Smoke Alarm Market Report Scope & Overview:

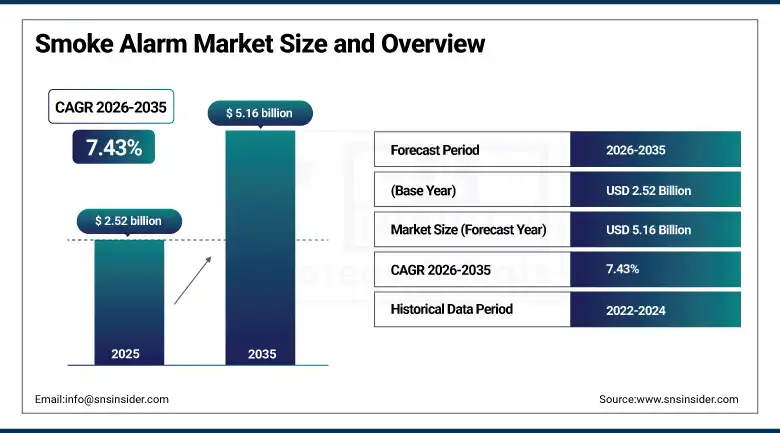

The Smoke Alarm Market was valued at USD 2.52 Billion in 2025 and is expected to reach USD 5.16 Billion by 2035, growing at a CAGR of 7.43% from 2026 to 2035.

Smoke alarms are the most widely installed single-point fire safety device in the world, present in over 96% of U.S. homes and mandatory under building codes across virtually every developed economy. The smoke alarm market is undergoing a meaningful technology bifurcation between commodity standalone alarms and smart connected systems. Conventional standalone battery-operated smoke alarms detect fires and emit a local audible alarm.

Smart IoT-connected smoke alarms transmit alerts to resident smartphones wherever they are located, integrate with smart home ecosystems including Amazon Alexa, Google Home, and Apple HomeKit for automation responses, connect to professional monitoring services for emergency dispatch. This functional enhancement over standalone alternatives is commercially compelling for the growing smart home technology adopter market.

Google Nest's Nest Protect maintained a leading position in the U.S. smart smoke alarm market in 2025. Its combination of smoke and carbon monoxide detection, voice alerts, LED indicators, and smartphone connectivity supports strong consumer demand. Premium smart features enable pricing significantly above conventional alarms, highlighting growing adoption of connected home safety technologies.

Market Size and Forecast

-

Market Size in 2026E: USD 2.71 Billion

-

Market Size by 2035: USD 5.16 Billion

-

CAGR: 7.43% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Smoke Alarm Market - Request Free Sample Report

Smoke Alarm Market Trends

-

Smart IoT-enabled smoke alarms are gaining popularity due to remote monitoring and smartphone notification capabilities.

-

Combination smoke and carbon monoxide alarms are increasingly preferred for residential safety compliance.

-

Ten-year sealed lithium battery alarms are replacing traditional battery-powered models due to lower maintenance needs.

-

Multi-sensor and AI-based technologies are reducing nuisance alarms caused by cooking, steam, and dust.

-

Integration with professional monitoring services is expanding residential fire safety and emergency response capabilities.

The U.S. Smoke Alarm Market Outlook

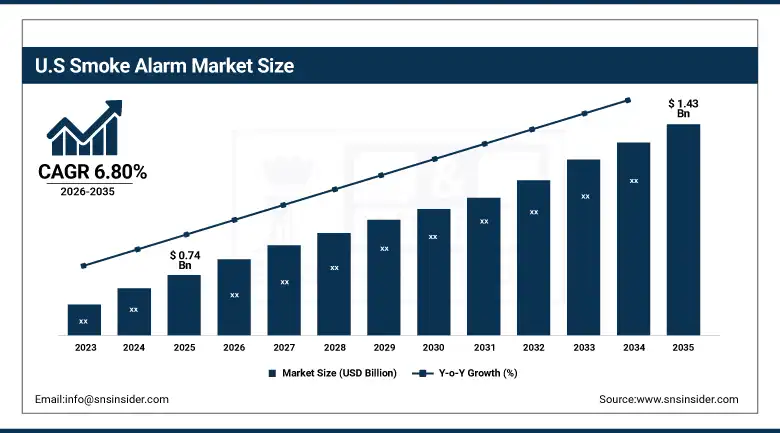

The U.S. smoke alarm market was valued at USD 0.74 Billion in 2025 and is expected to reach USD 1.43 Billion by 2035, growing at a CAGR of 6.80% from 2026 to 2035.

