Positive Airway Pressure Devices Market Report Scope & Overview:

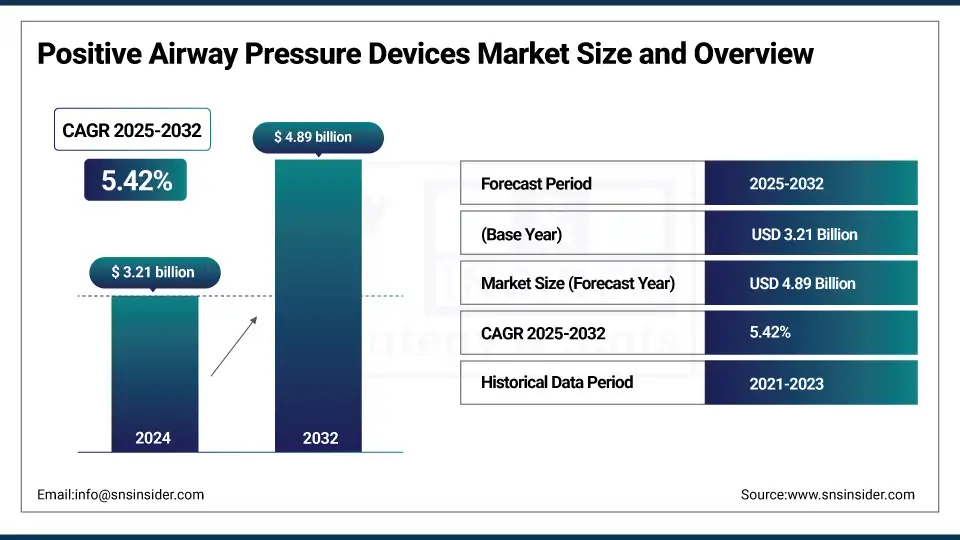

The positive airway pressure devices market size was valued at USD 3.21 billion in 2024 and is expected to reach USD 4.89 billion by 2032, growing at a CAGR of 5.42% over the forecast period of 2025-2032.

The global Positive Airway Pressure devices market is expanding since the population suffering over obstructive sleep apnea is increasing due to the lifestyle modifications, including obesity, smoking, alcohol, and sedentary living. These factors lead to airway collapse and poor sleep quality and increase the need for proper treatment. With increased awareness and better diagnostics, plus a trend toward home-based care, more patients are prescribed PAP devices, including CPAP, APAP, and BiPAP to help mitigate symptoms and improve sleep outcomes.

To Get more information On Positive Airway Pressure Devices Market - Request Free Sample Report

For instance, in February 2025, the U.S. National Sleep Foundation reported an 11% rise in sleep apnea cases linked to obesity, highlighting BMI-driven demand for PAP devices

