Orthopedic Implants Market Report Scope & Overview:

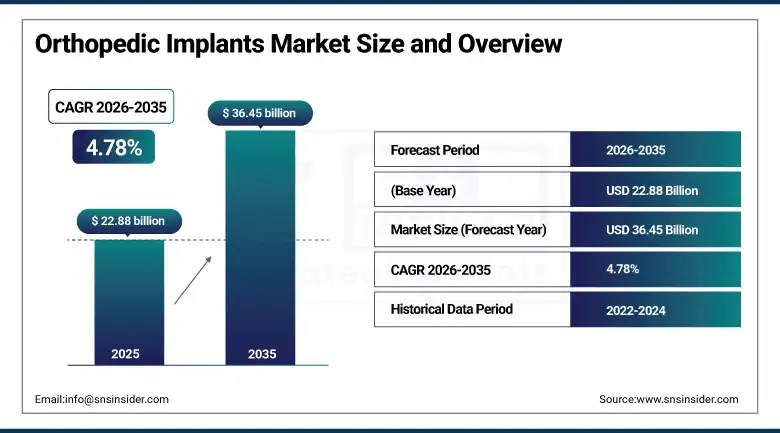

The Orthopedic Implants Market was valued at USD 22.88 Billion in 2025 and is expected to reach USD 36.45 Billion by 2035, growing at a CAGR of 4.78% from 2026–2035.

The global orthopedic implants market is advancing at a commercially reliable pace driven by the dual structural forces of ageing population demographics creating growing musculoskeletal disorder prevalence and the surgical innovation pipeline continuously expanding the clinically appropriate patient population for joint replacement, spinal fusion, and fracture fixation procedures. Musculoskeletal conditions affect approximately 1.71 billion people globally, with osteoarthritis, osteoporosis, and trauma-related fractures representing the primary clinical indications driving orthopedic implant procedure volume growth. The market’s commercial trajectory is reinforced by the progressive extension of joint replacement age indications.

In May 2025, ConforMIS launched its iTotal CR-F patient-specific knee implant in Europe, featuring enhanced personalised fit and improved surgical instrumentation designed specifically for the European market’s regulatory and clinical practice environment. The launch reflects the growing clinical acceptance of patient-specific implants as a premium standard-of-care option whose superior fit and functional outcomes justify above-standard-implant pricing in the European reimbursement environment where clinical outcome evidence increasingly influences procurement decisions.

Market Size and Forecast

-

Market Size in 2026E: USD 23.97 Billion

-

Market Size by 2035: USD 36.45 Billion

-

CAGR: 4.78% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Orthopedic Implants Market - Request Free Sample Report

Orthopedic Implants Market Trends

-

Rising adoption of robotic-assisted orthopedic surgery platforms is improving implant positioning accuracy and reproducibility, creating above-average clinical outcome evidence.

-

Growing development of 3D-printed patient-specific implants is expanding clinical applicability to complex revision cases, unusual anatomy, and younger patients.

-

Increasing investment in bioresorbable and bioactive implant materials is creating next-generation orthopedic implants that provide temporary mechanical support during healing before degrading safely.

-

Rising minimally invasive surgical technique adoption for joint replacement and spinal procedures is improving recovery speed, reducing hospital stay duration.

-

Expanding emerging market healthcare infrastructure investment is creating growing procedure volume capacity in Asia Pacific, Latin America, and the Middle East.

