Programmable Network Market Report Scope & Overview:

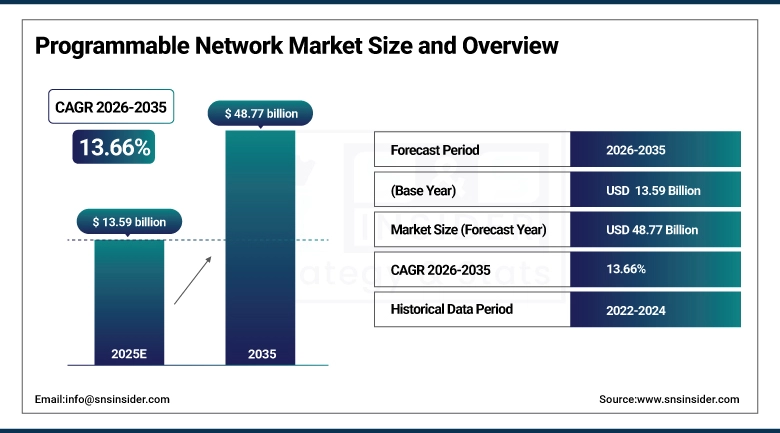

The Programmable Network Market size was valued at USD 13.59 Billion in 2025 and is projected to reach USD 48.77 Billion by 2035, growing at a CAGR of 13.66% during 2026–2035.

Network infrastructure that cannot be reconfigured without touching physical hardware has become a practical liability at a time when the workloads running on those networks change continuously and unpredictably. Programmable networks built on software-defined principles, API-driven control planes, and hardware that separates forwarding logic from management intelligence address this directly. They allow network behavior to be changed from software, at speed, without dispatching engineers to equipment rooms. For hyperscale cloud operators managing tens of thousands of servers across multiple data centers, that capability is operationally non-negotiable. For telecommunications carriers rearchitecting their infrastructure to support 5G network slicing, it is technically required.

Market Size and Forecast:

-

Market Size in 2025: USD 13.59 Billion

-

Market Size by 2035: USD 48.77 Billion

-

CAGR: 13.66% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Programmable Network Market - Request Free Sample Report

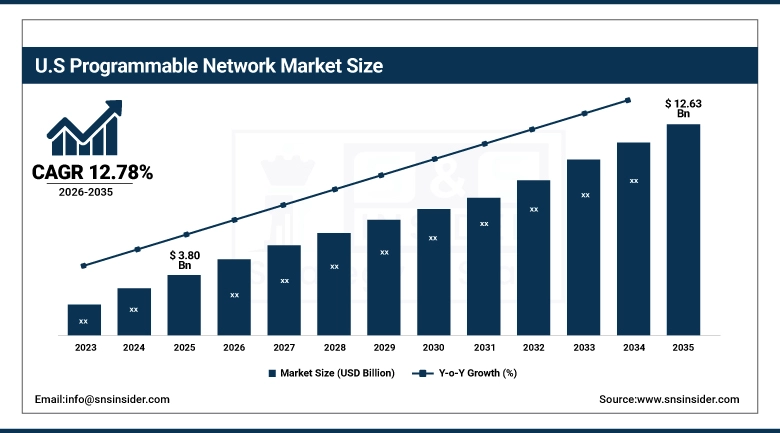

The U.S. Programmable Network Market was valued at USD 3.80 Billion in 2025 and is projected to reach USD 12.63 Billion by 2035, growing at a CAGR of 12.78% during 2026–2035. The United States market is defined by the scale of its hyperscale cloud operators, the density of its enterprise IT infrastructure, and the financial capacity of its telecommunications carriers to invest in next-generation network architectures at a pace that most other national markets cannot match.

Key Programmable Network Market Trends:

-

SDN adoption expands beyond data centers into WANs and campuses, boosting operational efficiency.

-

Intent-based networking automates policy-driven configurations, reducing dependency on specialized network engineers.

-

AI-driven network operations detect anomalies, predict capacity, and remediate faster than humans.

