Insecticides Market Report Scope & Overview:

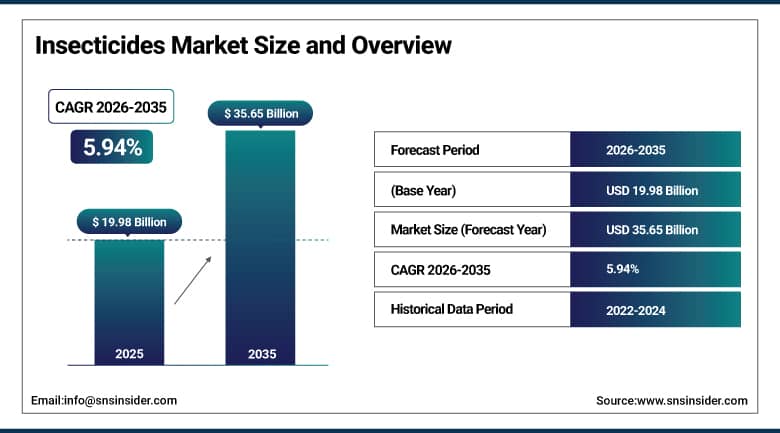

Insecticides Market was valued at USD 19.98 billion in 2025 and is expected to reach USD 35.65 billion by 2035, growing at a CAGR of 5.94% from 2026-2035.

The Insecticides Market is expected to grow due to increased demand for food globally, the requirement for improved agricultural productivity, and higher incidences of pests that affect crop production. The expansion of agriculture businesses and crop protection innovations will also contribute to the market’s growth. The occurrence of pests is also being fueled by climatic changes; thus, there is an increase in the use of insecticides. Another factor that is driving market growth is technological innovation in eco-friendly insecticides and government initiatives encouraging sustainable agriculture.

The U.S. Environmental Protection Agency (EPA) regulates all insecticide registrations under FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act) with mandatory resistance management stewardship requirements. The USDA's National Agricultural Statistics Service reports that U.S. farmers treat approximately 225 million acres with insecticides annually the largest single application area of any pesticide class.

Insecticides Market Size and Forecast

- Market Size in 2025: USD 19.98 Billion

- Market Size by 2035: USD 35.65 Billion

- CAGR: 5.94% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026-2035

- Historical Data: 2022-2024

To Get More Information On Insecticides Market - Request Free Sample Report

Insecticides Market Trends

- Rising need to enhance crop protection and agricultural productivity is driving the insecticides market.

- Growing adoption across agriculture, horticulture, and commercial farming is boosting market growth.

- Expansion of global food demand and pressure on yield optimization is fueling insecticide usage.

- Increasing focus on integrated pest management (IPM) and targeted pest control solutions is shaping adoption trends.

- Advancements in bio-based insecticides, precision spraying, and formulation technologies are improving effectiveness and sustainability.

- Rising concerns over crop damage, pest resistance, and food security are supporting market expansion.

- Collaborations between agrochemical companies, research institutions, and farming communities are accelerating innovation and global adoption.

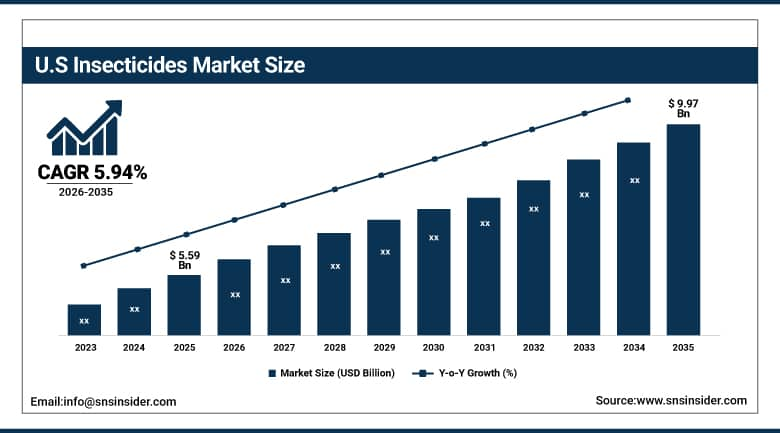

U.S. Insecticides Market was valued at USD 5.59 billion in 2025 and is expected to reach USD 9.97 billion by 2035, growing at a CAGR of 5.94% from 2026-2035.

Insecticides Market Growth in the United States is fueled by growing pest pressures resulting from changing climates, high demand for productive agricultural produce, and increased use of efficient crop protection products. Increased sustainability in agriculture, the use of biodegradable insecticides, and pest management techniques are additional factors aiding in growth.

