Whole Body Imaging Market Report Scope & Overview:

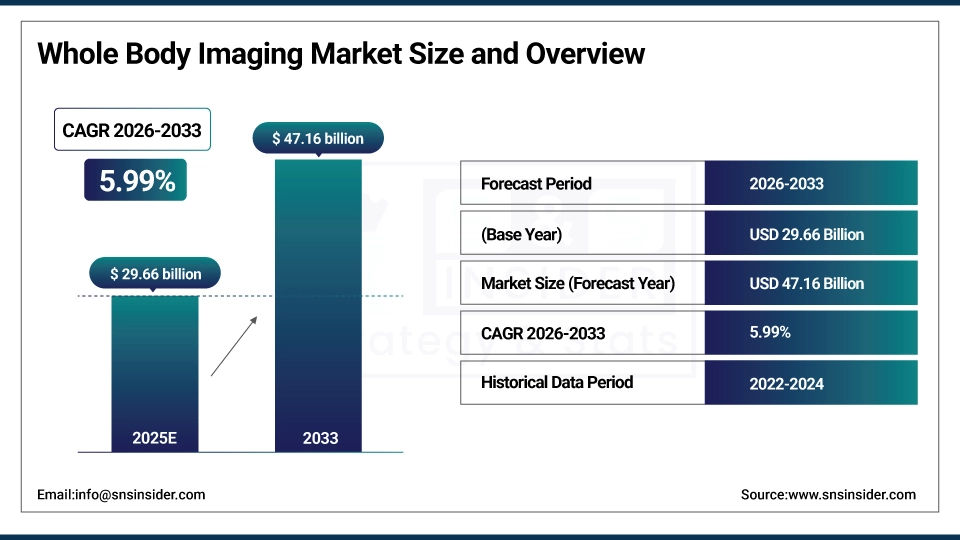

The Whole Body Imaging Market size was valued at USD 29.66 billion in 2025E and is expected to reach USD 47.16 billion by 2033, growing at a CAGR of 5.99% over the forecast period of 2026-2033.

Technological innovations, including hybrid imaging modality (PET/MRI, SPECT/CT), high field MRI, and AI-based imaging, are playing a vital role in accelerating real-time, accurate diagnosis and enhancing workflow, positively impacting the global whole-body imaging market trend. Now, as the geriatric population also faces chronic and degenerative diseases along with the growing ageing demographics, there is an escalating need for full-body scanning and its subsequent follow-ups. These are the drivers driving the uptake rates and thus a trend of whole-body imaging globally.

For instance, in March 2025, Siemens Healthineers reported that global adoption of PET/MRI and PET/CT systems grew 14% year-on-year, driven by oncology and neurodegenerative diagnostics.

Whole Body Imaging Market Size and Forecast:

-

Market Size in 2025E: USD 29.66 Billion

-

Market Size by 2033: USD 47.16 Billion

-

CAGR: 5.99% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Whole Body Imaging Market - Request Free Sample Report

Key Whole Body Imaging Market Trends

-

Advances in imaging modalities: Growth in PET-MRI, PET-CT, and hybrid scanners enabling comprehensive diagnosis.

-

AI & automation: Integration of AI for image reconstruction, anomaly detection, and workflow efficiency.

-

Personalized diagnostics: Imaging tailored to patient risk, genetics, and Oncology pathways.

-

Collaborative ecosystems: Partnerships among imaging centers, pharma, and AI firms for precision medicine.

-

Non-invasive innovations: Development of radiation-free or low-dose technologies for safer screening.

-

Regulatory & awareness support: Rising screening guidelines, reimbursement backing, and preventive healthcare adoption.