-

Open networking with merchant silicon and disaggregated software shifts competition to software services.

-

5G network slicing drives carriers to deploy programmable infrastructure for isolated, performance-guaranteed networks.

Programmable Network Market Growth Drivers:

-

Escalating Data Center Complexity, Cloud Adoption, and 5G Infrastructure Investment Are Creating Network Environments Where Programmability Is No Longer Optional

The operational argument for programmable networks has been made theoretically for two decades, but the practical urgency driving adoption today is rooted in something more concrete: the gap between what modern applications require from a network and what statically configured infrastructure can deliver has become operationally painful at scale. Hyperscale data center operators running microservices architectures across thousands of servers need network policies that update in milliseconds as workloads spin up, migrate, and terminate. A network team configuring those changes manually through CLI interfaces simply cannot keep pace the automation that programmable infrastructure enables is not a convenience, it is a functional requirement. The 5G buildout adds a further layer of technical necessity: network slicing, which allows a single physical 5G infrastructure to run multiple isolated virtual networks with different performance guarantees for different customers, cannot be implemented on non-programmable infrastructure at all.

Programmable Network Market Restraints:

-

Legacy Infrastructure Inertia, Skills Shortages, and Multi-Vendor Interoperability Complexity Are Slowing Enterprise and Carrier Migration to Programmable Network Architectures

The transition to programmable network infrastructure is not technically complicated in the way that early SDN deployments were the technology has matured substantially and the vendor ecosystem has consolidated around workable standards and APIs. What actually slows adoption is organizational and operational rather than technical. Large enterprises and telecommunications carriers have network infrastructure that was purchased, configured, and optimized over years or decades, staffed by teams whose skills are oriented around the operating practices of that infrastructure. Migrating to programmable architectures requires not just new hardware and software purchases but parallel operation of old and new systems during a transition period that carries risk, retraining of network teams on programming concepts and automation tools that differ fundamentally from traditional network operations work, and integration of programmable network components with legacy systems that were not designed to be controlled by external software.

Programmable Network Market Opportunities:

-

AI-Driven Network Automation, Open Networking Architectures, and Emerging Market Digital Infrastructure Investment Are Opening Growth Pathways That Extend Well Beyond Core Data Center SDN Deployments

The mix of programmable networking with AI and machine learning is creating a new way to manage networks that is much better than what each technology can do on its own. Programmable infrastructure offers the APIs and data streams that allow AI systems to see the network's status in real-time across many devices at once. AI provides the pattern recognition and decision logic that can act on that telemetry at a speed and consistency that human operations teams cannot match. Together, they produce networks that can detect and respond to performance degradation, security incidents, and capacity constraints autonomously, reducing the operational burden on network teams and improving the consistency of network behavior across large and complex environments.

Programmable Network Market Segment Analysis:

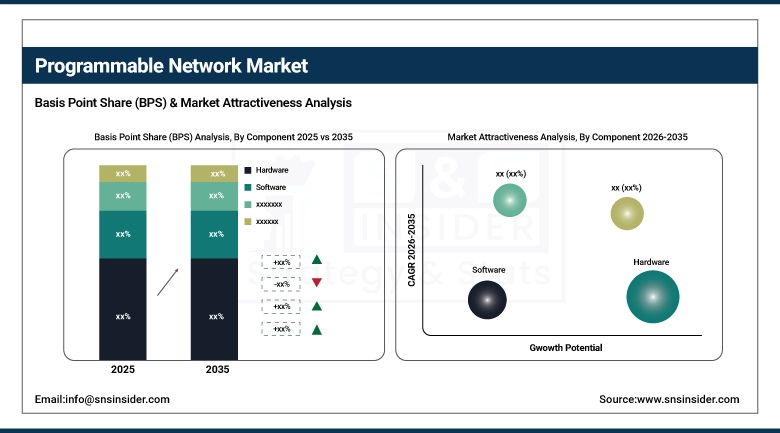

By Component: Hardware Leads Programmable Network Market While Software Registers Fastest CAGR Through 2035

Hardware dominated with a 42.18% share in 2025, valued at approximately USD 5.73 Billion, while Software is expected to grow at the fastest CAGR of approximately 15.40% through 2035. Hardware holds the leading share because programmable network deployments require physical infrastructure programmable ASICs, P4-capable switching platforms, and SmartNIC-equipped servers that carries high per-unit values and is purchased in volume by data center operators and telecommunications carriers executing infrastructure buildout programs.

