Pentaerythritol Market Report Scope & Overview:

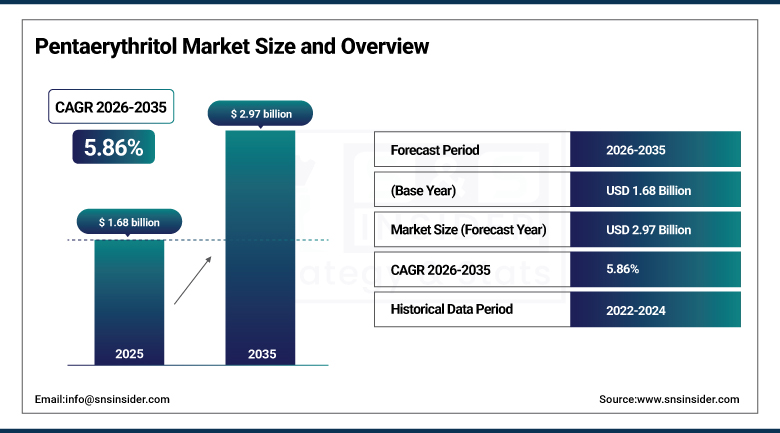

The Pentaerythritol Market was valued at USD 1.68 Billion in 2025 and is expected to reach USD 2.97 Billion by 2035, growing at a CAGR of 5.86% from 2026-2035.

The global pentaerythritol market is on an upward trend, which is facilitated by its crucial position as a multi-purpose polyol intermediate used in various industries such as alkyd resins for paints and coatings, radiation curable acrylates, rosin esters for adhesive and ink applications, synthetic lubricants in aviation and industrial uses, intumescent flame retardants, and pentaerythritol tetranitrate (PETN) for explosives and detonators. Pentaerythritol is manufactured using the condensation of formaldehyde and acetaldehyde in the presence of a basic catalyst, and there are only a few large scale chemical manufacturers globally from China, Europe, and the United States.

The global pentaerythritol market is driven by the revival of global construction activities, which is leading to higher alkyd resin demand the use of radiation curing in coating and inks to reduce volatile organic compounds and the increased use of synthetic lubricants in automotive and aerospace applications due to inadequate performance of petrochemical lubricants in extreme pressure and temperature conditions.

In 2024, Perstorp Group announced the expansion of its pentaerythritol production capacity at its Stenungsund facility in Sweden by approximately 30,000 metric tons per year, increasing the site's total annual capacity to over 100,000 metric tons.

Market Size and Forecast

-

Market Size in 2026E: USD 1.77 Billion

-

Market Size by 2035: USD 2.97 Billion

-

CAGR: 5.86% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Pentaerythritol Market - Request Free Sample Report

Pentaerythritol Market Trends

-

Growing adoption of UV-curable coatings and inks is increasing demand for pentaerythritol-based acrylates.

-

Rising fire safety regulations are driving the use of pentaerythritol in intumescent flame retardant formulations.

-

Expanding demand for high-performance synthetic lubricants is boosting consumption of pentaerythritol esters.

-

Capacity expansions in China are intensifying global price competition and market supply.

-

Increasing focus on sustainability is encouraging development of bio-based pentaerythritol production technologies.

U.S. Pentaerythritol Market Outlook

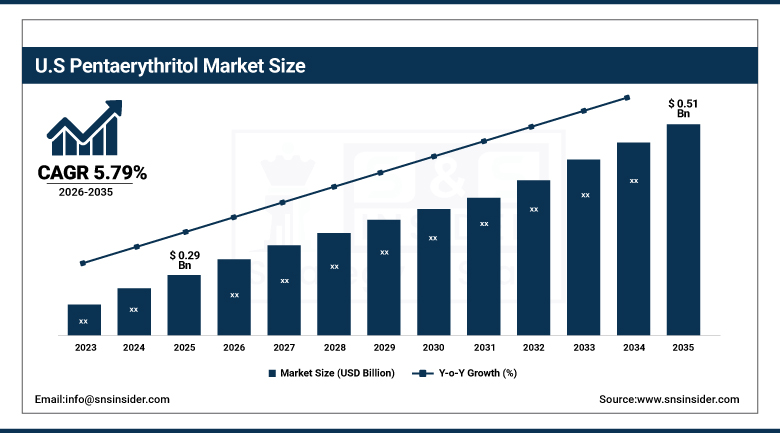

The U.S. Pentaerythritol Market was valued at approximately USD 0.29 Billion in 2025 and is expected to reach approximately USD 0.51 Billion by 2035, growing at a CAGR of approximately 5.79%.

