Structural Heart Imaging Market Report Scope & Overview:

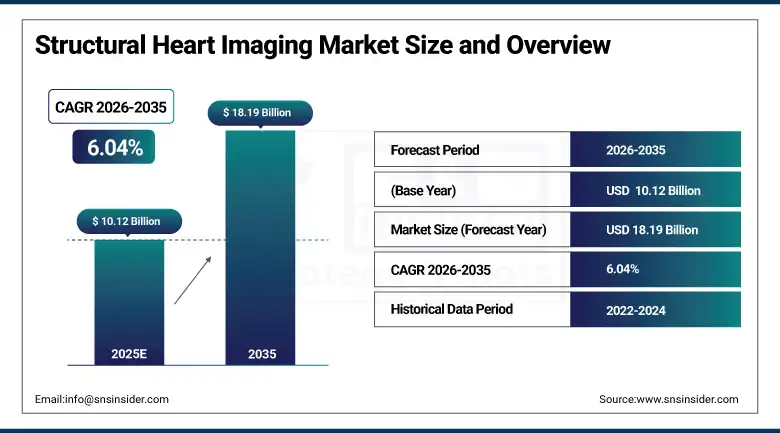

The Structural Heart Imaging Market size is estimated at USD 10.12 Billion in 2025 and is expected to reach USD 18.19 Billion by 2035, growing at a CAGR of 6.04% over the forecast period of 2026–2035.

The global structural heart imaging market has been exhibiting steady growth in recent years owing to the rising prevalence of structural heart diseases, increasing adoption of minimally invasive cardiac procedures, and advancements in diagnostic imaging technologies. Structural heart imaging is an essential tool for visualization and assessment of cardiac structure, the diagnosis of congenital and acquired heart valve disease, and for planning intricate interventional procedures. The increasing prevalence of diseases like aortic stenosis, mitral regurgitation and atrial septal defects has generated a need for accurate imaging techniques such as echocardiography, cardiac CT, MRI and nuclear imaging. In this competitive environment, healthcare systems globally are adopting advanced imaging technologies to augment accuracy in procedures and improved patient outcomes in cardiology workflows.

The increasing adoption of transcatheter structural heart procedures including TAVR, TMVR, and LAAC has fundamentally augmented the need for multimodality imaging platforms that can facilitate diagnosis, procedural planning, and post-procedural monitoring. Rising investments in healthcare infrastructure, rising adoption of AI-enabled imaging analysis and increasing partnerships & collaboration between device manufacturers and imaging technology providers are further impacting on competitive trends. Also, ongoing work on 3D echocardiography, real-time imaging systems and hybrid operating rooms have further allowed cardiologists to carry out such highly complicated procedures.

In February 2025, a major cardiovascular imaging consortium reported that the adoption of advanced multimodality cardiac imaging for structural heart interventions increased by 28% globally compared with the previous year, reflecting the growing clinical importance of imaging technologies in structural heart disease management.

Structural Heart Imaging Market Size and Forecast:

-

Market Size in 2025: USD 10.12 Billion

-

Market Size by 2035: USD 18.19 Billion

-

CAGR: 6.04% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Structural Heart Imaging Market - Request Free Sample Report

Structural Heart Imaging Market Trends:

-

Growing adoption of multimodality imaging techniques combining echocardiography, CT, and MRI for comprehensive assessment of structural heart diseases.

-

Rapid advancements in 3D and 4D echocardiography technology enabling detailed visualization of cardiac valves and structural abnormalities.

-

Increasing integration of artificial intelligence algorithms to assist cardiologists in automated image interpretation and clinical decision support.

-

Rising demand for real-time imaging guidance during transcatheter structural heart procedures such as TAVR and TMVR.

-

Expansion of hybrid catheterization laboratories equipped with advanced imaging systems for complex structural heart interventions.

-

Growing clinical use of cardiac CT imaging for procedural planning and anatomical evaluation prior to transcatheter valve replacement.

-

Development of high-resolution imaging technologies that improve visualization of cardiac structures and enhance procedural safety.

