Ophthalmic lasers market report scope & overview

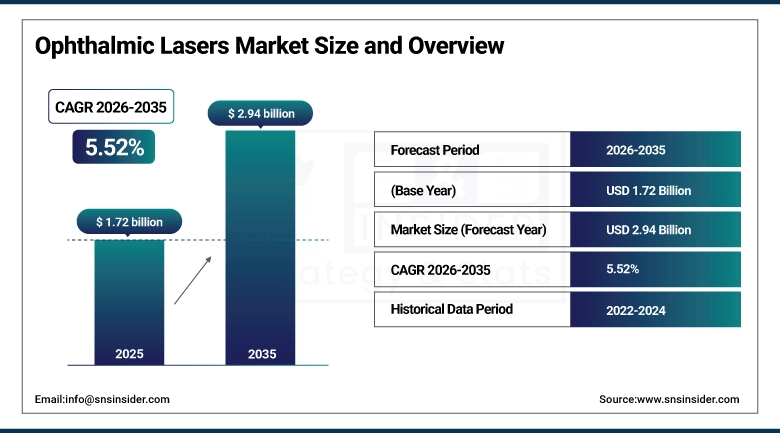

The ophthalmic lasers market was valued at USD 1.72 billion in 2025 and is expected to reach USD 2.94 billion by 2035, growing at a CAGR of 5.52% from 2026–2035.

The global ophthalmic lasers market is advancing steadily on the back of the world’s escalating burden of ocular diseases, an ageing global population whose susceptibility to vision-threatening conditions including cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration increases substantially with every additional decade of life, and the continuous technological innovation in laser platforms that is expanding the clinical indications addressable through laser-based treatment while simultaneously improving procedural safety, accuracy, and patient recovery experience across the full spectrum of ophthalmic laser applications. The World Health Organization’s estimate that approximately 2.2 billion people globally live with some form of vision impairment, combined with the projection that the global population aged over 60 will double to approximately 2.1 billion by 2050, defines the demographic and epidemiological foundation of a structurally growing ophthalmic laser market whose demand trajectory is supported by forces that are largely independent of economic cycles and consumer discretionary spending patterns.

The June 2024 FDA clearance of Carl Zeiss Meditec’s VisuMax 800 femtosecond laser platform for SMILE Pro refractive surgery in the United States marked a landmark event in ophthalmic laser market development, enabling a refractive surgery technique that had achieved substantial market penetration in Europe, Asia Pacific, and the Middle East to enter the world’s largest premium refractive surgery market for the first time, significantly expanding the commercially addressable U.S. refractive procedure market for femtosecond laser systems.

Market Size and Forecast

-

Market size in 2026E: USD 1.82 Billion

-

Market size by 2035: USD 2.94 Billion

-

CAGR: 5.52% from 2026 to 2035

-

Fastest growing region: Asia Pacific

-

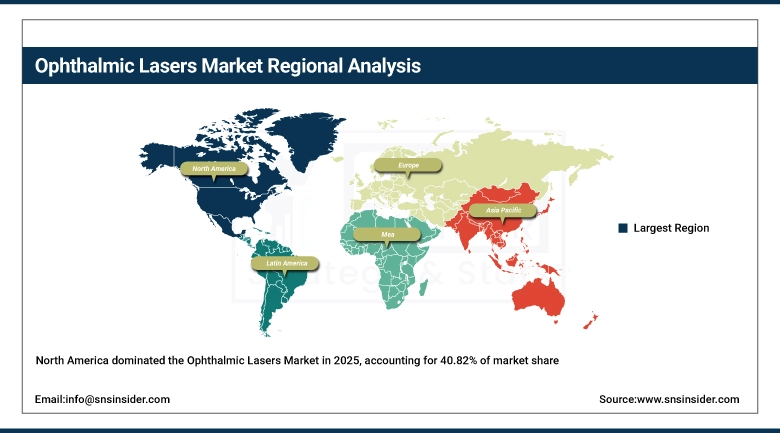

Largest region: North America

To Get more information on Ophthalmic Lasers Market - Request Free Sample Report

Ophthalmic lasers market trends

-

Increasing integration of AI-enabled ophthalmic laser systems is improving surgical precision, treatment customization, and post-operative visual outcomes in refractive and cataract procedures.