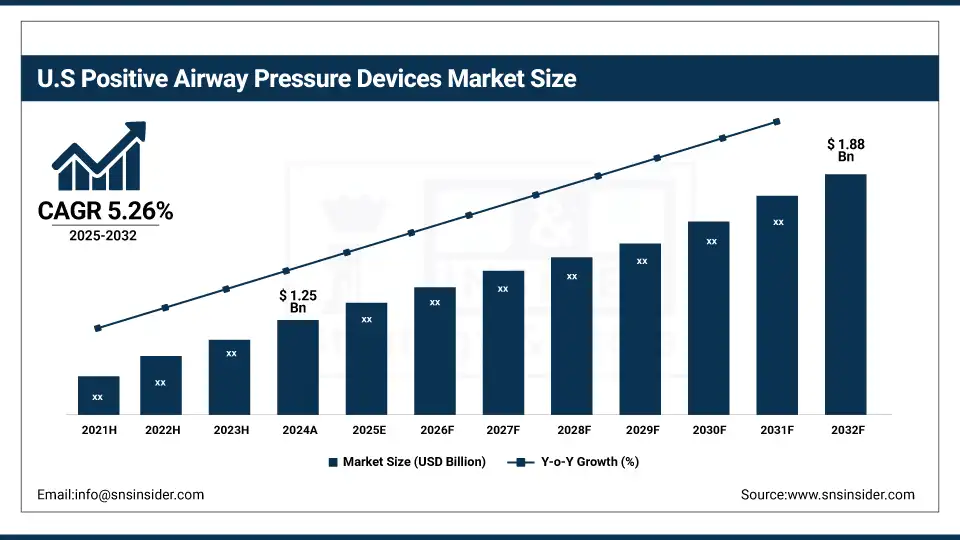

The U.S. positive airway pressure devices market was valued at USD 1.25 billion in 2024 and is expected to reach USD 1.88 billion by 2032, growing at a CAGR of 5.26% over 2025-2032.

The positive airway pressure devices market in the U.S. is largely driven by its robust healthcare infrastructure, large insurance coverage, and increasing geriatric population. Enabling policies, including Medicare aid access to PAP therapy, home-based care, and telehealth, facilitate the diagnosis and treatment of OSA. The growing need for chronic respiratory care also supplements adoption. These factors compiled lead to the country’s number one positive airway pressure devices market share.

For instance, in March 2025, CMS reported a 9.6% rise in Medicare Advantage enrollment, expanding senior access to PAP devices and reinforcing the U.S. market dominance through policy-driven adoption.

Market Dynamics:

Drivers:

-

Rising Awareness and Improved Diagnosis Drive the Positive Airway Pressure Devices Market Growth

Increasing awareness and diagnosis of sleep disorders are some of the key factors driving the positive airway pressure devices market. More public and clinical awareness of conditions, including sleep apnea has led to early identification and intervention. Improved screening devices, public health initiatives, and digital sleep tracking are raising rates of diagnosis and treatment. Rising emphasis on sleep health is significantly increasing its demand globally and drive the global positive airway pressure devices market share across geographies.

For instance, in February 2025, the American Academy of Sleep Medicine reported a 21% rise in sleep apnea screenings in primary care, boosting early diagnoses and PAP device demand.

Restraints:

-

Reimbursement Challenges are Restraining the Positive Airway Pressure Devices Market Growth

Reimbursement issues serve as an inhibiting factor for the global positive airway pressure devices market growth. Strict insurance requirements, costly out-of-pocket rental charges, and inadequate coverage of option therapies restrict patient access to PAP. Regional and insurance-based disparities also contribute to inconsistency in the practical approach to diagnosis and treatment. These financial and administrative obstacles result in a large proportion of clinically eligible patients missing the opportunity to receive timely care, which impairs the overall adoption and restrains the positive airway pressure devices market growth.

For instance, in January 2025, the American Sleep Apnea Association reported that 34% of the U.S. patients discontinued PAP therapy within 6 months due to insurance-related barriers and high costs.

Segmentation Analysis:

By Product

Continuous Positive Airway Pressure was the dominant segment in the positive airway pressure devices market analysis, with a 65.70% market share in 2024, as the first-choice therapy for obstructive sleep apnea. High uptake of the monitor is driven by its established effectiveness, ease of use, and widespread clinical acceptance. Robust insurance coverage and home use add to the adoption of CPAP, which adds significantly to the total airway pressure devices market share globally.

Bilevel Positive Airway Pressure is emerging as the fastest-growing segment in the global positive airway pressure devices market, with a CAGR of 6.10%, driven by its ability to manage complicated respiratory disorders as COPD and respiratory failure. The two-pressure setting allows customizing the pressure to each patient for greater comfort and compliance. Growing demand for hospital and critical care use is propelling the adoption, driving a meteoric rise in the positive airway pressure devices market growth in various regions.

By Application

In 2024, the Obstructive Sleep Apnea, controlled positive airway pressure devices market had with 76.64% market share, since it is the most common sleep-related breathing disorder managed using PAP therapy. Mounting obesity, inactive habits, and improved diagnoses lead to higher rates of OSA detection. The high patient population has led to wider adoption of devices, and thus, OSA accounted for the largest positive airway pressure devices market share globally.