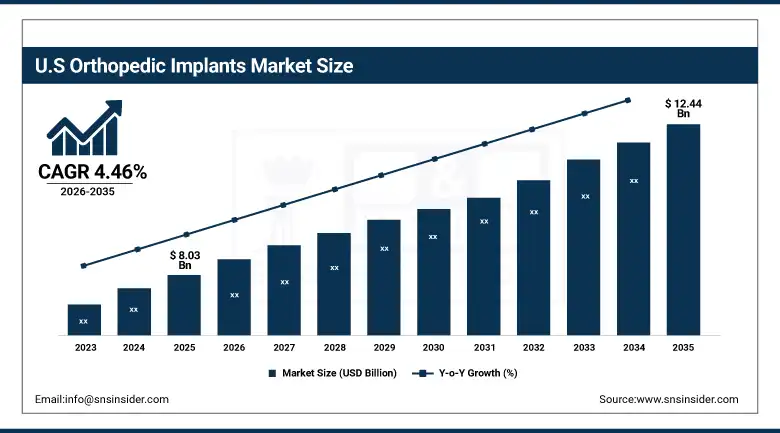

U.S. Orthopedic Implants Market Outlook

The U.S. Orthopedic Implants Market was valued at approximately USD 8.03 Billion in 2025 and is expected to reach approximately USD 12.44 Billion by 2035, growing at a CAGR of approximately 4.46%.

The United States is the world’s largest orthopedic implants market, anchored by the highest per-capita procedure rate of any national healthcare system, the most commercially advanced surgical robotics adoption, and the headquarters concentration of the global orthopedic implant industry’s leading companies. Zimmer Biomet, Stryker, Johnson & Johnson MedTech, Smith+Nephew, and Wright Medical collectively generate the majority of U.S. orthopedic implant revenue through established surgeon relationship networks and hospital system procurement contracts whose multi-year terms create commercially predictable revenue streams.

In March 2025, DePuy Synthes expanded its spine portfolio at AAOS 2025, introducing advanced implants and data-driven surgical technologies including improved navigation tools and digital surgical planning capabilities that reinforce its digital orthopaedics strategy. The launch demonstrates the commercial evolution of orthopedic implant strategy toward integrated technology ecosystems where implant product and digital surgical workflow are specified and purchased together as a comprehensive procedure solution whose bundled value proposition is more commercially compelling than individual component purchasing.

Orthopedic Implants Market Segment Analysis

-

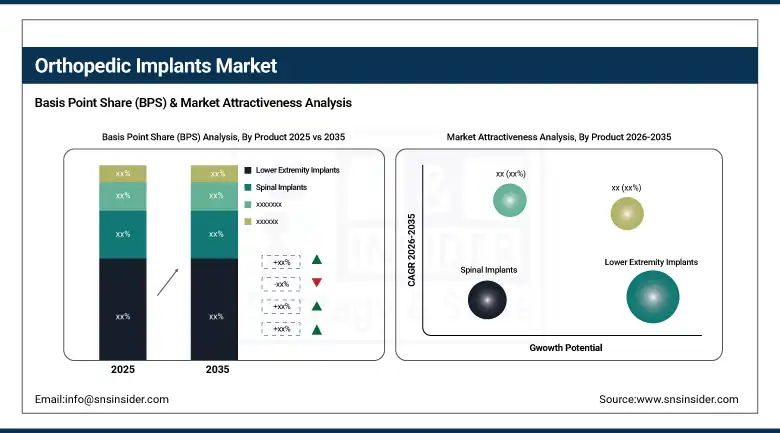

By Product, the Lower Extremity Implants segment dominated the Orthopedic Implants Market with 51.15% share in 2025, while the Dental Implants segment is the fastest growing with a CAGR of 6.98%.

-

By Material, the Metallic Material segment dominated the Orthopedic Implants Market with 47.36% share in 2025, while the Polymeric Biomaterials segment is the fastest growing with a CAGR of 7.24%.

-

By Distribution Channel, the Offline segment dominated the Orthopedic Implants Market with 83.64% share in 2025, while the Online segment is the fastest growing.

-

By End Use, the Hospitals segment dominated the Orthopedic Implants Market in 2025, while the Outpatient Facilities segment is the fastest growing.

By Product, lower extremity implants dominate, dental grows fastest

Lower extremity implants retained the dominant product position with 51.15% of the orthopedic implants market in 2025. Knee and hip replacement procedures represent the highest-volume surgical categories in elective orthopaedics globally, whose clinical demand is driven by the extraordinary prevalence of osteoarthritis in populations over 60 whose joint cartilage degeneration creates pain and functional impairment that surgical implant replacement resolves with documented effectiveness. The United States alone performs approximately 800,000 total knee replacements and 400,000 total hip replacements annually, and these volumes are growing with demographic ageing and the progressive extension of procedure eligibility toward younger patients whose body mass index and activity level profiles were previously considered elevated risk factors that limited clinical indication.

