Polyethylene Terephthalate Films Market Report Scope & Overview:

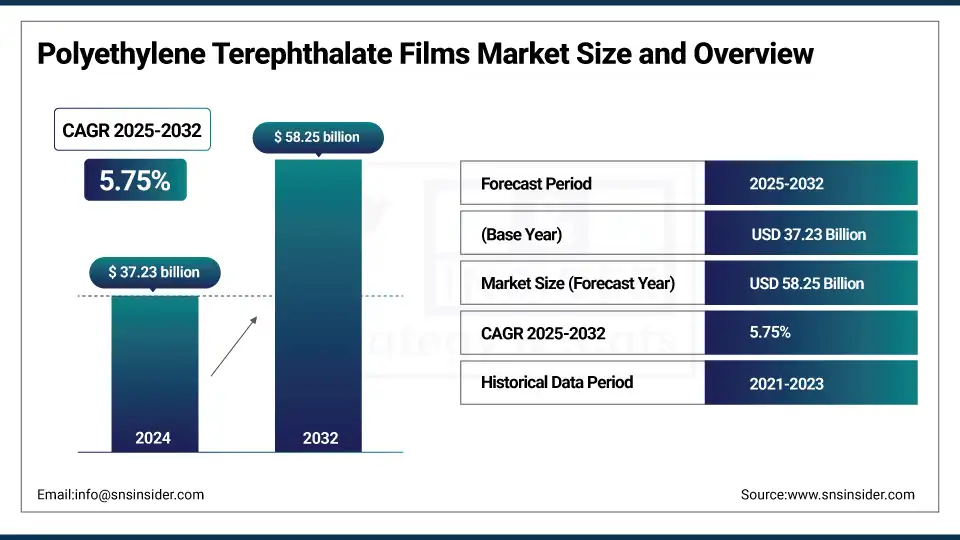

The Polyethylene Terephthalate Films Market Size was valued at USD 37.23 billion in 2024 and is expected to reach USD 58.25 billion by 2032, growing at a CAGR of 5.75% over the forecast period of 2025-2032.

Polyethylene terephthalate films market analysis shows the expansion in Electrical & Electronics due to its excellent electrical insulation, high tensile strength, and ability to resist heat and chemicals. The primary applications of these films include capacitors, flexible printed circuits, cable insulations, and display panels. As consumer electronics, renewable energy systems, and electric vehicles continue to advance by leaps and bounds, the need for higher-performance insulating and protective materials also increases. In addition, the increasing use of miniaturized and lightweight electronic components is also leading to the development of PET films as they offer robustness, resilience, and stability in the face of changing operating environments. Producers are likely to experience huge demand in the upcoming years due to this trend, which drives the polyethylene terephthalate films market growth.

To Get more information On Polyethylene Terephthalate Films Market - Request Free Sample Report

Meanwhile, the U.S. Bureau of Labor Statistics data shows the Producer Price Index for plastics packaging film and sheet manufacturing surged to 280.275 in June 2025, recording strengthened demand and pricing-power characteristics concerning industrial and electronic applications.