The U.S. is the largest pentaerythritol market among non-Asian single countries, thanks to the existence of a large paints and coatings market, which uses the alkyd resins that require the use of pentaerythritol as a polyol component; a domestic synthetic lubricants market, which uses the aviation and industrial applications of pentaerythritol ester base stock due to its performance properties; and a commercial explosives market, which uses pentaerythritol in the form of PETN in its mining, quarrying, and construction applications. The U.S. market is sourced through domestic production from Perstorp and LCY Chemical U.S. plants and import from Europe and China, with an emphasis on domestic production due to the sensitivity of supply due to national defense and security issues.

Momentive Performance Materials expanded its U.S. pentaerythritol ester lubricant base stock production in 2024, responding to growing demand from commercial aviation operators transitioning to synthetic lubricants meeting the latest OEM specifications for fuel-efficient high-bypass turbofan engines.

Pentaerythritol Market Segment Analysis

-

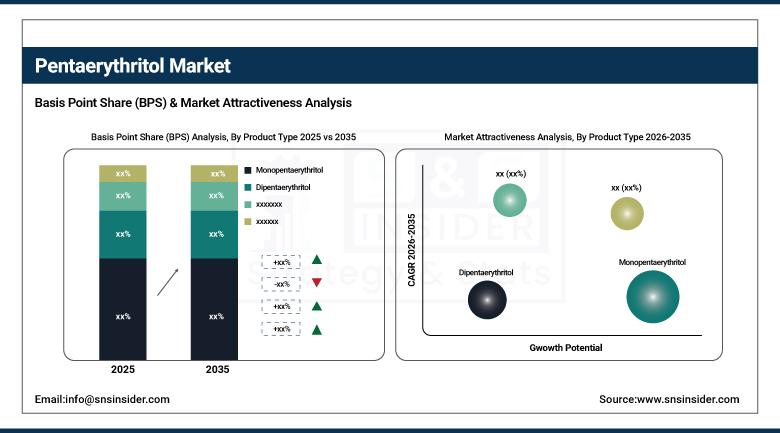

By Product Type, the Monopentaerythritol segment dominated the pentaerythritol market with 72.3% share in 2025, and lubricant ester applications whose combined volume substantially exceeds specialty dipentaerythritol applications.

-

By Application, the Alkyd Resins & Paints segment dominated the pentaerythritol market with 38.6% share in 2025, while the Radiation Curing segment is the fastest growing as UV and electron beam curing technology adoption replaces solvent-borne coating.

-

By End-Use Industry, the Paints & Coatings segment dominated the pentaerythritol market with 41.2% share in 2025, and industrial maintenance coating requirements whose alkyd resin content creates consistent pentaerythritol procurement at above-average volume per customer.

By Product Type, monopentaerythritol dominates, dipentaerythritol serves specialty applications

The leading product type remained the monopentaerythritol with a share of 72.3% in the pentaerythritol market in 2025. The dominance of monopentaerythritol is determined by the fact that it is a universal intermediate polyol, being used in all high-volume application segments on account of its four hydroxyl groups, which are needed for esterification reaction to synthesize alkyd resins, acrylates, rosin esters, and lubricant esters. The commercial availability of high purity grades for producing radiation curable acrylates and technical grades for alkyd resins and lubricants creates an advantage for monopentaerythritol that maintains its leading position.

The dipentaerythritol finds its use in specialized applications such as high-performance lubricant esters for military and aviation purposes due to their extraordinary thermal stability and high resistance to oxidation, special acrylates for UV-curable optical coatings, and flame-retardant applications, where its higher functionality provides better char formation at elevated temperatures. All these applications have above average cost per kilogram and low volume, thus creating a commercially relevant premium segment.