Dental implants are the fastest-growing product segment at a CAGR of 6.98% because the convergence of rising oral health awareness, expanding cosmetic dentistry investment, and the growing consumer understanding of dental implants’ superior long-term outcomes relative to dentures and bridges is creating above-average procedure volume growth across both developed and emerging dental markets.

By Material, metallic dominates, polymeric grows fastest

Metallic materials retained the dominant material position with 47.36% of the orthopedic implants market in 2025. The commercial primacy of metallic implants, primarily titanium alloys, cobalt-chromium alloys, and stainless steel, reflects their unmatched combination of mechanical strength, fatigue resistance, biocompatibility, and processability for the load-bearing structural implant applications that joint replacement, fracture fixation, and spinal instrumentation represent. Titanium’s osseointegration properties, whose surface chemistry promotes direct bone attachment without fibrous tissue interposition, are particularly clinically significant for cementless implant fixation whose long-term stability outcomes are superior to cemented alternatives in younger, more active patients.

Polymeric biomaterials are the fastest-growing material category at a CAGR of 7.24% because the combined commercial momentum of polyether ether ketone spinal implant adoption, bioresorbable interference screw and fixation device development, and ultra-high-molecular-weight polyethylene bearing surface innovation is creating growing revenue contribution from polymer-based implant applications that were previously minor components of the orthopedic implant market’s material composition.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

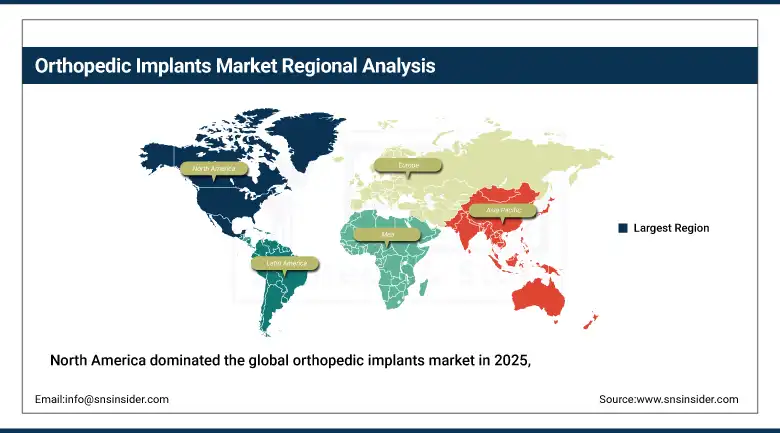

North America Orthopedic Implants Market Insights

North America dominated the global orthopedic implants market in 2025, with the United States accounting for approximately 87.4% of North American revenues. The region’s market leadership is grounded in the highest per-capita orthopedic procedure rate globally, the most advanced surgical robotics adoption whose Mako, ROSA, and Navio systems create premium implant procurement relationships, and the headquarters concentration of Zimmer Biomet, Stryker, and Johnson & Johnson MedTech whose combined market share defines the commercial landscape. CMS’s reimbursement framework for joint replacement procedures, whose ambulatory surgical centre DRG payments are progressively expanding outpatient procedure eligibility, is simultaneously creating commercial momentum for both procedure volume growth and the care pathway innovation that outpatient joint replacement requires.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s elective joint replacement programme, whose provincial health authority procurement creates consistent institutional demand that international and domestic orthopedic implant manufacturers serve through established distribution relationships.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Orthopedic Implants Market Insights

Europe is a sophisticated orthopedic implants market where EU MDR’s strengthened clinical evidence requirements for device CE marking, national health system reimbursement criteria, and the premium clinical outcome positioning of patient-specific and robotic-assisted implant systems collectively shape a procurement environment whose quality and evidence standards sustain premium product investment.

Germany accounts for approximately 22.3% of European revenues through its large hospital network, above-average orthopaedic procedure volume, and the commercial presence of Aesculap and B. Braun whose domestic market relationships sustain consistent revenue alongside international competitor procurement.

