Scar Treatment Market Report Scope & Overview:

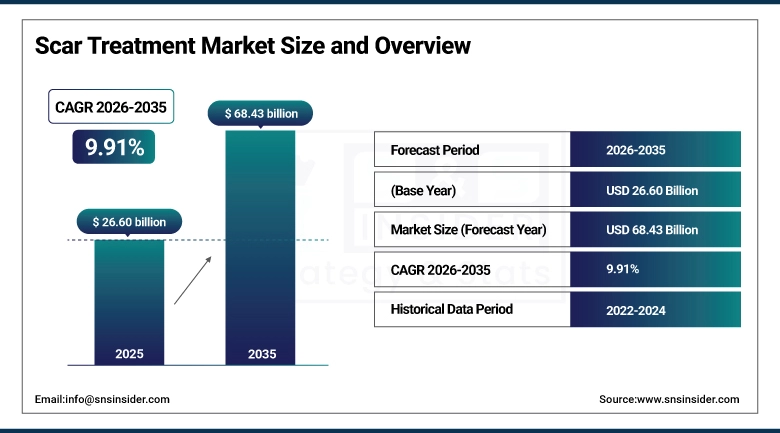

The Scar Treatment Market was valued at USD 26.60 Billion in 2025 and is expected to reach USD 68.43 Billion by 2035, growing at a CAGR of 9.91% from 2026-2035.

The Scar Treatment Market is expanding due to increasing awareness and demand for advanced cosmetic and reconstructive procedures. Rising prevalence of acne, surgical scars, burns, and traumatic injuries is driving adoption of topical treatments, injectables, and laser therapies. Technological advancements in minimally invasive procedures, innovative scar management products, and growing preference for effective, faster-healing solutions are further fueling market growth. Additionally, increasing disposable income and aesthetic consciousness are supporting widespread consumer uptake.

Over 100 million surgical and trauma scars occur annually worldwide; 70% of patients seek scar treatments, with laser therapy and injectables growing at 12% yearly due to demand for faster, effective, minimally invasive solutions.

Scar Treatment Market Size and Forecast:

-

Market Size in 2025: USD 26.60 Billion

-

Market Size by 2035: USD 68.43 Billion

-

CAGR: 9.91% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Scar Treatment Market - Request Free Sample Report

Scar Treatment Market Trends:

-

Rising demand for minimally invasive and non-surgical scar treatments boosting market growth globally

-

Increasing awareness of post-surgery and acne scar management driving adoption of advanced treatment solutions

-

Growing use of laser therapy, silicone gels, and microneedling for effective scar reduction outcomes

-

Expansion of dermatology clinics and aesthetic centers supporting accessibility to innovative scar treatment options

-

Rising preference for personalized and combination therapies to improve skin appearance and patient satisfaction

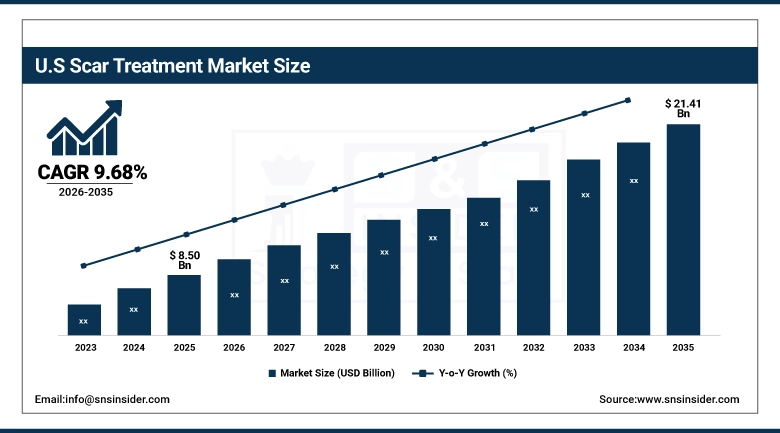

U.S. Scar Treatment Market was valued at USD 8.50 billion in 2025 and is expected to reach USD 21.41 billion by 2035, growing at a CAGR of 9.68% from 2026-2035.

Growth in the U.S. Scar Treatment Market is driven by rising prevalence of acne, surgical, and traumatic scars, coupled with increasing demand for advanced topical, injectable, and laser therapies. Technological innovations, minimally invasive procedures, and growing aesthetic awareness are further boosting adoption across healthcare and cosmetic sectors.

