T-cell Lymphoma Market Report Scope & Overview:

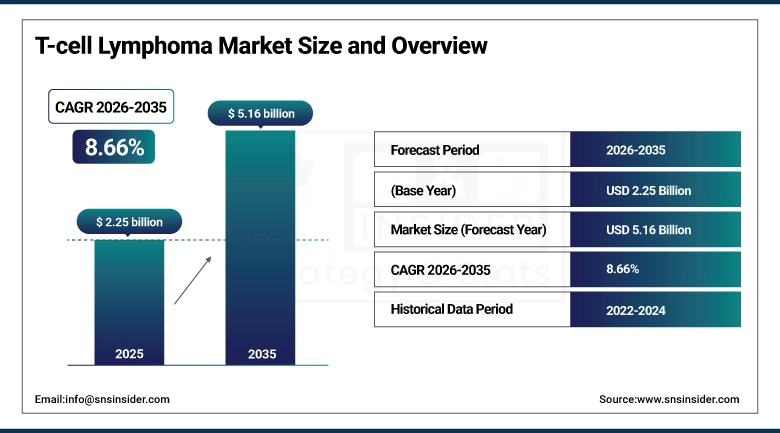

The T-cell Lymphoma Market size was estimated at USD 2.25 Billion in 2025 and is expected to reach USD 5.16 Billion by 2035 and grow at a CAGR of 8.66% over the forecast period of 2026-2035.

The global T-cell Lymphoma market is expanding due to the increasing incidence of the disease and emerging technologies. As growing numbers of people are diagnosed, what you seek are effective and “aggressive” treatment options. Meanwhile, advancements including targeted therapies, immunotherapies, and novel diagnostics are enhancing patient outcomes and the rise of treatment. AI in drug development and personalized medicine. It is noted that AI is elevating the precision and efficiency of treatment.

For instance, in March 2025, WHO reported a 5.1% global rise in non-Hodgkin lymphoma cases, with T-cell lymphomas comprising 10–15%, especially rising in Asia and North America.

T-cell Lymphoma Market Size and Forecast:

-

Market Size in 2025: USD 2.25 Billion

-

Market Size by 2035: USD 5.16 Billion

-

CAGR: 8.66% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On T-cell Lymphoma Market - Request Free Sample Report

T-cell Lymphoma Market Trends:

-

Rising incidence of T-cell lymphomas is driving demand for targeted therapies.

-

Growing adoption of monoclonal antibodies, immunotherapies, and combination treatment regimens is boosting market growth.

-

Expansion of clinical trials and ongoing R&D for novel drugs is enhancing treatment options.

-

Increasing awareness and early diagnosis initiatives are improving patient outcomes and therapy uptake.

-

Advancements in precision medicine and personalized treatment approaches are shaping market trends.

-

Supportive regulatory approvals and inclusion in treatment guidelines are facilitating wider adoption.

-

Collaborations between pharmaceutical companies, biotech firms, and healthcare providers are accelerating innovation and global market penetration.

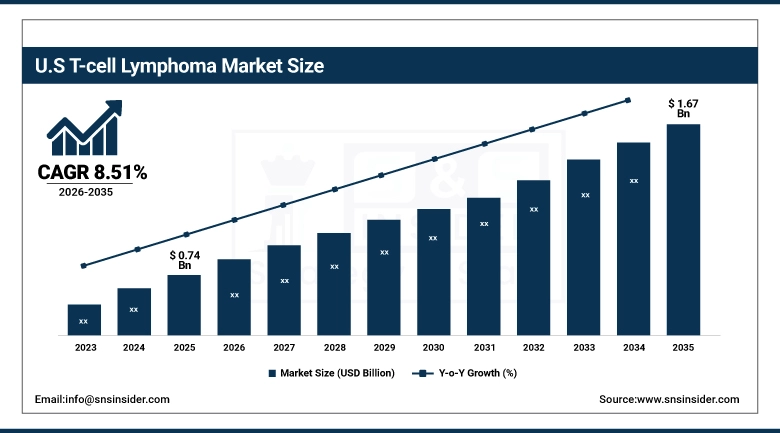

The U.S. T-cell Lymphoma Market was valued at USD 0.74 billion in 2025 and is expected to reach USD 1.67 billion by 2035, growing at a CAGR of 8.51% from 2026 to 2035.

The U.S. leads the T-cell Lymphoma market, driven by the strong biotech innovation environment, excellent R&D infrastructure, high expenditure on innovation, and swift approval for new compounds. Targeted therapies are being developed based on advanced new technologies, including CAR-T, AI, and gene editing.

