Agricultural Lubricant Market Analysis & Overview:

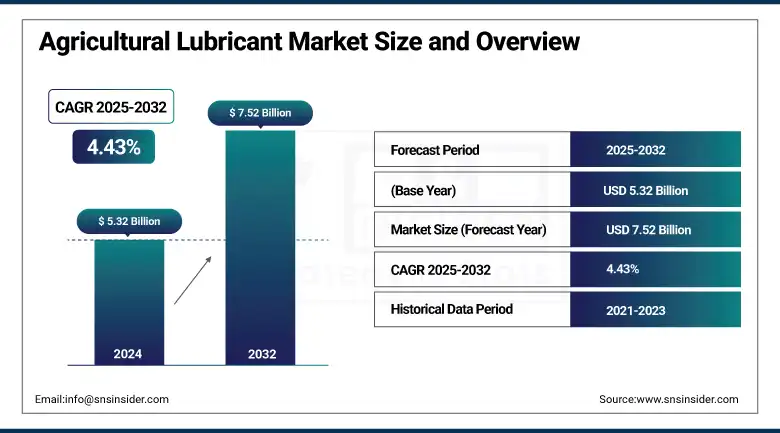

The Agricultural Lubricant Market size was valued at USD 5.32 billion in 2024 and is expected to reach USD 7.52 billion by 2032, growing at a CAGR of 4.43% over the forecast period of 2025-2032.

The agricultural lubricants market is going through transformation, and farm machinery lubricants are increasingly complemented by IoT-equipped sensors to monitor the condition of oil at any given time, which encourages a predictive maintenance approach and minimizes machine downtime. Agricultural lubricants manufacturers are enhancing their offerings with high-performance agricultural equipment oils and bio-based products to meet strict environmental regulations from the USDA BioPreferred Program. Adoption of precision agriculture and growing demand for equipment electrification are also driving factors for the market in agricultural lubricants. Meanwhile, some partnerships, such as John Deere testing out sensor-based lubricant monitoring, exemplify new prospects for the U.S. agricultural lubricants market outlook globally.

To Get more information On Agricultural Lubricant Market - Request Free Sample Report

-

U.S. sales of Ag tractors were down 11.3% while combine sales decreased 26.4% in 2020 compared with the previous year, the Association of Equipment Manufacturers reported December 31, 2024.

-

As of June 2021, there were more than 16,000 products featuring the USDA Certified Biobased Product label in the BioPreferred catalog, representing 139 categories of biobased products including applications for the Agricultural Lubricant Market.

-

Agricultural Lubricant Market Dynamics:

Drivers:

-

Integration of IoT-Based Lubrication Monitoring Systems Enhances Agricultural Equipment Efficiency

IoT smart sensors for lubricants in the farm equipment now give real-time oil-condition monitoring to help limit downtime and extend maintenance cycles for our farmers. According to the USDA in 2024, 70% of major U.S. farms implement autosteering and GPS-based systems. This integration encourages the economic use of oil, a service that is tailored made and it is a part of the agricultural lubricant market expansion. Performance-based agricultural machinery oils are formulated using these tools by the agricultural lubricants industries that improves equipment life and accuracy.

-

Expansion of Large-Scale U.S. Farms Boosts Agricultural Lubricant Market Growth

The rise of large-scale commercial farming escalates the demand for premium quality lubricants. In 2023, the USDA said more than 50% of row-crop acres in the U.S. were using digital tools, along with an increase in tractor and oil use. This is propelling the agricultural lubricants market size due to the requirement of efficient farm machinery lubricants, and agricultural lubricant and oil for combines, tractors, and sprayers that small and large farms need, promoting innovation among agricultural lubricants companies.

Restraints:

-

Volatility in Crude and Base Oil Prices Undermines Lubricant Profitability and Impedes Market Growth

The price of mineral oil-based lubricants is linked directly to the fluctuating price of crude oil. In January 2025, according to the Chemanalyst, U.S. base oil prices were flat despite higher crude costs. But any abrupt change would disrupt the Agricultural Lubricant Market Share as it heightens production costs and decreases margins. The smaller companies, in particular the producers of agricultural lubricants, are at risk, and this limits the big companies of the industry from investing in R&D of advanced formulations, leading to agricultural lubricant market growth.

-

Limited Rural Infrastructure Impedes Distribution of High-Performance Lubricants

The inability to reach out to high-quality farm machinery lubricant limits premium products in rural or developing regions, where a proper distribution channel and proper infrastructure exist. According to the Business Insider reports in May 2025, the disconnect from farmer access to improved products is primarily the result of poor transport and connectivity. This invariably restricts the widespread adoption of synthetic and bio-based oils, especially in hinterland regions, and restrains the agricultural lubricants market trends, obstructing agricultural lubricants market analysis and long-term regional expansion.