By Application, alkyd resins & paints dominate, radiation curing grows fastest

Alkyd Resins & Paints continued to maintain its dominance in terms of application with 38.6% share of market in 2025. Alkyd resins continue to remain the most commercially significant type of synthetic resins for maintenance and architectural coatings in developing economies and applications where alkyd chemistry's performance in terms of resistance, binding power, flexibility and cost-efficiency is not matched by any other resin system available in the market. High volume demand created in the paints and coatings industry owing to consumption of pentaerythritol in preparation of alkyds helps sustain its dominant position in spite of slow erosion of market share by competing waterborne and radiation curing systems.

Radiation Curing was the fastest growing application owing to replacement of solvent-based coating formulations with UV and EB curable coating formulations due to rising cost of energy and increasing compliance requirement arising out of tightening of VOC regulations. Every tightening of the regulations related to emission of volatile organic compounds in EU, China and the US creates an opportunity for replacing the existing solvent borne alkyd coatings with more environment friendly radiation curing formulations which contain pentaerythritol acrylate monomers and therefore add to the value of pentaerythritol.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.4% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

46.8% |

|

Middle East & Africa |

Saudi Arabia |

33.2% |

|

Latin America |

Brazil |

44.5% |

North America Pentaerythritol Market Insights

North America is one of the important markets for pentaerythritol wherein the U.S. is responsible for roughly 79.4% of regional revenue. This market is supported by the country’s large paints and coatings industry, synthetic lubricant use in aviation and automotive sectors, demand for commercial explosives in mining and construction, and flame retardant demand in building materials due to tightening of fire codes. Local manufacturing capacity ensures supply security of the product in strategic uses whereas price pressures brought about by competitive imports from China forces local producers to invest in productivity enhancements.

Canada and Mexico provide roughly 20.6% of regional revenues by construction activities-driven demand for paints and coatings, rising automotive output leading to demand for synthetic lubricants, and mining operations in both countries resulting in commercial explosives demand with PETN composition leading to pentaerythritol usage.

Europe Pentaerythritol Market Insights

Europe represents an important strategic market due to strong local production capabilities of Perstorp (Sweden), European operations of LCY Chemical, and other regional manufacturers which generate supply self-sufficiency for almost all end uses while industrial emissions regulations of the EU increase above average demand growth for radiation curing coatings that substitute solvent-based products. Germany represents the largest European market for pentaerythritol accounting for about 24.6% of total revenues thanks to alkyd resins production of its chemical industry, automotive OEM coatings purchases, and specialty lubricants manufacturing which consumes synthetic ester base stock resulting in high per unit of product demand.

Netherlands, France, Sweden, and the UK are important secondary markets where chemical production, printing and packaging, and specialty coatings manufacturing generate steady demand for pentaerythritol and combine with the progressive regulatory environment of the region which promotes low-VOC coating systems and their radiation curing formulations.

Asia Pacific Pentaerythritol Market Insights

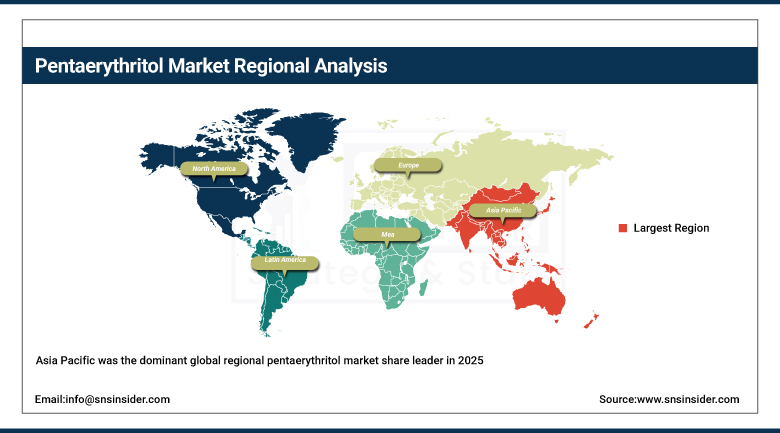

Asia Pacific was the dominant global regional pentaerythritol market share leader in 2025 and is the fastest growing due to the fact that China was the largest pentaerythritol producer and consumer in the world coupled with the fast-growing industries of India and Southeast Asia driving above-average growth rates in the paints, coatings, and construction markets. China comprises approximately 46.8% of the total Asia Pacific revenue through its large paints and coatings domestic market, explosives usage in mining and infrastructure construction and export-oriented chemical manufacturing which uses high amounts of pentaerythritol in the esters and acrylates it produces.

