Bunker Fuel Market Report Scope & Overview:

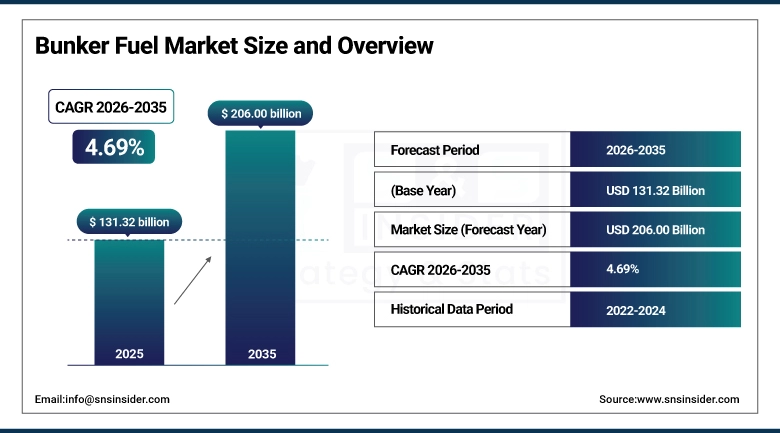

The Bunker Fuel Market was valued at USD 131.32 billion in 2025 and is expected to reach USD 206.00 billion by 2035, growing at a CAGR of 4.69% from 2026-2035.

The growth of the Bunker Fuel Market is due to the increase in international maritime trade, fleet size, and growth in containers, tankers, and bulk ships. Environmental regulations have also contributed to the growth of the Bunker Fuel Market, as the use of low sulfur and clean fuels has increased. Moreover, investments in port infrastructure and the development of fuel technology have contributed to the growth of the Bunker Fuel Market.

According to UN Trade, global seaborne trade volume reached about 12,720 million tonnes in 2024, marking continued moderate growth over prior years. This expansion reflects rising trade in containerized goods and bulk commodities, which directly supports demand for bunker fuel used by oceangoing vessels.

Bunker Fuel Market Size and Growth Forecast:

-

Bunker Fuel Market Size in 2025: USD 131.32 Billion

-

Bunker Fuel Market Size by 2035: USD 206.00 Billion

-

CAGR: 4.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Bunker Fuel Market - Request Free Sample Report

Bunker Fuel Market Trends

-

Rising global shipping activities and maritime trade are driving the bunker fuel market.

-

Growing demand for marine fuel in cargo ships, tankers, and container vessels is boosting market growth.

-

Expansion of international shipping routes and fleet sizes is fueling fuel consumption.

-

Increasing focus on compliance with IMO regulations and sulfur emission limits is shaping adoption trends.

-

Advancements in low-sulfur fuels, LNG bunkering, and alternative marine fuels are enhancing sustainability.

-

Rising crude oil production and fluctuations in oil prices are supporting market expansion.

-

Collaborations between shipping companies, fuel suppliers, and port authorities are accelerating innovation and global adoption.

U.S. Bunker Fuel Market Size Outlook:

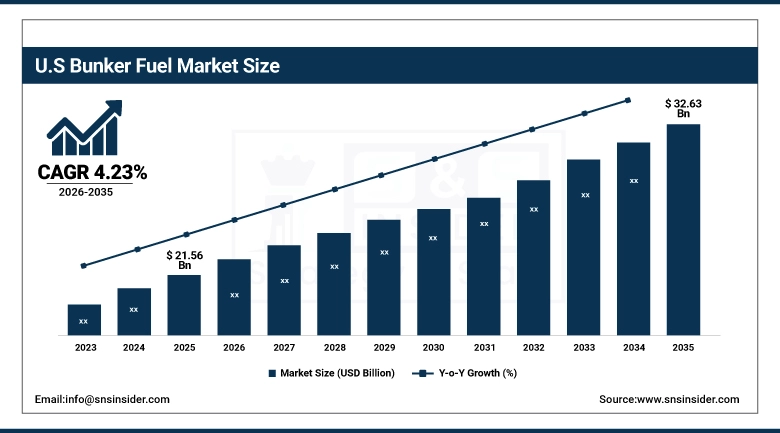

The U.S. Bunker Fuel Market was valued at USD 21.56 billion in 2025 and is expected to reach USD 32.63 billion by 2035, growing at a CAGR of 4.23% from 2026-2035. U.S. Bunker Fuel Market growth is driven by the rising trade activities, advanced infrastructure facilities in ports, expansion of the fleet size, and adherence to environmental norms, thus fueling the demand for low-sulfur and efficient fuels for container ships, tankers, and bulkers.