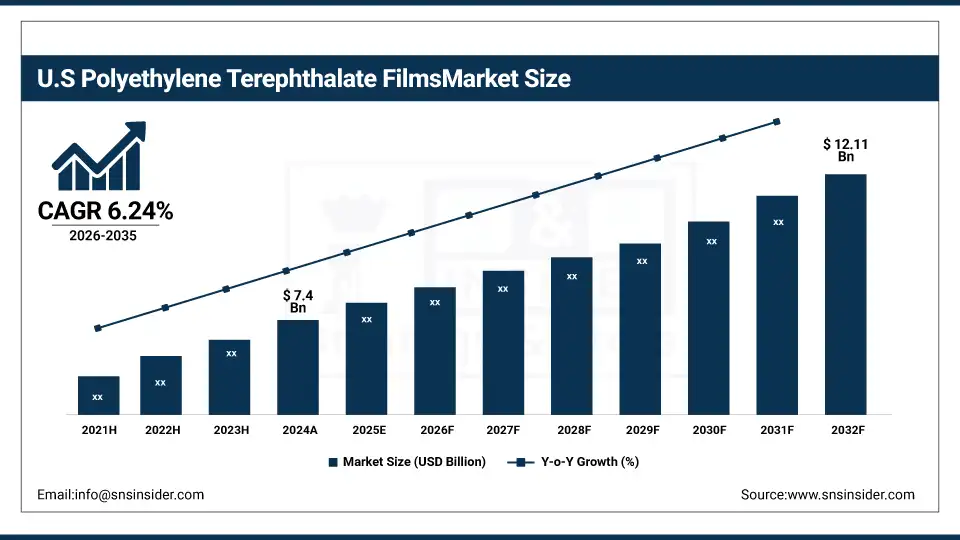

The U.S. Polyethylene Terephthalate Films market size was USD 7.4 billion in 2024 and is expected to reach USD 12.11 billion by 2032, growing at a CAGR of 6.24% over the forecast period of 2025-2032. The increased usage of packaged food and strong demand for flexible packaging vehicles from industries over there, and technological breakthroughs have been taking place in specialty PET films. Whether it be domestic output or warehouse advancements, there have also been some federal launches to encourage the manufacturing of goods in the U.S.

Market Dynamics:

Key Drivers:

-

Expanding Flexible Packaging Applications Drive the Market Growth

As PET films are very good at barrier, transparency, and recyclability properties, they are essential materials in food, beverage, and pharmaceutical packaging. According to the U.S. Flexible Packaging Association, flexible packaging expanded by 4% in 2023 on account of growing e-commerce and sustainable material needs. The direct beneficiary of this growth is PET film manufacturers, who are coming up with lightweight and recyclable solutions for packaging.

In 2023, Uflex Ltd., Mumbai, invested in a new PET film production line in Kentucky to provide packaging customers located in North America.

Restraints:

-

Fluctuating Raw Material Prices, Which May Hamper the Market Growth

PET films are highly dependent on the use of PTA (Purified Terephthalic Acid) and MEG (Glycol derived from crude oil). The fluctuation in global crude prices affects the PET film production cost, which is projected to limit the profit of PET Film Manufacturers. Crude oil in 2024 maintained an average price band between USD 70 – USD 90 per barrel according to the U.S. Energy Information Administration (EIA) data and created cost pressures for the downstream PET film producers.

Opportunities:

-

Technological Advancements in Specialty PET Films Create an Opportunity for the Market Growth

The specialty PET film market is predicted to experience increasing demand from the burgeoning applications in areas, such as solar panels, medical devices, and high-performance industrial coatings. Due to the improvements in coatings, metallization, and holography, PET films are also finding more specialized industrial applications. A total of USD 45 million in DOE funding will launch all programs in 2024, and this includes high-performance PET-based films for photovoltaic module advanced materials research

Mitsubishi Polyester Film opened an expanded South Carolina plant to make high-end PET films used in solar and medical, which drives the Polyethylene Terephthalate Films market trends.

Segment Analysis:

By Product Type

Biaxially Oriented PET (BoPET) films will continue to account for the major polyester film market share in 2024 with about 54.5%. This growth is driven by their high tensile strength, optical clarity, and dimensional stability, making them irreplaceable in a wide variety of applications, such as flexible packaging, imaging, and electrical insulation. Packagers find BoPET very attractive in an age, where the consumer needs product integrity while benefiting from a cool visual.

Metallized PET Films coated with a thin layer of metal, such as aluminum, are proving to be the fastest-growing. They are widely used for food packaging, coffee pouches, and specialty labels as they offer PET flexibility but with better moisture, oxygen, and light barrier properties.