India is a strong growth secondary regional market due to the fast-growing infrastructure construction and automotive production industries and paints and coatings industry capacity additions which drive above-average demand growth. Japan and South Korea were sources of above-average value per kg of pentaerythritol due to the special lubricant, electronics, and high performance coating applications which require technical grade pentaerythritol.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Pentaerythritol Market Insights

Saudi Arabia is the top revenue generator in MEA at 33.2% by virtue of its Vision 2030 infrastructure construction project which develops paints and coatings demand, the increasing petrochemicals industry where synthetic lubricants' usage results in pentathritol esters' purchasing, and the mining activities in MEA generating commercial explosives demand. The mining activities in South Africa and construction activities in UAE are among the key secondary revenue sources for the MEA pentathritol market.

Brazilian paints and coatings market, the Amazon and Minas Gerais mining operations developing commercial explosives demand, and the increasing automotive manufacturing which generates alkyd resins demand through coating processes are responsible for Brazil being the leading revenue generator in Latin America at 44.5%. Mexico and Colombia are some of the key secondary markets for Latin American market growth.

Market Dynamics

Growth Drivers: Global construction activity recovery driving alkyd resin demand and radiation-curing adoption displacing solvent-borne coating systems

Pentaerythritol market recovery through global construction activities is the key commercial demand driver since architectural and protective coatings used for residential, commercial and infrastructural construction use alkyd resins made from pentaerythritol and their volume is directly correlated with construction production volumes. The forecast of infrastructure investments increase in Asia, Africa and Latin America by World Bank and recovery of housing construction in developed countries results in multiyear demand growth trend for pentaerythritol whose paints and coatings application dominates pentaerythritol consumption in all major regional markets.

Adoption of radiation-cured technology leads to above average pentaerythritol demand growth in developed countries where volatile organic compounds (VOC) emission regulations become stricter, as pentaerythritol triacrylate and tetraacrylate based UV and EB curable systems replace solvent borne alkyd and acrylic systems. Each percentage point of coating and ink volume shifted from solvent-borne coating and ink system to radiation curable coating and ink increases pentaerythritol acrylate consumption which has above average price per kilogram compared to volume displaced cheaper alkyd systems.

Restraints: Raw material price volatility in formaldehyde and acetaldehyde and environmental concerns over formaldehyde in pentaerythritol production

Price fluctuations of raw materials of formaldehyde and acetaldehyde make it difficult for manufacturers of pentaerythritol due to increased cost instabilities whose level depends on the extent to which it influences the profit margins of the manufacturers in an industry environment whereby the pricing pressures of cheaper Chinese competition inhibit the timely passing of higher feedstock costs to the consumers. Every increase in natural gas prices and hence the cost of producing methanol and formaldehyde leads to margin squeezes among manufacturers of pentaerythritol due to the increased cost instabilities related to natural gas and petroleum markets.

Environmental worries about formaldehyde emissions during the manufacturing process and the usage of formaldehyde resins by end users lead to more investment into compliance by manufacturers while driving others to look for other alternatives to polyols because of the risk involved with formaldehyde emissions.

Opportunities: Bio-based pentaerythritol development and synthetic lubricant demand growth in high-performance applications

Development of bio-pentaerythritol is an important strategic opportunity in the long term with the ability to achieve commercial scale-ups in a cost-effective way allowing it to benefit from the high premium prices offered by the coating and adhesive formulators with sustainable policies mandating proof of bio-content in their formulations. Every bio-polyol with equivalent performance of petro-chemical pentaerythritol and carbon reduction capability adds high commercial value as there are high premium prices offered to environmentally differentiated products in European and North American markets.

Demand growth in synthetic lubricants in high performance automotive, aviation and industrial applications provides a commercially viable growth opportunity for pentaerythritol due to the special performance properties of its esters providing premium prices beyond commodity alkyd applications. Every introduction of new turbofan engine program, hybrid vehicle transmission design and industrial gearbox system adopting pentaerythritol based ester lubricants due to their energy efficient properties will generate repeat purchase with long application life cycle.