Scar Treatment Market Growth Drivers:

-

Increasing prevalence of acne, burns, surgical, and traumatic scars drives demand for effective scar treatment products and procedures globally

The growing incidence of acne, burn injuries, surgical interventions, and traumatic accidents worldwide has significantly increased the need for scar management solutions. Patients and healthcare providers are seeking effective treatments to minimize scar formation, improve skin appearance, and enhance overall quality of life. This rising prevalence drives demand for a variety of scar treatment options, including topical products, laser therapies, injectables, and other medical devices. Increased patient awareness and physician recommendations further accelerate adoption, fueling continuous growth in the scar treatment market globally.

Over 90% of individuals experience traumatic or surgical scars annually, while acne affects nearly 85% of teens and young adults; rising burn incidence and cosmetic awareness fuel global demand for advanced scar therapies.

-

Rising awareness and preference for cosmetic and aesthetic procedures boost adoption of advanced scar treatment therapies and minimally invasive solutions

Increasing focus on personal appearance and aesthetic outcomes has led more individuals to seek professional scar treatment options. Awareness campaigns, social media influence, and availability of minimally invasive procedures such as laser therapy, microneedling, and injectables encourage adoption. Patients now prefer treatments with faster recovery times, fewer side effects, and visible results. The combination of growing cosmetic consciousness, easy access to dermatology clinics, and the desire for improved self-esteem is driving widespread acceptance of advanced scar treatment therapies worldwide, supporting overall market growth.

Over 60% of patients now prioritize scar minimization post-surgery, with 70% choosing minimally invasive treatments for superior cosmetic outcomes, fueling demand for advanced scar therapy technologies globally.

Scar Treatment Market Restraints:

-

High cost of advanced scar treatment therapies limits patient accessibility, especially in low-income regions, restricting overall market adoption

Advanced scar treatments, such as laser therapies, injectables, and specialized topical formulations, often come with high costs that many patients cannot afford. In low-income regions, limited healthcare budgets and out-of-pocket expenses prevent widespread adoption, restricting market growth. Additionally, insurance coverage for cosmetic or reconstructive procedures is often minimal or unavailable, further limiting patient access. The high treatment costs make it challenging for providers to expand their services to underserved populations, slowing overall adoption of advanced scar treatment solutions globally.

Advanced scar treatments cost USD1,500–USD5,000 per session, limiting access for 70% of patients in low-income regions; high expenses restrict widespread adoption despite clinical benefits and growing demand.

-

Lack of awareness among patients regarding available treatment options reduces demand, particularly in developing countries with limited dermatology education

Many patients remain unaware of effective scar treatment options, including modern lasers, injectables, and topical therapies. In developing countries, limited access to dermatology education, healthcare resources, and awareness campaigns contributes to low patient knowledge. This lack of awareness results in delayed treatment, reliance on ineffective remedies, or avoidance of professional care. Consequently, demand for scar treatment products and services remains restricted. Educating patients about treatment benefits, safety, and effectiveness is crucial to increasing adoption and driving growth in emerging markets.

Over 60% of patients in developing regions remain unaware of advanced ankle replacement options, with limited orthopedic education and low public awareness leading to delayed or foregone treatment despite viable clinical solutions.

Scar Treatment Market Opportunities:

-

Rising awareness about scar management and cosmetic appearance is increasing demand for advanced scar treatment solutions globally

Increasing public focus on aesthetic appearance and skin health is driving demand for effective scar treatment solutions. Awareness campaigns, social media influence, and dermatology education are encouraging patients to seek treatments for acne scars, surgical scars, and burn scars. This growing awareness is prompting both healthcare providers and cosmetic clinics to offer advanced therapies. As patients prioritize improved appearance and self-confidence, the global market for scar management solutions—including topicals, injectables, and laser therapies—is expanding significantly.

Over 70% of patients now prioritize scar minimization post-surgery, with global demand for advanced scar treatments rising as cosmetic outcomes become a key factor in treatment decisions, especially among younger and aesthetic-conscious populations.