Whole Body Imaging Market Report Highlights

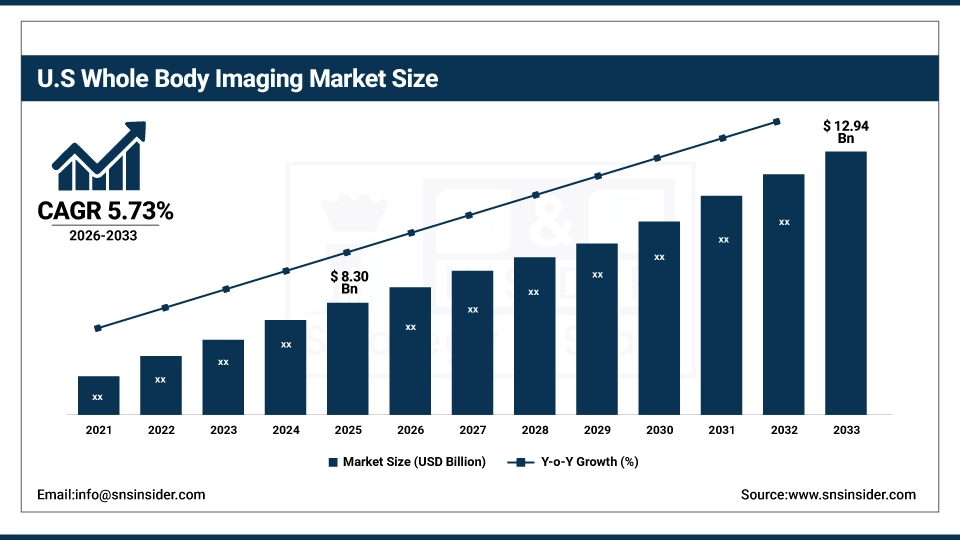

The U.S. whole body imaging market was valued at USD 8.30 billion in 2025E and is expected to reach USD 12.94 billion by 2033, growing at a CAGR of 5.73% over 2026-2033. The U.S. leads the whole-body imaging market, followed by the advanced healthcare sector, increased adoption of hybrid imaging systems (PET/MRI and PET/CT), the emergence of AI-assisted diagnostics tools, and the favorable reimbursement scenario. Furthermore, the significant number of geriatric populations living with chronic diseases and the early introduction of preventive screening programs are the key factors contributing to its large share in the U.S. and contributing to the largest regional market.

Whole Body Imaging Market Growth Drivers:

-

Expansion of Diagnostic Centers and Outpatient Facilities is Driving the Whole Body Imaging Market Growth

The increasing number of diagnostic centers and easy accessibility of the outpatient services are the factors boosting the global whole body imaging market share. Freestanding for-profit imaging centers, outpatient imaging facilities, and portable imaging all contribute to easy access, shorter waiting times, and a greater number of full-body scans. That pattern is particularly acute in dense living areas and fueling the spread and growth of the market.

For instance, in January 2025, Siemens Healthineers reported that over 120 new outpatient imaging centers were launched in North America and Europe, boosting the whole-body imaging market share.

Whole Body Imaging Market Restraints:

-

Radiation Exposure Concerns are Hampering the Whole Body Imaging Market Growth

The whole-body imaging market is hindered by concerns, including radiation exposure. Techniques including CT and PET scans expose subjects to ionizing radiation and raise safety concerns for patients, particularly children, the elderly, and other at-risk populations. This safety concern restricts repeat imaging, affects adoption in some markets, and requires more rigid standards for safety that may restrict market growth and overall service utilization.

Whole Body Imaging Market Opportunities:

-

AI-Driven Imaging Analytics Drive Future Growth Opportunities for the Whole-Body Imaging Market

The opportunity in AI driven imaging analytics is to help alleviate critical high machine utilization in whole body imaging while providing for earlier, more accurate diagnosis. AI improves image reconstruction, decreases scan times, and identifies subtle abnormalities earlier than previous approaches. It further enables automated reporting, predictive modelling, and precision oncology, enabling clinicians to tailor Oncology procedures and streamline the workflow, and reducing diagnostic errors.

For instance, in October 2024, Clinical trial data showed AI-enabled PET/CT boosted lesion detection sensitivity by 22%, enhancing accuracy and reliability in whole-body cancer screening diagnostics.

Key Whole Body Imaging Market Segment Analysis

-

By modality, magnetic resonance imaging (MRI) held the largest share of around 40.80%in 2025, and the computed tomography (CT) segment is expected to register the highest growth with a CAGR of 6.69%.

-

By application, the oncology segment dominated the market with approximately 45.60% share in 2025, while metastasis detection is expected to register the highest growth with a CAGR of 6.50%.

-

By procedure type, diagnostic imaging accounted for the leading share of nearly 62.28% in 2025, and is expected to register the highest growth with a CAGR of 6.21%.

-

By end user, the hospitals led the market with about 55.80% share in 2025, while the diagnostic imaging centers segment is forecasted to grow the fastest at a CAGR of 6.45%.

By Application, the Oncology Segment dominates, while the Metastasis Detection Segment Shows Rapid Growth

The oncology segment held the largest revenue share of approximately 45.60% in 2025, owing to its prevalence globally and the importance of imaging in early diagnosis, staging, treatment planning, and follow-up. Market drivers are advances in PET/CT and PET/MRI, AI-driven diagnostics, and an increase in the geriatric population. On the other hand, the metastasis detection segment is predicted to grow at the strongest CAGR of approximately 6.50% during 2026-2033, owing to the growing demand for early detection of cancer dissemination and accurate treatment scheduling. Factors include increasing cancer cases, advances in PET/CT and PET/MRI, and AI-assisted imaging for precise detection of lesions.