-

Rising adoption of selective laser trabeculoplasty (SLT) as a first-line glaucoma treatment is driving demand for advanced ophthalmic laser platforms globally.

-

Growing preference for femtosecond laser-assisted cataract surgery is supporting premium ophthalmic procedure adoption due to improved accuracy and lens positioning outcomes.

-

Expanding ophthalmology infrastructure and increasing myopia prevalence in Asia Pacific are accelerating ophthalmic laser market growth across emerging economies.

-

Integration of ophthalmic laser technologies with telemedicine and digital health platforms is improving remote diagnosis, patient monitoring, and workflow efficiency.

The U.S. ophthalmic lasers market outlook

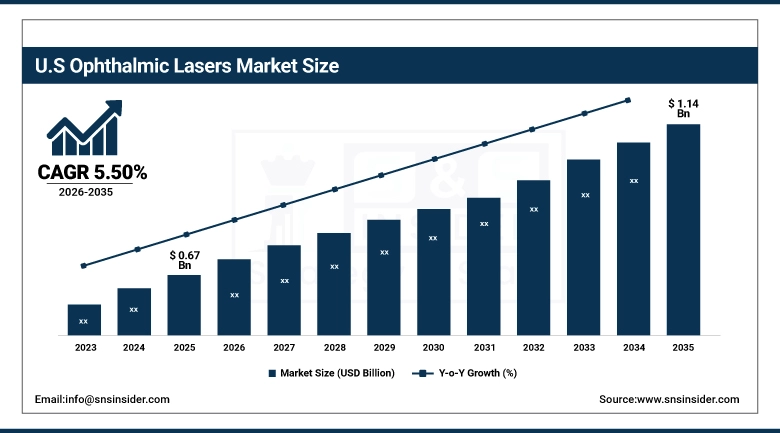

The U.S. ophthalmic lasers market was valued at USD 0.67 billion in 2025 and is expected to reach USD 1.14 billion by 2035, growing at a CAGR of 5.50%, anchored by the world’s highest density of board-certified ophthalmologists per capita, the most extensively developed ambulatory surgical centre infrastructure for outpatient ophthalmic procedures, comprehensive Medicare and commercial insurance coverage for medically necessary laser procedures, and the largest premium refractive surgery market globally whose consumer willingness to pay for superior visual outcomes drives disproportionate adoption of the most technologically advanced femtosecond and excimer laser platforms.

The United States ophthalmic laser market is driven by advanced ophthalmology infrastructure, strong adoption of AI-assisted surgical planning, and rising demand for premium refractive procedures such as LASIK, SMILE, and cataract surgeries. Increasing integration of advanced femtosecond laser systems and digital workflow technologies is further supporting market expansion across ambulatory surgical centers and ophthalmology clinics.

Additionally, Medicare coverage for selective laser trabeculoplasty (SLT) as a first-line glaucoma treatment is accelerating procedure volumes in the U.S., supported by growing clinical acceptance of laser-based glaucoma management and increasing prevalence of age-related eye disorders.