The United Kingdom, France, and Spain are significant secondary European markets where NHS and equivalent national health system joint replacement programmes, growing private orthopaedic practice investment, and the progressive EU MDR compliance of established implant manufacturers create consistent orthopedic implant procurement. ConforMIS’s May 2025 European launch of its iTotal CR-F patient-specific knee implant demonstrates the commercial momentum of personalised implant technology whose European regulatory approval creates access to a market receptive to premium clinical outcome evidence.

Asia Pacific Orthopedic Implants Market Insights

Asia Pacific is the fastest-growing regional orthopedic implants market at a CAGR of 4.43% through 2035, driven by the combination of rapidly ageing populations whose musculoskeletal disorder burden is approaching developed market prevalence levels, expanding healthcare infrastructure investment that is increasing surgical procedure capacity, and growing patient awareness of joint replacement as an effective treatment for osteoarthritis-related pain and functional impairment.

China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary combination of a large and rapidly ageing population and the government’s progressive expansion of joint replacement procedure reimbursement coverage under the national health insurance programme.

India and South Korea represent commercially significant secondary markets within Asia Pacific. India’s rapidly expanding private hospital sector investment and growing middle class’s willingness to invest in joint replacement procedures create above-average commercial growth momentum. MicroPort’s June 2025 launch of the Evolution Knee System for Asian markets reflects the commercial investment that orthopedic implant manufacturers are making to develop products specifically optimised for Asian patient anatomy and surgical practice preferences.

MEA & Latin America Orthopedic Implants Market Insights

The Middle East and Africa and Latin America are growing orthopedic implants markets where expanding hospital infrastructure, growing medical tourism, and rising musculoskeletal disease burden are creating structured demand for implant procedures.

Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its Vision 2030 healthcare infrastructure investment, the NCCI’s joint replacement procedure reimbursement programme, and the medical tourism sector’s attraction of international patients to Saudi healthcare facilities whose implant specification mirrors international premium standards.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large hospital network, the SUS public health system’s joint replacement programme, and the growing private health insurance sector whose orthopaedic procedure coverage creates dual-channel commercial demand from both public and private healthcare settings.

Market Dynamics

Growth Drivers: Ageing population demographics increasing musculoskeletal disorder procedure volume and emerging market healthcare infrastructure expansion creating new procedure capacity

Demographic ageing is the orthopedic implants market’s most structurally certain and commercially reliable growth driver. The global population over 65 is projected to reach 1.5 billion by 2050, creating a continuously expanding pool of patients at elevated risk for the osteoarthritis, osteoporosis, and degenerative joint disease whose clinical management through implant procedures represents the market’s commercial foundation. This demographic driver is structurally certain and independent of economic cycle variation in a way that elective consumer spending markets are not, as musculoskeletal pain and functional impairment create clinical need whose treatment motivation persists through economic variability.

Robotic-assisted surgery adoption is simultaneously creating a technology upgrade cycle that elevates the per-procedure implant specification and commercial value by creating premium surgeon preference for robotic-compatible implant systems whose design is optimised for robotic placement accuracy. Stryker’s MAKO, Zimmer Biomet’s ROSA, and Smith+Nephew’s Navio platforms each create long-term commercial relationships with adopting hospitals and surgeons whose commitment to platform-specific implant catalogues sustains exclusive implant procurement that generic competitive bidding cannot displace once the surgical programme is established.

Restraints: High implant cost limiting access in price-sensitive healthcare systems, and regulatory pathway complexity for new biomaterial approval

The high cost of premium orthopedic implants creates access limitations in public healthcare systems whose reimbursement frameworks set procedure prices below the commercial cost of the most advanced implant technologies, creating procurement pressure toward lowest-cost compliant implant alternatives that limits premium product penetration in cost-constrained healthcare environments. This cost pressure is most commercially significant in European national health systems and developing market public hospitals whose combined orthopedic procedure volume is substantial but whose average implant selling price is materially below the premium achieved in U.S. and private-pay markets.

Implant revision surgery requirements create clinical outcome uncertainty that influences surgeon and patient decision-making around primary procedure timing. Primary total knee replacement implants have documented 15-year survivorship rates of approximately 90%, but the 10% of patients who require revision surgery face substantially more complex and costly procedures whose outcome uncertainty creates hesitation in younger patient populations whose longer life expectancy creates greater revision exposure over their lifetime.