The USDA's Economic Research Service reports that U.S. crop production losses to insect pests including direct damage and yield drag from pest stress cost American agriculture an estimated USD 15-20 billion annually without insecticide protection. California's Department of Pesticide Regulation maintains one of the world's most stringent state-level insecticide regulatory frameworks, driving adoption of newer, lower-toxicity active ingredients among California specialty crop producers.

Insecticides Market Segment Analysis

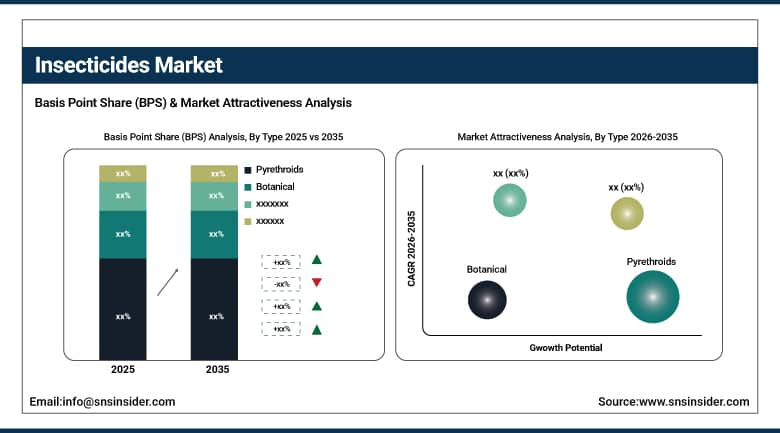

- By Type, Pyrethroids segment dominated the Insecticides Market in 2025 with ~38% share; Botanical segment fastest growing (CAGR).

- By Application, Cereals & Grains segment dominated with ~40% share in 2025; Fruits & Vegetables fastest growing (CAGR).

By Type, Pyrethroids segment dominates the Insecticides Market, Botanicals expected to grow fastest

Pyrethroids dominate the Insecticides Market due to their high efficiency, wide spectrum of pests control, and low toxicity to humans compared with other chemical classes. These chemicals are used extensively in agricultural production to protect essential crops from insect attacks, resulting in increased output. Fast action, stability in sunlight, and low price further encourage their use. Demand for pyrethroids among large farming operations remains high.

The botanical insecticides category is one of the highest growth categories in the Insecticides Market, owing to growing demand for products that are environmentally friendly, non-toxic, and do not leave any residues behind. Made from natural substances obtained from plants, they have gained a lot of popularity in organic farming systems. Growing consumer awareness about eating chemical-free foods, coupled with stringent regulations against chemical pesticides, is boosting their adoption.

By Application, Cereals & Grains segment dominates the Insecticides Market, Fruits & Vegetables segment expected to grow fastest

Cereals and grains held approximately 40% of insecticide market revenue in 2025 a dominance explained by the combination of sheer acreage and the global importance of crops like wheat, rice, corn, and barley. These crops are cultivated in virtually every major agricultural country, creating a geographically diverse and volume-intensive demand base for insect control. Key pests including aphids, armyworms, stem borers, and grain beetles cause direct yield loss and post-harvest storage damage that farmers must protect against to maintain profitability. Government-supported food security programs in India, China, and sub-Saharan Africa often focus specifically on protecting cereal production through recommended insecticide programs, sustaining public sector demand alongside commercial agricultural procurement.

Fruits and vegetables are growing at the fastest application CAGR because they represent the insecticide market segment most directly driven by quality requirements rather than just yield quantity. A blemished apple or a pest-damaged strawberry is commercially worthless at the retail level regardless of its nutritional content, which means the insecticide use standard in horticulture is perfection rather than acceptable loss. The per-hectare insecticide intensity in fruit and vegetable production significantly exceeds field crops, and the expansion of global horticultural trade with fresh produce moving between continents under stringent maximum residue limit requirements is driving investment in newer, lower-residue insecticide chemistries that protect fruit quality while meeting importing country regulatory thresholds.

Insecticides Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

88% |

|

Europe |

France |

22% |

|

Middle East & Africa |

Brazil |

45% |

|

Latin America |

Brazil |

48% |

Asia Pacific Insecticides Market Insights

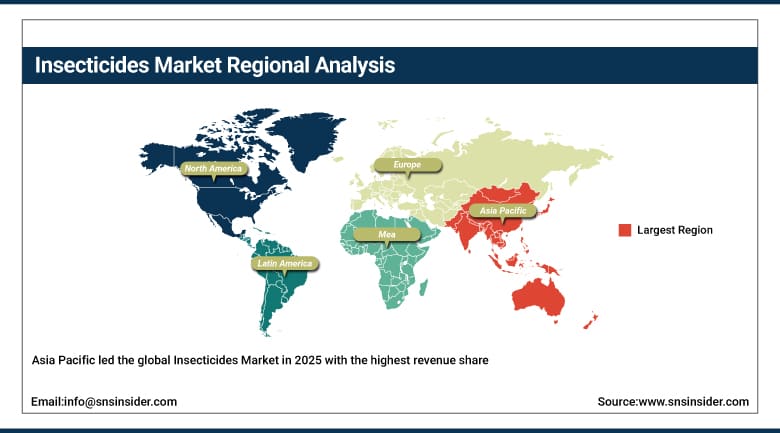

Asia Pacific led the global Insecticides Market in 2025 with the highest revenue share, driven by the region's dominant position in global agricultural production and the high pest pressure associated with tropical and subtropical farming systems. China, India, Japan, and Southeast Asian nations collectively represent the world's largest agricultural production area and face some of its most intense pest management challenges rice brown planthopper, cotton bollworm, fall armyworm, and locust outbreaks create continuous demand for effective insect control. The region's large smallholder farming population creates a high-volume but price-sensitive market that favors established generic chemistries while also showing growing interest in bio-insecticide alternatives supported by government extension programs promoting integrated pest management.

India's Ministry of Agriculture and Farmers' Welfare estimates that pest infestations reduce Indian crop yields by approximately 25% annually, representing one of the strongest structural drivers of insecticide demand in any single national market. China's National Agricultural Technology Extension and Service Center has mandated resistance management rotations across registered insecticide programs for major crops, supporting demand for multiple chemical class options.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Insecticides Market Insights

North America held a significant share in the global Insecticides Market in 2025, driven by the United States' large-scale commercial farming sector and the sophisticated precision agriculture technology that characterizes American crop protection practices. The market is prominent due to large commercial farms, advanced technology in crop cultivation, and government implementing strict guidelines for protecting crops. The USA and Canada generate high demand for pest control solutions given the high vulnerability of key crops like corn, soybeans, and wheat. Corteva Agriscience, FMC Corporation, and Bayer CropScience have strong domestic market positions through their continuous development of innovative insecticide formulations, bio-based, and precision-targeted solutions.

The EPA's registration review program has completed assessment of over 200 insecticide active ingredients since 2006, with use restrictions and cancellations for some organophosphates and neonicotinoids shaping the commercial landscape. The USDA's Pest Management Research Program funds insecticide resistance monitoring and IPM development programs across all major U.S. crop systems.

Europe Insecticides Market Insights

Europe represents a mature but evolving insecticides market where regulatory action has been the dominant market-shaping force for over a decade. The EU's progressive restriction and cancellation of neonicotinoid active ingredients, following scientific assessments of pollinator impacts, has accelerated a market restructuring toward alternative chemistry and biological control methods. France's EcoPhyto program has set ambitious targets for reducing pesticide use nationally, creating structural pressure on insecticide volumes even as the need for effective crop protection remains. European specialty crop production vineyards, orchards, and vegetable production across southern Europe sustains premium insecticide demand where growers can access newer selective products at prices that justify their development cost recovery.

The EU's Farm to Fork Strategy targets a 50% reduction in chemical pesticide use and a 50% reduction in more hazardous pesticide use by 2030 across all EU member states. The European Food Safety Authority (EFSA) has published updated risk assessments for all major insecticide classes under the EU sustainable use of pesticides framework.

Middle East & Africa and Latin America Insecticides Market Insights

Both regions represent growing insecticide markets driven by expanding agricultural production, growing food security ambitions, and the spread of invasive pest species that require urgent chemical control. Brazil is the largest single insecticide market in Latin America and one of the largest in the world, driven by its massive soybean, corn, and sugarcane production sectors where soybean aphid, fall armyworm, and sugarcane borer create intense insecticide demand. Africa's growing adoption of commercial farming practices particularly in Kenya, Ethiopia, Tanzania, and South Africa is creating growing demand for modern insecticide programs as production scale increases and pest management moves beyond traditional practices.

Insecticides Market Growth Drivers:

- Rising global food demand and pest resistance challenges driving sustained agricultural insecticide investment worldwide

The fundamental logic of insecticide market growth is demographic and agronomic simultaneously. More people need more food, and more food requires more crop protection against the insect populations that compete with humans for that production. The FAO's projection that world food production must increase by 70% by 2050 compared to early-2000s levels to feed 9.1 billion people translates directly into sustained demand for all effective crop protection inputs, including insecticides. At the same time, the resistance management challenge is creating its own demand dynamic: as pest populations evolve resistance to established chemistries, farmers need access to new active ingredients that maintain efficacy against resistant populations. That ongoing need drives R&D investment at crop protection companies, creates demand for new product registrations, and sustains the market's volume and value growth simultaneously across both chemical and biological insecticide categories.

FAO estimates that crop losses to pests including insects, weeds, and plant diseases reduce global agricultural production by 20-40% annually. The International Service for the Acquisition of Agri-biotech Applications (ISAAA) reports that effective pest management through combined crop protection approaches generates approximately USD 3 in value per USD 1 invested in crop protection chemicals globally.

Insecticides Market Restraints:

- Increasing regulatory restrictions and growing resistance issues limiting long-term efficacy of established insecticide chemistries

The insecticides market faces a dual structural challenge that creates ongoing headwinds for established chemistry classes. Regulatory pressure particularly in the EU where a precautionary approach to pesticide registration has resulted in the non-renewal of multiple previously approved active ingredients is progressively reducing the available chemistry toolbox for European farmers. Each regulatory restriction narrows the options available for resistance management rotation, which paradoxically accelerates resistance development in the remaining approved chemistry classes. High costs of developing new bio-based and advanced formulations bio-insecticide development programs require 7-10 years and significant investment before product registration create barriers that slow the rate at which new alternatives can replace restricted products.

Insecticides Market Opportunities:

- Bio-based insecticides and precision agriculture integration creating new sustainable growth opportunities in global markets

The growing acceptance of bio-insecticides both in regulatory frameworks and in farmer practice represents the clearest opportunity for sustained market growth at premium price points. Biological insecticides based on entomopathogenic microorganisms, insect-parasitic nematodes, RNA interference technology, and pheromone-based mating disruption systems are each maturing toward commercial scale deployment that was not achievable five years ago. Regulatory accelerated review pathways for reduced-risk biopesticides in the U.S. under FIFRA Section 25(b) and equivalent provisions in the EU and Australia are reducing time-to-market for biological products. The integration of insecticide applications with precision agriculture platforms using AI pest monitoring to trigger applications only when economic threshold pest densities are confirmed creates a commercial use case for premium-priced selective insecticides where efficacy and environmental compatibility justify higher product costs.

Recent Developments:

- 2025: BASF launched Inscalis, a new aphicide based on the novel active ingredient afidopyropen, providing effective control of aphid species including those resistant to established neonicotinoid and pyrethroid insecticides, with rapid systemic uptake and a favorable environmental profile that meets EU registration requirements for use in canola and cereal crops.

- 2025: Corteva Agriscience expanded commercial availability of its Isoclast Active (sulfoxaflor) insecticide in key Asian markets following successful registration approvals, targeting sucking pest management in rice, vegetables, and fruit crops where neonicotinoid restrictions have created unmet pest control needs for growers.

- 2026: Syngenta launched its biological insecticide Mainspring (cyantraniliprole) in a new microencapsulated formulation that extends residual activity by 30% compared to the standard formulation, targeting high-value vegetable and berry growers who require extended protection windows between spray applications to reduce labor costs.

Insecticides Market Key Players

Some of the Insecticides Market Companies

- AMVAC Chemical Corp.

- UPL Ltd.

- Bayer AG

- BASF SE

- FMC Corp.

- Corteva Agriscience

- Nufarm Ltd.

- Bioworks, Inc.

- Syngenta Group

- Sumitomo Chemical

- Adama Agricultural Solutions

- Valent BioSciences

- Mitsui Chemicals Agro, Inc.

- Gowan Company

- Nippon Soda Co., Ltd.

- Helm AG

- Isagro S.p.A.

- Rotam Global AgroSciences

- Rallis India Ltd.

- PI Industries Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.98 Billion |

| Market Size by 2035 | USD 35.65 Billion |

| CAGR | CAGR of 5.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pyrethroids, Organophosphates, Carbamates, Chlorinated Hydrocarbons, Botanical, Others) • By Application, (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AMVAC Chemical Corp., UPL Ltd., Bayer AG, BASF SE, FMC Corp., Corteva Agriscience, Nufarm Ltd., Bioworks, Inc., Syngenta Group, Sumitomo Chemical, Adama Agricultural Solutions, Valent BioSciences, Mitsui Chemicals Agro, Inc., Gowan Company, Nippon Soda Co., Ltd., Helm AG, Isagro S.p.A., Rotam Global AgroSciences, Rallis India Ltd., PI Industries Ltd.. |

Frequently Asked Questions

The Insecticides Market was valued at USD 19.98 billion in 2025.

The Insecticides Market is expected to grow at a CAGR of 5.94% from 2026 to 2035.

The Fruits & Vegetables segment is expected to register the fastest CAGR through 2035.

Increasing agricultural productivity needs which drive market growth.

Asia Pacific dominated the Insecticides Market in 2025.

Get in Touch