COPD is the fastest-growing segment in the global positive airway pressure devices market trend, as a result of expanding international prevalence and the growing adoption of BiPAP for respiratory management. Growing COPD cases, along with increasing exposure to pollution, are leading to demand for non-invasive ventilation. This growing clinical need is driving the global positive airway pressure devices market growth.

By End-user

The Hospitals & Clinics controls the global positive airway pressure devices industry with a significant market share of 72.30%, owing to their importance in early diagnosis, sleep studies, and acute respiratory management. These institutions typically take care of the sickest patients who need BiPAP or CPAP at the inpatient level of care. These players have superior infrastructure and receive reimbursements, which aid them in the swift adoption of high-end positive airway pressure devices market share and ensure dominance in the clinical market.

In the positive airway pressure devices industry, the home care settings segment plays a vital role, registering the fastest growth over the forecast period, driven by the trend to remote monitoring, convenience, and low-cost management of chronic sleep disorders, including OSA. Growing preference for portable and connected PAP devices for long-term home use is increasing the patients’ compliance, thereby responsible to the positive overall airway pressure devices market growth in developed and developing regions.

Regional Analysis:

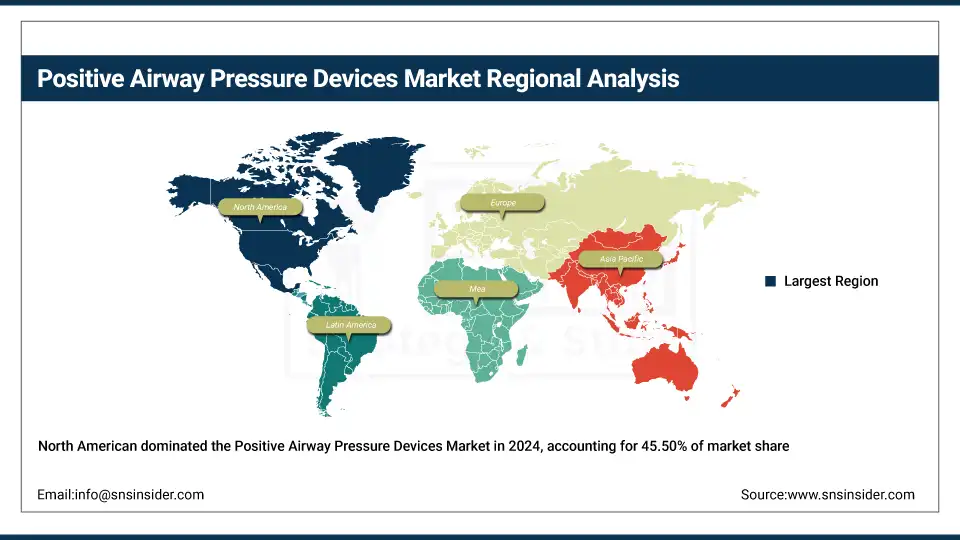

In 2024, the North American region dominated the positive airway pressure devices industry and accounted for 45.50% of the overall revenue share owing to its state-of-the-art healthcare system, high awareness of sleep diseases, and robust insurance-based modalities. Obstructive sleep apnea is common in the basin due to the high rates of obesity, aging seniors, and a sedentary lifestyle. The availability of diagnostic tools, including home sleep tests and sleep labs, also increases the acceptance of PAP therapy. Moreover, major players, including ResMed and Philips Respironics, are well established in the U.S., ensuring innovative practice and availability, further consolidating the dominance of North America in the PAP devices market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe accounts for the second major share in the global positive airway pressure devices industry on account of an increase in sleep apnea awareness, a growing aged population, and developed public healthcare systems. Stable device uptake is promoted by governmental reimbursement policies and greater acceptance of home-based sleep therapy. Besides this, the availability of prominent manufacturers and increasing clinical attention towards non-invasive respiratory care to lead Europe to a significant position in the global market for positive airway pressure devices.