Opportunities: Patient-specific implant commercial scaling through 3D printing cost reduction and outpatient joint replacement procedure pathway development

Patient-specific orthopedic implants represent the most commercially differentiated product development direction in the orthopedic implant market whose 3D printing manufacturing technology is progressively reducing the cost premium over standard catalogue implants. As patient-specific implant manufacturing cost approaches the level where premium pricing reflects clinical outcome improvement value rather than manufacturing cost subsidy, the addressable market expands from complex revision and unusual anatomy cases toward the mainstream primary joint replacement market whose volume scale creates transformational commercial opportunity for manufacturers who achieve cost-competitive personalised implant delivery.

Outpatient joint replacement procedure development is creating the most commercially significant care pathway evolution in the orthopedic implants market, as the progressive qualification of total knee and hip replacement for ambulatory surgical centre performance creates access to a new institutional procurement channel whose combined volume is growing rapidly with CMS reimbursement framework evolution and clinical pathway validation. Outpatient joint replacement facilities’ implant procurement concentrates volume in fewer implant system families whose per-system volume efficiency sustains competitive pricing relationships that different procurement dynamics than the hospital market creates.

Recent Developments:

-

2025: ConforMIS launched its iTotal CR-F patient-specific knee implant in Europe in May 2025, featuring enhanced personalised fit and improved surgical instrumentation for the European market, expanding the company’s footprint in patient-specific joint replacement solutions and reflecting growing European clinical acceptance of personalised implants as a premium standard-of-care option.

-

2025: DePuy Synthes expanded its spine portfolio at AAOS 2025 in March 2025, introducing advanced spinal implants and data-driven surgical technologies including improved navigation tools and digital surgical planning capabilities that reinforce its digital orthopaedics strategy across spinal fusion and minimally invasive procedures.

-

2025: MicroPort introduced the Evolution Knee System in June 2025, targeting Asian markets with advanced knee replacement implants featuring improved alignment guides and enhanced durability specifications, demonstrating the commercial investment that major orthopedic implant manufacturers are making in Asia-specific product development that addresses regional patient anatomy and surgical practice characteristics.

Orthopedic Implants Market Key Players

-

Zimmer Biomet Holdings

-

Stryker Corporation

-

Johnson & Johnson MedTech

-

Smith+Nephew

-

Medtronic

-

Wright Medical Group

-

NuVasive

-

Arthrex

-

DJO Global

-

CONMED Corporation

-

Integra LifeSciences

-

B. Braun SE

-

Corin Group

-

ConforMIS

-

MicroPort Scientific Corporation

Orthopedic Implants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 22.88 Billion |

| Market Size by 2035 | USD 36.45 Billion |

| CAGR | CAGR of 4.78% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Lower Extremity Implants, Spinal Implants, Dental, and Upper Extremity Implants) • by Material (Metallic Material, Ceramic Biomaterials, Polymeric Biomaterials, and Others) • by Distribution Channel (Offline, and Online) • by End Use (Hospitals, and Outpatient Facilities) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Zimmer Biomet Holdings, Stryker Corporation, Johnson & Johnson MedTech, Smith+Nephew, Medtronic, Wright Medical Group, NuVasive, Arthrex, DJO Global, CONMED Corporation, Integra LifeSciences, B. Braun SE, Corin Group, ConforMIS, MicroPort Scientific Corporation |

Frequently Asked Questions

The Orthopedic Implants Market is expected to grow at a CAGR of 4.78% from 2026 to 2035.

The Orthopedic Implants Market was valued at USD 22.88 Billion in 2025.

Ageing global population demographics increasing musculoskeletal disorder prevalence and surgical procedure volume, robotic-assisted orthopedic surgery adoption elevating implant specification and clinical outcome quality, and emerging market healthcare infrastructure expansion creating growing new procedure capacity.

Lower Extremity Implants dominated the Orthopedic Implants Market with 51.15% share in 2025.

North America dominated the Orthopedic Implants Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch