

Get in Touch