Ophthalmic Lasers Market Segment Analysis

-

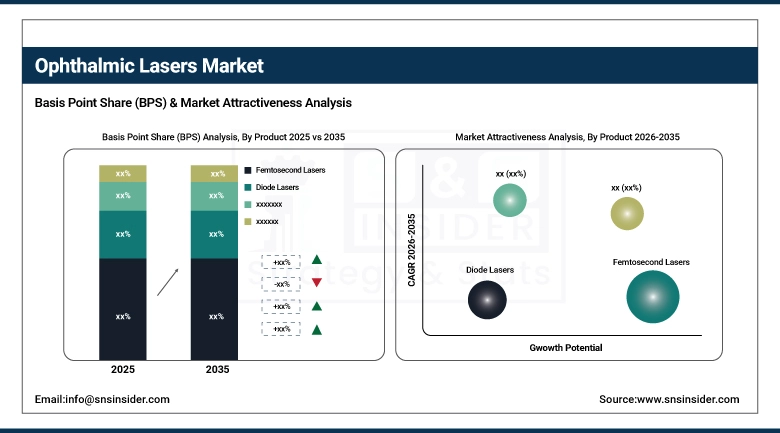

By product, photocoagulation lasers captured the largest revenue share of approximately 43.18% in 2025, driven by their established role as the standard of care for diabetic retinopathy, macular oedema, and retinal tear treatment across the large global patient population with these conditions; femtosecond lasers are the fastest-growing product segment.

-

By application, cataract removal led the ophthalmic lasers market with approximately 32.67% share in 2025. Glaucoma treatment is projected to grow at the highest CAGR of approximately 6.73% through 2035.

-

By end user, outpatient facilities accounted for the largest end-user share of approximately 62.44% in 2025 and are projected to grow at the highest CAGR of approximately 6.08% through 2035.

Photocoagulation lasers dominate product segment, femtosecond lasers grow fastest

Photocoagulation lasers retained the dominant product position with approximately 43.18% of the ophthalmic lasers market in 2025, a dominance grounded in the extraordinary prevalence of the retinal and macular conditions for which photocoagulation laser treatment is the established standard of care and the cumulative decades of clinical evidence, physician training, and healthcare system infrastructure investment that have embedded photocoagulation laser treatment deeply into the global ophthalmology practice landscape. The worldwide burden of diabetic retinopathy, estimated to affect approximately 103 million people globally with prevalence growing proportionally with the diabetes epidemic that shows no sign of abating, represents the most numerically significant demand driver for photocoagulation laser procedure volume, as laser photocoagulation remains the primary intervention for preventing vision loss from proliferative diabetic retinopathy and clinically significant diabetic macular oedema across the global retinal care community.

Femtosecond lasers are the fastest-growing product segment at a CAGR driven by the convergence of several powerful demand forces: the FDA clearance of the VisuMax 800 for SMILE Pro refractive surgery in the United States in June 2024 is enabling the world’s largest premium refractive surgery market to adopt a minimally invasive flapless corneal lenticule extraction technique that has demonstrated superior biomechanical stability, faster visual recovery, and lower dry eye incidence relative to LASIK in comparative clinical studies, creating a significant technology upgrade cycle among U.S. refractive surgery centres.

Cataract removal leads applications, glaucoma grows fastest

Cataract removal retained the dominant application position with approximately 32.67% of the ophthalmic lasers market in 2025, reflecting the extraordinary global prevalence of cataract as both the leading cause of preventable blindness worldwide and the most commonly performed elective surgical procedure across every major healthcare system globally, with the WHO estimating over 17 million cataract surgeries performed annually and procedure volumes continuing to grow as population ageing expands the cataract-affected population faster than current surgical capacity additions can reduce the prevalent backlog in lower-income markets. The premium cataract surgery segment’s progressive adoption of femtosecond laser-assisted techniques is the most commercially dynamic component of the cataract laser market, as patients and surgeons in high-income markets increasingly select femtosecond laser-assisted cataract surgery for its demonstrated advantages in capsulotomy circularity and reproducibility, reduced ultrasound energy during lens fragmentation, and more precise corneal incision geometry that collectively support superior intraocular lens positioning and premium lens optical outcome delivery relative to manual phacoemulsification technique.

Glaucoma treatment is the fastest-growing application at a CAGR of approximately 6.73% through 2035, driven by the remarkable clinical evidence base that has accumulated around selective laser trabeculoplasty’s effectiveness as a first-line open-angle glaucoma treatment and the progressive incorporation of SLT first-line recommendations into major ophthalmology clinical practice guidelines including those of the American Academy of Ophthalmology and the European Glaucoma Society following the LiGHT trial’s definitive evidence of SLT’s clinical equivalence to topical medication with superior patient quality of life and economic outcomes.

