Biopesticides Market Report Scope & Overview:

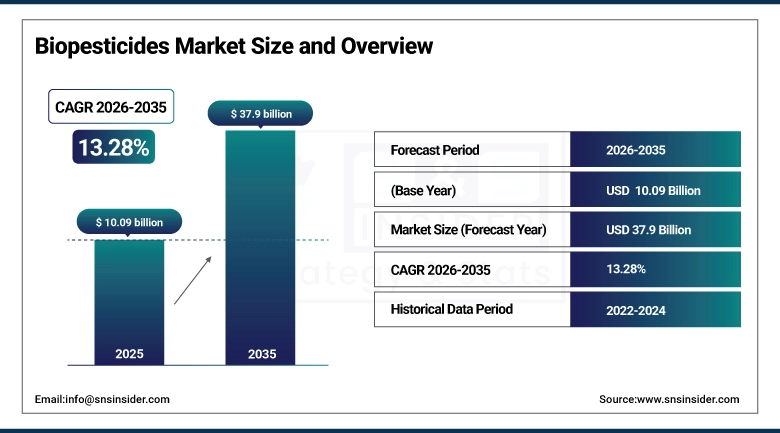

The Biopesticides Market was valued at USD 10.09 Billion in 2025 and is expected to reach USD 37.9 Billion by 2035, growing at a CAGR of 14.07% from 2026-2035.

Biopesticides Market are experiencing a commercial moment, two decades in the making. The combination of regulatory pressure on synthetic pesticides, consumer demand for residue-free produce, confirmed pesticide resistance in key pest populations, and real advancements in microbial formulation technology have combined to establish market conditions whereby biopesticides are no longer simply the compromise choice made by farmers when conventional chemistry is limited they are beginning to be the solution of choice when performance, residue profiles & supply chain sustainability requirements intersect. The range of pest biology covered by Bacillus thuringiensis (Bt) products, entomopathogenic fungi, entomopathogenic nematodes, semi chemicals for mating disruption, and RNA interference based pest control comprise a truly diverse technology portfolio that spans insect, fungal, bacterial and nematode pests on the majority of crops. The EU's 2030 Farm to Fork goal of 50% lower chemical pesticide use, and the rising phase-out schedule of active ingredients in California, as well as the prospect of expanding certification programs including organic and free of pesticide residues, are driving commercial interest in biopesticide substitutes faster than innovation priorities can adapt to change within the crop protection industry.

FIFRA Section 33 established an accelerated registration review process for biopesticides, allowing for successful registrations in one year or less, as opposed to the 3 year timeline common with standard registration reviews at EPA. The European Commission's Farm to Fork Strategy sets ambitious targets to halve chemical pesticide use and reduce the more hazardous pesticide by 50% by 2030, creating the biggest regulatory demand driver behind biopesticide adoption in European agricultural markets.

Biopesticides Market Size and Forecast

-

Market Size in 2025: USD 10.09 Billion

-

Market Size by 2035: USD 37.9 Billion

-

CAGR: 14.07% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Biopesticides Market - Request Free Sample Report

Biopesticides Market Trends

-

Biocontrol agent discovery through genomic screening of soil microbiome diversity is accelerating the identification of novel Bt strains, entomopathogenic fungi, and antagonistic bacteria with improved efficacy against resistant pest populations.

-

RNA interference (RNAi) biopesticides delivering dsRNA that silences specific pest gene expression are advancing toward commercial deployment for Colorado potato beetle, Western corn rootworm, and varroa mite control applications.

-

Biofungicide adoption in high-value horticulture is growing as zero-residue export market requirements and consumer clean label preferences drive growers toward fungal disease management programs that conventional fungicides cannot serve.

-

Microencapsulation and polymer coating technologies are extending biopesticide field persistence, improving rainfastness, and enabling controlled release profiles that conventional liquid biopesticide formulations could not achieve.

-

Combination products blending biological active ingredients with reduced-risk synthetic pesticides are gaining regulatory and commercial acceptance as a bridge strategy that delivers improved performance while reducing conventional pesticide use intensity.