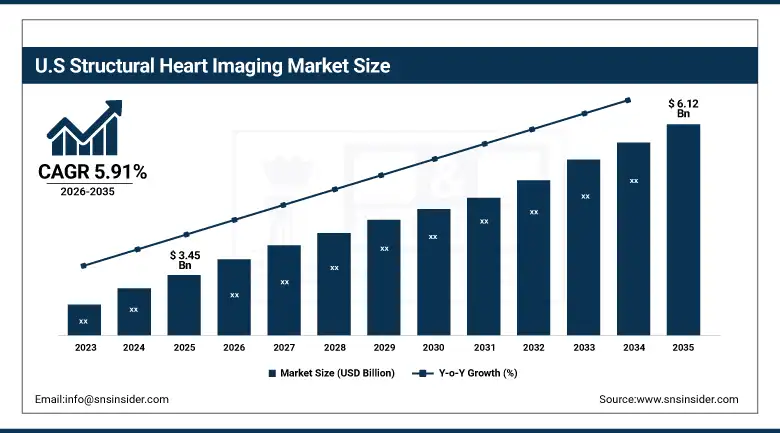

The U.S. Structural Heart Imaging Market is estimated at USD 3.45 billion in 2025 and is expected to reach USD 6.12 billion by 2035, growing at a CAGR of 5.91% from 2026-2035. The United States holds a significant share of the global market owing to the presence of advanced healthcare infrastructure, high adoption of minimally invasive cardiac procedures, and strong investments in cardiovascular imaging technologies. The widespread use of cardiac CT, MRI, and echocardiography in clinical cardiology practices and the presence of leading medical imaging technology companies have accelerated the development and adoption of next-generation structural heart imaging platforms.

Structural Heart Imaging Market Growth Drivers:

-

Rising Prevalence of Structural Heart Diseases Driving Demand for Advanced Imaging Solutions

Rising incidence of structural heart diseases globally is one of the key driver fuelling the growth of structural heart imaging market. Accurate image-based evaluation is essential for early diagnosis and guidance of management in the treatment of heart disease, including aortic stenosis, mitral valve prolapse, tricuspid regurgitation, and congenital heart defects. Imaging technologies for structural heart procedures enable cardiologists to see, in great detail, the valves, chambers, and surrounding anatomy, to help them decide on the most effective treatment.

Additionally, the growing elderly population is a key factor in the rising prevalence of degenerative valve diseases needing model imaging and interventional therapies. Consequently, there is significant capital investment by healthcare providers towards high-resolution anatomical visualization and functional assessment of cardiac structure using advanced imaging technology. In addition, increasing the number of structural heart programs in hospitals and specialty cardiac centers continues to drive demand for advanced imaging solutions.

For example, in March 2025, a leading cardiovascular hospital network reported a 35% increase in structural heart procedures performed with multimodality imaging guidance, highlighting the growing reliance on advanced imaging technologies in modern cardiology.

Structural Heart Imaging Market Restraints:

-

High Cost of Advanced Imaging Systems and Limited Accessibility in Developing Regions

High price paired with advanced structural heart imaging technologies is the main challenge for future growth of the market. The high cost of sophisticated imaging systems like cardiac CT scanners, MRI systems, and hybrid catheterization laboratories associated with capital investment may limit their acceptability among smaller healthcare facilities and hospitals in developing regions. Also, the maintenance costs, need of infrastructure as well as special training for health care professionals add up costs of operations.

The second challenge is the lack of trained imaging specialists who can interpret complex cardiac imaging data and guide structural heart procedures. This is especially true in developing economies where specialist cardiology access and complex imaging infrastructure are still lacking. Thus, the healthcare systems need to invest in train programmes & technologies that can undoubtedly facilitates imaging workflows to make accessibility easier.