Outpatient facilities dominate end user, also grow fastest

Outpatient facilities retained the dominant end user position with approximately 62.44% of the ophthalmic lasers market in 2025 and are simultaneously projected to grow at the highest CAGR of approximately 6.08% through 2035, reflecting the structural transition of ophthalmic laser procedure delivery from hospital-based inpatient and day surgery settings toward the ambulatory surgical centre, refractive surgery clinic, and specialist ophthalmology outpatient department formats that combine clinical safety with patient convenience and healthcare system cost efficiency in ways that are aligning the incentives of patients, practitioners, payers, and healthcare administrators around outpatient delivery as the preferred model for all ophthalmic laser procedure categories where the clinical safety profile of modern laser platforms makes inpatient-level care provision unnecessary. The ambulatory surgical centre model’s particular commercial advantages in ophthalmology reflect the relatively brief procedure times of most ophthalmic laser interventions, the immediate ambulatory recovery profile that laser-based ophthalmic procedures typically provide, and the operational economics of high-volume, streamlined outpatient ophthalmic procedure programmes whose efficiency and patient throughput characteristics generate superior financial performance relative to the higher overhead cost structures of hospital-based surgical suite delivery.

Regional analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America ophthalmic lasers market insights

North America dominated the global ophthalmic lasers market in 2025 with the United States accounting for approximately 87.4% of North American revenues, driven by the world’s highest per-capita ophthalmologist density, the most extensively developed ambulatory surgical centre infrastructure, comprehensive public and private insurance coverage for medically necessary laser procedures, and the largest premium elective refractive surgery market whose consumer willingness to pay for superior visual outcome technology drives disproportionate adoption of the most advanced femtosecond and excimer laser platforms available. The U.S. ophthalmic laser market benefits from the FDA’s rigorous but commercially viable device clearance pathway whose pre-market review processes, while demanding, provide the regulatory approval foundation that enables rapid commercial diffusion of clinically validated new laser technologies across the country’s 18,000 practicing ophthalmologists and 6,000 ambulatory surgical centres with ophthalmic procedure capability. Canada contributes approximately 12.6% of North American ophthalmic laser revenues through a publicly funded healthcare system with broad provincial coverage for medically necessary ophthalmic laser procedures and a growing private pay premium refractive market particularly in British Columbia and Ontario whose urban professional demographic creates strong demand for premium refractive surgery technology.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe ophthalmic lasers market insights

Europe is a technically sophisticated ophthalmic laser market where the concentration of some of the world’s leading ophthalmic laser manufacturers including Carl Zeiss Meditec, Wavelight (acquired by Alcon), and Schwind Eye-Tech-Solutions in Germany and Austria provides the region’s ophthalmology community with privileged access to the most advanced laser platform technologies and the clinical collaboration relationships with manufacturer R&D teams that support frontier application development. Germany accounts for approximately 22.3% of European ophthalmic laser revenues as the region’s largest national market, anchored by a dense network of private refractive surgery centres whose premium service positioning and German consumer culture of quality investment in health and vision drive high-value laser system adoption, combined with a hospital ophthalmology sector whose cataract surgery volume and glaucoma treatment activity generates substantial consumable and service revenue for the installed base of ophthalmic laser platforms across the country’s university hospital ophthalmology departments and major regional eye centres.