-

Precision biological pest management using drone application, variable rate technology, and pest monitoring IoT networks is enabling biopesticide application targeting that improves efficacy and reduces total application volume.

-

Biostimulant and biopesticide co-formulation products that simultaneously improve plant resilience and control pests are creating premium product categories that command price premiums justifying development investment.

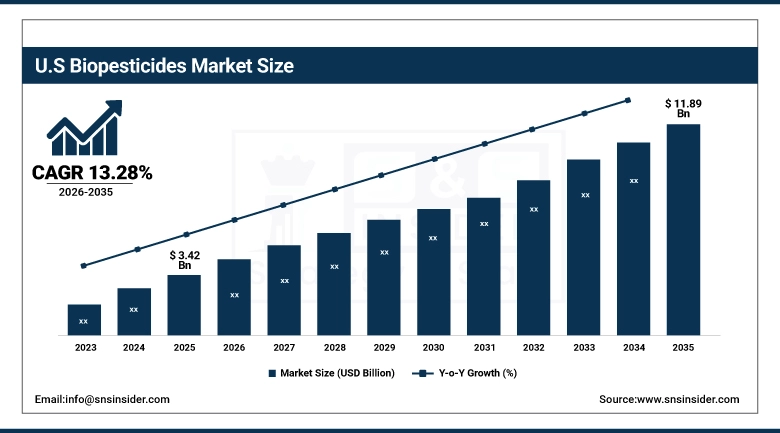

The U.S. Biopesticides Market was valued at USD 3.42 Billion in 2025 and is expected to reach USD 11.89 Billion by 2035, growing at a CAGR of 13.28% from 2026–2035.

The Biopesticides Market is most dominated by North America in the global market space, led by the dominance of the USA owing to having a well-structured domestic organic farming sector, an active EPA biopesticide registration program with fast-tracked biopesticide review timelines, USDA grant programs promoting development of biological crop protection products and a long history of growth in the specialty crop sector almond, grapes, strawberries, leafy vegetables etc. where zero-residue production requirements and easy access to high-premium markets strongly favour the biopesticide economics. Hundreds of U.S. biopesticide technology companies such as Certis Biologicals, Marrone Bio Innovations, Valent BioSciences have created commercially relevant product pipelines across bioinsecticides, biofungicides, and bionematicides, which are marketed through decades-old distribution systems utilized by thousands of organic and conventional growers. The National Organic Program (NOP) rules of the USDA compel organic produce to be given as organic, so as to draw in the need of those clients who are worried about their wellbeing and their states of the planet, as it were, the NOP rules in absence of other assessment are focused on driving a mechanized biopesticide market area that works to guarantee that there remains a steady groundwork for the interest of the biopesticides regardless of whether tipping point or a tendency to receive biopesticides in agribusiness decays.

The U.S. Environmental Protection Agency, which has become the world leader for biopesticides, says it has registered 400+ biopesticide active ingredients and 1,400+ biopesticide product registrations, more than all countries combined. In 2025, U.S. certified organic land totaled over 5.5 million acres, and the USDA Economic Research Service documents that every increase in organic acreage creates more demand for biopesticide products.

Biopesticides Market Segment Analysis

-

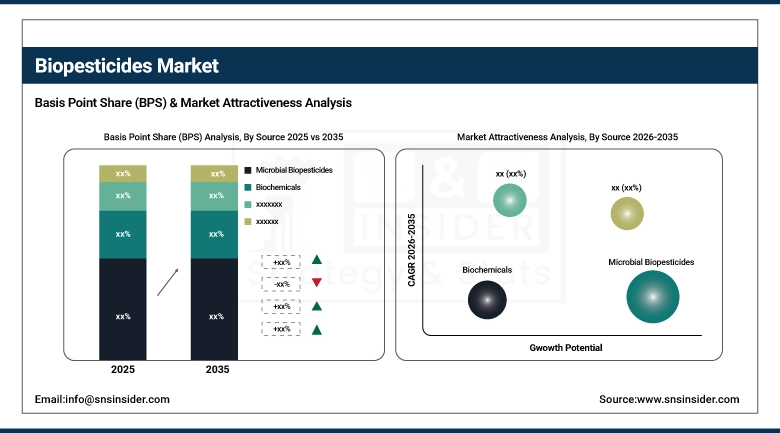

By Source, Microbial Biopesticides dominated with 65.2% share in 2025; Biochemicals and PIPs growing steadily.