Structural Heart Imaging Market Opportunities:

-

Technological Innovations in Imaging Platforms Creating New Market Opportunities

Growth Opportunity in the Structural Heart Imaging Market Owing to Advancement of Imaging Platforms Continued Highest Volume of Technological Growth Recent advancements in high-resolution imaging technologies, in vivo 3D visualization tools, and artificial intelligence image analysis systems are revolutionizing the diagnosis and management of structural heart diseases. Such innovations provide physicians with high-resolution anatomical and functional information, essential for the development of a proper stratified approach to complex transcatheter procedures.

Moreover, the use of artificial intelligence and machine learning algorithms in cardiac imaging systems has enhanced diagnostic precision while decreasing the interpretation time. AI-based software tools automate lesion detection, quantification of cardiac structures and guiding the clinician towards the best therapy. Based on the trend of imaging technology companies working with cardiovascular device manufacturers on a greater scale to enable integrated imaging solutions to allow for next-generation structural heart interventions, we expect the pace of development of these solutions to increase further.

For instance, in January 2025, a leading medical imaging company introduced an AI-assisted cardiac CT analysis platform capable of automatically evaluating valve anatomy and predicting procedural outcomes for transcatheter valve replacement procedures.

Structural Heart Imaging Market Segment Analysis:

-

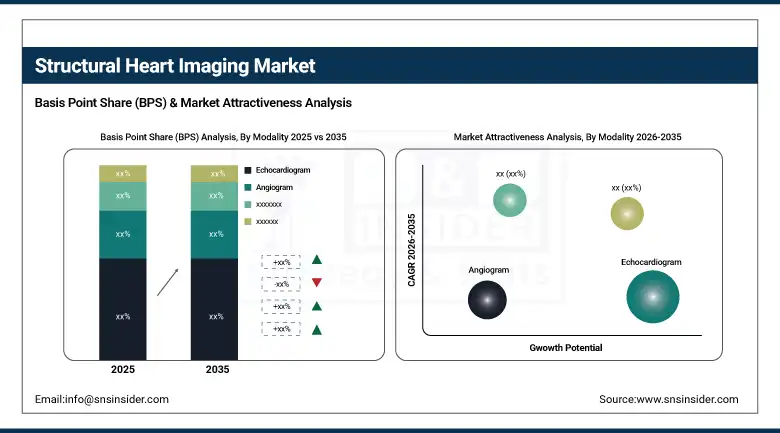

By modality, echocardiogram accounted for the largest share of 39.48% in 2025, while the CT imaging segment is anticipated to exhibit the fastest growth at a CAGR of 7.32%.

-

By application, diagnostic imaging dominated the market with a revenue share of approximately 63.26% in 2025, while interventional cardiology is expected to register the highest CAGR of 6.87% during the forecast period.

-

By procedure, transcatheter aortic valve replacement (TAVR) held the highest market share of around 34.75% in 2025 due to the increasing adoption of minimally invasive valve replacement procedures.

-

By end user, hospitals & clinics led the market with a share of 61.84% in 2025, while ambulatory surgical centers are projected to grow at the fastest CAGR of 6.55% between 2026 and 2035.

By Modality, Echocardiogram Dominates the Market While CT Imaging Shows Strong Growth

In 2025, the segment of echocardiogram accounted for the largest market share of around 39.48% owing to its commonly used as the primary imaging modality for the evaluation of any structural heart defect. Echocardiography provides a real-time image of cardiac structures, so it is an excellent modality to determine the structural abnormalities of valves, assess overall heart function, and guide interventional procedures. Continuous advancements in 3D and transesophageal echocardiography technology have revolutionized clinicians' visualization of complex cardiac anatomy.

Among the imaging types, cardiac CT imaging is expected to grow segmented over the forecast, at a CAGR of 7.32%. Segment growth is driven by the increasing adoption of CT imaging for pre-procedural planning of transcatheter valve replacements, which requires comprehensive anatomical visualization of cardiac structures.

By Application, Diagnostic Imaging Leads While Interventional Cardiology Expands Rapidly

In 2025, the structural heart imaging market was dominated by the diagnostic imaging segment, which contributed to ~63.26% to the overall share in terms of revenue. Segment growth is attributed to high demand for precise imaging methods to diagnose structural heart diseases in early stages. Techniques in diagnostic imaging are an important part of cardiac abnormality diagnosis and assessing disease state.