By Deployment Mode: On-Premises Leads While Cloud-Based Deployment Drives Fastest Growth Through 2035

On-Premises dominated with a 58.72% share in 2025, valued at approximately USD 7.98 Billion, while Cloud-Based deployment is expected to grow at the fastest CAGR of approximately 16.63% through 2035. On-premises deployment retains its dominant share because the majority of existing programmable network infrastructure data center SDN fabrics, carrier SDN deployments, and enterprise campus automation runs on hardware that organizations own and operate within their facilities. The installed base of on-premises programmable networking is large and the procurement cycles for expanding it are well established.

By Application: Data Center Networking Leads While Network Automation & Orchestration Drives Fastest Growth Through 2035

Data Center Networking dominated with a 31.84% share in 2025, valued at approximately USD 4.33 Billion, while Network Automation & Orchestration is expected to grow at the fastest CAGR of approximately 14.66% through 2035. Data center networking holds its leading application share because the hyperscale and enterprise data center segments represent the highest-density and highest-value deployments of programmable switching and routing infrastructure, where the operational case for software-defined control is most clearly quantifiable and the procurement scale is largest.

By End-User: Telecommunications Service Providers Lead While Cloud Service Providers Register Fastest CAGR Through 2035

Telecommunications Service Providers dominated with a 36.14% share in 2025, valued at approximately USD 4.91 Billion, while Cloud Service Providers are expected to grow at the fastest CAGR of approximately 15.21% through 2035. Telecommunications carriers hold the dominant end-user share because their 5G infrastructure buildout programs, network function virtualization deployments, and SD-WAN service launches have all created large programmable networking procurement volumes that dwarf what any single enterprise or cloud customer generates. The scale of carrier network infrastructure covering transport, core, metro, and access layers means that even incremental programmability adoption across those layers creates substantial market revenue.

Programmable Network Market Regional Analysis:

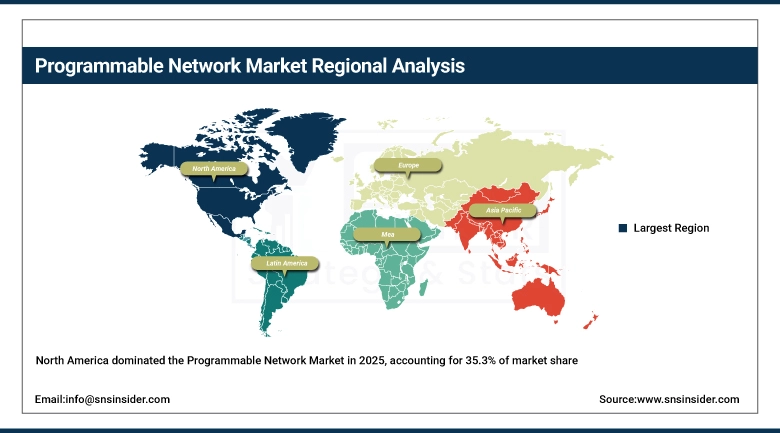

North America Programmable Network Market Insights

North America dominated the Programmable Network Market in 2025, accounting for 35.3% of market share, valued at USD 4.79 Billion, and is projected to reach USD 16.29 Billion by 2035 at a CAGR of 13.04% during the forecast period. The region's market leadership is grounded in the concentration of hyperscale cloud operators, the depth of enterprise IT infrastructure investment, and the financial scale of its telecommunications carriers executing 5G buildout programs. The United States hosts the world's largest deployments of programmable data center networking by absolute switch port count, and the vendor ecosystem concentrated in Silicon Valley and the broader U.S. technology industry produces the hardware, operating systems, and management software that defines the global state of the art in network programmability.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Programmable Network Market Insights