-

By Type, Bioinsecticides dominated the Biopesticides Market in 2025; Biofungicides fastest growing (CAGR).

-

By Crop Type, Fruits & Vegetables dominated the Biopesticides Market in 2025; Cereals & Grains growing fastest in absolute volume terms.

By Source, Microbial Biopesticides segment dominates the Biopesticides Market, Biochemicals growing steadily

In 2025, the Biopesticides Market was dominated by Microbial Biopesticides, accounting for around 65.2% share of total revenue. This leadership exemplifies the commercial readiness and broad product application portfolio developed by data related to the collections of organisms, primarily Bacillus thuringiensis, Beauveria bassiana, Metarhizium anisopliae, Trichoderma species, Bacillus subtilis, through decades of agricultural deployment. Bt products are registered for control of various caterpillar and some beetle larva types on several hundred crop types around the world and are among the most used insecticides in organic production systems. Fungal agents causing disease in insects (i.e., entomopathogenic fungi) are important biocontrol agents used for whitefly, thrips, aphid, and other insect pests targeted in horticultural production, where their inherent contact and systemic modes of action can complement the horticultural production cultural and chemical pest management program. The commercial aspect of the microbial segment denotes both the technical diversity of the available organisms and the fact that major agricultural markets are at ease with their biosafety status.

Biochemical biopesticides These are naturally occurring compounds such as insect pheromones, plant extracts and fatty acid-based products, composing a burgeoning class with specific prominence in mating disruption and specialized pest management implementations. This represents a regulatory category called plant-incorporated protectants (PIPs), where the pesticide active ingredient is produced by recombinant plant material itself, and includes Bt transgenic crops and is growing with the introduction of insect resistant biotech crop varieties in new geographic markets and crop species.

By Type, Bioinsecticides dominate the Biopesticides Market, Biofungicides expected to grow fastest

Bioinsecticides retained the dominant type in Biopesticides Market in the 2025, bolstered by the diverse applicability of Bt-based products and entomopathogenic fungi across hundreds of crop and pest combinations, the length of commercial history that has built farmer familiarity and regulatory comfort with biological insect control, and the intensity of regulatory pressure on synthetic insecticides—driving substitution towards biological alternatives, particularly neonicotinoids and organophosphates. This biopesticide category supports the highest potential use base of any biopesticide class, supporting high sales volumes across diverse farming systems at the same time, because these bioinsecticide products can be registered for either organic and/or conventional production systems.

The type with the highest rate of growth is expected to be biofungicides through 2035 supported by the increasing importance of fungal disease management in the commercial production of high-value crops and the particular limitations of synthetic fungicide resistance management addressed by biopesticides. Specific fruit and vegetable fungal pathogens such as gray mold (Botrytis cinerea), powdery mildews, and Fusarium species are rapidly evolving resistance to major fungicide chemical classes, thus accelerating the commercial necessity for resistance management programs, whereas biofungicides derived from Trichoderma, Bacillus subtilis and Coniothyrium minitans provide disease suppression via modes of action that differ from the resistance mechanism employed by the synthetic fungicides.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