During the forecast period from 2026 to 2035, the interventional cardiology segment is expected to grow rapidly with a CAGR of 6.87%. With the increasing number of minimally invasive procedures (TAVR, TMVR, and LAAC) performed in the cardiac cath lab, there is a growing demand for advanced imaging systems that can deliver real-time guidance in complex cardiac interventions.

By End User, Hospitals & Clinics Dominate the Market

In 2025, hospitals & clinics held the largest revenue share of more than 61.84% in the structural heart imaging market. Hospitals with competitive advanced imaging infrastructure, specialized cardiology departments and hybrid operating rooms can perform complex structural heart procedures in an efficient manner. Moreover, increasing investments in cardiovascular centers and advanced diagnostic facilities are complementing the segmental growth.

Ambulatory surgical centers will be growing steadily as the focus moves towards outpatient cardiac procedures, and compact imaging systems will promote minor surgical procedures in ambulatory settings around the globe.

Structural Heart Imaging Market Regional Highlights:

North America Structural Heart Imaging Market Insights:

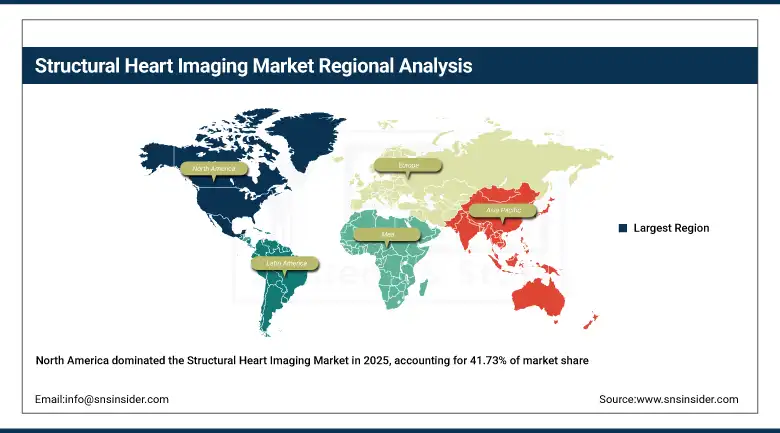

North America accounted for the largest share of the global structural heart imaging market with a revenue share of 41.73% in 2025. The presence of advanced healthcare infrastructure, a high volume of structural heart procedures, and early adoption of innovative imaging technologies are key factors driving market growth in the region. The United States plays a dominant role due to strong investments in cardiovascular research, advanced imaging facilities, and the presence of leading medical device companies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Structural Heart Imaging Market Insights:

Based on Region, the PR Market is segmented into North America, Europe, Asia-Pacific and Rest of the World. North America held the largest regional market for structural heart imaging due to increasing cardiovascular diseases, and well established to advanced cardiac imaging modalities across the region coupled with rapidly ageing population. Europe is the second largest regional market for structural heart imaging market. Market growth in the region is supported by government initiatives to improve cardiovascular treatment and the existence of special cardiac centers.

Asia Pacific Structural Heart Imaging Market Insights:

Asia Pacific is expected to be the fastest-growing regional market with a CAGR of 7.12% over the forecast period. On the other hand, the growing burden of cardiovascular diseases, increasing healthcare expenditure, and rapid healthcare infrastructure development in China, India, and Japan will pave way for the growth of the regional market in the future.

Latin America and Middle East & Africa Structural Heart Imaging Market Insights:

The Latin America and Middle East & Africa structural heart imaging market is slowly integrating to the structure due to betterment in healthcare infrastructure and awareness of advanced cardiac imaging technology. This trend is anticipated to propel future growth in the market across these regions as governments and healthcare organizations are emphasizing to increase access to specialized cardiology services and advanced cardiac diagnostic technologies.