-

Technological advancements in laser therapy, injectables, and topical formulations create opportunities for more effective and minimally invasive scar treatments

Innovations in scar treatment technologies, such as fractional lasers, microneedling injectables, and bioactive topical formulations, are enhancing treatment outcomes. Minimally invasive procedures reduce recovery time, pain, and side effects, increasing patient adoption. Healthcare providers can leverage these advancements to offer personalized, efficient, and effective scar management solutions. Continuous research and development are introducing new devices and products that target various scar types, driving market growth. These technological developments provide opportunities for clinics, hospitals, and dermatology centers to expand services and attract a larger patient base.

Over 60% of dermatologists report increased use of laser therapy and targeted injectables for scar revision, while topical formulations with growth factors show 40% higher patient satisfaction, driving adoption of minimally invasive scar solutions globally.

Scar Treatment Market Segment Highlights

-

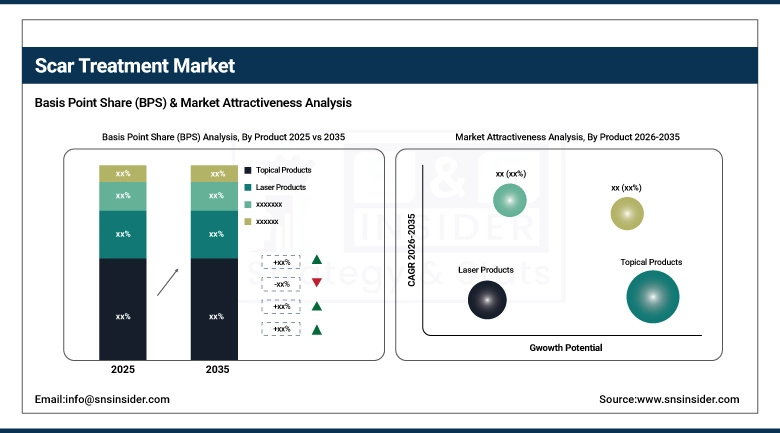

By Product In 2025, Topical Products led the market with 65% share while Laser Products is the fastest-growing segment (2026–2035)

-

By Application In 2025, Acne Scars led the market with 40% share while Traumatic Scars is the fastest-growing segment (2026–2035)

-

By Type In 2025, Atrophic Scars led the market with 40% share while Hypertrophic & Keloid Scars is the fastest-growing segment (2026–2035)

-

By End-use In 2025, Homecare led the market with 60% share while Clinics is the fastest-growing segment (2026–2035)

Scar Treatment Market Segment Analysis

By Product, Topical Products segment led in 2025; Laser Products segment expected fastest growth 2026–2035

Topical Products dominated the Scar Treatment Market in 2025 because they are non-invasive, easy to use, widely available, and cost-effective for treating various scar types. High patient preference, over-the-counter availability, and consistent efficacy in reducing scar appearance contributed to their strong adoption across homecare and clinical settings.

Laser Products are expected to grow fastest from 2026–2035 due to increasing preference for advanced, minimally invasive treatments that offer faster results and precise scar remodeling. Rising awareness of aesthetic procedures, technological advancements in laser systems, and growing adoption in dermatology clinics accelerate the segment’s market expansion.

By Application, Acne Scars segment led in 2025; Traumatic Scars segment expected fastest growth 2026–2035

Acne Scars dominated the Scar Treatment Market in 2025 because of their high prevalence among adolescents and adults worldwide. Continuous demand for effective scar management solutions, including topical creams, silicone gels, and minimally invasive procedures, supports strong adoption, making acne scars the largest segment in terms of treatment focus.

Traumatic Scars are expected to grow fastest from 2026–2035 due to increasing incidents of accidents, surgeries, and injuries requiring specialized interventions. Rising demand for reconstructive procedures, awareness of aesthetic outcomes, and the availability of advanced treatment options drive rapid growth in this segment.

By Type, Atrophic Scars segment led in 2025; Hypertrophic & Keloid Scars segment expected fastest growth 2026–2035

Atrophic Scars dominated the Scar Treatment Market in 2025 because they are common, particularly post-acne or post-surgery, and require ongoing management. High patient awareness, wide range of treatment options, and favorable outcomes with topical and procedural therapies contribute to the segment’s leading market share.

Hypertrophic & Keloid Scars are expected to grow fastest from 2026–2035 due to increasing recognition of their clinical complexity and aesthetic impact. Rising adoption of advanced treatments such as corticosteroid injections, laser therapy, and combination therapies drives demand in dermatology clinics and specialized scar treatment centers.