France |

22% |

|

Asia Pacific |

China |

50% |

|

Middle East & Africa |

South Africa |

35% |

|

Latin America |

Brazil |

52% |

North America Biopesticides Market Insights

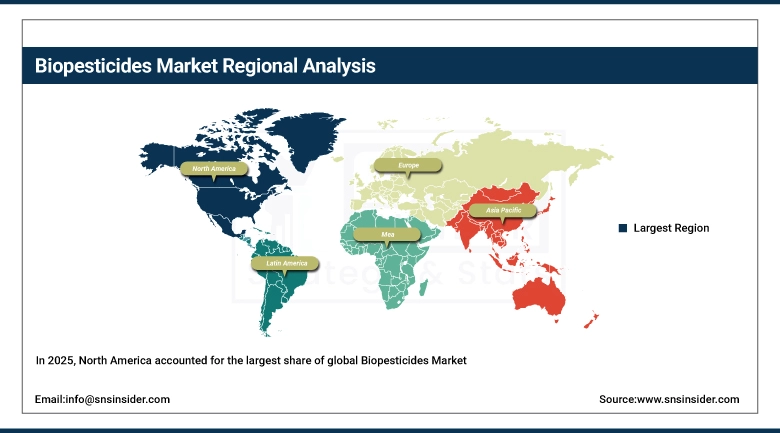

In 2025, North America accounted for the largest share of global Biopesticides Market revenues, driven by the U.S., the largest organic farming sector in the world; favorable biopesticide regulation, with a fast review process; a commercially mature biopesticide supplier ecosystem; and growing retailer demand for biopesticide-based practices. The U.S. specialty crop sector especially the California almond, grape, strawberry and leafy vegetable industries hold the highest value, lower costs for biopesticides and several other biopesticide markets with growth potential worldwide where premium-priced crops support higher biopesticide prices and buyers require clean labels and reduce residue profiles, creating pull-through demand. There is also a growing demand for biopesticides in the U.S. commodity crop production corn, soybeans, cotton sector which has been traditionally dominated in biological products use where the technology has been more skewed towards specialty crop sector.

In the last ten years, California's Department of Pesticide Regulation (CDPR) has cancelled registrations for numerous synthetic active ingredients, thus directly resulting in the mandatory replacement of these pesticides with biopesticide across the more than USD 20 billion annual production of California specialty crops. Biological control agents have been released for over 30 classical biocontrol program by USDA's Agricultural Research Service since 2015, and the commercial biopesticide market has expanded through R&D at government research programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Biopesticides Market Insights

The global Biopesticides Market in Europe is the leading regional market in terms of growth. Early adopters are mainly European growers of wine grapes, stone fruit, vegetables and other specialty crops, where market access requirements for residue-free produce imported to sensitive markets creates the price premium that allows the economics of the biopesticide to work. Wherever synthetic alternatives have been cancelled, systematic biopesticide adoption is engendered by the reduced number of active ingredients approved by the positive list of the EU and reviewed under the Regulation EC over the last 20 years.

The EU's Regulation on sustainable use of plant protection products (SUR) implementation is progressively restricting the use of synthetic pesticides across European agricultural landscapes, impacting horticulture production with a heavy reliance on fungicides and insecticides for which synthetic alternatives are withdrawn. Since 2020, more than 30 microbial biopesticide active substances have been approved in Europe under accelerated evaluation procedures aimed at enabling implementation of the Farm to Fork Strategy.

Asia Pacific Biopesticides Market Insights

Asia Pacific currently is the fastest growing Biopesticides Market and the major four national markets of the Biopesticides Market– China, India, Japan, and Australia– have been at different stages of adoption. China leads the world in pesticide production and is investing heavily in development of domestic biopesticide production as part of its crop sustainability strategy. Thus, the largest number of certified organic farmers in the world coming from India represent a substantial base-demand for biopesticide. Japan promotes a premium agriculture sector, with low levels of maximum acceptable residues for domestic and exported produce, and Japanese growers also are known for their high biopesticide adoption. Biopesticide application is gradually increasing in Australian horticulture and broadacre cropping, with the development of integrated pest management programmes in both systems promoting wider use across the Australia's major export agriculture production.

Under India's National Mission for Sustainable Agriculture, biopesticides is identified as a priority technology by the Ministry of Agriculture and Farmers' Welfare, with subsidy schemes managing to reduce the cost of certain approved biopesticide products by 25-50% for farmers. China was in a position to speed up its biopesticide review process at home by establishing a unique, expedited registration pathway at the end of 2018 that halved review timelines from the average of 36 months to 18 months in order to get more products into Chinese commercial hands sooner.

