Semiconductor Memory Market Size & Overview:

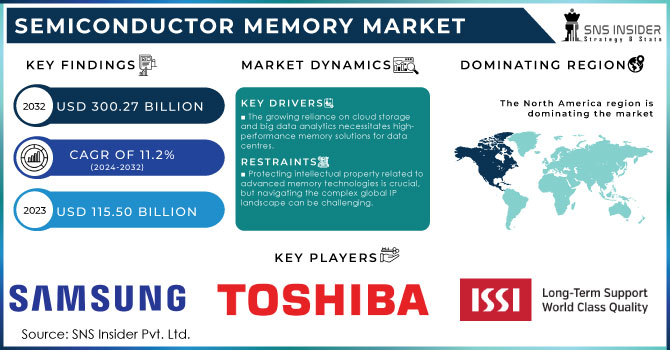

The Semiconductor Memory Market Size was valued at USD 122.35 Billion in 2023 and is expected to reach USD 273.03 Billion by 2032 and grow at a CAGR of 9.4% over the forecast period 2024-2032. The market can include production volume, demand-supply gap, pricing trends, technological advancements, and investment trends. Other important data points include the penetration of various memory types and adoption rates in different end-user industries, R&D spending, and trade flow analysis. Information regarding government policies, regulatory effects, and patent filing can give deeper insights into the market. Mergers and acquisitions statistics, funding trends, and manufacturing capacity utilization rates may also be able to give better insights into the market dynamics, future growth opportunities, and impact of emerging technologies such as AI and IoT.

Get More Information on Semiconductor Memory Market - Request Sample Report

Market Dynamics

Key Drivers:

-

Growing Demand for High-Performance Computing and AI Applications Drives the Semiconductor Memory Market Growth

The increasing adoption of high-performance computing, artificial intelligence (AI), and machine learning is significantly driving the demand for advanced semiconductor memory solutions. High-speed, low-latency DRAM and NAND memory technologies have become essential for applications that require handling of large datasets efficiently. Apart from that, the proliferation of data centers, cloud computing and edge computing are helping to bring high-capacity memory modules into the mainstream. As various industries are embracing automation and AI-driven analytics, manufacturers are investing in innovation to enhance processing speeds and efficiency; hence, semiconductor memory is becoming a crucial tool in the digital transformation of various sectors.

Restraints

-

Supply Chain Disruptions and Semiconductor Shortages Hamper the Growth of the Semiconductor Memory Market

Global supply chain disruptions and semiconductor shortages have posed major challenges to the semiconductor memory market. Fluctuations in production levels due to geopolitical tensions, trade restrictions, and raw material shortages have resulted in a shortage of memory chips. The COVID-19 pandemic exacerbated these disruptions and led to higher lead times and price volatility. Moreover, dependency on a limited number of semiconductor foundries has created supply bottlenecks. Such impediments on the side of manufacturers affect their ability to come up with high demand-responsive productions hence delay their product launches and revenue within industries dependent on semiconductor memory solutions.

Opportunities

-

Rising Investments in Next-Generation Memory Technologies Create Lucrative Opportunities in the Semiconductor Memory Market

The increasing investments in next-generation memory technologies such as MRAM, ReRAM, and 3D NAND would open up the semiconductor memory market to a good growth opportunity. Advanced memory solutions offer higher speeds, lower power consumption, and greater durability over traditional DRAM and NAND. Industry leaders continue to invest R&D budgets toward developing innovative architectures for memory applications that support high-performance computing, AI, and IoT applications. In addition, government initiatives and private funding in semiconductor research and development accelerate the commercialization of cutting-edge memory solutions, opening new markets and areas for technology access.

Challenge

-

Rising Manufacturing Costs and High Capital Expenditure Pose a Major Challenge for the Semiconductor Memory Market

The semiconductor memory market is continuously faced with high manufacturing costs and large capital outlay needed to build production facilities. With semiconductor nodes advancing to newer levels, the cost of fabrication equipment, cleanroom facilities, and qualified manpower continues to increase. The move towards high-end technologies, such as EUV lithography, for manufacturing memory chips further calls for enormous financial investments. Only a few major players have the resources to invest in next-generation fabrication plants, leading to market consolidation. These high costs pose a significant barrier for new entrants and hinder the scalability of semiconductor memory production, affecting overall industry competitiveness.

Segments Analysis

By Application

2023, the Consumer Electronics segment led the semiconductor memory market, accounting for over 32% of global revenue. The dominance is based on the increasing requirement for advanced memory solutions in various devices, including smartphones, tablets, and smart home appliances. Some of the coies, like SK Hynix, have been crucial in this space; their HBM products are growing mainly due to the increasing investment in AI servers and inference processing.

IT & Telecommunications segment, a projected compound annual growth rate (CAGR) of 11.52% underscores the increasing need for efficient data storage and processing capabilities. Broadc recently unveiled 3.5D XDSiP technology, which is designed to make the performance of custom AI processors for cloud providers greatly improve the need for generative AI infrastructure that is on the rise. These depments report that semiconductor memory is critical in both consumer electronics and IT & telecoms-the rising infra that must be able to keep up with swift advances in devices and networks to meet growing data and performance demands.

By Type

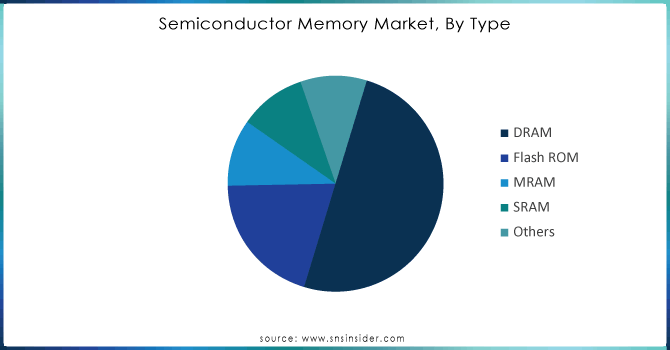

In 2023, the DRAM segment captured the largest share of the semiconductor memory market, accounting for 46% of the total revenue. DRAM (Dynamic Random Access Memory) continues to dominate due to its widespread application in consumer electronics, PCs, and data centers. As data consumption increases and the demand for high-speed processing grows, major companies have invested in DRAM product innovations.

The Flash ROM segment is experiencing the highest CAGR at 11.33% during the forecast period. Flash ROM is favored for its non-volatile nature, retaining data without power, making it ideal for storage in mobile devices, automotive applications, and IoT devices. Recent product developments include advancements in 3D NAND flash technology, which significantly boosts storage density and performance.

Need any Customization as Per Your Business Requirement on Semiconductor Memory Market - Enquiry Now

Regional Analysis

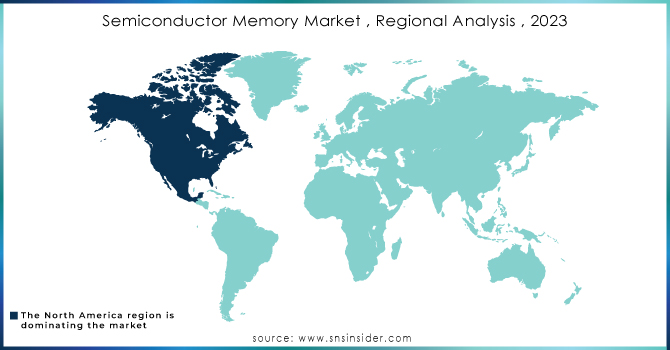

In 2023, the Asia Pacific region dominated the semiconductor memory market, holding an estimated market share of around 43%. The reason for this region's dominance can be attributed to its well-established electronics manufacturing base, with the key countries like China, Japan, South Korea, and Taiwan hosting some of the world's largest memory chip manufacturers, such as Samsung, SK Hynix, and Micron. The region also enjoys favorable government policies and robust infrastructure, further strengthening its position in the global semiconductor memory market.

North America, is the fastest-growing region in the semiconductor memory market, with an estimated CAGR of around 10-11.24% during 2023 and the forecast period. The main growth factor behind this market is the ever-growing demand for advanced memory solutions in data centers, AI, and cloud computing, especially in the United States, where these tech giants-Amazon, Google, and Microsoft-have been highly investing in AI and cloud infrastructure. Increasing technological advancements in automotive electronics, IoT devices, and mobile technology also enhance the demand for semiconductor memory.

Key Players

Some of the major players in the Semiconductor Memory Market are:

-

Integrated Silicon Solution Inc. (IS61LP20448, IS46/48/64 Series DRAM)

-

Micron Technology, Inc. (Micron DDR4 Memory, Micron NOR Flash Memory)

-

Macronix International Co., Ltd. (MX25L25635E Flash Memory, MX30LF1G18AC-10 Flash Memory)

-

Samsung (Samsung DRAM Memory, Samsung NAND Flash Memory)

-

SK HYNIX INC. (SK hynix DDR4 DRAM, SK hynix NAND Flash Memory)

-

Taiwan Semiconductor Manufacturing Company Limited (TSMC 7nm Process, TSMC 5nm Process)

-

Texas Instruments Incorporated (TI DRAM Memory, TI Flash Memory)

-

Infineon Technologies AG (Infineon DRAM, Infineon NAND Flash Memory)

-

IBM Corporation (IBM FlashSystem, IBM Storage Memory Modules)

-

TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION (Toshiba NAND Flash Memory, Toshiba DRAM)

-

KIOXIA Corporation (KIOXIA NAND Flash Memory, KIOXIA DRAM)

-

Winbond Electronics Corporation (Winbond NAND Flash Memory, Winbond DRAM)

-

Renesas Electronics Corporation (Renesas Flash Memory, Renesas DRAM)

-

Fujitsu Limited (Fujitsu DRAM, Fujitsu NAND Flash Memory)

-

Powerchip Technology Corporation (Powerchip DRAM, Powerchip Flash Memory)

Recent Trends

-

In January 2025, Samsung Electronics announced plans to launch an enhanced version of its High Bandwidth Memory (HBM) 3E chips in the first quarter of 2025, aiming to double its supply target to meet growing demand.

-

In November 2024, Toshiba's subsidiary, Kioxia, projected that flash memory demand would nearly triple by 2028, driven by the surge in artificial intelligence applications.

-

December 2024: The U.S. Commerce Department finalized a grant of up to $458 million to SK Hynix for constructing an advanced chip packaging and R&D facility in Indiana. This plant will produce high-bandwidth memory chips for training AI systems and create 1,000 jobs.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 122.35 Billion |

| Market Size by 2032 | US$ 273.03 Billion |

| CAGR | CAGR of 9.4 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (SRAM, MRAM, DRAM, Flash ROM, Others) • By Application (Consumer Electronics, IT & Telecommunication, Automotive, Industrial, Aerospace & Defense, Medical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Integrated Silicon Solution Inc., Micron Technology, Inc., Macronix International Co., Ltd., Samsung, SK HYNIX INC., Taiwan Semiconductor Manufacturing Company Limited, Texas Instruments Incorporated, Infineon Technologies AG, IBM Corporation, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, KIOXIA Corporation, Winbond Electronics Corporation, Renesas Electronics Corporation, Fujitsu Limited, Powerchip Technology Corporation. |

Frequently Asked Questions

Ans: Asia pacific dominated the Semiconductor Memory Market in 2023.

Ans: Consumer Electronics segment dominated the Semiconductor Memory Market.

Ans: The major growth factor of the Semiconductor Memory Market is the increasing demand for high-performance memory solutions driven by advancements in AI, cloud computing, and consumer electronics.

Ans: The Semiconductor Memory Market size was USD 122.35 billion in 2023 and is expected to Reach USD 273.03 billion by 2032.

Ans: The Semiconductor Memory Market is expected to grow at a CAGR of 9.4% during 2024-2032.

Get in Touch