Bunker Fuel Market Growth Drivers:

-

Increasing global maritime trade is driving higher demand for bunker fuels across shipping fleets worldwide consistently over the past decade

Increase in international ship operations and trade route expansion have led to an increase in bunker fuel demand. Containers, tankers, and bulk cargo vessels need large quantities of bunker fuels for long voyages. Increase in import-export operations in emerging economies is adding fuel to the fire. E-commerce operations have increased the demand for bunker fuels. Upgrading trade infrastructures is resulting in the use of large vessels, which need higher quantities of bunker fuels. Shipping companies are investing heavily in reliable bunker fuel procurement systems, thereby ensuring continuous operations. This is directly contributing to the growth of the bunker fuel market, resulting in high revenue generation.

Bunker Fuel Market Restraints:

-

Volatile crude oil prices and supply chain disruptions are limiting consistent bunker fuel supply globally across multiple fleets

The fluctuating crude oil prices cause uncertainties in the prices of bunker fuels. This has a significant effect on the budget of shipping operators. A sudden rise in prices can cause inefficiency in the consumption of oil fuels. In addition, there are issues in the supply of IFO 380, IFO 180, and MGO/MDO fuels. This is because of supply chain issues, geopolitical issues, and refinery shutdowns. Inconsistency in the refueling infrastructure at ports also contributes to the constraints in the supply of fuels. This has made it challenging for small distributors to maintain consistency in the supply of fuels. This has resulted in restraining the growth of the oil fuels market by introducing uncertainties in the supply and prices of oil fuels.

Bunker Fuel Market Opportunities:

-

Expansion of alternative fuels and low-sulfur fuel solutions is creating significant revenue opportunities in bunker fuel market globally

With increased environmental awareness and stringent emission regulations, opportunities have emerged for suppliers to develop their services in terms of low-sulfur fuels and clean forms of energy. Diversification can be achieved for companies by incorporating biofuels, LNG bunkering services, and hybrid fuels. Technology can play a vital role in improving the overall value proposition for suppliers in terms of fuel blending technology, storage optimization, and supply chain management. Working in collaboration with shipping companies on sustainable fuels can open doors for recurring revenue streams. With increasing demand for fuels in emerging countries such as those in the Asia-Pacific region, opportunities are available for expanding supplier networks.

The International Maritime Organization (IMO) mandated the IMO 2020 sulfur cap, reducing globally permitted sulfur in marine fuels from 3.5 % to 0.5 %, forcing a shift toward low‑sulfur bunker fuels such as VLSFO and MGO.

Bunker Fuel Market Segment Highlights

-

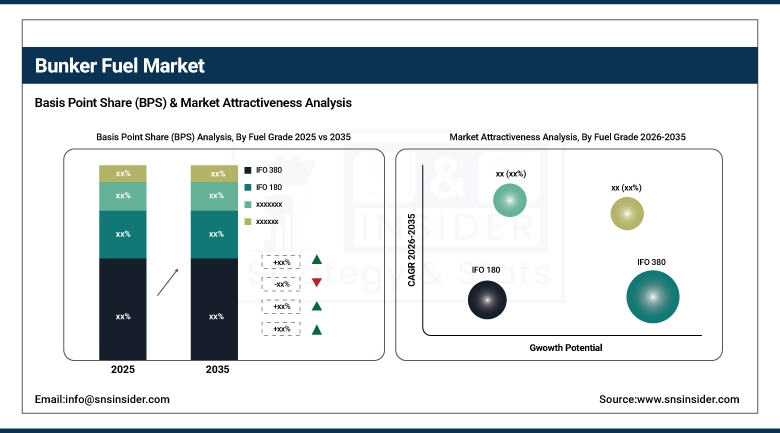

By Fuel Grade, IFO 380 dominated the Bunker Fuel Market with ~34% share in 2025; MGO/MDO fastest growing (CAGR).

-

By End User, Container Fleet dominated the Bunker Fuel Market with ~40% share in 2025; Tanker Fleet fastest growing (CAGR).