Middle East & Africa and Latin America Biopesticides Market Insights

The Middle East & Africa Biopesticides Market is steadily expanding, driven by increasing focus on sustainable agriculture, water scarcity challenges, and the need to enhance crop productivity, with countries such as South Africa, Israel, and the UAE leading adoption in high-value crops and greenhouse farming, supported by government initiatives promoting integrated pest management (IPM) and reduced reliance on chemical pesticides, while international programs are boosting adoption across African nations. Meanwhile, Latin America represents a high-growth region in the Biopesticides Market, led by Brazil, Argentina, and Mexico, where strong export-oriented agriculture and strict residue regulations from North America and Europe are accelerating demand for biopesticides, supported by fast regulatory approvals, widespread IPM adoption, and favorable climatic conditions that enhance the effectiveness of biological crop protection solutions.

Growth Drivers:

Rising organic farming demand and strict synthetic pesticide regulations driving global biopesticide adoption across major agricultural markets

The biopesticide market, in contrast, is being pulled from both sides in a virtuous circle. By means of stringent standards for health and environmental effects in the EU, U.S., and increasingly other large markets, registrations of synthetic pesticides are incrementally cancelled, forcing a broader transformation to organic and biological alternatives across many pest management applications. Consumer demand for residue-free, organically certified and clean-label food products is thereby sending this commercial market signal that will justify the premium on both sales and prices that organic and other specialty growers require in order to pay the individually higher per-hectare cost of biopesticide-based pest management programs. These two forces are structurally aligned in a mutually reinforcing way, as regulatory restriction generates mandatory substitution demand and consumer preference generates voluntary adoption demand, both of which, together, underpin above-market revenue growth across the biopesticide category for the foreseeable future.

According to the Food and Agriculture Organization, implemented effective pest management with biological control can decrease crop losses to pests by 20-40%. According to the Organic Trade Association in its Organic Industry Survey, U.S. organic food and beverage sales topped USD 67 billion in 2023, providing an immediate, long-term, market-driven demand for biopesticide-compliant crop production in the supply chains of this high-value market.

Restraints:

Higher production costs and limited shelf life constraining biopesticide adoption among cost-sensitive smallholder farmers globally

There are genuine commercial barriers which are limiting the faster uptake of biopesticides, particularly in cost-sensitive developing markets. The manufacture of microbial biopesticides necessitates the use of dedicated fermentation facilities, rigorous quality control to maintain biological efficacy and often refrigerated storage and transport infrastructure to maintain product effectiveness from manufacture to farm application. The production and supply chain requirements lead to per-unit costs that are generally 2-4x higher than synthetic pesticide alternatives with the same efficacy for the same target pest, which creates an economic barrier that many smallholder farmers, especially in low-income markets, cannot cross without government subsidization. Microbial products tend to have a shorter shelf life often 1-2 years as opposed to 5+ years for synthetic chemical formulations presenting inventory risk for distributors and retailers servicing seasonal agricultural markets in which precise demand timing is hard to anticipate.

Opportunities:

Government subsidy programs and RNAi biopesticide technology innovation creating significant new biopesticide market growth opportunities

In developing markets with large agricultural sectors, government subsidy and support programs are also becoming the most efficient way of filling the cost gap that inhibits wider biopesticide adoption. Farmers in India, Brazil, China and some African countries receive direct subsidies for purchasing biopesticides through extension programs, input subsidy schemes and government procurement for public pest management programs — generating demand order volumes that allow commercial producers to establish increasingly cheaper production scale. Archer Daniels Midland (ADM) Situational Overview RNAi-based biopesticides are the most technically exciting biological pest control innovation since first commercial introduction of Bt Higher level of pest sapidity than most other biopesticide Higher commercial & regulatory compliance speed due to scope specific design nature, which is regulatory friendly-potentially non-toxic gene silencing products toward living organisms No other sector of pesticides has a similar pathway to company develop lead RNAi products industry is likely to develop providable development programs into commercial availability US & EU.