Asia Pacific ophthalmic lasers market insights

Asia Pacific is the fastest-growing regional ophthalmic lasers market, driven by the world’s highest myopia prevalence in countries including China, South Korea, Japan, Singapore, and Taiwan where genetic predisposition and educational study intensity create myopia rates of 70 to 90% among young adult populations who represent the primary demographic for refractive surgery procedure consideration, the extraordinary population scale of China and India whose absolute prevalence of cataract, glaucoma, and diabetic retinopathy creates enormous treatment demand that is only beginning to be matched by the healthcare infrastructure capable of delivering laser-based care at the required volume and geographic reach. China accounts for approximately 61.7% of Asia Pacific ophthalmic laser revenues and represents the most commercially consequential growth market in global ophthalmic laser equipment, where the combination of the world’s most severe myopia epidemic creating the largest national refractive surgery patient pool globally, rapid private ophthalmology clinic network expansion in tier-one and tier-two cities, and a growing willingness among China’s urban professional class to invest in premium refractive surgery for spectacle independence is driving laser platform adoption at rates that are making China the fastest-growing national market for premium femtosecond laser refractive platforms of any geography in the world.

Latin America and MEA ophthalmic lasers market insights

Latin America and the Middle East and Africa are growing ophthalmic laser markets where rising prevalence of diabetes-related vision complications, expanding private ophthalmology clinic infrastructure, and growing urban middle-class demand for premium refractive surgery are creating commercially meaningful ophthalmic laser adoption beyond the limited public hospital laser capability that historically characterised these regions’ ophthalmic care delivery. Brazil accounts for approximately 44.2% of Latin American ophthalmic laser revenues through the combination of South America’s most sophisticated private ophthalmology sector, a large diabetic population generating significant retinal laser treatment demand, and a refractive surgery market whose quality and technology standards match those of European equivalents, making Brazil an important test market for new ophthalmic laser platform introductions in the Latin American region.

Market dynamics

Growth drivers: Rising global prevalence of ocular diseases driven by ageing populations and diabetes epidemic, expanding first-line clinical evidence for SLT in glaucoma management

The primary structural growth drivers for the ophthalmic lasers market are the demographically inevitable expansion of the ophthalmic disease burden as global population ageing creates a growing cohort of patients at heightened risk for the age-associated ocular conditions that laser treatment addresses most effectively, combined with the progressive broadening of clinical evidence and guideline endorsement for laser-based treatment across an expanding range of ophthalmic indications that is increasing the proportion of ophthalmic disease patients whose standard of care includes a laser procedure component. The global diabetes epidemic is simultaneously the most powerful non-demographic driver of ophthalmic laser market growth, as the IDF’s projection of 783 million diabetic patients globally by 2045 creates an expanding pipeline of patients at risk for diabetic retinopathy whose progression to vision-threatening complications generates demand for photocoagulation and anti-VEGF combined treatment protocols that include laser as a standard component across the global retinal care infrastructure.

Restraints: High acquisition cost of advanced laser platforms limiting adoption in lower-income markets, reimbursement variability for elective refractive procedures, and clinical learning curve for new laser techniques

A significant restraint on the ophthalmic lasers market is the high capital acquisition cost of premium laser platforms, particularly femtosecond laser systems whose purchase prices in the USD 300,000 to USD 600,000 range represent substantial capital commitments for individual ophthalmology practices and smaller ambulatory surgical centres that may be unable to generate the procedure volume required to justify the acquisition investment through direct procedure revenue, particularly in markets where refractive surgery prices are compressed by competitive intensity or limited by reimbursement schedules that do not adequately reflect the technology cost of femtosecond laser-assisted techniques relative to manual alternatives.

Opportunities: Expanding glaucoma SLT adoption in emerging markets where medication adherence challenges make laser treatment particularly attractive, minimally invasive vitreoretinal laser device development

The selective laser trabeculoplasty opportunity in emerging markets represents a particularly compelling growth vector, as the clinical profile of SLT as a one-time or infrequently repeated office-based procedure without the chronic medication cost and patient compliance requirements of topical glaucoma drops makes it especially advantageous in markets where medication adherence is structurally challenged by medication access, cost, and patient health literacy constraints that limit the effectiveness of chronic pharmacological glaucoma management in real-world clinical practice. New minimally invasive subthreshold and micropulse laser systems for retinal treatment represent an innovation opportunity to expand the proportion of diabetic retinopathy and macular disease patients who are candidates for laser-based treatment, as reduced side effect profiles relative to conventional threshold photocoagulation make these systems appropriate for earlier-stage disease treatment that conventional laser parameters would not justify.