By Modality, Magnetic Resonance Imaging (MRI) Leads the Market, While Computed Tomography (CT) Registers Fastest Growth

The magnetic resonance imaging (MRI) segment accounted for the highest revenue share of approximately 40.80% in 2024, owing to the essential role in the early identification of disease, staging of cancer, and monitoring therapy. Market drivers include the prevalence of chronic disease, PET/MRI technology, AI-enabled imaging, and older population growth. In comparison, the computed tomography (CT) segment is anticipated to achieve the highest CAGR of nearly 6.69% during the 2026-2033 period, due to its fast-speed photography, high resolution, and non-invasive diagnosis. Market drivers are the increasing prevalence of cancer and cardiovascular diseases.

By Procedure Type, Diagnostic Imaging Lead, and Registers Fastest Growth

The diagnostic imaging accounted for the largest share of the whole body imaging market with about 62.28%, owing to its potential role in personalized medicine and patient monitoring. The factors driving the growth of this market are the growing use of AI and machine learning for accurate image interpretation and the increasing geriatric population. In addition, the E-Commerce development segment is slated to grow at the fastest rate with a CAGR of around 6.21% throughout the forecast period of 2026-2033, owing to the growing need for early diagnosis of diseases, rising cancer and cardiac cases, and growing adoption of hybrid modalities including PET/CT and PET/MRI.

By End User, Hospitals Lead, While the Diagnostic Imaging Centers Segment Grows the Fastest

The hospitals held the largest revenue share of around 55.80% in the whole body imaging market in 2025, owing to their well-established infrastructure, access to high-quality imaging tools, and complete diagnostic facilities. Furthermore, factors include a high number of patient admissions. On the flip side, the Diagnostic Imaging Centers segment, however, is projected to register the highest CAGR of around 6.45% during the forecast period of 2026 - 2033, owing to the rise of ambulatory services, cost, and the convenience of patients. Key drivers include increasing awareness of preventive healthcare and, proliferation of independent imaging centers.

Whole Body Imaging Market Regional Analysis:

North America Urine Testing Cups Market Insights

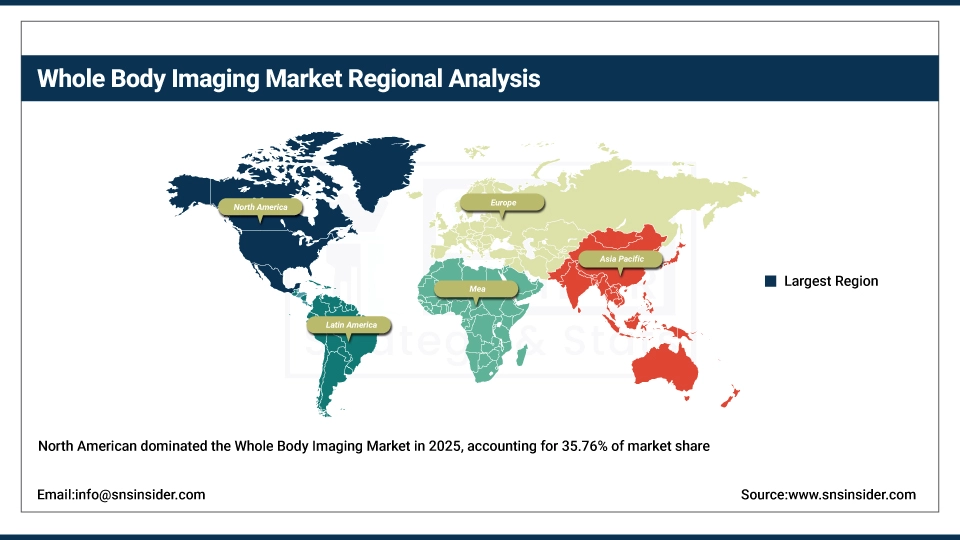

North America accounted for the highest revenue share of approximately 35.76% in 2024 of the whole body imaging market, owing to its robust healthcare system, early implementation of state-of-the-art imaging technology, and high healthcare expenditure. These factors include increasing preference for PET/CT, PET/MRI, and AI-based imaging techniques and the growing number of the geriatric population and rising incidence of chronic diseases, favorable reimbursement coverage, and government initiatives for preventive care. Much of which is supplemented by leading imaging system providers, mature diagnostic centers, and high public awareness, and North America holds the largest market share globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Urine Testing Cups Market Insights

Asia Pacific is the fastest-growing segment in the whole-body imaging market with a CAGR of 6.79%, as a result of the escalating expenditure on healthcare and healthcare infrastructure. Factors, including a rapid increase in population, a substantial geriatric population, a rise in the incidence of chronic diseases, including cancer and cardiovascular diseases, and a rise in awareness about preventive healthcare and the early diagnosis of diseases, are motivating the market.