Agricultural Lubricant Market Segmentation Analysis:

By Product Type

Engine Oil dominated the agricultural lubricant market with a 43.2% share. The prominence of Engine Oil also reflects its role with high-horsepower tractors and combines, with high-shear-viscosity (gear) improvers providing excellent protection for heavily loaded engines. The Association of Equipment Manufacturers estimated that for December 2024, more than 68% of new US tractor deliveries called for high-end engine oils and longer service intervals (AEM, Dec 2024). Industry-leading groups like Shell and Exxon Mobil are taking advantage of these trends to launch advanced engine oil formulations that are used to meet stricter EPA emissions requirements and increased equipment hours.

Hydraulic Fluid is anticipated to witness the highest growth with a 5.32% CAGR from 2025 to 2032. Among the hydraulic fluids, synthetic hydraulic oils provide better viscosity stability under different load conditions, which is why they are favored. According to the USDA, in August 2023, 55% of larger U.S. farms used auto-downforce hydraulic systems for their production. FUCHS and TotalEnergies offered formulators in 2024 for low-foaming synthetic hydraulic fluids for precision steering and electro-hydraulic controls.

By Base Oil

In 2024, mineral oil dominated and accounted for a share of about 64.1% in the agricultural lubricant market. In this category, Group II resulted in a perfect balance between cost and performance. As of this year, the American Petroleum Institute estimated that Group I and II mineral oils made up approximately 65% of base-oil volumes. In late 2024, Valvoline and Chevron, as agricultural lubricants companies, provided NTF-2 specification mineral blends to tractor and combine companies with a compatible OEM warranty support mechanism, further boosting the dominance of mineral oil in real-world use.

Synthetic oil is expected to be the fastest-growing segment of base oil during the forecast period, with 5.0% CAGR. This segment gained from better low-temperature fluidity and thermal stability, driven by polyalphaolefin-based formulations. According to the USDA BioPreferred Program, certified synthetic-blend lubricants for farm equipment have increased by 15% compared to June 2021. The launch of PAO-rich oils from TotalEnergies and Phillips 66 in Q1 2024 drives the rapid adoption of synthetic oil across the U.S. tractors and combines, illustrating both performance trends and consumer preferences.

By Farm Equipment

Tractor applications continue to dominate the agricultural lubricant sector, accounting for 55.8% of the total share in 2024. The extensive hours row-crop models log in the fields drove consumption within Tractors. In 2023, average U.S. row-crop tractor service hours of 1,250 were reported by USDA ERS, which was 30% higher than the average service hours of non-row-crop units. Based on these requirements, manufacturers, such as John Deere and AGCO, developed their Farm Machinery Lubricants, promoting high-viscosity engine oils and gear lubricants designed for row-crop work. This row-crop equipment compatibility focus is prominently played through reinforcing the Tractor subsegment dominance and overall tractor segment leadership.

During the forecast period of 2025 to 2032, the combines farm equipment is the fastest growing segment, along with a robust CAGR. In the U.S., deliveries of rotary combines also climbed at a faster pace in December, up 25.3%, as reported by the Association of Equipment Manufacturers. Some companies, including Chevron and FUCHS, developed Agricultural Machinery Oils as multi-functional agricultural lubricants for use in rotary combines, covering transmission, hydraulic, and torque-converter systems. These developments consolidated the self-propelled rotary combines as market leaders and facilitated quick combine segment growth in all key producing regions.

By Sales Channel

Aftermarket held the largest market share of 58.3% in 2024 in the agricultural lubricant market. While in the aftermarkets, it was independent service centers and the farm co-ops who spearheaded distribution by way of localized support. According to the Equipment Dealers Association, 62% of the U.S. farmers bought lubricants through aftermarket channels for grouped-in maintenance packages in Q4 2024. Agricultural lubricants players, such as Schaeffer and Rymax, ensured stronger aftermarket networks by providing on-farm oil analysis and receiving just-in-time delivery, and empowering independent distributors to roll over rural areas, further enhancing equipment’s uptime, lead time, and uptime.

OEM channels is the fastest-growing segment, which is growing at the highest CAGR of 4.89% during the forecast period of 2025 to 2032. Factory fill extended life oil programs in the OEM space are predominantly driven by end-to-end warranty protection. CNH Industrial’s most recent 2024 Sustainability Report highlighted 18% year-on-year growth in deliveries of proprietary OEM lubricants. Deere and CNH introduced factory-fill oil packages with high-technology Agricultural Machinery Oils in new equipment during early 2025. These whole-package solutions also shortened the service cycle by 20%, thus rapidly expanding the OEM channel and greatly improving customer satisfaction.