The Asia Pacific region is projected to grow with the fastest CAGR of 6.04% over the forecast period, fueled by a growing acknowledgment of the issue of sleep disorders, rising obesity, and growing urbanization. With the progression of medical facilities in regions including China, India, and Japan, the early diagnosis and treatment of OSA are increasingly emergent. Furthermore, the demand for at-home sleep testing and portable PAP therapy is increasing as costs decrease and government health agencies promote home testing and therapy as a viable option. It also has the advantage of regional manufacturers providing low-cost solutions. Increasing healthcare expenditure, rise in medical tourism, and increasing prevalence of chronic respiratory diseases are amongst the few positive factors responsible for the demand of medical gases and equipment. Together, these have led to rapid positive airway pressure devices market growth in Asia Pacific and an increased global presence.

The Middle East & Africa have the least share in the positive airway pressure devices market because of low awareness of sleep apnea, underdiagnosis, and limited availability of specialty health care services. Inconsistent reimbursement, economic constraints, and a lack of sleep clinics continue to limit market penetration. Furthermore, the high cost of PAP devices in comparison with the income range also restricts affordability, which in turn dampens greater acceptance, and this is negatively affecting market growth in the region as a whole.

Latin America is a relatively small market for the positive airway pressure devices industry, with growth spurred by increased awareness of sleep apnea and access to healthcare. CPAP and BiPAP use are on the rise in countries including Brazil and Mexico, particularly in urban areas. Nonetheless, economic inequalities, inequality in insurance access, and underdetection still create barriers for PAP therapy implementation on a large scale in the region.

Key Players:

Positive airway pressure device companies include ResMed Inc., Philips Respironics, Fisher & Paykel Healthcare Corporation, Limited, 3B Medical, Inc., DeVilbiss Healthcare LLC, BMC Medical Co., Ltd., Somnetics International, Inc., Vyaire Medical, Inc., Curative Medical, Inc., Löwenstein Medical Technology GmbH + Co. KG, and other players.

Recent Developments:

-

In March 2025, ResMed launched AirSense 11 AutoSet Elite in March 2025, enhancing personalized CPAP therapy with digital coaching and real-time monitoring, improving sleep apnea treatment adherence and clinical outcomes.

-

In February 2025, Fisher & Paykel released the NextGen SleepStyle CPAP featuring auto-adjusting humidification, pressure relief, and user-friendly design to boost comfort and adherence in obstructive sleep apnea therapy.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.21 billion |

| Market Size by 2032 | USD 4.89 billion |

| CAGR | CAGR of 5.42% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Continuous Positive Airway Pressure, Automatic Positive Airway Pressure, Bilevel Positive Airway Pressure) • By Application (Obstructive Sleep Apnea, Respiratory Failures, COPD) • By End User (Home Care Settings, Hospitals & Clinics, Others )" |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ResMed Inc., Philips Respironics, Fisher & Paykel Healthcare Corporation, Limited, 3B Medical, Inc., DeVilbiss Healthcare LLC, BMC Medical Co., Ltd., Somnetics International, Inc., Vyaire Medical, Inc., Curative Medical, Inc., Löwenstein Medical Technology GmbH + Co. KG, and other players. |

Frequently Asked Questions

ResMed Inc., Philips Respironics, Fisher & Paykel Healthcare Corporation, Limited, 3B Medical, Inc., DeVilbiss Healthcare LLC, BMC Medical Co., Ltd, are the key players in the Positive Airway Pressure Devices Market.

Reimbursement Challenges are Restraining the Positive Airway Pressure Devices Market Growth

The CAGR of the Positive Airway Pressure Devices Market is 5.42% during the forecast period of 2025-2032.

The North American region dominated the Positive Airway Pressure Devices Market in 2024.

The projected market size for the Positive Airway Pressure Devices Market is USD 4.89 billion by 2032.

Get in Touch