The United States accounts for 79.3% of North American demand in 2025. The U.S. Programmable Network Market was valued at USD 3.80 Billion in 2025 and is projected to reach USD 12.63 Billion by 2035, growing at a CAGR of 12.78% during 2026–2035. The depth of the U.S. market reflects procurement activity across multiple simultaneous investment cycles: hyperscale data center expansion, enterprise SD-WAN replacement of MPLS, federal government network modernization programs, and carrier 5G core deployments are all generating programmable networking procurement in parallel rather than in sequence, sustaining the market at a pace that single-driver markets cannot match.

Europe Programmable Network Market Insights

Europe held a 27.6% share of the Programmable Network Market in 2025, valued at USD 3.76 Billion, and is expected to reach USD 12.74 Billion by 2035 at a CAGR of 13.02% during the forecast period. European demand is anchored by large telecommunications carriers executing 5G core virtualization programs, enterprise SD-WAN deployments driven by the distributed workforce trends that accelerated during and after the pandemic years, and growing data center investment in Germany, the Netherlands, Ireland, and the Nordic countries from both domestic operators and U.S. hyperscale operators expanding their European footprint. Regulatory requirements around data sovereignty and network security create additional demand for programmable security enforcement capabilities that can be configured and audited at the policy level.

Germany Programmable Network Market Insights

Germany leads the European market, supported by the scale of its enterprise IT sector, the technical sophistication of its industrial network operations in manufacturing and automotive verticals, and the active 5G network buildout by Deutsche Telekom, Vodafone Germany, and Telefonica Deutschland. German enterprise adoption of SD-WAN and network automation has been among the strongest in Europe, driven by the complexity of managing distributed manufacturing and logistics networks that span multiple countries and require consistent policy enforcement across geographically dispersed locations.

Asia Pacific Programmable Network Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 14.80% from 2026 to 2035, rising from USD 3.42 Billion in 2025 to USD 13.57 Billion by 2035. The region's growth leadership reflects several simultaneous forces: China's domestic technology investment in homegrown SDN platforms and programmable networking hardware as part of its technology self-sufficiency programs; Japan and South Korea's advanced telecommunications carriers executing network function virtualization and 5G slicing deployments; India's rapidly expanding data center market driven by domestic cloud adoption and foreign hyperscale investment; and Southeast Asian digital infrastructure buildout programs in Indonesia, Vietnam, and Thailand that are deploying programmable networking as the foundational architecture for new data center and carrier infrastructure.

China Programmable Network Market Insights

China is the dominant national market within Asia Pacific, driven by the scale of Alibaba Cloud, Tencent Cloud, and Huawei's cloud infrastructure deployments, the 5G buildout by China Mobile, China Unicom, and China Telecom that represents the world's largest single 5G network construction program by site count, and substantial government investment in sovereign networking technology. Chinese vendors including Huawei and ZTE are competitive participants in the global programmable networking market and are the primary suppliers for Chinese carrier and government network programs, giving the domestic market a supply-side dynamic that differs materially from Western markets where U.S. and European vendors dominate.

Latin America and Middle East & Africa Programmable Network Market Insights

Latin America held approximately 6.5% of the global Programmable Network Market in 2025, valued at USD 0.88 Billion, and is expected to reach USD 3.38 Billion by 2035 at a CAGR of 14.41% during the forecast period. Brazil and Mexico lead regional adoption, driven by telecommunications carrier network modernization programs, growing enterprise SD-WAN deployment among multinational companies with Latin American operations, and expanding data center investment in São Paulo and Mexico City from both regional and international operators. Middle East & Africa held approximately 5.4% of market share in 2025, valued at USD 0.74 Billion, and is expected to reach USD 2.79 Billion by 2035 at a CAGR of 14.25% during the forecast period. Gulf state digital infrastructure investment particularly in the UAE and Saudi Arabia, where sovereign cloud and smart city programs are driving data center and network modernization at government-backed scale is the primary regional demand driver. South Africa leads the African continent's programmable networking adoption within a concentrated private sector technology market.