For instance, in April 2025, IN 2024, the BIO Industry Report revealed that U.S. biotech firms contributed 41% of global oncology R&D spending in 2024, with a strong focus on T-cell lymphoma innovation.

T-cell Lymphoma Market Growth Drivers:

-

Increasing Prevalence of Autoimmune Disorders Driving the T-cell Lymphoma Market Growth

The rising incidence of autoimmune diseases is one of the major drivers for the T-cell Lymphoma market. Autoimmune diseases create an environment of immune dysregulation and chronic inflammation, increasing the likelihood of T cell malignant transformation. There are also shared genetic risk factors and overlap in treatments that link the two. With the growing prevalence of autoimmune diseases globally, the at-risk population increases and so does demand for, and the size of the T-cell Lymphoma market as it gains market share by offering innovative, immunity-targeted therapies.

For instance, in May 2025, NIH reported a 6.7% rise in autoimmune disease prevalence in the U.S. in 2024, linking increased cases to higher T-cell lymphoma risk.

T-cell Lymphoma Market Restraints:

-

High Initial R&D Costs, Restraining the T-cell Lymphoma Market

Rising initial R&D expenditure is the major factor inhibiting the growth of the T-cell Lymphoma market due to financial and technological barriers to entering the market. The development of new therapies is costly and requires specialized skills to create, with a long process filled with multiple regulatory hurdles and uncertainties. These are barriers to competition that allow bigger, better-resourced, and more scaled players to dominate. As a result, market entry is tough, hindering innovation while subsequently impacting the global T-cell Lymphoma market share.

For instance, in May 2025, Deloitte reported that the average cost to develop an oncology drug rose to $2.9 billion in 2024, with T-cell lymphomas among the most expensive categories.

T-cell Lymphoma Market Segment Analysis:

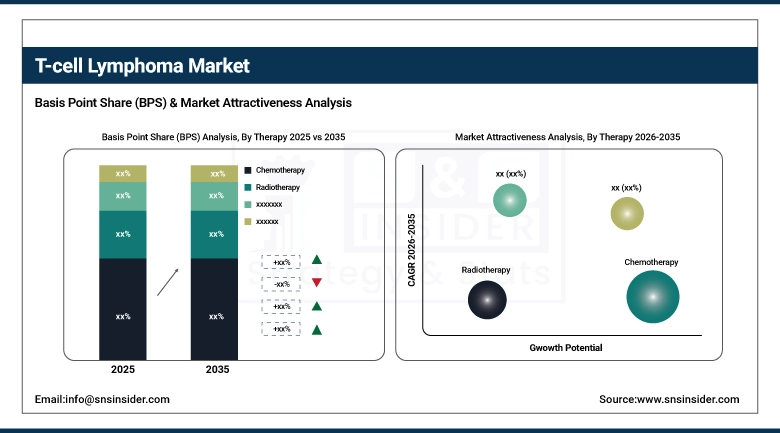

By Therapy

In 2025, the Chemotherapy segment controlled the global T-cell Lymphoma Market share, owing to its unquestioned position as the first-line therapy, particularly for aggressive subtypes, including PTCL and lymphoblastic lymphoma. The availability of the drug, low cost, and its place in standard treatment protocols contribute to its continued use. Even with new treatments, chemotherapy is still necessary for disease management, particularly in low and middle-income areas, and continues to maintain a sizeable part in the global T-cell lymphoma market share.

The Immunotherapy is the fastest-growing segment in the T-cell Lymphoma industry, as it is a selective therapy with increased survival and demonstrated efficacy in the treatment of relapsed or resistant cases. Therapies, including monoclonal antibodies and immune checkpoint inhibitors are becoming increasingly popular. Increased R&D investments, FDA approvals, and personalized therapeutic strategies are fueling the market.

By Type

Peripheral Drugs were the dominant segment in the T-cell Lymphoma Market analysis, with a market share of 67.86% share in 2025, owing to their extensive use for treating Peripheral T-cell Lymphoma. These agents are directed at unique T-cell markers and are associated with better response and less toxicity. Among key drivers are the increasing incidence of PTCL, the growing number of targeted therapies cleared for PTCL, and a growing presence of clinical research. This predominance adds a significant value to the overall T-cell Lymphoma Market share in the global oncology therapeutics industry.

The Lymphoblastic is emerging as the fastest growing segment in the T-cell Lymphoma Market trend, with a CAGR of 9.00%, driven by an aggressive nature and an increase in prevalence in adolescents and young adults. Treatment is in high demand due to the developments in high-intensity chemotherapy regimens, early diagnosis, and the care of pediatric oncology. So, are an increasing activity of clinical trials and targeted drug development.