Structural Heart Imaging Market Competitive Landscape:

Launched in 1994 (from General Electric´s healthcare division) GE HealthCare is a USD 19 billion global medical technology and digital solutions innovator. They are located in Finland and their products include: diagnostic imaging, patient monitoring, ultrasound, and digital healthcare solutions. GE Healthcare develops advanced imaging systems such as MRI, CT, ultrasound, and molecular imaging technologies that enable early disease detection, precision diagnostics, and better clinical outcomes.

-

In Nov 2025, GE HealthCare introduced new AI-enabled imaging and diagnostic solutions aimed at improving workflow efficiency, enhancing clinical decision-making, and expanding access to advanced medical imaging technologies across global healthcare systems.

Founded in 1847, Siemens Healthineers is a global leading medtech company headquartered in Germany, focusing in the areas of medical imaging, laboratory diagnostics, as well as advanced therapy solutions. Its innovative systems are used to create MRI, CT scanners, ultrasound equipment, digital diagnostic platforms, and much more to make diagnosis precision medicine and management of the patient more manageable.

-

In Oct 2025, Siemens Healthineers expanded its portfolio of AI-powered imaging and diagnostic solutions, supporting healthcare providers with advanced technologies designed to improve diagnostic efficiency and patient outcomes.

Royal Philips, established in 1891, is a global market leader in Health technology with the development of diagnostic imaging, patient monitoring and ultrasound, as well as connected healthcare solutions through Philips Healthcare. The firm provides innovative medical devices and digital health platforms that deliver precision diagnosis, imaging-guided therapy, and remote monitoring to patients. Philips Healthcare aims to draw synergy between AI, analytics and cloud tech and then integrate into its clinical-collaboration environment to enable the mobile health care across the hospital, clinic and home-care environments of the world.

-

In Sept 2025, Philips Healthcare launched new integrated imaging and digital health solutions designed to enhance clinical decision support, streamline hospital workflows, and expand access to advanced diagnostic technologies.

Structural Heart Imaging Market Key Players:

-

GE HealthCare

-

Siemens Healthineers

-

Philips Healthcare

-

Canon Medical Systems

-

Fujifilm Holdings Corporation

-

Hitachi Medical Systems

-

Samsung Medison

-

Mindray Medical International

-

Edwards Lifesciences

-

Abbott Laboratories

-

Boston Scientific Corporation

-

Medtronic plc

-

Terumo Corporation

-

LivaNova PLC

-

Bracco Imaging

-

Circle Cardiovascular Imaging

-

Pie Medical Imaging

-

Toshiba Medical Systems

-

Ziosoft Inc.

-

Arterys Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.12 Billion |

| Market Size by 2035 | USD 18.19 Billion |

| CAGR | CAGR of 6.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Modality (Echocardiogram, Angiogram, CT, MRI, Nuclear Imaging, Other Modalities)• By Application (Diagnostic Imaging, Interventional Cardiology) • By Procedure (Transcatheter Aortic Valve Replacement (TAVR), Surgical Aortic Valve Replacement (SAVR), Transcatheter Mitral Valve Repair (TMVR), Left Atrial Appendage Closure (LAAC), Tricuspid Valve Replacement and Repair) • By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Diagnostic Imaging Centers, Other End Use) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | GE HealthCare, Philips Healthcare, Siemens Healthineers, Canon Medical Systems, Hitachi Medical Systems, Fujifilm Holdings Corporation, Mindray Medical International, Samsung Medison, Neusoft Medical Systems, Toshiba Medical, Esaote , Edan Instruments, Chison Medical Technologies, SonoScape , Koninklijke Philips N.V. , GE Vivid, Shimadzu Corporation, Analogic Corporation, B-K Medical, Fukuda Denshi |

Frequently Asked Questions

North America dominated the Structural Heart Imaging Market in 2024.

The Interventional Cardiology segment dominated the Structural Heart Imaging Market in 2024.

Rise in awareness of animal health is also one of the key factors for the growth of the Structural Heart Imaging Market.

The Structural Heart Imaging Market size was USD 9.54 billion in 2024 and is expected to reach USD 15.09 billion by 2032.

The Structural Heart Imaging Market is expected to grow at a CAGR of 6.04% from 2025-2032.

Get in Touch