-

By Seller Type, Major Oil Company dominated the Bunker Fuel Market with ~46% share in 2025; Large Independent Distributors fastest growing (CAGR).

By Fuel Grade, IFO 380 segment dominates the Bunker Fuel Market, MGO/MDO segment expected to grow fastest

IFO 380 segment held the highest revenue share in the Bunker Fuel Market in 2025. This is because IFO 380 is highly available, cheaper, and best used by large vessels for long-distance voyages. Its high energy content and compatibility with ship engines make IFO 380 the best choice for large fleets of ships.

The MGO/MDO segment is anticipated to show the highest CAGR from 2026-2035. This is because of the implementation of sulfur emission regulations and environmental compliance. Shipping firms are opting for low sulfur fuels for their vessels in order to comply with the IMO 2020 regulations. Technology has made MGO/MDO fuels more accessible for small vessels.

By End User, Container Fleet segment dominates the Bunker Fuel Market, Tanker Fleet segment expected to grow fastest

The Container Fleet segment holds the largest market share in the Bunker Fuel Market in terms of revenue in 2025. The large-scale operations of container fleets across the globe contribute significantly to the demand for bunker fuels. The frequent port calls of these fleets over international routes require large quantities of fuel oil for their operations.

Tanker Fleet segment is expected to register the highest CAGR during 2026-2035. This is due to the increasing demand for crude oil and petroleum products. Large-scale operations for meeting global energy requirements demand high quantities of compliant fuels for long-haul routes. This factor is driving the adoption of advanced fuels such as MGO/MDO for tanker fleets.

By Seller Type, Major Oil Company segment dominates the Bunker Fuel Market, Large Independent Distributors segment expected to grow fastest

Major Oil Company segment has the largest share in the Bunker Fuel Market in terms of revenue in 2025. This is because they have large production capacity and distribution networks. They have already established contracts with the shipping lines. They can provide competitive prices and quality assurance. So, they maintain dominance over the independent distributors in the bunker fuel market.

The Large Independent Distributors Segment is expected to have the highest CAGR in terms of market growth during the period 2026-2035. This is due to their flexibility in sourcing low sulfur fuels or specialty fuels. They can easily adapt to changes in regional regulations and can service smaller fleets compared to major oil companies.

Bunker Fuel Market Regional Analysis

Asia Pacific Bunker Fuel Market Insights

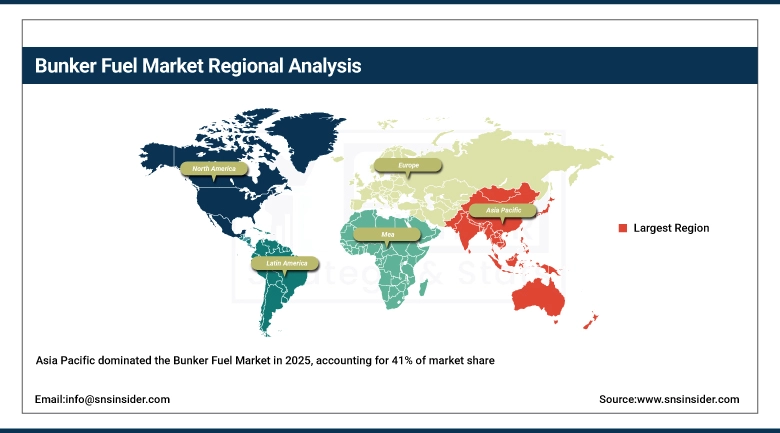

Asia Pacific held the highest share in the Bunker Fuel Market in terms of revenue at 41% in 2025, owing to the presence of major shipping centers, developing infrastructure in ports, and high trade volumes. Countries like China, Singapore, and Japan have high trade volumes in terms of container vessels, oil tankers, and bulk carriers, thus increasing the demand for bunker fuels. With the rise in industrialization and trade volumes, along with its strategic location for trade, Asia Pacific is the leading bunker fuels market across the globe.

Get Customized Report as per Your Business Requirement - Enquiry Now

Middle East & Africa Bunker Fuel Market Insights

The Middle East & Africa segment is anticipated to have the highest CAGR of 7.70% from 2026-2035 due to increasing investments in modernization of ports, growing exports of oil, and increasing shipping activities. Trade connectivity, strategic shipping routes, and the need for cleaner fuels like low sulfur content fuels are also accelerating the growth of the Middle East & Africa market. In addition, there are increasing supply chain networks from regional players and independent distributors, thus increasing the growth rate of bunker fuels in the Middle East & Africa market.