Europe Urine Testing Cups Market Insights

Europe is the second-leading region in the whole body imaging market because of the developed healthcare infrastructure, higher adoption rate for advanced imaging technologies, and the strong regulatory framework. Factors including rising prevalence of chronic diseases, rapidly growing geriatric population, rising demand for PET/CT and MRI systems, increasing investment in the installation of advanced medical imaging modalities, and rise in the number of people undergoing early disease detection are some of the driving factors for the market growth. These factors together help to increase imaging procedure volumes and retain the substantial European market share globally.

Latin America (LATAM) and Middle East & Africa (MEA) Urine Testing Cups Market Insights

The Middle East & Africa are witnessing the growth of the whole body imaging market, supported by the burgeoning healthcare infrastructure, high health consciousness in the Gulf countries, and surging incidence of cancer. Adoption is driven in Latin America by Brazil and Mexico, with government-supported diagnostics programs and private sector investments. Increasing awareness and advancing imaging techniques, combined with international cooperation in building diagnostic capacity, are driving progress in both regions.

Competitive Landscape for the Whole Body Imaging Market:

GE HealthCare, as a global leader in diagnostic imaging, GE HealthCare specializes in AI-powered imaging features, hybrid technologies, and accurate diagnostics. Its advancements improve workflow efficiency, early diagnosis, and treatment for people everywhere.

-

In May 2024, introduced Revolution Apex Elite CT with AI-driven reconstruction, lowering radiation dose by 20% and improving oncology whole-body imaging precision for safer, faster diagnostics.

Siemens Healthineers leads the way in whole body imaging with PET/CT, MRI, and AI-enabled systems. It focuses on oncology and cardiovascular applications, enabling enhanced diagnostic accuracy, shorter scan time, and the adoption of precision medicine in the healthcare system globally.

-

In October 2024, a Clinical trial confirmed AI-powered PET/CT enhanced lesion detection by 22%, strengthening whole-body cancer screening accuracy and positioning Siemens as a leader in precision diagnostics.

Philips Healthcare is participating in the convergence of AI, cloud, and hybrid imaging for all-over imaging. The product’s emphasis on patient-centric care, process automation, and green technologies has led many of the world’s leading hospitals, diagnostic centres, and clinical trial facilities to integrate ASE reporting solutions.

-

In March 2025, the Expanded IntelliSpace AI Workflow Suite in Europe reduced radiology reporting errors by 30%, boosting efficiency and accuracy in oncology and cardiovascular whole-body imaging practices.

Whole Body Imaging Market Key Players:

Some of the whole body imaging market companies are:

-

GE Healthcare

-

Siemens Healthineers

-

Philips Healthcare

-

Canon Medical Systems

-

Fujifilm Holdings

-

Hitachi Medical Systems

-

Samsung Medison

-

Carestream Health

-

Hologic

-

Shimadzu Corporation

-

Esaote SpA

-

ICAD, Inc.

-

Stryker Corporation

-

Konica Minolta Healthcare

-

Neusoft Medical Systems

-

Mindray Medical International

-

Medtronic plc

-

Varian

-

Esaote North America

-

Zoncare Medical

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 29.66 billion |

| Market Size by 2033 | USD 47.16 billion |

| CAGR | CAGR of 5.99% From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Modality (Computed Tomography (CT), Magnetic Resonance Imaging (MRI),Nuclear Imaging, Other Modalities) • By Application (Oncology, Trauma and Emergency Care, Metastasis Detection, Full-Body Health Screenings) • By Procedure Type (Diagnostic Imaging, Treatment Planning, Monitoring & Follow-up) •By End User (Hospitals, Diagnostic Imaging Centers, Other End Users) |

| Regional Analysis/Coverage | "North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America)" |

| Company Profiles | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, Fujifilm Holdings, Hitachi Medical Systems, Samsung Medison, Carestream Health, Hologic, Shimadzu Corporation, Esaote SpA, ICAD, Inc., Stryker Corporation, Konica Minolta Healthcare, Neusoft Medical Systems, Mindray Medical International, Medtronic plc, Varian, Esaote North America, Zoncare Medical and other players. |

Frequently Asked Questions

North America dominated the Whole Body Imaging Market in 2025.

The Magnetic Resonance Imaging (MRI) segment dominated the Whole Body Imaging Market in 2025.

Expansion of Diagnostic Centers and Outpatient Facilities is Driving the High-Intensity Focused Ultrasound Market Growth.

The Whole Body Imaging Market size was USD 29.66 billion in 2025E and is expected to reach USD 47.16 billion by 2033.

The Whole Body Imaging Market is expected to grow at a CAGR of 5.99% over the forecast period.

Get in Touch