T-cell Lymphoma Market Regional Analysis:

North America T-cell Lymphoma Market Insights

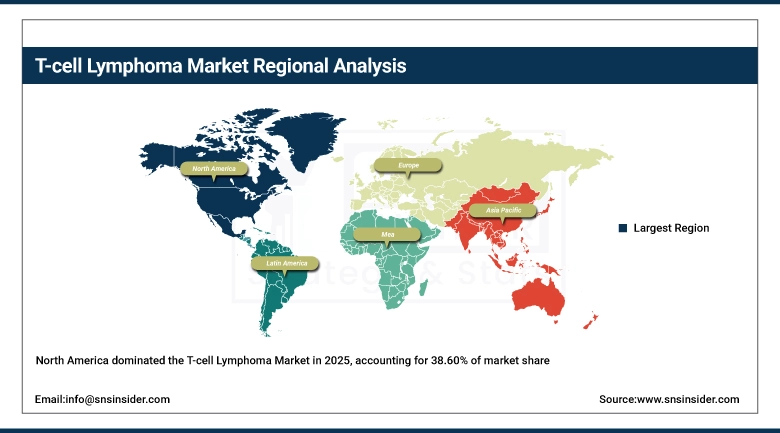

In 2025, the North American region dominated the T-cell Lymphoma industry and accounted for 38.60% of the overall revenue share, owing to extensive awareness, and early adoption of novel treatments, including CAR-T cell therapies and monoclonal antibodies. The presence of major pharmaceutical companies, well-established clinical research networks, and a strong regulatory backing from the FDA allows for rapid drug development and approvals. Further, high health care spending and access to specialised oncology centres favour widespread treatment availability.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe T-cell Lymphoma Market Insights

Europe accounts for a significant T-cell Lymphoma market share, attributed to robust public healthcare systems, increasing lymphoma awareness and growing availability of advanced treatments. The area enjoys favorable EMA regulations, increased clinical trials, and early acceptance of targeted and immunotherapies. Moreover, high diagnosis rates and investment in oncology infrastructure also contribute to ongoing innovation.

Asia Pacific T-cell Lymphoma Market Insights

The Asia Pacific region is projected to grow with the fastest CAGR of 9.16% over the forecast period, owing to the increasing incidence and development of medical care facilities and awareness about hematologic malignancy. Some of the emerging economies, including China, Japan, South Korea, and India, are spending massively on oncology services, diagnostics, and research. It is a push for newer and more expensive treatments, as new targeted drugs and immunotherapies become more readily available and researchers develop more treatments in clinical trials.

Middle East & Africa and Latin America T-cell Lymphoma Market Insights

The Middle East, Africa, and Latin America hold the lowest to moderate shares in the T‑cell Lymphoma market. Growth in these regions is driven by expanding healthcare infrastructure, increasing cancer awareness, government funding, and partnerships with international providers, improving access to diagnostics and therapies. However, high treatment costs, limited specialists, restrictive healthcare budgets, and rural inaccessibility continue to hinder widespread adoption, though market expansion remains positive.

T-cell Lymphoma Market Competitive Landscape:

Takeda Pharmaceuticals is a global biopharmaceutical company focused on oncology, hematology, gastroenterology, and rare diseases. Its oncology division emphasizes targeted therapies, immuno-oncology, and innovative clinical research in blood cancers. Takeda invests in translational research, clinical trials, and strategic partnerships to advance treatment options for hematologic malignancies, including lymphoma, while maintaining a commitment to patient access, safety, and global expansion of evidence-based therapies.

-

2025: Discontinued its cell therapy R&D, including gamma delta T‑cell platforms, and will seek partners to advance cancer immunotherapy programs, impacting future lymphoma cell therapy efforts.

-

2024: Presented oncology and lymphoma clinical data at ASCO 2024, covering multiple blood cancers to optimize treatment approaches.

-

2023: Shared hematologic cancer and lymphoma research at ASH 2023, reinforcing commitment to hematologic malignancy treatment.

Bristol-Myers Squibb is a global biopharma leader specializing in oncology, immunology, cardiovascular, and fibrosis therapies. Its oncology portfolio emphasizes next-generation immunotherapies, including CAR‑T cell therapies, targeted agents, and combination approaches. BMS prioritizes clinical innovation, regulatory leadership, and global access to advanced cancer treatments, particularly in hematologic malignancies such as lymphoma, chronic lymphocytic leukemia, and marginal zone lymphoma.

-

2025: Received European Commission approval to expand use of Breyanzi® CAR‑T for adults with relapsed/refractory follicular lymphoma.

-

2025: Reported positive topline Breyanzi results in marginal zone lymphoma, strengthening its lymphoma portfolio.