Agricultural Lubricant Market Regional Outlook:

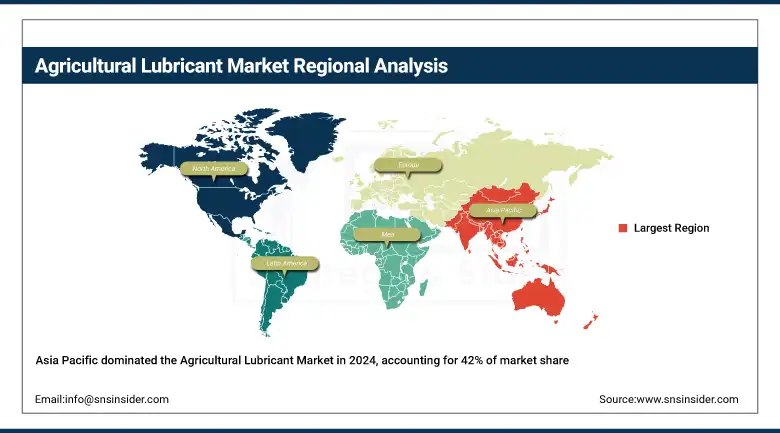

Asia Pacific dominated and held a major share of the agricultural lubricant market, accounting for approximately 42%, due to the rising mechanization. In India, mechanization is at a rate of 47%, and in China, it is 60% due to the government initiatives, such as India’s SMAM programme and increased farm incomes. The region already accounts for more than 40% of the world’s use of lubricants, driven by top gainers including rice, wheat, and oil seeds. IOC and Sinopec have been producing lubricants in the region to address this requirement locally. Many farmers are employing new multi-service oils for their tractors and combines. Increasing investments in rural infrastructure and growing high-yielding acreage in the APAC could propel the agricultural lubricant market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North American region emerged as the fastest-growing region with the highest CAGR of 5.13%. Increased demand is being fueled by a rapid embrace of advanced farm equipment (precision tractors and combines) and strong farm incomes and policies that are favorable to the farm sector. In the North American region, the U.S. led the market with USD 779.41 million and accounted for a market share of 67% in 2024. For instance, the U.S. 4-wheel-drive tractor sales increased by 9.4% in May 2024, and Canadian combine sales soared by 58.4%. Specialized tractor-grade lubricants have been introduced by the major oil companies. Overall, modernization, new investment incentives, and new product introductions point to ongoing strength in North American lubricant demand.

Europe is the second-largest regional market, accounting for 19.6% of the global market. Tractor registrations were only down ~4–5% in Germany and France in 2024, but total equipment stocks are still at very high levels. Restrictive EU regulations (EU Lubricants Ecolabel, for instance) and climate goals are giving an extra boost to biodegradable OME-endorsed oils. The major OEs (AGCO, Claas, CNH, etc.) work with oil manufacturers to innovate complex fuel formulations for Euro VI engines and multi-utility farm equipment. These sustainability criteria and OEM relationships are the foundation for Europe’s solid lubricant demand, even during cyclical farm income pressures.

LAMEA witnessed a rise in the demand for agricultural lubricants due to growing mechanization and crop productivity. Its farms are 75% mechanized, so it will be farming 12mt soybean oil in 2024 and 2025, while Argentina is into huge volume grain farming. This growth is backed by infrastructure improvements, credit programs, and enhanced lubricant capacity by Petrobras and YPF. In the Middle East & Africa, Egypt’s “New Delta” will turn 9,240 km² into agricultural land, while South Africa is renewing its machinery. Governments in the region are focusing on the development of agriculture, which is expected to increase the demand for agricultural lubricants and farm machinery oils throughout LAMEA.

Key Players:

The major competitors in the agricultural lubricant market include Shell plc, Exxon Mobil Corporation, TotalEnergies SE, Chevron Corporation, BP plc (Castrol), Valvoline Inc., FUCHS Petrolub SE, Phillips 66, PETRONAS Lubricants International, and Schaeffer Manufacturing Co.

Recent Developments:

-

September 2024: Maxol launched Agri-Max Plus Grease for agriculture and updated packaging for sustainability, aiming to meet high-performance and environmental standards in farming operations.

-

July 2023: Kramp partnered with Shell Lubricants to distribute agricultural lubricants across the U.K., improving farmers’ access to quality oils and reducing equipment downtime.

-

February 2023: Neste launched ReNew lubricants using renewable or re-refined base oils to support sustainable farming, targeting reduced emissions and fossil oil dependency.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.32 billion |

| Market Size by 2032 | USD 7.52 billion |

| CAGR | CAGR of 4.43% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Engine Oil, Transmission Oil, Hydraulic Fluid, Grease, Others) •By Base Oil (Mineral Oil, Synthetic Oil, Bio-Based) •By Farm Equipment (Tractors, Combines, Implements) •By Sales Channel (OEMs, Aftermarkets) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Shell plc, Exxon Mobil Corporation, TotalEnergies SE, Chevron Corporation, BP plc (Castrol), Valvoline Inc., FUCHS Petrolub SE, Phillips 66, PETRONAS Lubricants International, Schaeffer Manufacturing Co. |

Frequently Asked Questions

Key players in the Agricultural Lubricant Market include Shell, Exxon Mobil, Chevron, TotalEnergies, and Valvoline.

OEM channels are growing rapidly in the Agricultural Lubricant Market due to factory-fill programs and warranty-backed oil packages.

Engine oil led the Agricultural Lubricant Market in 2024 with a 43.2% share, driven by thermal stability and extended drain intervals.

IoT-enabled oil monitoring enhances uptime and maintenance, fueling innovation and efficiency in the Agricultural Lubricant Market.

The Agricultural Lubricant Market is projected to reach USD 7.52 billion by 2032, growing at a CAGR of 4.43% from 2025 to 2032.

Get in Touch