Competitive Landscape for Programmable Network Market:

Cisco Systems is the world's largest networking company and the market's most comprehensive supplier of programmable network technology, with product lines spanning programmable switches and routers, the DNA Center intent-based networking platform, SD-WAN through its Viptela and Meraki platforms, network automation software, and cloud-managed networking services. Cisco's competitive position in programmable networking is built on the breadth of its portfolio it can supply hardware, operating system, controller, automation software, and managed service components from a single vendor and on the scale of its installed enterprise and carrier customer base, which gives it both a migration upgrade opportunity and a competitive moat built on operational familiarity.

In March 2025, Cisco announced the general availability of Cisco Networking Cloud, a unified cloud management platform that consolidates management of campus, branch, data center, and WAN network domains into a single interface backed by AI-driven insights and automated remediation capabilities.

VMware operates in the programmable network market primarily through its NSX network virtualization and security platform and its SD-WAN solution derived from the VeloCloud acquisition. NSX provides software-defined networking and micro-segmentation capabilities for virtualized and cloud environments, enabling network security policies to follow workloads as they move across hybrid and multi-cloud infrastructure rather than being tied to fixed network perimeters. The platform is deployed across a large enterprise installed base that uses VMware virtualization infrastructure, giving NSX a natural installed base for expansion that does not require displacing existing networking hardware.

In January 2025, VMware, now operating as part of Broadcom following the acquisition completed in late 2023, announced NSX 4.2 with enhanced AI-powered security policy recommendations that analyze network traffic patterns to identify over-permissive access rules and suggest least-privilege replacements.

Programmable Network Market Key Players:

-

Cisco Systems, Inc.

-

Juniper Networks, Inc.

-

VMware, Inc.

-

Huawei Technologies Co., Ltd.

-

Nokia Corporation

-

Arista Networks, Inc.

-

Extreme Networks, Inc.

-

Hewlett Packard Enterprise (HPE)

-

NEC Corporation

-

IBM Corporation

-

Oracle Corporation

-

Dell Technologies Inc.

-

Ciena Corporation

-

Ericsson AB

-

Broadcom Inc.

-

Fujitsu Limited

-

ZTE Corporation

-

Citrix Systems, Inc.

-

Pluribus Networks

-

Big Switch Networks

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.59 Billion |

| Market Size by 2035 | USD 48.77 Billion |

| CAGR | CAGR of 13.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, and Services) • By Deployment Mode (On-Premises and Cloud-Based) • By Application (Data Center Networking, Network Automation & Orchestration, Network Virtualization, and Software-Defined Networking (SDN)) • By End-User (Telecommunications Service Providers, Enterprises (IT & BFSI), Cloud Service Providers, and Government & Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cisco Systems, Inc., Juniper Networks, Inc., VMware, Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Arista Networks, Inc., Extreme Networks, Inc., Hewlett Packard Enterprise (HPE), NEC Corporation, IBM Corporation, Oracle Corporation, Dell Technologies Inc., Ciena Corporation, Ericsson AB, Broadcom Inc., Fujitsu Limited, ZTE Corporation, Citrix Systems, Inc., Pluribus Networks, Big Switch Networks. |

Frequently Asked Questions

The Programmable Network Market size was USD 13.59 Billion in 2025 and is expected to reach USD 48.77 Billion by 2035.

Rising demand for network automation, SDN adoption, 5G deployment, and AI-driven network management.

Hardware dominated the Programmable Network Market.

North America dominated the Programmable Network Market in 2025.

The Programmable Network Market is expected to grow at a CAGR of 13.66% from 2026-2035.

Get in Touch