The United States is the world's largest smoke alarm market by installed base and revenue, governed by the National Fire Protection Association's NFPA 72 standard requirements and local fire marshal installation mandates that collectively create the residential and commercial smoke alarm regulatory framework globally.

The U.S. Consumer Product Safety Commission's performance requirements for smoke alarms and the UL 217 listing standard for smoke detecting units define the minimum technical performance baseline that all commercially sold U.S. smoke alarms must satisfy. The residential replacement market is the largest ongoing commercial driver, as the estimated 10-year functional service life of smoke alarms combined with the estimated 116 million U.S. households creates an annual replacement cycle.

Kidde, a subsidiary of Carrier Global, launched its Smart series smoke and CO alarms in 2025. The products feature voice alerts, smartphone connectivity, and smart home compatibility. Positioned below Nest Protect in price, they target mainstream consumers upgrading from conventional alarms to connected safety systems.

Smoke Alarm Market Segment Analysis

-

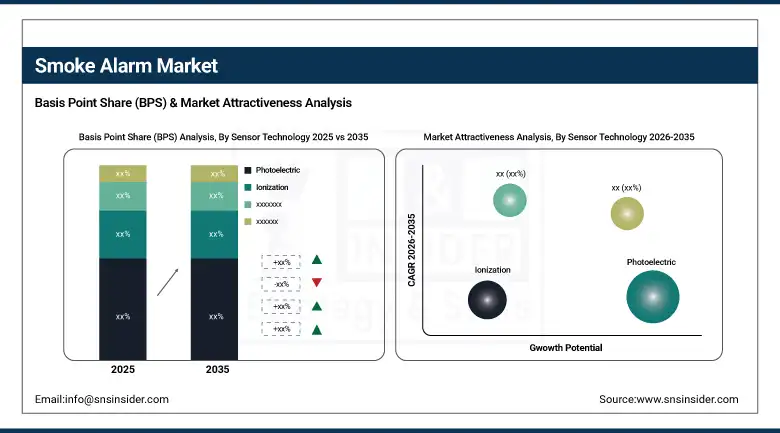

By Sensor Technology, the photoelectric segment dominated the market with 42.35% share in 2025, while the combination/dual sensor segment is the fastest growing with a CAGR of 9.14% during 2026 to 2035.

-

By Connectivity, the wired segment dominated the market with 39.28% share in 2025, while smart/IoT-connected alarms are growing at the fastest CAGR of 9.67% during the forecast period.

-

By Installation Type, the ceiling-mounted segment dominated the market with 51.46% share in 2025, while wall-mounted configurations serve specific architectural requirements.

-

By Application, the residential segment dominated the market with 46.51% share in 2025, while the commercial segment is the fastest growing with a CAGR of 8.93% through 2026 to 2035.

By Sensor Technology, photoelectric dominates, combination/dual sensors grow fastest

Photoelectric sensors generated 42.35% of smoke alarm market revenue in 2025, reflecting their well-documented superiority in detecting slow, smoldering fires that characterize the majority of residential fire starts, whose gradual progression generates dense visible smoke before the rapid flame development that ionization sensors detect most effectively. Regulatory and professional fire safety body recommendations in multiple markets including Australia, the United Kingdom, and increasingly U.S. jurisdictions favor photoelectric technology for residential applications on the basis of its more appropriate response profile for the typical residential fire scenario.

Combination or dual sensor alarms are growing fastest at a CAGR of 9.14%, driven by the compelling consumer logic of comprehensive fire detection coverage that incorporates both slow smoldering detection from the photoelectric sensor and fast flaming fire detection from the ionization sensor in a single device, eliminating the technology selection burden while providing the most complete detection profile across the full range of fire types.

By Application, residential dominates, commercial grows fastest

Residential applications generated 46.51% of smoke alarm market revenue in 2025. The residential segment's commercial dominance reflects the scale of the global housing stock, the mandatory residential smoke alarm installation requirements of virtually every developed country building code, and the replacement market dynamics of an installed base of several hundred million residential smoke alarms globally whose 10-year service life generates a large and structurally predictable annual replacement volume.