By End-use, Homecare segment led in 2025; Clinics segment expected fastest growth 2026–2035

Homecare dominated the Scar Treatment Market in 2025 because of convenience, affordability, and ease of self-administration. Patients prefer topical creams, gels, and silicone-based products that can be applied at home, reducing clinic visits and enabling continuous scar management, driving the segment’s large market share.

Clinics are expected to grow fastest from 2026–2035 due to increasing adoption of procedural treatments such as laser therapy, microneedling, and surgical revision. Rising patient preference for professional interventions, advanced technologies, and aesthetic outcomes fuels rapid growth in clinical scar treatment services.

Scar Treatment Market Regional Analysis:

North America Scar Treatment Market Insights

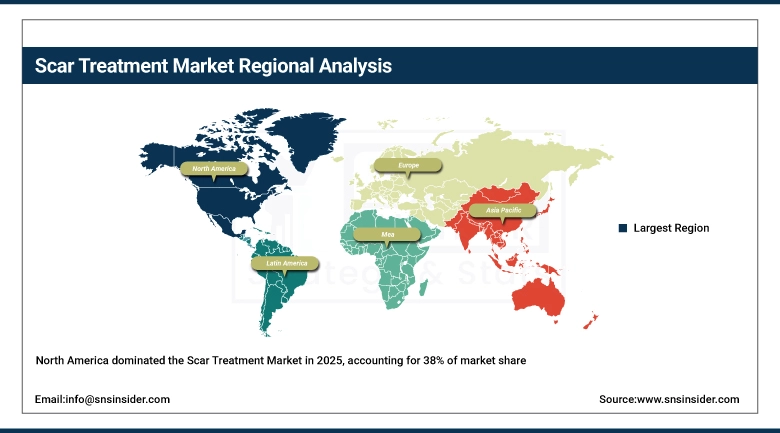

North America dominated the Scar Treatment Market with a 38% share in 2025 due to advanced healthcare infrastructure, high awareness of cosmetic and dermatological procedures, and strong presence of leading scar treatment product manufacturers. Rising demand for minimally invasive therapies, favorable reimbursement policies, and increasing adoption of laser and topical treatments further strengthened regional leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Scar Treatment Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 11.51% from 2026–2035, driven by increasing awareness of scar management, rising cosmetic and dermatology clinics, and growing disposable income. Expanding medical tourism, urbanization, and adoption of advanced scar treatment technologies such as silicone gels, laser therapy, and microneedling accelerate market growth in the region.

Europe Scar Treatment Market Insights

Europe held a significant share in the Scar Treatment Market in 2025, supported by well-established healthcare infrastructure, high adoption of advanced dermatological and cosmetic procedures, and presence of leading manufacturers. Growing awareness of scar management, increasing demand for minimally invasive treatments, and favorable reimbursement policies further strengthened Europe’s market position.

Middle East & Africa and Latin America Scar Treatment Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Scar Treatment Market in 2025, driven by rising awareness of cosmetic and dermatological procedures, increasing healthcare infrastructure, and expanding availability of advanced scar treatment technologies. Growing medical tourism, urbanization, and rising disposable income further supported the regions’ emerging market presence.

Scar Treatment Market Competitive Landscape:

Smith & Nephew is a British multinational medical‑equipment company headquartered in Watford, UK. It develops and sells products across three main segments: Orthopaedics (hip and knee reconstruction), Sports Medicine & ENT (minimally invasive joint repair), and Advanced Wound Management (dressings, bioactive therapies). The company operates globally, with over 18,000 employees and revenues exceeding USD5.8 billion.

-

Mar 2025, at AAOS 2025, they showcased advanced orthopedic reconstruction technologies including their new CATALYSTEM hip system, LEGION knee system, and AETOS shoulder system.

Johnson & Johnson Services, Inc. is the MedTech and Innovative Medicine division of Johnson & Johnson following its consumer-health spin-off. The company manages a diverse portfolio of products, including surgical instruments, orthopedic implants, interventional devices, vision care solutions, and pharmaceutical innovations. With a global workforce exceeding 130,000 employees and operations in more than 175 countries, J&J Services continues the company’s long-standing commitment to advancing medical technologies, delivering innovative healthcare solutions, and improving patient outcomes worldwide.