Europe Bunker Fuel Market Insights

Europe in the Bunker Fuel Market has stringent environmental policies and advanced port infrastructure. The region has high demand for low-sulfur fuel. Major ports such as Rotterdam, Hamburg, and Antwerp help in the high fuel consumption of container ships, tankers, and bulkers. The emphasis on clean fuel and the implementation of IMO 2020 regulations and the use of smart port technologies help in the steady growth of the bunker fuel market in the region.

North America Bunker Fuel Market Insights

The Bunker Fuel market in North America is fueled by the large shipping activities carried out in the U.S. and Canadian waters with the support of key ports such as Los Angeles, Houston, and Vancouver. The market in the region is focused on the implementation of environmental regulations with the adoption of low-sulfur fuels. The import-export activities in the region, along with the presence of key oil companies, contribute significantly towards the demand for bunker fuels in the market.

Latin America Bunker Fuel Market Insights

Latin America in the Bunker Fuel Market has been observing steady growth in the region because of the expansion in port infrastructure and the increase in trade activities. Key ports in the region include Santos, Buenos Aires, and Veracruz. These ports facilitate the operations of container ships, tankers, and bulkers. The increase in the demand for low-sulfur fuels and the expansion in the export of oil products and the development of logistics in the region contribute to the growth of the market.

Bunker Fuel Market Competitive Landscape:

Exxon Mobil Corporation

Exxon Mobil Corporation is a global energy corporation based in Irving, Texas, USA. The corporation specializes in oil, gas, and petrochemical production. In terms of the marine fuels business segment, ExxonMobil aims to supply conventional and low emission bunker fuels, including biofuel blends, to support the decarbonization of shipping and develop new environmental regulations. ExxonMobil relies on research and development activities as well as operational trials to develop fuels for better performance and greenhouse gas emissions reduction.

-

2026: ExxonMobil completed a successful sea trial of its first marine bio fuel oil with Stena Bulk in Rotterdam, demonstrating a potential 40% CO₂ emissions reduction versus conventional marine fuel in real vessel operations.

-

2025: ExxonMobil emphasized strategic support for low‑emission marine bunker fuels (including bio blends) and expanded fuel supply capabilities across global bunkering ports.

Bunker Fuel Companies are:

-

BP Plc

-

Royal Dutch Shell Plc

-

TotalEnergies SE

-

Chevron Corporation

-

Gazpromneft Marine Bunker LLC

-

Bunker Holding

-

KPI OceanConnect

-

Peninsula Petroleum

-

Cockett Marine Oil

-

Glencore

-

Trafigura

-

Vitol

-

Mercuria Energy Group

-

Aegean Marine Petroleum Network

-

Chemoil

-

Sentek Marine

-

Minerva Bunkering

-

GAC Bunker Fuels

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 131.32 Billion |

| Market Size by 2035 | USD 206.00 Billion |

| CAGR | CAGR of 4.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fuel Grade (IFO 380, IFO 180, MGO/MDO, Other IFO) • By Seller Type (Major Oil Company, Large Independent Distributors, Small Independent Distributors) • By End User (Container Fleet, Tanker Fleet, Bulk and General Cargo Fleet, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Exxon Mobil Corporation, BP Plc, Royal Dutch Shell Plc, TotalEnergies SE, Chevron Corporation, Gazpromneft Marine Bunker LLC, World Kinect Corporation, Bunker Holding, KPI OceanConnect, Peninsula Petroleum, Cockett Marine Oil, Glencore, Trafigura, Vitol, Mercuria Energy Group, Aegean Marine Petroleum Network, Chemoil, Sentek Marine, Minerva Bunkering, GAC Bunker Fuels. |

Frequently Asked Questions

Asia Pacific dominated the Bunker Fuel Market in 2025.

The Major Oil Company segment dominated the Bunker Fuel Market in 2025.

Increasing global maritime trade is driving higher demand for bunker fuels across shipping fleets worldwide consistently over the past decade.

The Bunker Fuel Market was valued at USD 131.32 billion in 2025.

The Bunker Fuel Market is expected to grow at a CAGR of 4.69% from 2026 to 2035.

Get in Touch