Recent developments

-

2025: Alcon launched an upgraded LenSx femtosecond laser system in February 2025 with enhanced AI-assisted pre-surgical planning and expanded arcuate incision customisation capabilities, targeting the premium cataract surgery segment across North American and European ambulatory surgical centre accounts where surgeons seeking to optimise toric intraocular lens alignment and premium lens outcomes represent the most commercially valuable customer segment.

-

2025: Carl Zeiss Meditec expanded commercial rollout of its VisuMax 800 femtosecond laser platform for SMILE Pro refractive surgery in the United States following the June 2024 FDA clearance, establishing partnerships with leading U.S. refractive surgery centre networks and providing clinical training and outcomes monitoring infrastructure to support the U.S. market’s adoption of SMILE Pro as a premium alternative to LASIK.

-

2025: IRIDEX Corporation advanced its MicroPulse laser therapy product line with updated delivery parameters for subthreshold macular laser treatment, providing retinal specialists with refined clinical protocols for the laser management of diabetic macular oedema and central serous chorioretinopathy that minimise retinal thermal damage while maintaining clinically meaningful anatomical and visual acuity improvement outcomes.

Ophthalmic Lasers Market Key Players are:

-

Alcon Inc.

-

Carl Zeiss Meditec AG

-

Bausch + Lomb Inc.

-

Lumenis Be Ltd.

-

IRIDEX Corporation

-

Topcon Corporation

-

Ellex Medical Lasers Ltd.

-

Johnson & Johnson Vision Care Inc.

-

NIDEK Co., Ltd.

-

Quantel Medical

-

Syneron Medical Ltd.

-

ARC Laser GmbH

-

BISON Medical

-

A.R.C. Laser GmbH

-

Meridian AG

-

Optos plc (Nikon)

-

Ziemer Ophthalmic Systems AG

-

Schwind Eye-Tech-Solutions GmbH

-

Laserex Technologies

-

Eye-Q Laser

Ophthalmic lasers market report scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.72 Billion |

| Market Size by 2035 | USD 2.94 Billion |

| CAGR | CAGR of 5.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Photocoagulation Lasers, Femtosecond Lasers, Excimer Lasers, YAG Lasers, Diode Lasers, SLT Lasers, Others) •By Application (Cataract Removal, Refractive Error Correction, Glaucoma Treatment, Diabetic Retinopathy Treatment, Age-Related Macular Degeneration, Others) •By End User (Outpatient Facilities, Inpatient Facilities) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alcon Inc., Carl Zeiss Meditec AG, Bausch + Lomb Inc., Lumenis Be Ltd., IRIDEX Corporation, Topcon Corporation, Ellex Medical Lasers Ltd., Johnson & Johnson Vision Care Inc., NIDEK Co., Ltd., Quantel Medical, Syneron Medical Ltd., ARC Laser GmbH, BISON Medical, A.R.C. Laser GmbH, Meridian AG, Optos plc (Nikon), Ziemer Ophthalmic Systems AG, Schwind Eye-Tech-Solutions GmbH, Laserex Technologies, Eye-Q Laser |

Frequently Asked Questions

North America dominated the ophthalmic lasers market in 2025, with the United States as the leading national market within the region.

Photocoagulation lasers dominated with approximately 43.18% revenue share in 2025.

Rising global prevalence of age-related ocular diseases including cataracts, glaucoma, diabetic retinopathy, and AMD driven by ageing populations and the diabetes epidemic.

The ophthalmic lasers market was valued at USD 1.72 billion in 2025.

The ophthalmic lasers market is expected to grow at a CAGR of 5.52% from 2026 to 2035.

Get in Touch