Recent Developments:

-

2025: BASF launched Velondis, a novel bioinsecticide based on the entomopathogenic fungus Isaria fumosorosea, targeting sucking pests including whitefly, aphids, and thrips in high-value vegetable and ornamental horticulture where conventional insecticide resistance has reduced effective pest control options and zero-residue market access requirements sustain demand for biological alternatives.

-

2025: Marrone Bio Innovations received EPA registration for its RNA interference-based bioinsecticide targeting the Western corn rootworm — one of the most economically damaging corn pests in the U.S. Midwest — marking the first EPA registration of an RNAi-based foliar biopesticide and establishing a regulatory precedent for the entire RNAi biopesticide product class.

-

2026: Corteva Agriscience launched BioPD 2.0, an expanded portfolio of bioinsecticide, biofungicide, and biostimulant combination products specifically designed for integrated biological management programs in European horticulture, developed in direct response to Farm to Fork implementation guidance and the cancellation of conventional active ingredients that previously anchored European vegetable and vine crop protection programs.

Biopesticides Market Key Players

-

BASF SE

-

Bayer AG

-

Syngenta AG (ChemChina)

-

Corteva Agriscience

-

Certis Biologicals LLC

-

Marrone Bio Innovations Inc.

-

Valent BioSciences LLC

-

Bioworks Inc.

-

Koppert Biological Systems

-

Novozymes A/S

-

Isagro S.p.A.

-

Andermatt Biocontrol AG

-

Intrachem Group

-

Plant Health Care plc

-

Seipasa S.A.

-

Lallemand Plant Care

-

Stockton Bio-Agriculture Ltd.

-

CABI (Centre for Agriculture and Bioscience International)

-

Sumitomo Chemical Agro Europe S.A.S.

-

Arysta LifeScience (UPL Ltd.)

Biopesticides Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.09 Billion |

| Market Size by 2035 | USD 37.9 Billion |

| CAGR | CAGR of 14.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Microbial Biopesticides [Bacteria, Fungi, Viruses, Protozoa], Biochemicals [Botanical Extracts, Semiochemicals, Minerals, Others], Plant-Incorporated Protectants (PIPs)) • By Type (Bioinsecticides [Bacillus thuringiensis, Beauveria bassiana, Metarhizium anisopliae, Verticillium lecanii, Nucleopolyhedroviruses (NPV) & Granuloviruses (GV), Others], Biofungicides [Trichoderma spp., Bacillus spp., Pseudomonasspp., Streptomyces spp., Others], Bionematicides [Paecilomyces lilacinus, Bacillus firmus, Pasteuria spp., Others], Bioherbicides [Phytophthora palmivora, Alternaria cassia, Others]) • By Formulation (Liquid, Dry) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Plantation Crops, Turf & Ornamentals, Others) • By Mode of Application (Seed Treatment, Soil Treatment, Foliar Spray, Post-Harvest Treatment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Bayer AG, Syngenta AG (ChemChina), Corteva Agriscience, Certis Biologicals LLC, Marrone Bio Innovations Inc., Valent BioSciences LLC, Bioworks Inc., Koppert Biological Systems, Novozymes A/S, Isagro S.p.A., Andermatt Biocontrol AG, Intrachem Group, Plant Health Care plc, Seipasa S.A., Lallemand Plant Care, Stockton Bio-Agriculture Ltd., CABI (Centre for Agriculture and Bioscience International), Sumitomo Chemical Agro Europe S.A.S., Arysta LifeScience (UPL Ltd.) |

Frequently Asked Questions

Ans: North America dominated the Biopesticides Market in 2025.

Ans: The Biofungicides segment is expected to register the fastest CAGR through 2035.

Ans: The Microbial Biopesticides segment dominated with approximately 65.2% share in 2025.

Ans: The Biopesticides Market was valued at USD 10.09 billion in 2025.

Ans: The Biopesticides Market is expected to grow at a CAGR of 14.07% from 2026 to 2035.

Get in Touch