-

December 2024, J&J MedTech joined global surgical experts to develop a standardized classification system for surgical site outcomes (SSOs), aiming to improve reporting on post-operative complications.

Mölnlycke Health Care AB is a leading Swedish MedTech company headquartered in Gothenburg, specializing in advanced wound care and single-use surgical products, including dressings, gloves, drapes, gowns, and antiseptics. Established in 1849, the company operates in over 100 countries with 14 manufacturing facilities worldwide. Mölnlycke focuses on delivering high-quality, innovative healthcare solutions while emphasizing sustainability in both its product development and operational practices, making it a trusted partner in hospitals and surgical centers globally.

-

September 2024, Mölnlycke formed a distribution partnership with Ondine Biomedical (“Starwave” product) to fight hospital-acquired infections in key markets across the UK, Europe, and the Middle East.

Merz Pharma GmbH & Co. KGaA is a family-owned German pharmaceutical and MedTech company headquartered in Frankfurt am Main. The company operates across three main segments: Aesthetics, offering dermal fillers and neurotoxins; Therapeutics, focusing on neurological movement disorders; and Consumer Care, providing specialized healthcare products. Merz is recognized for its botulinum neurotoxin treatments and maintains state-of-the-art biologic manufacturing facilities in Dessau, Germany. Its strong focus on innovation and quality ensures global leadership in aesthetics and neurological therapies.

-

June 2025, Merz Aesthetics, a Merz division, received Health Canada approval for its regenerative biostimulator Radiuses to treat moderate wrinkles on the décolleté.

Scar Treatment Market Key Players:

-

Smith & Nephew plc

-

Johnson & Johnson Services, Inc.

-

Mölnlycke Health Care AB

-

Merz Pharma GmbH & Co. KGaA

-

Lumenis (XIO Group)

-

Sonoma Pharmaceuticals, Inc.

-

Perrigo Company plc (Mederma)

-

Bausch Health Companies, Inc.

-

Cynosure (Hologic, Inc.)

-

Avita Medical, Ltd.

-

HRA Pharma

-

Polytech Health & Aesthetics GmbH

-

CCA Industries, Inc.

-

NewMedical Technology, Inc.

-

Suneva Medical, Inc.

-

Scar Heal, Inc. (Rejûvaskin)

-

Stratpharma AG

-

CellResearch Corporation

-

Kerecis (Coloplast)

-

Silagen

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 26.60 Billion |

| Market Size by 2035 | USD 68.43 Billion |

| CAGR | CAGR of 9.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Topical Products, Laser Products, Injectables, Others) • By Application (Acne Scars, Surgical Scars, Burn Scars, Traumatic Scars, Others) • By Type (Atrophic Scars, Hypertrophic & Keloid Scars, Contracture Scars, Stretch Marks) • By End-Use (Hospitals, Clinics, Homecare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Smith & Nephew plc, Johnson & Johnson Services, Inc., Mölnlycke Health Care AB, Merz Pharma GmbH & Co. KGaA, Lumenis, Sonoma Pharmaceuticals, Inc., Perrigo Company plc, Bausch Health Companies, Inc., Cynosure (Hologic, Inc.), Avita Medical, Ltd., HRA Pharma, Polytech Health & Aesthetics GmbH, CCA Industries, Inc., NewMedical Technology, Inc., Suneva Medical, Inc., Scar Heal, Inc., Stratpharma AG, CellResearch Corporation, Kerecis, Silagen |

Frequently Asked Questions

The Scar Treatment Market was valued at USD 26.60 Billion in 2025, reflecting strong demand for advanced scar management products and therapies worldwide.

The market is expected to reach USD 68.43 Billion by 2035, driven by increasing cases of surgical scars, acne scars, burn scars, and rising aesthetic awareness.

The market is projected to grow at a CAGR of 9.91% from 2026 to 2035, indicating steady and robust long-term expansion.

Key growth drivers include the rising prevalence of skin injuries, increasing cosmetic procedures, technological advancements in laser therapies, and growing demand for minimally invasive treatments.

Common scar treatment options include topical creams, silicone sheets, laser treatment, injectable therapies, dermabrasion, and surgical revision procedures.

Get in Touch