-

2024: FDA approved Breyanzi for relapsed/refractory CLL or small lymphocytic lymphoma in adults.

-

2023: Presented strong Breyanzi data for follicular lymphoma and CLL at ASH 2023, highlighting deep, durable responses.

Novartis is a multinational pharmaceutical company with expertise in innovative therapies for oncology, hematology, ophthalmology, and gene therapy. In oncology, Novartis focuses on CAR‑T therapies, targeted small molecules, and immuno-oncology approaches to treat aggressive and relapsed hematologic malignancies. The company invests in global clinical trials, regulatory strategy, and scientific partnerships to advance treatment options for patients with lymphoma and other B‑cell malignancies.

-

2025: FDA approved Kymriah CAR‑T for adult patients with relapsed/refractory follicular lymphoma.

-

2025: Announced interim results from pivotal follicular lymphoma CAR‑T study, showing Kymriah meeting primary endpoint.

-

2025: Received positive CHMP opinion for Kymriah in relapsed/refractory follicular lymphoma in Europe.

-

2023: Ongoing CAR‑T lymphoma trials (e.g., Belinda study) advanced clinical research in aggressive B‑cell non-Hodgkin lymphoma.

Merck is a global healthcare company focused on innovative medicines, vaccines, and immunotherapies. Its oncology division emphasizes immuno-oncology, bispecific antibodies, and precision therapies for hematologic malignancies. Merck prioritizes clinical trials, regulatory approvals, and strategic acquisitions to expand its lymphoma and B‑cell malignancy pipeline, aiming to improve outcomes and patient access through combination therapies, checkpoint inhibitors, and next-generation targeted treatments.

-

2025: Initiated Phase 3 waveLINE‑010 trial evaluating zilovertamab vedotin + chemotherapy in untreated diffuse large B‑cell lymphoma.

-

2025: Announced KEYTRUDA approvals and ongoing trials for relapsed/refractory classical Hodgkin lymphoma.

-

2024: Acquired bispecific antibody CN201 for B‑cell malignancies, strengthening its hematologic oncology pipeline.

T-cell Lymphoma Market Key Players:

-

Takeda Pharmaceutical Company Limited

-

Bristol‑Myers Squibb Company

-

Novartis AG

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Merck & Co., Inc.

-

Hoffmann‑La Roche Ltd

-

Acrotech Biopharma

-

Citius Pharma

-

Chipscreen Biosciences

-

Innate Pharma

-

Daiichi Sankyo Company, Limited

-

Eisai Co., Ltd.

-

Genor Biopharma Co. Ltd

-

Genmab A/S

-

Seattle Genetics (Seagen Inc.)

-

Spectrum Pharmaceuticals, Inc.

-

Kyowa Kirin Co., Ltd.

-

Autolus Therapeutics PLC

-

Astellas Pharma Inc.

-

Soligenix Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.25 billion |

| Market Size by 2035 | USD 5.16 billion |

| CAGR | CAGR of 8.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Peripheral Drugs, Lymphoblastic) • By Therapy (Radiotherapy, Chemotherapy, Immunotherapy, Stem Cell Transplantation, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Takeda Pharmaceutical Company Limited, Bristol‑Myers Squibb Company, Novartis AG, Johnson & Johnson (Janssen Pharmaceuticals), Merck & Co., Inc., Hoffmann‑La Roche Ltd, Acrotech Biopharma, Citius Pharma, Chipscreen Biosciences, Innate Pharma, Daiichi Sankyo Company, Limited, Eisai Co., Ltd., Genor Biopharma Co. Ltd, Genmab A/S, Seattle Genetics (Seagen Inc.), Spectrum Pharmaceuticals, Inc., Kyowa Kirin Co., Ltd., Autolus Therapeutics PLC, Astellas Pharma Inc., Soligenix Inc. |

Frequently Asked Questions

North America led in 2025 with 38.6% revenue share, supported by advanced healthcare infrastructure, early adoption of CAR-T and monoclonal antibody therapies.

Peripheral T-cell lymphoma drugs dominated in 2025 with 67.86% share, owing to high incidence, targeted therapies, and extensive clinical research.

Growth is driven by rising prevalence of T-cell lymphomas, advancements in immunotherapy, targeted therapies, personalized medicine, and ongoing clinical R&D activities.

In 2025, the T-cell Lymphoma Market was valued at USD 2.25 billion, reflecting increasing diagnoses and demand for advanced therapies globally.

The market is projected to grow at a CAGR of 8.66% from 2026 to 2035, driven by rising incidence and adoption of targeted and immunotherapies.

Get in Touch