Commercial applications are growing fastest at a CAGR of 8.93%, driven by the growing complexity and premium value of commercial fire detection and alarm system installations in commercial buildings, retail facilities, offices, hospitality venues, and healthcare institutions whose integrated addressable fire alarm systems command substantially higher per-device values than residential consumer products.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

United Kingdom |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Smoke Alarm Market Insights

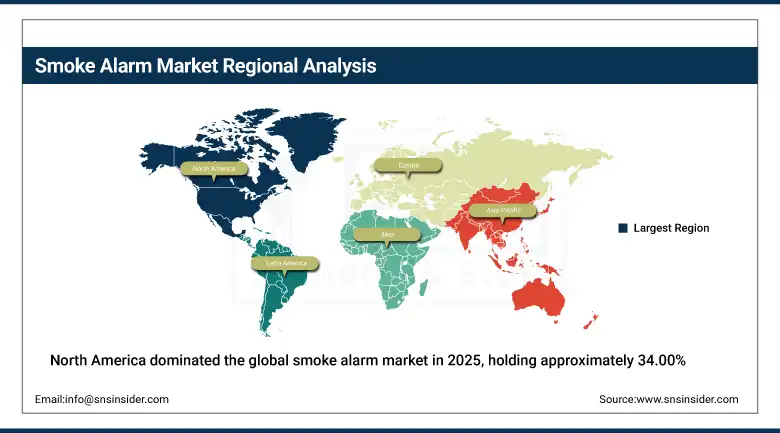

North America dominated the global smoke alarm market in 2025, holding approximately 34.00% of global revenues. The United States accounts for approximately 82.47% of regional revenue through its combination of the world's largest residential smoke alarm installed base, comprehensive federal and state regulatory frameworks mandating smoke alarm installation and maintenance, and the commercially most developed smart smoke alarm consumer adoption.

Canada contributes supplementary demand through its aligned fire safety regulatory framework, whose National Building Code requirements parallel U.S. NFPA 72 standards, and its growing smart home technology adoption rate that is driving Canadian residential smoke alarm replacement toward smart connected products at a pace comparable to U.S. market trends.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Smoke Alarm Market Insights

Europe held approximately 26.00% of global Smoke Alarm revenues in 2025. The United Kingdom's mandatory smoke alarm legislation requiring at least one working smoke alarm on each floor of every residential rental property under the Smoke and Carbon Monoxide Alarm Regulations 2022 has been the most commercially consequential single regulatory event in the recent European smoke alarm market, creating a large mandatory installation and upgrade requirement across the 4.4 million private rental sector properties in England alone.

Germany, France, the Netherlands, and Scandinavian countries each impose residential smoke alarm installation requirements whose enforcement and replacement cycle compliance sustain commercial volume. The UK accounts for approximately 28.47% of European revenues through its active regulatory mandate, high smart alarm adoption in the premium residential segment, and the commercial presence of leading manufacturers including Aico and FireAngel.

Asia Pacific Smoke Alarm Market Insights

Asia Pacific is the fastest-growing regional Smoke Alarm market, projected to expand at a CAGR of approximately 9.14% through 2035. The region's growth is driven by rapidly expanding construction activity across China, India, Southeast Asia, and Australia, progressive adoption of fire safety building codes that mandate smoke alarm installation in new residential and commercial construction, and growing consumer awareness of residential fire risk whose casualty burden in Asia Pacific's dense urban housing stock is creating government and consumer motivation for improved fire safety infrastructure.

China accounts for approximately 38.47% of Asia Pacific revenues through its enormous construction sector, progressively strengthening fire safety regulation, and domestic smoke alarm manufacturing sector that serves both domestic and export markets competitively.

MEA & Latin America Smoke Alarm Market Insights

Middle East and Latin America are growing Smoke Alarm markets where expanding urban construction, progressive adoption of international fire safety standards, and growing government and property developer awareness of fire safety obligations are creating developing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its world-class commercial and residential construction programme whose building codes align with international fire safety standards including NFPA and British Standards that mandate comprehensive smoke detection system installation.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large urban housing stock, progressive fire safety regulation development, and growing commercial building sector whose fire protection system investment is increasing with insurance industry pressure and post-incident regulatory enforcement.

Market Dynamics

Growth Drivers: Global expansion of mandatory residential smoke alarm installation regulations is creating demand across replacement and new installation markets.

Smoke alarm market growth is anchored by two simultaneously operating commercial forces. Regulatory expansion is progressively mandating smoke alarm installation and replacement across residential property categories and geographic markets that were previously underserved or unregulated, creating new addressable markets from existing building stock.

Smart home technology adoption is simultaneously preimmunizing the product mix by converting existing conventional alarm replacement occasions into smart connected alarm purchase events whose higher per-unit revenue and cross-selling potential for CO detection, professional monitoring, and home automation ecosystem integration substantially expand the commercial value of each replacement transaction. Together, these forces create a market whose volume growth from regulatory expansion combines with value growth from smart product premiumization to generate revenue growth above either factor alone would produce.

Restraints: Commodity pricing pressure in conventional standalone alarm segments constrain overall market value growth.

The conventional battery-operated standalone smoke alarm is one of the most commoditized safety devices in the retail market, with private label products available at major home improvement and general merchandise retailers for under USD 10 that satisfy minimum regulatory requirements and create significant downward price pressure on branded conventional alarm product lines. This commodity pricing dynamic limits the revenue value of the replacement cycle for the majority of the global residential smoke alarm installed base whose buyers prioritize minimum compliance cost over product premium features.

Consumer resistance to smart alarm pricing, where the USD 80 to USD 130 price points of leading smart alarm products represent a 4 to 6 times premium over conventional equivalents, constrains smart alarm market penetration to the most technology-engaged and affluent consumer segments whose proportion of the total replacement market moderates overall smart alarm volume growth.

Opportunities: Smart home ecosystem integration and commercial building alarm system modernization represent market growth opportunities beyond.

The rapid global expansion of smart home technology adoption, with installed smart home device counts projected to exceed 1.8 billion globally by 2030, creates a growing consumer base whose prior smart home investment and ecosystem familiarity dramatically increases their receptivity and willingness-to-pay for smart smoke alarms that integrate with their existing Google, Amazon, or Apple home automation infrastructure. Each smart home ecosystem expansion event including new smart speaker placement, smart lighting installation, or home security camera addition creates an ancillary smart smoke alarm upsell opportunity for retailers and installers servicing these customers.

Commercial building addressable fire alarm system modernisation, driven by building automation integration requirements, insurance premium incentives for connected detection systems, and smart building management platform adoption, represents a premium market segment whose commercial building operator customers justify higher-value addressable system procurement.

Recent Developments:

-

2025: Kidde launched its Kidde Smart series of interconnected smoke and CO alarms with smartphone app integration, Amazon Alexa and Google Assistant compatibility, and voice alert functionality.

-

2025: Google Nest expanded Nest Protect integration across its extended smart home ecosystem, reinforcing its market leadership in the premium smart smoke alarm segment.

-

2024: Aico, the UK's smoke and CO alarm manufacturer, launched its Ei3000 series of smart alarms with enhanced wireless interconnection and the Aico SmartLINK gateway enabling multi-alarm home monitoring through the HomeLINK smart home safety platform.

Smoke Alarm Market key players are:

-

Honeywell International Inc.

-

Johnson Controls International PLC

-

Siemens AG

-

Robert Bosch GmbH

-

Kidde (Carrier Global Corporation)

-

First Alert (Resideo Technologies Inc.)

-

Google LLC (Nest Protect)

-

Hochiki Corporation

-

Eaton Corporation PLC

-

Apollo Fire Detectors Ltd.

-

ABB Ltd.

-

FireAngel Safety Technology Group PLC

-

X-Sense Innovations Co. Ltd.

-

Halma plc

-

Gentex Corporation

-

Ei Electronics Ltd.

-

Universal Security Instruments Inc.

-

NAPCO Security Technologies Inc.

-

Schneider Electric SE

-

Panasonic Corporation

Smoke Alarm Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.52 Billion |

| Market Size by 2035 | USD 5.16 Billion |

| CAGR | CAGR of 7.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sensor Technology (Ionization, Photoelectric, Combination/Dual Sensor) • By Connectivity (Wired, Wireless/Battery-Operated, Smart/IoT-Connected) • By Installation Type (Ceiling-Mounted, Wall-Mounted) • By Application (Residential, Commercial, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Johnson Controls International PLC, Siemens AG, Robert Bosch GmbH, Kidde (Carrier Global Corporation), First Alert (Resideo Technologies Inc.), Google LLC (Nest Protect), Hochiki Corporation, Eaton Corporation PLC, Apollo Fire Detectors Ltd., ABB Ltd., FireAngel Safety Technology Group PLC, X-Sense Innovations Co. Ltd., Halma plc, Gentex Corporation, Ei Electronics Ltd., Universal Security Instruments Inc., NAPCO Security Technologies Inc., Schneider Electric SE, Panasonic Corporation |

Frequently Asked Questions

The Smoke Alarm Market is expected to grow at a CAGR of 7.43% from 2026 to 2035.

The Smoke Alarm Market was valued at USD 2.52 Billion in 2025.

The primary growth factors are global expansion of mandatory residential smoke alarm installation regulations.

The photoelectric segment dominated the Smoke Alarm Market with 42.35% share in 2025.

North America dominated the Smoke Alarm Market in 2025.

Get in Touch