By Thickness

The PET film market is led by films with a thickness of less than 50 microns, as these are extensively used in the packaging (especially FMCG), labeling, and lamination industries. It has a low profile, which is ideal for minimizing the costs of materials and allows faster production at high speeds, as the required mechanical strength would not be compromised.

The 50–100-micron thickness category held a significant market share. These films offer a combination of durability, flexibility, and protection properties, making them more predominantly used in the solar panel back sheets, electrical insulation layers, and automotive window tinting.

By Application

Packaging is the largest application area for PET films, accounting for more than 38% of the bio-PET film market in 2023. This is predominantly driven by the increasing global demand for eco-friendly packaging solutions, such as those recycled materials, and clear packaging options, especially within the food and beverage industry and pharmaceutical sector.

The rate of growth in electrical and electronics is skyrocketing on the backs of the growing prevalence of PET films for capacitor insulation purposes, flexible printed circuitry elements, and display protection. With dielectric strength, thermal stability, and mechanical robustness, the material is an excellent candidate for many next-generation devices in the electric vehicle and wearable electronics markets.

By End-Use Industry

The food & beverages sector is the largest consumer of PET film, representing close to 39% use of polyester film in 2023. This industry appreciates the PET films because they comply with food safety, allow light-weighting, and endow a strong barrier that preserves flavors, aromas, and nutrients. As eco-friendly and mono-material pack designs are gaining momentum, PET is also being validated as a sustainable option.

The electrical and electronics industry is growing at the fastest rate in terms of market share. Continuous electrification of transportation and commodities, the further miniaturization of consumer electronics, and the emergence of flexible displays alike require PET films for insulation, lamination, or optical functions.

Regional Analysis:

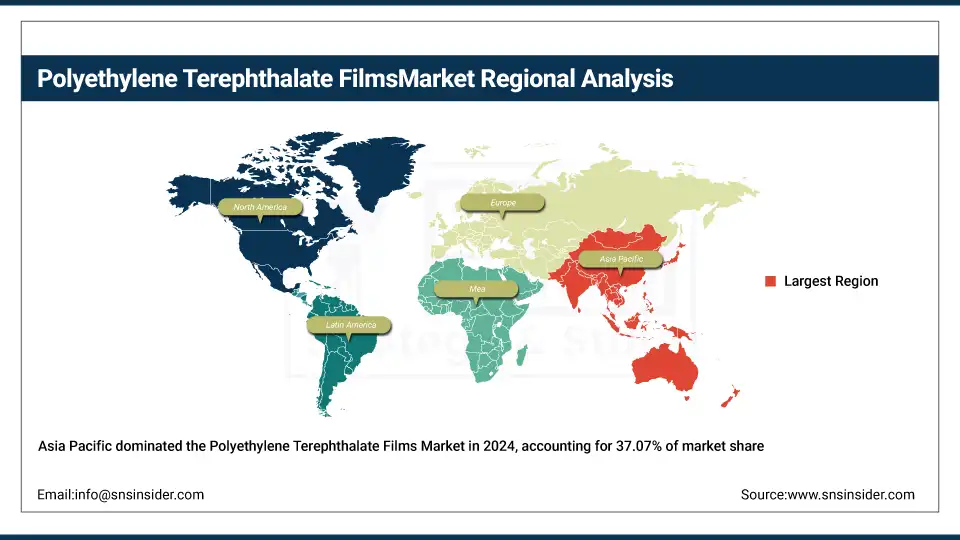

Asia Pacific held the largest Polyethylene Terephthalate Films Market Share in 2024, around 37.07% 2024. The high demand from the packaging, electronics, and automotive industries has resulted in Asia Pacific emerging as the largest PET films market, mainly due to the region being a low production cost centre characterized by huge volume manufacturing capacity. The SCAs are supported by the strong supply chain, growing population density regions, such as China and India offering high consumption, and governmental policies toward recyclable packaging. India UFlex Ltd to enhance capacities at its Gujarat-based PET Film Plant till 2024 to meet growing domestic and global demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North America region is the fastest-growing market. The market is owing to the development in packaging technology, increased demand for sustainable materials, and high usage in the electronics and healthcare sectors. In the U.S. and Canada, transparent PET film is actually encouraged to be used in sustainable applications due to the sophisticated recycling systems that are established in both countries. Toray Plastics (America), Inc. will invest in upgrading its Rhode Island PET film production line aimed at improving the efficiency and capacity for high-performance packaging films that are manufactured using state-of-the-art technologies.