Recent Developments:

-

2024: Perstorp Group announced the expansion of its pentaerythritol production capacity at its Stenungsund, Sweden facility by approximately 30,000 metric tons per year, increasing total site capacity to over 100,000 metric tons to serve growing European alkyd resin and radiation-curing acrylate demand.

-

2024: Momentive Performance Materials expanded its U.S. pentaerythritol ester lubricant base stock production capacity to serve growing commercial aviation demand for synthetic lubricants meeting the latest OEM specifications for high-bypass turbofan engines.

-

2024: Celanese Corporation announced the development of a bio-based pentaerythritol pathway using fermentation technology, targeting commercialization by 2027 to serve European coating and adhesive formulators with sustainability-driven bio-based polyol requirements.

Pentaerythritol Market Key Players

-

Perstorp Group

-

Celanese Corporation

-

Evonik Industries AG

-

LCY Chemical Corporation

-

Mitsui Chemicals, Inc.

-

Univar Solutions Inc.

-

Merck KGaA

-

BASF SE

-

Kanoria Chemicals & Industries Ltd.

-

Jiangsu Kaimei Chemical Co., Ltd.

-

Baoding Guoxiu Chemical Co., Ltd.

-

Henan Pengda Chemical Co., Ltd.

-

Hubei Yihua Chemical Industry Co., Ltd.

-

Shandong Dongda Chemical Group Co., Ltd.

-

Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC)

-

Leuna-Harze GmbH

-

Vangaveti Enterprises Pvt. Ltd.

-

Koei Chemical Co., Ltd.

-

TCI Chemicals (India) Pvt. Ltd.

-

Otto Chemie Pvt. Ltd.

Pentaerythritol Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.68 Billion |

| Market Size by 2035 | USD 2.97 Billion |

| CAGR | CAGR of 5.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Monopentaerythritol, Dipentaerythritol, Technical Grade Pentaerythritol, Others) • By Application (Alkyd Resins & Paints, Radiation Curing, Rosin Esters, Lubricants, Explosives, Flame Retardants, Plasticizers, Others) • By End-Use Industry (Paints & Coatings, Adhesives & Sealants, Construction, Automotive, Aerospace & Defense, Electrical & Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Perstorp Group; Celanese Corporation; Evonik Industries AG; LCY Chemical Corporation; Mitsui Chemicals, Inc.; Univar Solutions Inc.; Merck KGaA; BASF SE; Kanoria Chemicals & Industries Ltd.; Jiangsu Kaimei Chemical Co., Ltd.; Baoding Guoxiu Chemical Co., Ltd.; Henan Pengda Chemical Co., Ltd.; Hubei Yihua Chemical Industry Co., Ltd.; Shandong Dongda Chemical Group Co., Ltd.; Gujarat Narmada Valley Fertilizers & Chemicals Ltd. (GNFC); Leuna-Harze GmbH; Vangaveti Enterprises Pvt. Ltd.; Koei Chemical Co., Ltd.; TCI Chemicals (India) Pvt. Ltd.; Otto Chemie Pvt. Ltd. |

Frequently Asked Questions

The Paints & Coatings segment dominated the Market with 41.2% share in 2025, driven by global construction activity recovery and architectural coatings demand growth in emerging markets.

The Alkyd Resins & Paints segment dominated the Market with 38.6% share in 2025, while Radiation Curing is the fastest growing segment driven by VOC regulation tightening and UV curing technology adoption.

The Pentaerythritol Market was valued at USD 1.68 Billion in 2025.

Global construction activity recovery driving alkyd resin and paints & coatings demand, and accelerating adoption of radiation-curable coating and ink formulations replacing solvent-borne systems in response to tightening VOC emission regulations in Europe, North America, and China.

Monopentaerythritol dominated the Pentaerythritol Market with 72.3% share in 2025, driven by its position as the universal polyol intermediate across alkyd resins, acrylates, rosin esters, and lubricant ester applications.

Asia Pacific dominated the global Market in 2025, with China accounting for approximately 46.8% of regional revenues through its position as the world's largest pentaerythritol producer and consumer across paints, explosives, and chemical manufacturing applications.

The Pentaerythritol Market is expected to grow at a CAGR of 5.86% from 2026 to 2035.

Get in Touch