Europe maintains a significant share of the Polyethylene Terephthalate Films market. It is due to stringent EU laws over environmental sustainability of packaging, alongside increased electronics production and continued innovation around lighter automotive materials. These grades are popular among countries, such as Germany, France and Italy, which have high usage of good quality, recyclable PET films Klöckner Pentaplast has expanded its PET film recycling operations in Spain, where it will focus on meeting the goals of the European Union Circular Economy and support the growing need for sustainable packaging solutions by increasing availability and reducing investment needs.

Key Players:

Major Polyethylene Terephthalate Films companies are DuPont Teijin Films, Mitsubishi Polyester Film, Toray Plastics, SKC Films, Uflex, Jindal Poly Films, Polyplex Corporation, Cosmo Films, Ester Industries, Vacmet India, SRF Limited, Terphane, Jiangsu Shuangxing Color Plastic New Materials, Zhejiang Great Southeast, Fuwei Films, Garware Hi-Tech Films, Klockner Pentaplast, Flex Films, Sichuan Dongfang Insulating Material, and Kolon Industries.

Recent Developments:

-

March 2024 – DuPont Teijin Films introduced a recyclable PET film to enhance sustainability within its product portfolio, aligning with the industry’s growing emphasis on eco-friendly material solutions.

-

April 2024 – Toray Plastics increased its production capacity in Japan to address rising demand for PET films, especially for high-performance uses in electronics and packaging sectors.

| Report Attributes | Details |

| Market Size in 2024 | USD 37.23 Billion |

| Market Size by 2032 | USD 58.25Billion |

| CAGR | CAGR of5.75% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: BoPET (Biaxially Oriented PET) Films, Metallized PET Films, Coated PET Films, Holographic PET Films, Others (e.g., matte PET, chemically treated PET) • By Thickness: Below 50 microns, 50–100 microns, Above 100 microns • By Application: Packaging, Electrical & Electronics, Imaging, Industrial, Others (labels, tapes, graphic arts) • By End-Use Industry: Food & Beverage, Pharmaceuticals, Electrical & Electronics, Automotive, Printing & Publishing, Others |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | DuPont Teijin Films, Mitsubishi Polyester Film, Toray Plastics, SKC Films, Uflex, Jindal Poly Films, Polyplex Corporation, Cosmo Films, Ester Industries, Vacmet India, SRF Limited, Terphane, Jiangsu Shuangxing Color Plastic New Materials, Zhejiang Great Southeast, Fuwei Films, Garware Hi-Tech Films, Klockner Pentaplast, Flex Films, Sichuan Dongfang Insulating Material, Kolon Industries |

Frequently Asked Questions

Ans: Major players include DuPont Teijin Films, Toray Plastics, Mitsubishi Polyester Film, SKC Inc., and Jindal Poly Films.

Ans. Asia Pacific leads the global PET films market, followed by North America and Europe, driven by strong manufacturing bases and high consumption in end-use sectors.

Ans BOPET films dominate the PET films segment, offering superior tensile strength, thermal stability, and barrier properties essential for packaging, electronics, and industrial uses.

Ans Rising adoption of sustainable and recyclable PET films, technological advancements in film coatings, and increased use in high-performance applications are key growth trends.

Ans Packaging, electronics, automotive, and solar energy industries are the primary drivers of PET films demand due to their durability, clarity, and barrier properties.

Get in Touch